A Century Properties Group, Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sec 17-A Fy 2011

CENTURY rn Y IioIJF. 1t.I 1 F.5 C; l-io 1; P, 1 KC";. 16 April 20 12 THE PHILIPPINE STOCK EXCHANGE, INC. PSE Center, Exchange Road: Ortigas Center lasig City Attention: MS. JANET A. ENCARNACION Head: Disclosure Grozp Gentlemen: ,4ttached please find the Amended SEC Form 17-A amending the notes to financials inhcating subsequent event of the Dividend declaration of Century Properties Group Inc. Thank yoc. Very truly yor/rs, 0 LYREE USON -CRUZ COVER SHEET [6 0 15 16 16 S.E.C. Registration Number (FORMERLY EAST ASIA POWER RESOURCES CORPORATION) (Company's Full Name) 21st FLOOR, PACIFIC STAR BUZLDING, SEN. GIL PUYAT CORNER MAKATI AVE., MAKATI CITY (Business Address: No. Street City / Town / Province) I Neko lyree Uson -Cruz (632) 7935520 1 Contact Person Company Telephone Number SEC FORM -17 A - Amended Annual Report with Audited 2011 Consolidated F/S 0 6 2 7 Month Day FORM TYPE Month Day Fiscal Year Annual Meeting I Secondary License Type, IfApplicable [777 Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings 7I To be accomplished by SEC Personnel concerned File Number LCU Document I.D. Cashier STAMPS Remarks = pls. use black ink for scanning purposes. SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended: December 31, 2011 2. SEC Identification Number: 60566 3. BIR Tax Identification No.: 004-504-281-000 4. Exact name of issuer as specified in its charter: CENTURY PROPERTIES GROUP INC. -

Hilfi,,,Ful Rt, W Flinance

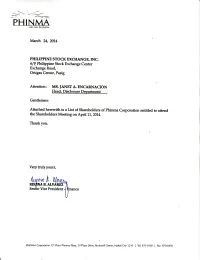

J\N V-/----/- Life an be l>etter March 24,2014 PHILIPPINE STOCK EXCHANGE, INC. /F Philippine Stock Exchange Center Exdrange Road, Ortigas Center, Pasig Attention: MS.IANETA-ENCARNACION Head, Disclosure Depa@ent Genflemen: Attached herewith is a List of Shareholders of Phinma Coqporation entitled to attend the Shareholders Meeting on April 11.',ZOl4. Thankyou. Verytrulyyours, hilfi,,,ful rt, W REqfNA B. Senior Vice ^LvirREYt4\\President flinance PH|NMACorporationl2eFloorPhinmaPlaza,3gPlazaOrive,nockwell Center,Makati City1210 lTel:870-0100 lFax:870-0456 Stock Transfer Service Inc. Page No. 1 PHINMA CORPORATION Stockholder MasterList As of 03/18/2014 Sth. No. Name Address Citizenship Holdings ---------------------------------------------------------------------------------------------------------------------------------------------------------------- 0090000083 YU, JUAN G. &/OR YU JOHN PETER C. 12 WALL ST. Filipino 35,000 DONA RITA VILLAGE BANILAD, CEBU CITY 000AI203 EDENCIO ABAN NO ADDRESS Filipino 443 000AI055 GABRIEL M. ABEDES QUIRINO, BACNOTAN Filipino 1,342 LA UNION 000AI363 JUAN BOSCO P. ABELLANA MT. CARMEL PARISA RD. 8 Filipino 252 PROJECT 6, QUEZON CITY 000AI171 ARTURO G. ABELLO C/O RAFAEL ABELLO SR. Filipino 4,704 PUROK ROXAS, TANGUB BACOLOD CITY 000AI366 CARLOS ABELLO C/O JOSE SANTOS Filipino 100 ADM BLDG. ATENEO DE MANILA UNIVERSITY KATIPUNAN AVE. QUEZON CITY 000AI341 EDUARDO G. ABELLO &/OR MARILEN P. ABELLO 206 MARIA PATERNO Filipino 3,317 SAN JUAN, METRO MANILA 000AI333 ELISA G. ABELLO 206 M. PATERNO ST. Filipino 1,804 SAN JUAN, METRO MANILA 000AI00C EMILIO ABELLO 206 M. PATERNO ST. Filipino 2,704 SAN JUAN, METRO MANILA 000AI063 MANUEL ABELLO 1725 BALBOA STREET Filipino 1,500 ERORECO VILLAGE BACOLOD CITY 000AI108 MANUEL G. ABELLO 699 BUFFALO, GREENHILLS Filipino 1,375 MANDALUYONG CITY 000AI167 PACITA G. -

