Organization & Structure of Open Source Software Development Initiatives

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Open Source Ethos Guiding Beliefs Or Ideals That Characterize a Community

Open Source Ethos guiding beliefs or ideals that characterize a community Patrick Masson Open Source Initiative [email protected] What is the mission of the conference? …bring smart and creative people together; …inspire and motivate them to create new and amazing things; …with an intimate group of like minded individuals. What is the mission of the conference? …bring smart and creative people together; …inspire and motivate them to create new and amazing things; …with an intimate group of like minded individuals. This is the open source ethos – guiding beliefs, ideals of a community It's a great time to be working with open source 1.5 Million Projects 78% of companies run on open source 64% of companies participate It's a great time to be working with open source 88% expect contributions to grow 66% consider before proprietary <3% Don't use OSS 2015 Future of Open Source Survey Black Duck, Northbridge It's a great time to be working with open source It's a great time to be working with open source It's a great time to be working with open source It's a great time to be working with open source Open-course/Open-source Marc Wathieu CC-BY-NC-SA https://www.flickr.com/photos/marcwathieu/2412755417/ _____ College first Massive Open source Online Course (MOOC) Are you seeing other examples of this Mini-MOOC trend (free, I began but did not finish my first The Gates grantees aren’t the only ones open source courses by a MOOC (Massive Open-Source, startup or organization)? Online Course). -

Katalog Elektronskih Knjiga

KATALOG ELEKTRONSKIH KNJIGA Br Autor Naziv Godina ISBN Str. Porijeklo izdavanja 1 Peter Kent Pay Per Click Search 2006 0-471-74594-3 130 Kupovina Engine Marketing for Dummies 2 Terry Large Access 1 2007 Internet Freeware 3 Kevin Smith Excel Lassons & Tutorials 2004 Internet Freeware 4 Terry Michael Photografy Tutorials 2006 Internet Freeware Janine Peterson Phil Pivnick 5 Jake Ludington Converting Vinyl LPs 2003 Internet Freeware to CD 6 Allen Wyatt Cleaning Windows XP 2004 0-7645-7311-X Poklon for Dummies 7 Peter Kent Sarch Engine Optimization 2006 0-4717-5441-2 Kupovina for Dummies 8 Terry Large Access 2 2007 Internet Freeware 9 Dirk Dupon How to write, create, 2005 Internet Freeware promote and sell E-books on the Internet 10 Chayden Bates eBook Marketing 2000 Internet Freeware Explained 11 Kevin Sinclair How To Choose A 1999 Internet Freeware Homebased Bussines 12 Bob McElwain 101 Newbie-Frendly Tips 2001 Internet Freeware 13 Windows Basics 2004 Poklon 14 Michael Abrash Zen of Graphic 2005 Poklon Programming, 2. izdanje 15 13 Hot Internet 2000 Internet Freeware Moneymaking Methods 16 K. Williams The Complete HTML 1998 Poklon Teacher 17 C. Darwin On the Origin of Species Internet Freeware 2/175 Br Autor Naziv Godina ISBN Str. Porijeklo izdavanja 18 C. Darwin The Variation of Animals Internet Freeware 19 Bruce Eckel Thinking in C++, Vol 1 2000 Internet Freeware 20 Bruce Eckel Thinking in C++, Vol 2 2000 Internet Freeware 21 James Parton Captains of Industry 1890 399 Internet Freeware 22 Bruno R. Preiss Data Structures and 1998 Internet -

Producing Open Source Software How to Run a Successful Free Software Project

Producing Open Source Software How to Run a Successful Free Software Project Karl Fogel Producing Open Source Software: How to Run a Successful Free Software Project by Karl Fogel Copyright © 2005-2018 Karl Fogel, under the CreativeCommons Attribution-ShareAlike (4.0) license. Version: 2.3098 Home site: http://producingoss.com/ Dedication This book is dedicated to two dear friends without whom it would not have been possible: Karen Under- hill and Jim Blandy. i Table of Contents Preface ............................................................................................................................. vi Why Write This Book? ............................................................................................... vi Who Should Read This Book? .................................................................................... vii Sources ................................................................................................................... vii Acknowledgements ................................................................................................... viii For the first edition (2005) ................................................................................ viii For the second edition (2017) ............................................................................... x Disclaimer .............................................................................................................. xiii 1. Introduction ................................................................................................................... -

