Kuwento Sa Bawat Kuwenta

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Scoping of Legislations on Climate Change and Natural Disasters Vis-À

Scoping of Legislations on Climate Change and Natural Disasters vis-à-vis Tenure Founded in 1979, ANGOC is a regional asso- ciation of national and regional networks of non-government organizations (NGOs) in Asia actively engaged in food security, agrarian reform, sustainable agriculture, participatory governance, and rural development. ANGOC network mem- Asian NGO Coalition for Agrarian Reform bers and partners work in 14 Asian countries with and Rural Development an effective reach of some 3,000 NGOs and com- 33 Mapagsangguni Street munity-based organizations (CBOs). ANGOC Sikatuna Village, Diliman actively engages in joint field programs and policy 1101 Quezon City, Philippines debates with national governments, intergovern- mental organizations (IGOs), and international P.O. Box 3107, QCCPO 1101, Quezon City, Philippines financial institutions (IFIs). Tel: +63-2 3510481 Fax: +63-2 3510011 Email: [email protected] ANGOC is the convenor of the Land Watch Asia URL: www.angoc.org (LWA) campaign. ANGOC is also a member of the International Land Coalition (ILC) and the Facebook: www.facebook.com/AsianNGOCoalition Twitter: https://twitter.com/ANGOCorg Global Land Tool Network (GLTN). Skype: asianngocoalition About the Authors Dr. Antonio Gabriel La Viña Atty. Joyce Melcar Tan He is a teacher, thinker, She currently consults lawyer, author, social with the Asian Devel- entrepreneur, and an opment Bank on Envi- environmental and ronmental Law in Asia human rights advocate. and teaches Natural He was Executive Resources and Envi- Director of the Manila Observatory from 2016 to ronmental Law, as well as International Climate 2017, Dean of the Ateneo School of Government Change Law at the Ateneo Law School. -

Filipino Ties the Official Newsletter of Cfo

4 TH QUARTER ISSUE October - December 2018 FILIPINO TIES THE OFFICIAL NEWSLETTER OF CFO www.cfo.gov.ph PHILIPPINES CELEBRATES THE MONTH OF OVERSEAS FILIPINOS AND THE INTERNATIONAL MIGRANTS DAY Next page --> IN THIS ISSUE National Capital Region’s Regional Development Philippines celebrates the Monthof Overseas Filipinos and Plan 2017-2022 launched, p.22 the International Migrants Day, p.1 Batangas celebrates Annual Migration Day; Localized Government Quality Body lauds CFO for Balinkbayan Website Launched, p.23 ISO 9001:2015 mark, p.16 Ilocos Region tackles Migration and Development CFO lauds US Government for returning from a gender lens, p.25 Balangiga Bells, p.18 The Municipality of Rosales, Pangasinan launches Sub-committee on International Migration and localized Balinkbayan website, p.26 Development (SCIMD) National-Regional meet CFO conducts capacity building trainings on the for the first time, p.20 Balinkbayan Project for Cebu City officials, p.27 December is the most joyous month of the FilTies Editorial Team year. In the Philippines, it is celebrated as the “Month of Overseas Filipinos” in honor of the significant contributions of the more than Editors: Rodrigo V. Garcia, Marita D. Apattad 10 million overseas Filipinos to Philippine Michelle Dawn Bande development and nation-building. In the global scene, the United Nations General Assembly Contributors: Andrea Luisa C. Anolin, Erwin Paul S. Cristobal, proclaimed December 18 as International Warner A. Dawal, Princess Mayumi Kaye Peralta, Migrants Day in 2000. Patricia Marie -

