ATRS 10005 04 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

DATE and TIME: Monday June 22, 2020 – 6:30 P.M

Page 1 of 4 MEETING: REGULAR CITY COUNCIL MEETING DATE AND TIME: Monday June 22, 2020 – 6:30 P.M. Zoom Meeting On-Line Here is the public invitation link for this Zoom meeting Webinar ID: 897 7506 0372 Registration Link: https://us02web.zoom.us/webinar/register/WN_RVbbRyivQlmOhVr4YvvmOg I. CALL TO ORDER: This meeting has been given public notice in accordance with the Section 25-19-106 of the Freedom of Information Act, in such form that will apprise the General Public and news media of subject matter that is intended for consideration and action. II. PLEDGE OF ALLEGIANCE; I. ROLL CALL: Mayor Peter Christie, Council Members John Flynn, Linda Lloyd, James Wozniak, Larry Wilms, Doug Fowler and Steven Bourke II. CITIZEN INPUT/PUBLIC APPEARANCES: Please be advised that it is the policy of the municipality that there will be a three (3) minute time limit, per person, with time extension per the Chief Presiding Officer’s discretion. III. COUNCIL REPLY: Council members will have the opportunity to reply to the comments and concerns raised during the Citizen Input period. This will be limited to comments and will not be a discussion period. IV. APPROVAL OF MINUTES: May 18, 2020 Regular Meeting V. REPORTS: Monthly Financial Report April 2020 VI. MOTION TO SUSPEND RULES: and read all proposed Ordinances and Resolutions on the agenda by title only. VII. OLD BUSINESS: 1. ORDINANCE N0- REPEALING AND REPLACING SECTION 4-27 OF THE CODE OF ORDINANCES OF THE CITY OF BELLA VISTA TO ELIMINATE THE DOG LICENSING REQUIREMENT AND TO ENACT A MANDATORY MICROCHIP REQUIREMENT FOR DOGS.(Third Reading) VIII. -

STATE LOCAL EDUCATION AGENCY (ENROLLMENTS > 1250) ENR. 504S RATE CONNECTICUT Newtown School District 4570 710 15.53% TEXAS

As a supplement to the corresponDing Zirkel analysis in the Educa'on Law Reporter, this compilaon, in DescenDing orDer of the percentage of 504-only stuDents, is baseD on the 2015-16 CRDC Data. To obtain the actual complete Data anD to request any correcbons, please go Directly to hdps://ocrData.eD.gov/ STATE LOCAL EDUCATION AGENCY (ENROLLMENTS > 1250) ENR. 504s RATE CONNECTICUT Newtown School District 4570 710 15.53% TEXAS Carrizo Springs Consol. InDep. School District 2254 325 14.41% CONNECTICUT Weston School District 2393 343 14.33% TEXAS Pittsburg InDep. School District 2472 335 13.55% TEXAS Pleasanton InDep. School District 3520 467 13.26% TEXAS Van Alstyne InDep. School District 1336 174 13.02% NEW JERSEY Hanover Park Regional High School District 1561 200 12.81% TEXAS Buna InDep. School District 1456 183 12.56% TEXAS Tatum InDep. School District 1687 208 12.32% TEXAS Crockett InDep. School District 1280 157 12.26% NEW YORK WinDsor Central School District 1697 208 12.25% TEXAS Hughes Springs InDep. School District 1266 153 12.08% TEXAS Pottsboro InDep. School District 4284 507 11.83% TEXAS Lake Dallas InDep. School District 3945 467 11.83% TEXAS NorthsiDe InDep. School District 105049 12425 11.82% TEXAS Kerrville InDep. School District 5038 592 11.75% TEXAS Gatesville InDep. School District 2853 335 11.74% TEXAS GoDley InDep. School District 1780 205 11.51% PENNSYLVANIA WallingforD-Swarthmore School District 3561 401 11.26% GEORGIA Wilkinson County Schools 1523 169 11.09% LOUISIANA Terrebonne Parish School District 18445 2039 11.05% NEW YORK Briarcliff Manor Union Free School District 1469 162 11.02% WASHINGTON Mercer IslanD School District 4423 485 10.96% TEXAS Community InDep. -