Linux Lunacy V & Perl Whirl

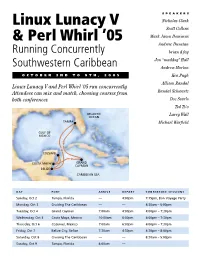

SPEAKERS Linux Lunacy V Nicholas Clark Scott Collins & Perl Whirl ’05 Mark Jason Dominus Andrew Dunstan Running Concurrently brian d foy Jon “maddog” Hall Southwestern Caribbean Andrew Morton OCTOBER 2ND TO 9TH, 2005 Ken Pugh Allison Randal Linux Lunacy V and Perl Whirl ’05 run concurrently. Attendees can mix and match, choosing courses from Randal Schwartz both conferences. Doc Searls Ted Ts’o Larry Wall Michael Warfield DAY PORT ARRIVE DEPART CONFERENCE SESSIONS Sunday, Oct 2 Tampa, Florida — 4:00pm 7:15pm, Bon Voyage Party Monday, Oct 3 Cruising The Caribbean — — 8:30am – 5:00pm Tuesday, Oct 4 Grand Cayman 7:00am 4:00pm 4:00pm – 7:30pm Wednesday, Oct 5 Costa Maya, Mexico 10:00am 6:00pm 6:00pm – 7:30pm Thursday, Oct 6 Cozumel, Mexico 7:00am 6:00pm 6:00pm – 7:30pm Friday, Oct 7 Belize City, Belize 7:30am 4:30pm 4:30pm – 8:00pm Saturday, Oct 8 Cruising The Caribbean — — 8:30am – 5:00pm Sunday, Oct 9 Tampa, Florida 8:00am — Perl Whirl ’05 and Linux Lunacy V Perl Whirl ’05 are running concurrently. Attendees can mix and match, choosing courses Seminars at a Glance from both conferences. You may choose any combination Regular Expression Mastery (half day) Programming with Iterators and Generators of full-, half-, or quarter-day seminars Speaker: Mark Jason Dominus Speaker: Mark Jason Dominus (half day) for a total of two-and-one-half Almost everyone has written a regex that failed Sometimes you’ll write a function that takes too (2.5) days’ worth of sessions. The to match something they wanted it to, or that long to run because it produces too much useful conference fee is $995 and includes matched something they thought it shouldn’t, and information. -

When Geeks Cruise

COMMUNITY Geek Cruise: Linux Lunacy Linux Lunacy, Perl Whirl, MySQL Swell: Open Source technologists on board When Geeks Cruise If you are on one of those huge cruising ships and, instead of middle-aged ladies sipping cocktails, you spot a bunch of T-shirt touting, nerdy looking guys hacking on their notebooks in the lounges, chances are you are witnessing a “Geek Cruise”. BY ULRICH WOLF eil Baumann, of Palo Alto, Cali- and practical tips on application develop- The dedicated Linux track comprised a fornia, has been organizing geek ment – not only for Perl developers but meager spattering of six lectures, and Ncruises since 1999 (http://www. for anyone interested in programming. though there was something to suit geekcruises.com/), Neil always finds everyone’s taste, the whole thing tended enough open source and programming Perl: Present and to lack detail. Ted T’so spent a long time celebrities to hold sessions on Linux, (Distant?) Future talking about the Ext2 and Ext3 file sys- Perl, PHP and other topics dear to geeks. In contrast, Allison Randal’s tutorials on tems, criticizing ReiserFS along the way, Parrot Assembler and Perl6 features were but had very little to say about network Open Source Celebs hardcore. Thank goodness Larry Wall file systems, an increasingly vital topic. on the Med summed up all the major details on Perl6 Developers were treated to a lecture on I was lucky enough to get on board the in a brilliant lecture that was rich with developing shared libraries, and admins first Geek Cruise on the Mediterranean, metaphors and bursting with informa- enjoyed sessions on Samba and hetero- scaring the nerds to death with my tion. -