Ccn Tin Importer Im0006021794 430968150000 Daesang Ricor Corporation Im0002959372 003873536000 Westpoint Industrial Sales Co

CCN TIN IMPORTER IM0006021794 430968150000 DAESANG RICOR CORPORATION IM0002959372 003873536000 WESTPOINT INDUSTRIAL SALES CO. INC. IM0002992817 000695510000 ASIAN CARMAKERS CORPORATION IM0002963779 232347770000 STRONG LINK DEVELOPMENT CORPORATION IM0003299511 002624091000 TABAQUERIA DE FILIPINAS INC. IM0003063011 217711150000 ASIAWIDE REFRESHMENTS CORPORATION IM0002963639 001007787000 GX INTERNATIONAL INC. IM0006830714 456650820000 MOBIATRIX INC IM0003014592 002765139000 INNOVISTA TECHNOLOGIES INC. IM0003214699 005393872000 MONTEORO CHEMICAL CORPORATION IM0004340299 000126640000 LINKWORTH INTERNATIONAL INC. IM0006804179 417272052000 EATON INDUSTRIES PHILIPPINES LLC PH IM0002957590 000419293000 ALLEGRO MICROSYSTEMS PHILS. INC. IM0004143132 001030408000 PUENTESPINA ORCHIDS AND TROPICAL IM0003131297 004558769000 ARCHITECKS METAL SYSTEMS INC. IM0003025799 103873913000 MCMASTER INTERNATIONAL SALES IM0002973979 000296020000 CARE PRODUCTS INC IM0003014231 001026198000 INFRATEX PHILIPPINES INC. IM0002962691 000288655000 EURO-MED LABORATORIES PHILS. INC. IM0003031438 006818264000 NORTHFIELDS ENTERPRISES INT'L. INC. IM0003170217 002925850000 KENRICH INT'L . DISTRIBUTOR INC. IM0003259994 000365522000 KAMPILAN MANUFACTURING CORPORATION IM0003132498 103901522000 PEONY MERCHANDISING IM0002959496 204366533000 GLOBEWIDE TRADING IM0002966514 000070213000 NORKIS TRADING CO INC. IM0003232492 000117630000 ENERGIZER PHILIPPINES INC. IM0003131513 000319974000 HI-Q COMMERCIAL.INC IM0003035816 000237662000 PHILIPPINE INTERNATIONAL DEV'T INC. IM0003090795 113041122000 -

Intellectual Property Center, 28 Upper Mckinley Rd. Mckinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel

Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date: 13 April 2021 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION .................................................................................................... 2 1.1 ALLOWED NATIONAL MARKS ............................................................................................................................................. 2 Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date: 13 April 2021 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION 1.1 Allowed national marks Application Filing No. Mark Applicant Nice class(es) Number Date 23 January 1 4/2009/00000782 ACZÉE EON PHARMATEK, INC. [PH] 3 2009 7 VS Makan Food Corporation 2 4/2017/00019774 December KUDETAH 43 [PH] 2017 8 August 3 4/2019/00014005 TING`S KITCHEN Ting Ting Xu [PH] 30 and32 2019 3 Sunwealth Land Development 4 4/2019/00015574 September CTC ARCADE 36 Corporation [PH] 2019 12 FERCAMPO Louis Maclean Far East Inc. 5 4/2019/00019668 November 1 FERTILIZER [PH] 2019 4 TITA TRAINING IS Personal Collection Direct 6 4/2019/00020973 December 35 THE ANSWER Selling, Inc. [PH] 2019 4 RITA RECRUITMENT Personal Collection Direct 7 4/2019/00020974 December 35 IS THE ANSWER Selling, Inc. [PH] 2019 4 CITA COLLECTION IS Personal Collection Direct 8 4/2019/00020975 December 35 THE ANSWER Selling, Inc. [PH] 2019 20 Huangteng Group Co., Ltd. 9 4/2019/00022020 December 37 [CN] 2019 1 March 10 4/2019/00501118 SIZZLING CITY Abo, Ranulfo A. -

