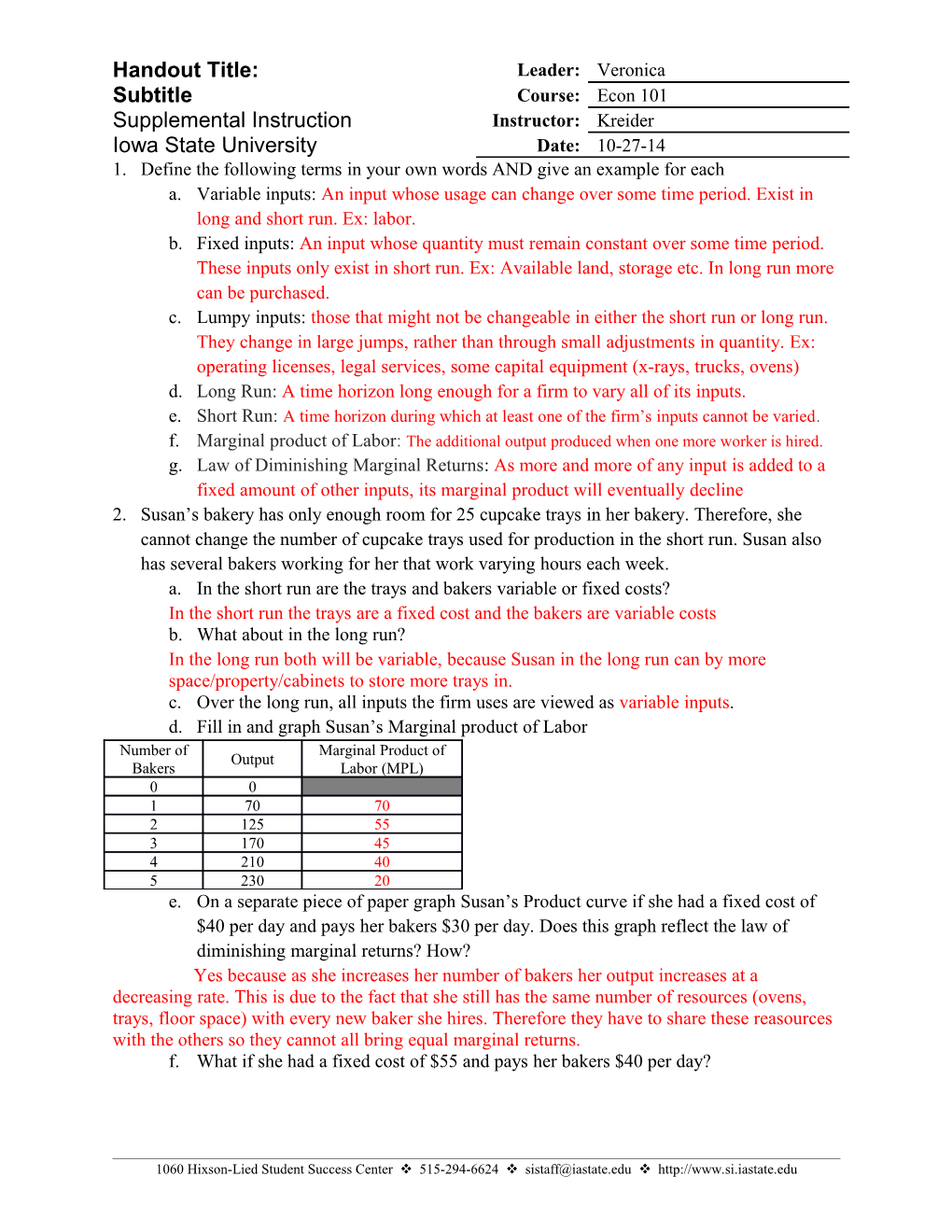

Handout Title: Leader: Veronica Subtitle Course: Econ 101 Supplemental Instruction Instructor: Kreider Iowa State University Date: 10-27-14 1. Define the following terms in your own words AND give an example for each a. Variable inputs: An input whose usage can change over some time period. Exist in long and short run. Ex: labor. b. Fixed inputs: An input whose quantity must remain constant over some time period. These inputs only exist in short run. Ex: Available land, storage etc. In long run more can be purchased. c. Lumpy inputs: those that might not be changeable in either the short run or long run. They change in large jumps, rather than through small adjustments in quantity. Ex: operating licenses, legal services, some capital equipment (x-rays, trucks, ovens) d. Long Run: A time horizon long enough for a firm to vary all of its inputs. e. Short Run: A time horizon during which at least one of the firm’s inputs cannot be varied. f. Marginal product of Labor: The additional output produced when one more worker is hired. g. Law of Diminishing Marginal Returns: As more and more of any input is added to a fixed amount of other inputs, its marginal product will eventually decline 2. Susan’s bakery has only enough room for 25 cupcake trays in her bakery. Therefore, she cannot change the number of cupcake trays used for production in the short run. Susan also has several bakers working for her that work varying hours each week. a. In the short run are the trays and bakers variable or fixed costs? In the short run the trays are a fixed cost and the bakers are variable costs b. What about in the long run? In the long run both will be variable, because Susan in the long run can by more space/property/cabinets to store more trays in. c. Over the long run, all inputs the firm uses are viewed as variable inputs. d. Fill in and graph Susan’s Marginal product of Labor Number of Marginal Product of Output Bakers Labor (MPL) 0 0 1 70 70 2 125 55 3 170 45 4 210 40 5 230 20 e. On a separate piece of paper graph Susan’s Product curve if she had a fixed cost of $40 per day and pays her bakers $30 per day. Does this graph reflect the law of diminishing marginal returns? How? Yes because as she increases her number of bakers her output increases at a decreasing rate. This is due to the fact that she still has the same number of resources (ovens, trays, floor space) with every new baker she hires. Therefore they have to share these reasources with the others so they cannot all bring equal marginal returns. f. What if she had a fixed cost of $55 and pays her bakers $40 per day?

1060 Hixson-Lied Student Success Center v 515-294-6624 v [email protected] v http://www.si.iastate.edu g. What if she had no fixed cost and hires bakers of different skill levels. Therefore she pays the first one $50 a day, the second and third $40 a day, the fourth $30 a day, and the fifth $25 a day?