Java Bytecode Manipulation Framework

Notice About this document The following copyright statements and licenses apply to software components that are distributed with various versions of the OnCommand Performance Manager products. Your product does not necessarily use all the software components referred to below. Where required, source code is published at the following location: ftp://ftp.netapp.com/frm-ntap/opensource/ 215-09632 _A0_ur001 -Copyright 2014 NetApp, Inc. All rights reserved. 1 Notice Copyrights and licenses The following component is subject to the ANTLR License • ANTLR, ANother Tool for Language Recognition - 2.7.6 © Copyright ANTLR / Terence Parr 2009 ANTLR License SOFTWARE RIGHTS ANTLR 1989-2004 Developed by Terence Parr Partially supported by University of San Francisco & jGuru.com We reserve no legal rights to the ANTLR--it is fully in the public domain. An individual or company may do whatever they wish with source code distributed with ANTLR or the code generated by ANTLR, including the incorporation of ANTLR, or its output, into commerical software. We encourage users to develop software with ANTLR. However, we do ask that credit is given to us for developing ANTLR. By "credit", we mean that if you use ANTLR or incorporate any source code into one of your programs (commercial product, research project, or otherwise) that you acknowledge this fact somewhere in the documentation, research report, etc... If you like ANTLR and have developed a nice tool with the output, please mention that you developed it using ANTLR. In addition, we ask that the headers remain intact in our source code. As long as these guidelines are kept, we expect to continue enhancing this system and expect to make other tools available as they are completed. -

Letter, If Not the Spirit, of One Or the Other Definition

Producing Open Source Software How to Run a Successful Free Software Project Karl Fogel Producing Open Source Software: How to Run a Successful Free Software Project by Karl Fogel Copyright © 2005-2021 Karl Fogel, under the CreativeCommons Attribution-ShareAlike (4.0) license. Version: 2.3214 Home site: https://producingoss.com/ Dedication This book is dedicated to two dear friends without whom it would not have been possible: Karen Under- hill and Jim Blandy. i Table of Contents Preface ............................................................................................................................. vi Why Write This Book? ............................................................................................... vi Who Should Read This Book? ..................................................................................... vi Sources ................................................................................................................... vii Acknowledgements ................................................................................................... viii For the first edition (2005) ................................................................................ viii For the second edition (2021) .............................................................................. ix Disclaimer .............................................................................................................. xiii 1. Introduction ................................................................................................................... -