EXPAT Nov 14-27, 2010

ENTER THE CONFLICT ZONE PAGE 6 expatexpatexpatNEWSPAPER November 14 - 27, 2010 Vol. XXVI No. 129 expatphilippines.wordpress.com The Philippines Forum for International Readers since 1981 AccessBy JAHZEEL ABIHAIL isG. CRUZ Tourism’s Priority – Lim WHAT’S Tourism Sec. Alberto Lim (center) attends a tourism ence.” He was also president of the Makati foster competition among carriers. INSIDE confab in Subic Business Club prior to his current post. “The lack of access has been an issue due As a longtime industry insider, Lim laments to protectionism. If you have better access, the that tourism in the country has “grown too way that Bali had better access and they grew slowly” over the past decade. The Department from 30,000 [foreign visitors] to 3 million, the expects to meet this year’s target of 3.3 mil- way that Vietnam has allowed foreign carriers lion foreign visitor arrivals, and plans a 10- to to bring in the tourists, we would have higher 15-percent increase for 2011 to 3.6 million, visitor numbers,” he adds. a number that will depend on infrastructure He also hopes to regain the meetings, in- growth and policy reforms. centives, conventions and exhibitions (MICE) market, which he says the country lost to its “I’m not a PR person,” says Tourism Improvements Needed Southeast Asian neighbors ever since the gov- Secretary Alberto Lim from behind his desk. Bohol needs airport upgrades; Siargao, ernment stopped supporting private sector TRAVEL A man who seems to prefer having his work more surfing facilities; Samar and Batanes, bidders. Now, the country’s largest exhibition Legazpi, beyond the lava speak for itself, he cites one obstacle above all more flights. -

2011: the Year of Transport Fares Increase

TRAVEL EVENTS PEOPLE Marinduque is perfect for Angola celebrates its Vanessa Suatengco a diamond a romantic getaway. 2 brigh, golden future. 4 in the hotel industry. 9 Legend of India AUTHENTIC INDIAN CUISINE Where the Food is LEGENDARY! expatNEWSPAPER 114B Jupiter St, Bel-air II, Makati City expatexpat Email: [email protected] Tel: 836-42-32/211-9864 January 30 - February 12, 2011 Vol. XXVI No. 134 expatphilippines.wordpress.com Mobile: 0917-8992566 Present this ad and get a 10% discount. THE PHILIPPINES FORUM FOR INTERNATIONAL READERS SINCE 1981 Valid until March 31, 2011. 2011: The Year of Transport Fares Increase By TIMOTHY JAY IBAY bit lower with stored-value ticket users facing an average of 33.7 percent fare increase, while hile fare increases have been in single-journey ticket users have it pegged at the works for a while now, hav- 50.3 percent. As of this writing, the Depart- ing withstood TROs, hearings ment of Transportation and Communication Wand general public opposition, 2011 will (DOTC) has yet to release the proposed fare finally see them for the Light Rail Tran- matrix for the MRT Line 3. sit (LRT) and Metro Rail Transit (MRT), In his first State of the Nation Address, Metro Manila taxi cabs, and the new South President Aquino pointed out that ordinary Luzon Expressway toll fees implement- tax payers, including those who live outside ed. The increases are far from marginal. the Metro, have been forced to foot the bill The LRT/MRT fares under the recently of the rising costs of running the trains due to approved fare matrix will go up by an average previous administrations’ refusal to hike fares. -