Needs Improvement Priority Schools Arkansas Was Required to Identify A

Needs Improvement Priority Schools Arkansas was required to identify a number of lowest-performing schools equal to at least five percent of the state’s Title I schools. Arkansas had 803 Title I schools in 2011, requiring at least 40 Title I schools be identified among the schools identified as Needs Improvement Priority Schools. Arkansas identified 48 schools which included 41 Title I schools. The criteria for identification of Priority Schools set by USDE included identifying schools that were: • Among the lowest five percent of schools in the state based on proficiency and lack of progress of the “All Students” group, or • Title I participating or Title I eligible high schools with graduation rates less than 60% over a number of years, or • Tier I or Tier II SIG schools implementing a school intervention model. An added ranks method was used to identify Needs Improvement Priority Schools. The details of this method are provided on pages 87 – 88 of Arkansas’s approved ESEA Flexibility request. This method was used in previous years to identify the persistently lowest achieving schools under Section 1003(g) of the Elementary and Secondary Schools Act. This method considers the rank of school performance in math and literacy for a three-year period. The three-year average math and literacy performance for Priority Schools ranged from 7.9% of students scoring at or above the Proficient level to 47.7% of students scoring at or above the Proficient level. Interventions for Needs Improvement Priority Schools are detailed on pages 88 – 96 of Arkansas’s approved ESEA Flexibility request. -

Schools and Libraries 1Q2014 Funding Year 2013 Commitments - 3Q2013 Page 1 of 136

Universal Service Administrative Company Appendix SL35 Schools and Libraries 1Q2014 Funding Year 2013 Commitments - 3Q2013 Page 1 of 136 Applicant Name City State Committed ABERDEEN SCHOOL DISTRICT 6-1 ABERDEEN SD 32,793.60 ABERNATHY INDEP SCHOOL DIST ABERNATHY TX 19,385.14 ABSECON PUBLIC SCHOOL DISTRICT ABSECON NJ 13,184.40 Academia Bautista de Puerto Nuevo, Inc Rio Piedras PR 59,985.00 ACADEMIA SAN JORGE SAN JUAN PR 45,419.95 ACHIEVE CAREER PREPARATORY ACADEMY TOLEDO OH 19,926.00 ACHILLE INDEP SCHOOL DIST 3 ACHILLE OK 49,099.48 ADA PUBLIC LIBRARY ADA OH 900.00 AF-ELM CITY COLLEGE PREP CHARTER SCHOOL NEW HAVEN CT 31,630.80 AFYA PUBLIC CHARTER MIDDLE BALTIMORE MD 17,442.00 ALBANY CARNEGIE LIBRARY ALBANY MO 960.00 ALBIA COMMUNITY SCHOOL DIST ALBIA IA 26,103.24 ALBION SCHOOL DISTRICT 2 ALBION OK 16,436.20 ALEXANDRIA COMM SCHOOL CORP ALEXANDRIA IN 32,334.54 ALICE INDEP SCHOOL DISTRICT ALICE TX 293,311.41 ALL SAINTS ACADEMY WINTER HAVEN FL 14,621.51 ALL SAINTS CATHOLIC SCHOOL NORMAN OK 1,075.34 ALLEGHENY-CLARION VALLEY SCH DIST FOXBURG PA 15,456.00 ALPINE COUNTY LIBRARY MARKLEEVILLE CA 16,652.16 ALPINE SCHOOL DISTRICT AMERICAN FORK UT 279,203.16 ALTOONA PUBLIC LIBRARY ALTOONA KS 856.32 ALVAH SCOTT ELEMENTARY SCHOOL HONOLULU HI 4,032.00 AMHERST COUNTY PUBLIC SCHOOL DIVISION AMHERST VA 245,106.00 AMSTERDAM CITY SCHOOL DISTRICT AMSTERDAM NY 96,471.00 ANTWERP LOCAL SCHOOL DISTRICT ANTWERP OH 22,679.24 ANUENUE SCHOOL HONOLULU HI 5,376.00 APPLE VALLEY UNIF SCHOOL DIST APPLE VALLEY CA 409,172.44 ARCHULETA CO SCHOOL DIST 50 PAGOSA SPRINGS CO 81,774.00 -