Annual Report

[Credits] Licensed under Creative Commons Attribution license (CC BY 4.0). All text by John Hsieh and Georgia Young, except the Letter from the Executive Director, which is by John Sullivan. Images (name, license, and page location): Wouter Velhelst: cover image; Kori Feener, CC BY-SA 4.0: inside front cover, 2-4, 8, 14-15, 20-21, 23-25, 27-29, 32-33, 36, 40-41; Michele Kowal: 5; Anonymous, CC BY 3.0: 7, 16, 17; Ruben Rodriguez, CC BY-SA 4.0: 10, 13, 34-35; Anonymous, All rights reserved: 16 (top left); Pablo Marinero & Cecilia e. Camero, CC BY 3.0: 17; Free This report highlights activities Software Foundation, CC BY-SA 4.0: 18-19; Tracey Hughes, CC BY-SA 4.0: 30; Jose Cleto Hernandez Munoz, CC BY-SA 3.0: 31, Pixabay/stevepb, CC0: 37. and detailed financials for Fiscal Year 2016 Fonts: Letter Gothic by Roger Roberson; Orator by John Scheppler; Oswald by (October 1, 2015 - September 30, 2016) Vernon Adams, under the OFL; Seravek by Eric Olson; Jura by Daniel Johnson. Created using Inkscape, GIMP, and PDFsam. Designer: Tammy from Creative Joe. 1] LETTER FROM THE EXECUTIVE DIRECTOR 2] OUR MISSION 3] TECH 4] CAMPAIGNS 5] LIBREPLANET 2016 6] LICENSING & COMPLIANCE 7] CONFERENCES & EVENTS 7 8] LEADERSHIP & STAFF [CONTENTS] 9] FINANCIALS 9 10] OUR DONORS CONTENTS our most important [1] measure of success is support for the ideals of LETTER FROM free software... THE EXECUTIVE we have momentum DIRECTOR on our side. LETTER FROM THE 2016 EXECUTIVE DIRECTOR DEAR SUPPORTERS For almost 32 years, the FSF has inspired people around the Charity Navigator gave the FSF its highest rating — four stars — world to be passionate about computer user freedom as an ethical with an overall score of 99.57/100 and a perfect 100 in the issue, and provided vital tools to make the world a better place. -

CLE Materials

Software Freedom Law Center Fall Conference at Columbia Law School CLE materials October 30, 2015 License Compliance Dispute Resolution Software Freedom Law Center October 30, 2015 1) Software Freedom Law Center: Guide to GPL Compliance 2nd Edition 2) Free Software Foundation: Principles for Community-Oriented GPL Enforcement 3) Terry J. Ilardi: FOSS Compliance @ IBM 15 Years (and count- ing) Software Freedom Law Center Guide to GPL Compliance 2nd Edition Eben Moglen & Mishi Choudhary October 31, 2014 Contents TheWhat,WhyandHowofGNUGPL . 3 CopyrightandCopyleft . 4 Concepts and License Mechanics of Copyleft. 6 LicenseProvisionsAnalyzed. 10 GPLv2............................... 10 GPLv3............................... 18 GPLSpecialExceptionLicenses . 31 AGPL............................... 31 LGPL ............................... 34 Understanding Your Compliance Responsibilities . 41 WhoHasComplianceObligations? . 41 HowtoMeetComplianceObligations . 43 TheKeytoComplianceisGovernance . 45 PrinciplesofPreparedCompliance . 47 HandlingComplianceInquiries . 48 Appendix1: OfferofSourceCode . 52 References................................ 56 This document presents the legal analysis of the Software Freedom Law Center and the authors. This document does not express the views, intentions, policy, or legal analysis of any SFLC clients or client organizations. This document does not constitute legal advice or opinion regarding any specific factual situation or party. Specific legal advice should always be sought from qualified legal counsel on the application -

Table of Contents • Index • Reviews • Reader Reviews • Errata Perl 6 Essentials by Allison Randal, Dan Sugalski, Leopold Tötsch

• Table of Contents • Index • Reviews • Reader Reviews • Errata Perl 6 Essentials By Allison Randal, Dan Sugalski, Leopold Tötsch Publisher: O'Reilly Pub Date: June 2003 ISBN: 0-596-00499-0 Pages: 208 Slots: 1 Perl 6 Essentials is the first book that offers a peek into the next major version of the Perl language. Written by members of the Perl 6 core development team, the book covers the development not only of Perl 6 syntax but also Parrot, the language-independent interpreter developed as part of the Perl 6 design strategy. This book is essential reading for anyone interested in the future of Perl. It will satisfy their curiosity and show how changes in the language will make it more powerful and easier to use. 1 / 155 • Table of Contents • Index • Reviews • Reader Reviews • Errata Perl 6 Essentials By Allison Randal, Dan Sugalski, Leopold Tötsch Publisher: O'Reilly Pub Date: June 2003 ISBN: 0-596-00499-0 Pages: 208 Slots: 1 Copyright Preface How This Book Is Organized Font Conventions We'd Like to Hear from You Acknowledgments Chapter 1. Project Overview Section 1.1. The Birth of Perl 6 Section 1.2. In the Beginning . Section 1.3. The Continuing Mission Chapter 2. Project Development Section 2.1. Language Development Section 2.2. Parrot Development Chapter 3. Design Philosophy Section 3.1. Linguistic and Cognitive Considerations Section 3.2. Architectural Considerations Chapter 4. Syntax Section 4.1. Variables Section 4.2. Operators Section 4.3. Control Structures Section 4.4. Subroutines Section 4.5. Classes and Objects Section 4.6. -