Shang List 052316

ISSUER STOCKHOLDER TYPE STOCKHOLDER NO STOCKHOLDER NAME ADDRESS NATIONALITY SHARES A. T. DE CASTRO SECURITIES SUITE 701, 7/F AYALA TOWER AYALA AVENUE, SHANG PROPERTIES, INC. BROKER 211123 PH 535 CORPORATION MAKATI CITY G/F FORTUNE LIFE BUILDING 162 LEGASPI ST., SHANG PROPERTIES, INC. BROKER 211238 AAA SOUTHEAST EQUITIES, INC. PH 8 LEGASPI VILL. MAKATI, METRO MANILA UNIT E 2904-A PSE CENTER SHANG PROPERTIES, INC. BROKER 80442 ABACUS SECURITIES CORPORATION EXCHANGE RD., ORTIGAS CENTER PH 2,049 PASIG CITY ALL ASIA SEC. MGMT. CORP. 7/F SYCIP-LAW ALL ALL ASIA SECURITIES MANAGEMENT SHANG PROPERTIES, INC. BROKER 211322 ASIA CENTER 105 PASEO DE ROXAS STREET PH 35 CORP. MAKATI CITY 5/F PACIFIC STAR BLDG., MAKATI SHANG PROPERTIES, INC. BROKER 80257 AMON SECURITIES CORP. A/C#001-54011 PH 6 AVE COR GIL PUYAT MAKATI CITY 5/F PACIFIC STAR BUILDING MAKATI AVE. COR. GIL SHANG PROPERTIES, INC. BROKER 211303 AMON SECURITIES CORPORATION PH 98 PUYAT AVE MAKATI CITY AMON SECURITIES CORPORATION A/C # 10TH FLR., PACIFIC STAR BLDG. MAKATI AVENUE, SHANG PROPERTIES, INC. BROKER 211050 PH 982 001-33247 COR. SEN GIL PUYAT AVENUE, MAKATI, M. M. 3/F ASIAN PLAZA 1, SENATOR GIL J. PUYAT SHANG PROPERTIES, INC. BROKER 211014 ANSCOR HAGEDORN SECURITIES INC PH 285 AVENUE, MAKATI METRO MANILA 9TH FLR., METROBANK PLAZA BLDG SEN GIL J. SHANG PROPERTIES, INC. BROKER 211244 ASI SECURITIES, INC. PH 142 PUYAT AVENUE MAKATI, METRO MANILA A/C-CAXN1222 RM. 207 SHANG PROPERTIES, INC. BROKER 80673 ASIAN CAPITAL EQUITIES, INC. PENINSULA COURT, PASEO DE ROXAS PH 785 COR., MAKATI AVE., MAKATI CITY SUITE 210 MAKATI STOCK EXCHANGE BLDG., SHANG PROPERTIES, INC. -

(Philippines) Energy Corp. I

CCN TIN IMPORTER IM0006021794 430968150000 DAESANG RICOR CORPORATION IM0003202135 002243275000 TEAM (PHILIPPINES) ENERGY CORP. IM0002993899 000619471000 BENLY INDUSTRIAL CORPORATION IM0002976072 000392245000 RG MEDITRON INC IM0003009734 003923000000 GRAND DRAGON ENTERPRISES INC. IM0003111776 201172648000 SIGN MEDIA INC. IM0002961377 100456785000 FAREN ENTERPRISES IM0003000079 203374173000 DOITSU TRADING LIMITED CO. IM0002972336 005774435000 ALUSIGN PLASTICS INC. IM0003125173 205859203000 TOP RIGID IND'L SAFETY SUPPLY INC. IM0003036170 000201873000 PHILIPPINE UNION COMMERCIAL INC. IM0003022218 103931119000 LYNBY TRADING IM0002993597 219883990000 BAYER CROPSCIENCE INC. IM0002970791 134029364000 PACARAN ENGINEERING IM0003138895 000531327000 EVERGREEN MANUFACTURING CORP IM0003214699 005393872000 MONTEORO CHEMICAL CORPORATION IM0003828131 006814533000 FLUID SOLUTIONS INC. IM0006641091 409507988000 HEDCOR SABANGAN INC. IM0005652073 008143217000 TIESTO APPAREL MANUFACTURING INC IM0002975033 000355188000 ORIENTAL MERCHANTS INC IM0002995697 241232289000 CHINA OCEANIS PHILIPPINES INC. IM0003083330 125966059000 LUMISPEC INDUSTRIAL SALES IM0003197638 005238082000 PILMICO ANIMAL NUTRITION CORPORATIO IM0003235076 192229234000 ANAKI SYSTEMS SALES IM0003213676 100851603000 MARI-LAO MARKETING IM0003018318 000323718000 KNOTSBERRY FARM MFG. CO. INC. IM0003035816 000237662000 PHILIPPINE INTERNATIONAL DEV'T INC. IM0003090795 113041122000 RANVIN MARKETING IM0003005836 100144060000 FLAVORITES ENTERPRISES IM0002976293 000200643000 APL LOGISTICS PHILIPPINES INC. -