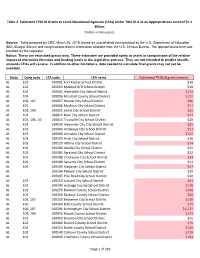

Page 1 of 283 State Cong Code LEA Code LEA Name Estimated FY2018

Table 2. Estimated FY2018 Grants to Local Educational Agencies (LEAs) Under Title IV-A at an Appropriations Level of $1.1 Billion Dollars in thousands Source: Table prepared by CRS, March 26, 2018, based on unpublished data provided by the U.S. Department of Education (ED), Budget Service and congressional district information available from the U.S. Census Bureau. The appropriations level was provided by the requester. Notice: These are estimated grants only. These estimates are provided solely to assist in comparisons of the relative impact of alternative formulas and funding levels in the legislative process. They are not intended to predict specific amounts LEAs will receive. In addition to other limitations, data needed to calculate final grants may not yet be available. State Cong code LEA code LEA name Estimated FY2018 grant amount AL 102 100001 Fort Rucker School District $10 AL 102 100003 Maxwell AFB School District $10 AL 104 100005 Albertville City School District $153 AL 104 100006 Marshall County School District $192 AL 106, 107 100007 Hoover City School District $86 AL 105 100008 Madison City School District $57 AL 103, 106 100011 Leeds City School District $32 AL 104 100012 Boaz City School District $41 AL 103, 106, 107 100013 Trussville City School District $20 AL 103 100030 Alexander City City School District $83 AL 102 100060 Andalusia City School District $51 AL 103 100090 Anniston City School District $122 AL 104 100100 Arab City School District $26 AL 105 100120 Athens City School District $54 AL 104 100180 Attalla -

Arkansas Higher Education Coordinating Board

Arkansas Higher Education Coordinating Board Regular Quarterly Meeting July 31, 2015 Arkansas Department of Higher Education 423 Main Street, Suite 400, Little Rock, Arkansas 72201 (501) 371-2000 ARKANSAS HIGHER EDUCATION COORDINATING BOARD REGULAR QUARTERLY MEETING Arkansas Department of Higher Education Five Main Place Building 423 Main Street Little Rock, AR 72201 SCHEDULE ______________________________________ Friday, July 31, 2015 Finance Committee 8:30 a.m. Academic Committee 9:15 a.m. Convene Coordinating Board Meeting *10:00 a.m. *Time approximate. Meeting will begin at the end of the Academic Committee meeting. ARKANSAS HIGHER EDUCATION COORDINATING BOARD REGULAR QUARTERLY MEETING Friday, July 31, 2015 10:00 a.m. Arkansas Department of Higher Education AGENDA I. EXECUTIVE *1. Approve Minutes of the April 30 Special Meeting and May 1 Regular Meeting 2. Agency Updates (Dr. Brett Powell) *3. Amendment to the Performance Based Funding (Dr. Powell) 4. Report on 2014 Fall College-Going Rate (Mr. Rick Jenkins) *14. Report of Nominating Committee (AHECB Chairman) II. FINANCE *5. Certification of Intercollegiate Athletic Budgets for 2015-16 (Ms. Tara Smith) *6. Economic Feasibility of Bond Issue for Arkansas Northeastern College (Ms. Chandra Robinson) *7. Economic Feasibility of Bond Issue for Arkansas Tech University (Ms. Robinson) *8. Economic Feasibility of Bond Issue for Arkansas Tech University (Ms. Robinson) *9. Economic Feasibility of Loan Issue for Arkansas Tech University (Ms. Robinson) *10. Economic Feasibility of Bond Issue for University of Arkansas, Fayetteville (Ms. Robinson) III. ACADEMIC *11. Institutional Certification Advisory Committee: Resolutions (Ms. Alana Boles) 12. Letters of Notification (Ms. Lillian Williams) 13. Letters of Intent (Ms. -

Arkansas Allocations to Leas Under the ESSER & GEER Fundspdf

Federal Emergency Aid for Public Education: Allocations to LEAs under ESSER & GEER ESSER Allocations to LEAs in Arkansas Across all three federal laws (CARES, CRRSA, and ARP), SEAs must use at least 90 percent of their grant awards to make subgrants to LEAs in proportion to the amount of funds that each LEA received under Title I, Part A in the most recent fiscal year. minimum DESE distribution to LEAs ESSER I Fund $115,882,774 ESSER II Fund 502,215,668 ARP ESSER Fund 1,127,905,050 Total, ESSER $1,746,003,492 GEER Allocations to Arkansas Both the CARES Act and CRRSA Act provided funding to Governors through the Governor’s Emergency Education Relief (GEER) Fund. The U.S. Department of Education is required to allocate 60 percent of the funds based on each state’s relative population of individuals aged 5 through 24, and 40 percent based on each state’s relative number of children counted under the Title I, Part A formula. GEER I Fund $30,663,725 GEER II Fund 13,378,181 Total, GEER $44,041,906 GEER funds may be used by the Governor of Arkansas in support of public elementary and secondary education, institutions of higher education (IHEs), or other education-related entities. A Governor has wide discretion in determining the entities in the State that will receive GEER funds. A Governor can choose to fund only LEAs, only IHEs, only education-related entities, or any combination of eligible entities. Arkansas Department of Education Division of Elementary and Secondary Education FY 2020‐21 CARES Act ‐ ESSER Funds Final Allocations with Equitable -