Account 03 Account Provider

Account identifier: account_03 Account provider: GEARY_SERVICE_PROVIDER_GMAIL Service type: GEARY_PROTOCOL_IMAP Service host: imap.gmail.com Error type: GearyImapError 8 Message: a007 STATUS: Command timed out Back trace: * geary_problem_report_construct * geary_account_problem_report_construct * geary_service_problem_report_construct * components_reflow_box_new * g_closure_invoke * g_signal_handler_disconnect * g_signal_emit_valist * g_signal_emit * geary_imap_engine_folder_operation_construct * g_subprocess_communicate_utf8 * g_task_attach_source * geary_imap_engine_generic_account_construct * g_subprocess_communicate_utf8 * g_task_attach_source * geary_imap_deserializer_stop_async * g_subprocess_communicate_utf8 * g_task_attach_source * geary_contact_store_impl_new * g_subprocess_communicate_utf8 * g_task_attach_source * geary_contact_store_impl_new * g_subprocess_communicate_utf8 * g_task_attach_source * geary_imap_client_session_send_command_async * g_subprocess_communicate_utf8 * g_task_attach_source * geary_nonblocking_batch_add * g_subprocess_communicate_utf8 * g_task_attach_source * geary_nonblocking_lock_get_is_cancelled * geary_scheduler_scheduled_instance_get_type * g_main_context_dispatch * g_main_context_dispatch * g_main_context_iteration * g_application_run * _vala_main * __libc_start_main * _start Geary version: 3.36.1 Geary revision: Ubuntu/3.36.1-1 GTK version: 3.24.20 GLib version: 2.64.3 WebKitGTK version: 2.28.4 Desktop environment: LXDE Distribution name: Ubuntu Distribution release: 20.04 Installation prefix: /usr -

Geary Email (Protonmail/Gmail/Icloud/Fast)

Geary Email (ProtonMail/Gmail/iCloud/Fas t) Gmail 1. Add the account to Geary Select the Gmail option in the window below. Enter your Gmail address and your password. Now sign into your Gmail account again using the same Gmail address and password to add your account to Geary. ProtonMail NOTE: Using ProtonMail with a 3rd Party Email Client is only supported on Paid “plans 1. Download the ProtonMail Bridge from here. 2. Install Protonmail Bridge Once the .deb file has been opened by Eddy click the Install button to install the application. 3. Setup Protonmail Bridge Once you open Protonmail Bridge from the Activities menu (in the top left) you will see the screen below. From here, enter your username and password that you using to sign into the ProtonMail website. Once signed in, you can review the configuration steps for Thunderbird at the link in the Protonmail Bridge. The steps for Thunderbird will work in Geary. Click on the arrow to the left of your username and then click on the Mailbox Configuration button to open the Email Settings window. This window will have your password (which is different then your ProtonmMail password), port numbers for IMAP and SMTP, as well as the security method for both IMAP and SMTP. 4. Add the account to Geary Once signed into Protonmail Bridge click the menu icon in the top left of Geary then click Accounts. Next click the Other email providers button to add the ProtonMail account. Now enter the information from the Mailbox Configuration window and note that we are entering the hostname IP address, followed by the port number like this: 127.0.0.1:1143 .