Revenue = Units Sold * Unit Price

Total Costs = Variable Costs + Fixed Costs

Fixed Costs are not dependent upon units sold. The fixed costs will be a “flat fee”.

Variable Costs will be the Cost required to produce A UNIT multiplied by the number of units produced/sold.

Profit = Revenue – Costs

The Break Even Point can be defined in two ways:

1) The point at which our Revenue equals our Costs 2) The point at which the Profit is zero.

To find the break – even point, we can use our profit equation and solve for Profit = 0.

Or, we can graph both our Cost, and revenue equations, and see where they intersect.

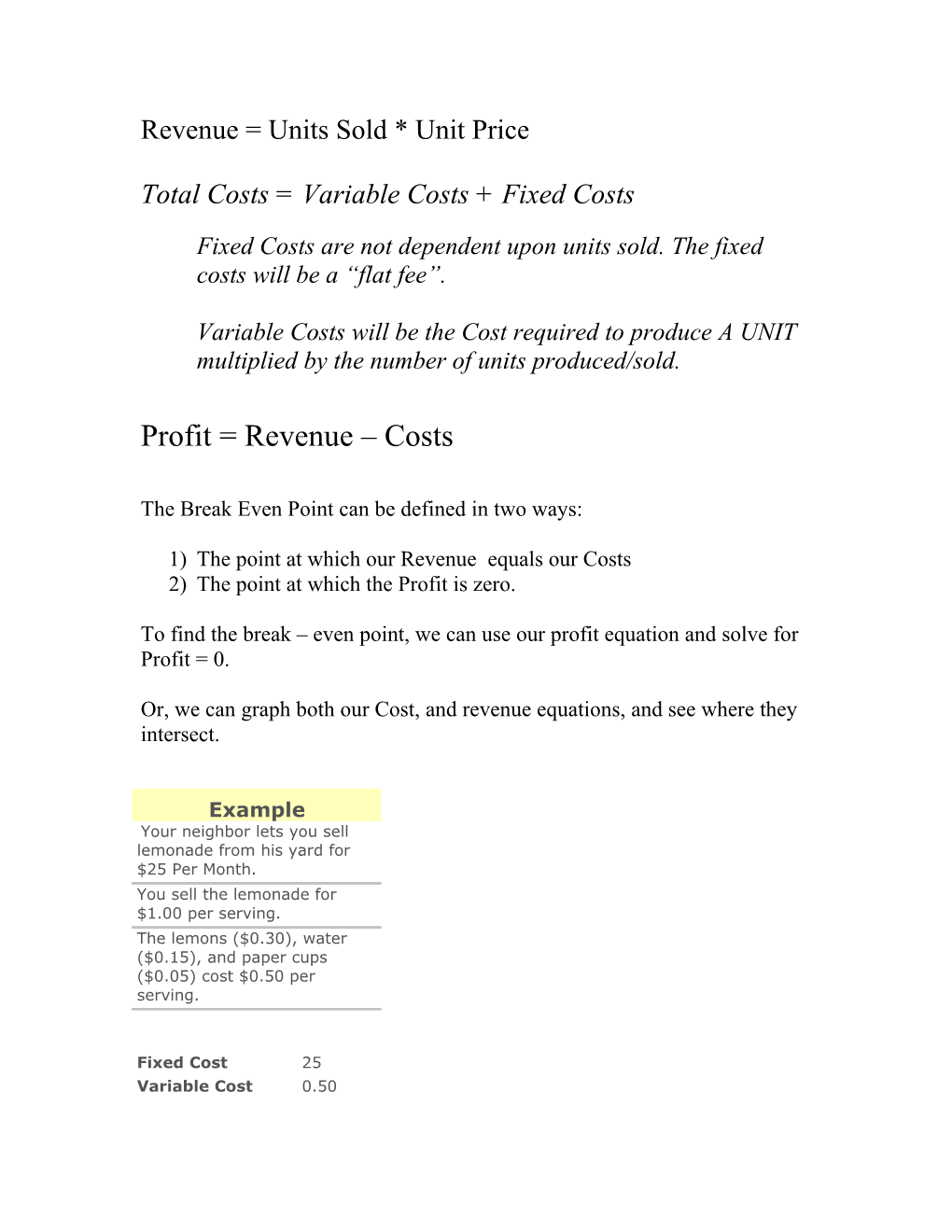

Example Your neighbor lets you sell lemonade from his yard for $25 Per Month. You sell the lemonade for $1.00 per serving. The lemons ($0.30), water ($0.15), and paper cups ($0.05) cost $0.50 per serving.

Fixed Cost 25 Variable Cost 0.50 Selling Price 1.00 Time Period Monthly

1. A local livestock producer utilizes compost waste to develop an organic fertilizer product. The fertilizer is prepared for retail sale in 50 pound bags. The retail sales price is $5.00 per bag. The average variable cost per bag is $2.80 and average annual fixed costs are $60,000. What is the break-even sales figure?

2: Sue’s Day Care

Seeing a need for childcare in her community, Sue decided to launch her own daycare service. Her service needed to be affordable, so she decided to watch each child for $12 a day. After doing her homework, Sue came up with the following financial information:

Selling Price (per child per day) – $12.00

Fixed Expenses (per month)

Insurance - 400

Rent - 200

Total Fixed Expenses - 600

Costs of goods sold - $4.00 per unit

Meals Snacks - 2 @ $1.50 (breakfast & lunch) 2 @ $0.50

The month of June has 20 workdays, Monday through Friday for four weeks. How many children will Sue need to take care of just to break-even in her new business? 3: Joe’s T-Shirts

Fill in as much information in this table as you can from the information below the table, then use it to calculate the break-even.

← For the month of June, he sold t-shirts at $10 each.

← He paid $5 for each t-shirt and $.80 per shirt for personalizing art materials.

← He pays $25 a month on his loan for a t-shirt printing machine.

← His monthly phone bill is $35.

← 4. You own a motel with a hundred rooms. Fixed daily cost is $1000 (includes mortgage, staff salaries, maintenance). Variable cost per room is $10 per room per day (includes extra utility cost, room cleanup, etc).

0 a. If you charge $50 per room, what is the breakeven point? (That is, how many rooms must be occupied for you to break even) 1 b. You have the option of subcontracting to improve room quality and the surroundings, but that would increase fixed costs to $1800, with no change to variable costs. You will, however, be able to charge $70 per room per day. What is the new break-even point? Part II Extend the analysis to a larger hotel like the Marriott or Hilton. What aspects of the analysis would change? Case A – Basic break-even point problem

In this simple problem your task is to work out the number of participants required to

Ensure the break-even point.

The data you need to make your calculation is as follows:

← Total Fixed Costs: $10,080

← Variable Cost per Participant: $2.00

← Ticket Price per Participant: $20

Case B – Variation of the basic break-even point problem

This problem is much the same problem as in case A except that you are given the

number of participants and you must work out what is the minimum price that

spectators must be charged.

The data you need to make your calculation is as follows:

← Total Fixed Costs: $10,000

← Variable Cost per Participant: $5.00

← Number of Participants Required: 500