Schools and Libraries 2Q2016 Funding Year 2015 Authorizations - 4Q2015 Page 1 of 182

Universal Service Administrative Company Appendix SL27 Schools and Libraries 2Q2016 Funding Year 2015 Authorizations - 4Q2015 Page 1 of 182 Applicant Name City State Primary Authorized 100 ACADEMY OF EXCELLENCE NORTH LAS VEGAS NV 11,790.32 4-J SCHOOL GILLETTE WY 207.11 A + ACADEMY CHARTER SCHOOL DALLAS TX 19,122.48 A + CHILDRENS ACADEMY COMMUNITY SCHOOL COLUMBUS OH 377.16 A B C UNIFIED SCHOOL DISTRICT CERRITOS CA 308,684.37 A SPECIAL PLACE SANTA ROSA CA 8,500.00 A W BEATTIE AVTS DISTRICT ALLISON PARK PA 1,189.32 A+ ARTS ACADEMY COLUMBUS OH 20,277.16 A-C COMM UNIT SCHOOL DIST 262 ASHLAND IL 518.70 A.C.E. CHARTER HIGH SCHOOL TUCSON AZ 1,530.03 A.M. STORY INTERMEDIATE SCHOOL PALESTINE TX 34,799.00 AAA ACADEMY BLUE ISLAND IL 39,446.55 AACL CHARTER SCHOOL COLORADO SPRINGS CO 10,848.59 AAS-ADMINISTRATIVE OFFICE SAN DIEGO CA 2,785.82 ABBOTSFORD SCHOOL DISTRICT ABBOTSFORD WI 6,526.23 ABERDEEN PUBLIC LIBRARY ABERDEEN ID 2,291.04 ABERDEEN SCHOOL DISTRICT 5 ABERDEEN WA 54,176.10 ABERDEEN SCHOOL DISTRICT 58 ABERDEEN ID 8,059.20 ABERDEEN SCHOOL DISTRICT 6-1 ABERDEEN SD 13,560.24 ABIDING SAVIOR LUTHERAN SCHOOL SAINT LOUIS MO 320.70 ABINGTON COMMUNITY LIBRARY CLARKS SUMMIT PA 208.81 ABINGTON SCHOOL DISTRICT ABINGTON PA 19,710.58 ABINGTON SCHOOL DISTRICT ABINGTON MA 573.19 ABSAROKEE SCHOOL DIST 52-52 C ABSAROKEE MT 16,093.91 ABSECON PUBLIC LIBRARY ABSECON NJ 372.26 ABUNDANT LIFE CHRISTIAN ACAD MARGATE FL 1,524.99 ACADEMIA ADVENTISTA DEL CENTRO RAMON RIVERA SAN SEBASTIAN PR 1,057.75 PEREZ ACADEMIA ADVENTISTA DEL NORESTE AGUADILLA PR 5,434.40 ACADEMIA ADVENTISTA DEL NORTE ARECIBO PR 7,157.47 ACADEMIA ADVENTISTA DR. -

County District School Date of Clinic Location of Clinic (Address) If Not at the School