Intellectual Property Center, 28 Upper Mckinley Rd

Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date: 28 January 2021 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION .................................................................................................... 2 1.1 ALLOWED NATIONAL MARKS ............................................................................................................................................. 2 Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date: 28 January 2021 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION 1.1 Allowed national marks Application No. Filing Date Mark Applicant Nice class(es) Number 16 June 1 4/2017/00009271 Green Cross, Inc. [PH] 5 2017 8 March Tristellar Trading Corporation 2 4/2018/00004269 ROYALE 30 2018 [PH] 24 April 3 4/2018/00006882 GAMEBOOKR Isaiah A. Mangundayao [PH] 35 2018 Mary Assumption S. Bautista- 20 June 4 4/2018/00010337 MARISON`S Villareal [PH] andMarison`s 43 2018 Home Cuisine, Inc. [PH] 8 October Batuhan Upland and Lowland 5 4/2018/00017813 BULFA 30 2018 Farmers Association [PH] 10 October 6 4/2018/00018191 KABAB REPUBLIC Ecko8 Trading Inc. [PH] 43 2018 10 October 7 4/2018/00018192 NAY LEBANESE Ecko8 Trading Inc. [PH] 43 2018 17 October 8 4/2018/00018674 SEACOM Seacom, Inc [PH] 7 and37 2018 26 May 9 4/2018/00502319 TUTU PASTRIES Mercado, Cearita [PH] 35 2018 11 July 10 4/2018/00503154 PW EVENTS MMM Partyworks Shop [PH] 35 2018 11 4/2019/00007456 7 May 2019 TICKETKO Journeytech Inc. -

List of Companies Issued with Certificate of Compliance (Coc) Companies Issued with Certificate of Compliance (Coc)

Department of Labor and Employment National Capital Region LIST OF COMPANIES ISSUED WITH CERTIFICATE OF COMPLIANCE (COC) as of March 12, 2015 NO.NO. EESSTTAABBLLIISSHHMMEENNT AADDDDRREESSSS 11 22GGOEE XXPPRREESSSS,II NNCC.. GGeenneerraalAA vviiaattiioonAA rreeaa,MM aanniillaDD oommeessttiicAA iirrppoorrtt,PP aassaayCC iittyy 22 22GGOGG RROOUUPP,II NNCC.. 1155//FTT iimmeesPP llaazzaBB llddgg..,UU NAA vvee.cc oorr.TT aafftAA vvee..,EE rrmmiittaa,MM aanniillaa 33 22GGOLL OOGGIISSTTIICCSS,II NNCC.. ##446MM eettrroAA ssiiaCC oommppoouunndd,TT IIPPAASEE lliissccoRR ooaadd,BB rrggyy.II bbaayyoo,TT aagguuiigCC iittyy 44 33K GGOOLLDDEEN FFOOOODDS CCOORRPPOORRAATTIIOONN 2 GGrraannaadda SStt..,BB rrggyy. VVaalleenncciiaa,QQ uueezzoonCC iittyy 55 88445EE NNTTEERRPPRRIISSEESS 88445SS ttoo.CC rriissttoSS tt..,BB iinnoonnddoo,MM aanniillaa 66 AA--1DD RRIIVVIINNGCC OO..,II NNCC.. 2SS ttaa.LL uucciiaSS tt..,PP llaaiinnvviieeww,MM aannddaalluuyyoonngCC iittyy 77 AAAAATT RRAAVVEELSS EERRVVIICCEESS,II NNCC.. JCC oojjuuaannccoBB llddgg..,11 119DD eellaRR oossaSS tt..,MM aakkaattiCC iittyy AAAAI PPEEEERRS IINNCCOORRPPOORRAATTEEDD AAAAI FFrreeiigghht MMaannaaggeemmeennt CCeenntteerr, KKaaiinnggiin RRooaad MMuullttii--nnaattiioonnaal DDrriivvee, PPaarraannaaqquue CCiittyy 88 AAAAI WWOORRLLDDWWIIDDE LLOOGGIISSTTIICCS IINNCC.. AAAAI FFrreeiigghht MMaannaaggeemmeennt CCeenntteerr, KKaaiinnggiin RRooaad MMuullttii--nnaattiioonnaal DDrriivvee, PPaarraannaaqquue CCiittyy 99 1010 AABBEELLAARRDDO GG. LLUUZZAANNO LLAAW OOFFFFIICCEE 55//F VViiccttoorriia BBllddgg.., 1166770 -