County District School Date of Clinic Location of clinic (address) if not at the school PULASKI ACADEMIC PLUS SCHOOL DISTRICT ACADEMICS PLUS TBA PULASKI ACADEMIC PLUS SCHOOL DISTRICT ACADEMICS PLUS TBA CRAWFORD ALMA SCHOOL DISTRICT ALMA HIGH SCHOOL 10/28/10 CRAWFORD ALMA SCHOOL DISTRICT ALMA INTERMEDIATE SCHOOL 11/1/10 CRAWFORD ALMA SCHOOL DISTRICT ALMA MIDDLE SCHOOL 11/4/10 CRAWFORD ALMA SCHOOL DISTRICT ALMA PRIMARY SCHOOL 10/25/10 BOONE ALPENA SCHOOL DISTRICT ALPENA ELEMENTARY SCHOOL 11/30/10 BOONE ALPENA SCHOOL DISTRICT ALPENA HIGH SCHOOL 11/30/10 GARLAND AR MATH & SCIENCE SCHOOL AR MATH & SCIENCE SCHOOL 10/13/10 PULASKI ARK. SCHOOL FOR THE BLIND ARK. SCHOOL FOR THE BLIND ELEM 10/20/10 PULASKI ARK. SCHOOL FOR THE BLIND ARK. SCHOOL FOR THE BLIND H.S. 10/20/10 PULASKI ARK. SCHOOL FOR THE DEAF ARK. SCHOOL FOR THE DEAF ELEM. 10/20/10 PULASKI ARK. SCHOOL FOR THE DEAF ARK. SCHOOL FOR THE DEAF H.S. 10/20/10 CLARK ARKADELPHIA SCHOOL DISTRICT ARKADELPHIA HIGH SCHOOL 11/17/10 CLARK ARKADELPHIA SCHOOL DISTRICT CENTRAL PRIMARY SCHOOL 11/12/10 CLARK ARKADELPHIA SCHOOL DISTRICT GOZA MIDDLE SCHOOL 11/12/10 CLARK ARKADELPHIA SCHOOL DISTRICT LOUISA PERRITT PRIMARY 11/10/10 County District School Date of Clinic Location of clinic (address) if not at the school CLARK ARKADELPHIA SCHOOL DISTRICT PEAKE ELEMENTARY SCHOOL 11/10/10 PULASKI ARKANSAS VIRTUAL SCHOOL ARKANSAS VIRTUAL ELEM SCHOOL TBA PULASKI ARKANSAS VIRTUAL SCHOOL ARKANSAS VIRTUAL MIDDLE SCHOOL TBA MISSISSIPPI ARMOREL SCHOOL DISTRICT ARMOREL ELEMENTARY SCHOOL 10/21/10 MISSISSIPPI ARMOREL SCHOOL DISTRICT ARMOREL HIGH SCHOOL 10/21/10 LITTLE RIVER ASHDOWN SCHOOL DISTRICT ASHDOWN HIGH SCHOOL 10/6/10 LITTLE RIVER ASHDOWN SCHOOL DISTRICT ASHDOWN JUNIOR HIGH SCHOOL 10/6/10 LITTLE RIVER ASHDOWN SCHOOL DISTRICT C. -

SL31 Funding Year 2012 Authorizations

Universal Service Administrative Company Appendix SL31 Schools and Libraries 4Q2013 Funding Year 2012 Authorizations - 2Q2013 Page 1 of 190 Applicant Name City State Primary Authorized (Fields Elementary) SOUTH HARNEY SCHOOL FIELDS OR 675.00 100 ACADEMY OF EXCELLENCE NORTH LAS VEGAS NV 16,429.32 21ST CENTURY CHARTER SCHOOL @ GARY GARY IN 325,743.99 4-J SCHOOL GILLETTE WY 697.72 A B C UNIFIED SCHOOL DISTRICT CERRITOS CA 16,506.78 A HOLMES JOHNSON MEM LIBRARY KODIAK AK 210.00 A SPECIAL PLACE SANTA ROSA CA 4,867.80 A W BEATTIE AVTS DISTRICT ALLISON PARK PA 8,971.58 A+ ARTS ACADEMY COLUMBUS OH 3,831.75 A.W. BROWN FELLOWSHIP CHARTER SCHOOL DALLAS TX 113,773.07 AAA ACADEMY POSEN IL 8,676.99 ABERDEEN PUBLIC LIBRARY ABERDEEN ID 2,236.80 ABERDEEN SCHOOL DISTRICT ABERDEEN MS 9,261.29 ABERDEEN SCHOOL DISTRICT 5 ABERDEEN WA 53,979.45 ABERDEEN SCHOOL DISTRICT 58 ABERDEEN ID 13,497.79 ABERNATHY INDEP SCHOOL DIST ABERNATHY TX 13,958.23 ABILENE FREE PUBLIC LIBRARY ABILENE KS 624.07 ABILENE INDEP SCHOOL DISTRICT ABILENE TX 18,698.04 ABILENE UNIF SCH DISTRICT 435 ABILENE KS 5,280.10 ABINGTON COMMUNITY LIBRARY CLARKS SUMMIT PA 259.00 ABINGTON SCHOOL DISTRICT ABINGTON PA 8,348.30 ABINGTON SCHOOL DISTRICT ABINGTON MA 6,133.45 ABSAROKEE SCHOOL DIST 52-52 C ABSAROKEE MT 1,430.26 ABSECON PUBLIC LIBRARY ABSECON NJ 131.30 ABSECON PUBLIC SCHOOL DISTRICT ABSECON NJ 5,091.22 ABUNDANT LIFE CHRISTIAN ACAD MARGATE FL 860.00 ACADAMY OF ST BARTHOLOMEW MIDDLEBURG HTS. -

Archived: 2003 Title I Grants to Local Educational Agencies

Fiscal Year 2003 Title I Grants to Local Educational Agencies - ARKANSAS Maximum Required Expenditures For Choice-Related Maximum Per-Child Transportation Expenditure For FY 2003 Title I And Supplemental Supplemental LEA ID District Allocation* Educational Services** Educational Services*** 502220 ACORN SCHOOL DISTRICT 111,372 22,274 1,484.95 502250 ALMA SCHOOL DISTRICT 476,788 95,358 1,018.78 502280 ALPENA SCHOOL DISTRICT 101,081 20,216 981.37 502310 ALREAD SCHOOL DISTRICT 31,439 6,288 1,209.19 502330 ALTHEIMER UNIFIED SCHOOL DISTRICT 347,874 69,575 1,391.50 502370 ALTUSDENNING SCHOOL DISTRICT 95,375 19,075 1,083.81 502430 ARKADELPHIA SCHOOLS 477,982 95,596 1,023.52 502460 ARKANSAS CITY SCHOOL DISTRICT 69,979 13,996 1,428.14 502550 ARMOREL SCHOOL DISTRICT 32,381 6,476 2,158.74 502580 ASHDOWN SCHOOL DISTRICT 339,810 67,962 1,020.45 502610 ATKINS PUBLIC SCHOOLS 264,995 52,999 996.22 502670 AUGUSTA SCHOOL DISTRICT 323,955 64,791 1,439.80 502700 BALD KNOB SCHOOL DISTRICT 374,234 74,847 1,281.62 502730 BARTONLEXA SCHOOL DISTRICT 146,897 29,379 1,335.43 500019 BATESVILLE SCHOOL DISTRICT 460,391 92,078 1,101.41 502790 BAUXITE SCHOOL DISTRICT 82,210 16,442 813.97 502820 BAY SCHOOL DISTRICT 120,284 24,057 1,366.86 500032 BEARDEN SCHOOL DISTRICT 178,759 35,752 1,004.27 502880 BEEBE SCHOOL DISTRICT 311,394 62,279 958.14 502960 BENTON SCHOOL DISTRICT 605,920 121,184 1,439.24 503060 BENTONVILLE PUBLIC SCHOOLS 722,409 144,482 972.29 503090 BERGMAN SCHOOL DISTRICT 150,444 30,089 1,002.96 503150 BERRYVILLE PUBLIC SCHOOLS 398,785 79,757 1,001.97 503210 -

AGENDA STATE BOARD of EDUCATION June 10, 2016 Arkansas Department of Education ADE Auditorium 9:00 AM

AGENDA STATE BOARD OF EDUCATION June 10, 2016 Arkansas Department of Education ADE Auditorium 9:00 AM Back Print Reports Report-1 Chair's Report Presenter: Chair Report-2 Commissioner's Report Presenter: Commissioner Johnny Key Report-3 2015 ATOY Report The 2015 Arkansas Teacher of the Year will present a component of her professional development project. Presenter: 2015 Arkansas Teacher of the Year Ms. Ouida Newton Report-4 2014-2015 Grade Inflation Report Presenter: Elbert Harvey Report-5 ForwARd Arkansas Report Presenter: Susan Harriman, Executive Director of ForwARd Report-6 Learning Services Report This information is provided to keep the State Board of Education apprised of the Department's work activities associated with college and career readiness. Presenter: Stacy Smith Report-7 Computer Science Report This information is provided to keep the State Board of Education apprised of the Department's work activities associated with Computer Science. Presenter: Anthony Owen Arkansas Social Studies Standards “A people without the knowledge of their past history, origin and culture is like a tree without roots.” – Marcus Garvey. The importance of the Social Studies Curriculum Frameworks to Arkansas K-12 education cannot be overlooked. Parents and educators readily agree on the importance of developing reading, writing and math skills. They even agree in our technological society on the importance of teaching science, but what about social studies? It is through the study of social studies that students become aware of the world around them and how that world directly impacts their lives. By learning about economics, civics and government, geography and history, students are able to develop core beliefs and values, an understanding of how the past has shaped the present and will shape the future, and the interconnectedness of the content areas.