TOUR OPERATORS As of September 30, 2011 EXPIRY GENERAL MANAGER REGION/NAME DATE ADDRESS EMAIL ADDRESS TEL / FAX NO

DEPARTMENT OF TOURISM ‐ PHILIPPINES OFFICE OF TOURISM STANDARDS AND REGULATION ACCREDITATION DIVISION LIST OF ACCREDITED TOUR OPERATORS As of September 30, 2011 EXPIRY GENERAL MANAGER REGION/NAME DATE ADDRESS EMAIL ADDRESS TEL / FAX NO. NATIONAL CAPITAL REGION CALOOCAN CITY GOLDMINES TOURS AND TRAVEL CORP 6/30/2012 357‐B BET 9TH & 10TH AVE. RIZAL EXT., GRACE PARK CALOOCAN [email protected] (632) 362‐3686 MS. EMELY CHUA MANILA ABACAST TRAVEL, INC. 6/30/2012 2nd Floor Enriqueta Bldg., 1675‐1677 A. Mabini St., Malate, Manila [email protected] 525‐67‐77 / 521‐43‐08 NEDILYN A. DALIMOT ACANTHUS TOURS AND TRAVEL CORPORATION 6/30/2012 463 JABONEROS ST BINONDO MANILA [email protected] (632) 241‐7295 LELE D KING AMITY TRAVEL CORPORATION 6/30/2012 G/F VIP BLDG. 1150 ROXAS BOULEVARD BRGY.667 ZONE 72 DISTRICT V ERMITA [email protected] 524‐9671‐76 / 521‐1328 BENJAMIN L. GANA JR. ANNSET HOLIDAYS INC 6/30/2012 U502 Dna Felisa Syiuco Bldg 1872 Remedios St corTaftAve Malate [email protected] 40065‐21/26 Serafina S. Joven AQUA TRAVEL AND TOURS 6/30/2012 1966 Jorge Bocobo St Malate Mla [email protected] 5231989 / 5222536 Thelma Zuniga ASIAVENTURE TOURS & TRAVEL INC 6/30/2012 Rm 305 De Villa Bldg 1153 MH del Pilar St Ermita Manila 5266929/5251811 Gianni Sylvain ATLAS TOURS & TRAVEL INC 6/30/2012 2/F Rm. 206 Franlour Koh Bldg 1307 M H Del Pilar cor Pfaura Mla [email protected] 5217325 / 5217325 Amorita Generillo BALIWAG TOURS & TRAVEL, INC. 6/30/2012 429 VICTORIA BLDG. -

THE PHILODRILL CORPORATION Page : 1 LIST of STOCKHOLDERS Date : 3/24/2014 As of March 19, 2014 Resident Banks

THE PHILODRILL CORPORATION Page : 1 LIST OF STOCKHOLDERS Date : 3/24/2014 As of March 19, 2014 Resident Banks SHARES ISSUED SHARES & OUTSTANDING SUBSCRIBED NO. CTZN NAME ADDRESS RECEIVABLES 100365 PHILIPPINES ALLIED BANK TA #5342 ALLIED BANK BLDG., AYALA 2,535,750 AVE., MAKATI, MM 100558 PHILIPPINES ALLIED BANKING CORP. FOR THE C/O ALLIED BANKING CORP 5,333,125 A/C OF L. R ECIO & CO., INC. AYALA AVE, MAKATI, MM 125281 PHILIPPINES BPI-INVESTMENT CORP., 17TH FLR., BPI BLDG., 34,500 ACCOUNT #75-07 AYALA AVENUE MAKAT, METRO MANILA 151185 VIRGIN CBNA MLA A/C 6011800001 8741 PASEO DE ROXAS 80,000 ISLANDS, MAKATI CITY BRITISH 150641 PHILIPPINES CBTC TRUST DIV. A/C PIM-3087 COMTRUST BLDG., AYALA 134,090 AVE., MAKATI, MM 150671 Others CITIBANK MANILA F/A OR CITIBANK N.A. CITIBANK 37,692 CBNY/EMERGING MARKETS CENTER, PASEO DE ROXAS, FUND/CTC MAKATI, MM 150782 UNITED CITIBANK MANILA FOR A/C OF CITIBANK N.A., CITIBANK 134,090 STATES CITIBANK LONDON CENTER 8741 PASEO DE ROXAS, MAKATI, MM 150927 Others CITIBANK MLA. FOR A/C MERRILL CITIBANK BLDG, PASEO DE 196,666 LYNCH PIER CE FENNER & SMITH ROXAS MAKATI, MM 150671 Others CITIBANK, MANILA FOR A/C C/O CITIBANK, N.A. PASEO 670,450 CITIBANK LONDON SUB A/C DE ROXAS MAKATI, MM STOCKBROKER 225198 PHILIPPINES FEBTC A/C #4111-00048-7 8/F, FEBTC CENTER SEN. 885,750 GIL PUYAT AVE. MAKATI CITY 225198 PHILIPPINES FEBTC A/C PC80-050 2/F PACIFIC STAR BLDG. 766,622 MAKATI AVE. COR. GIL PUYAT AVE.