The Daily Dispatch

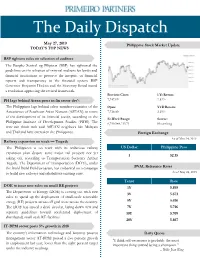

The Daily Dispatch Feb.May 2, 201727, 2019 Philippine Stock Market Update TODAY’S TOP NEWS BSP tightens rules on selection of auditors The Bangko Sentral ng Pilipinas (BSP) has tightened the guidelines on the selection of external auditors for banks and financial institutions to preserve the integrity of financial reports and transparency in the financial system. BSP Governor Benjamin Diokno said the Monetary Board issued a resolution approving the revised framework. Previous Close: 1 Yr Return: PH lags behind Asean peers in fin sector dev't 7,747.09 2.53% The Philippines lags behind other member-countries of the Open: YTD Return: Association of Southeast Asian Nations (ASEAN) in terms 7,718.80 3.19% of the development of its financial sector, according to the 52-Week Range: Source: Philippine Institute of Development Studies (PIDS). The 6,790.588,213.71 Bloomberg state-run think tank said ASEAN neighbors like Malaysia and Thailand have overtaken the Philippines. Foreign Exchange As of May 24, 2019 Railway expansion on track — Tugade The Philippines is on track with its ambitious railway US Dollar Philippine Peso expansion plan despite some major rail projects not yet 1 52.15 taking off, according to Transportation Secretary Arthur Tugade. The Department of Transportation (DOTr), under the Build Build Build program, has embarked on a campaign BVAL Reference Rates to build new railways and rehabilitate existing ones. As of May 24, 2019 Tenor Rate DOE to issue new rules on small RE projects 1Y 5.895 The Department of Energy (DOE) is coming out with new 3Y 5.673 rules to speed up the deployment of small-scale renewable energy (RE) projects across off-grid areas across the country. -

Souhrnná Terirotální Informace Filipíny

SOUHRNNÁ TERITORIÁLNÍ INFORMACE Filipíny Souhrnná teritoriální informace Filipíny Zpracováno a aktualizováno zastupitelským úřadem ČR v Manile (Filipíny) ke dni 10. 1. 2020 1:00 Seznam kapitol souhrnné teritoriální informace: 1. Základní charakteristika teritoria, ekonomický přehled (s.2) 2. Zahraniční obchod a investice (s.11) 3. Vztahy země s EU (s.19) 4. Obchodní a ekonomická spolupráce s ČR (s.22) 5. Mapa oborových příležitostí - perspektivní položky českého exportu (s.29) 6. Základní podmínky pro uplatnění českého zboží na trhu (s.41) 7. Kontakty (s.54) 1/62 http://www.businessinfo.cz/filipiny © Zastupitelský úřad ČR v Manile (Filipíny) SOUHRNNÁ TERITORIÁLNÍ INFORMACE Filipíny 1. Základní charakteristika teritoria, ekonomický přehled Filipíny jsou nejstarší demokracií v regionu jihovýchodní Asie s nadějně se rozvíjející ekonomikou s prozápadní kulturou. Země je jediným asijským státem s dominantním křesťanstvím (katolická církev, značný zájem o Pražské Jezulátko). Blízkost kultur, potenciál Filipín stát se v dohledné době jednou z 20 největších ekonomik světa a také schopnost ČR se v zemi prosazovat lépe než v tradičních asijských tygrech předjímá intenzitu vztahů a silný vzájemný zájem o spolupráci. MZV ČR proto podporuje rozšiřování spolupráce s Filipínami i na ostatní resorty mimo obvyklou zahraniční politiku, obchod a cestovní ruch. V současnosti se tak již rozvíjí spolupráce v resortech obchodu, financí, obrany, zemědělství, životního prostředí a školství. Podkapitoly: 1.1. Oficiální název státu, složení vlády 1.2. Demografické tendence: Počet obyvatel, průměrný roční přírůstek, demografické složení (vč. národnosti, náboženských skupin) 1.3. Základní makroekonomické ukazatele za posledních 5 let (nominální HDP/obyv., vývoj objemu HDP, míra inflace, míra nezaměstnanosti). Očekávaný vývoj v teritoriu s akcentem na ekonomickou sféru. -

Ayala Foundation 2009 Annual Report Shifting Paradigms

Ayala Foundation 2009 Annual Report Shifting Paradigms A teacher sits at her desk planning her next lesson. Her face brightens, as she thinks of a fresh approach to education—one that integrates technology, art and culture, and social awareness. Over the years, Ayala Foundation Inc. (AFI) has contributed significantly to transforming the face of education in the country. AFI has pioneered successful projects in improving the quality of public education, bringing technological tools to poor students, opening world-class facilities for art and culture, building awareness on the need to protect the environment, and encouraging social entrepreneurship. These projects have truly helped shift paradigms in education in the country. As it enters its 49th year, AFI reaffirms its commitment to take the spirit of innovation to people and communities it serves.This forward Contents annual report presents the many ground-breaking programs that AFI has introduced and sustained over the years. Even the unique layout design of the report reflects AFI’s creativity and inventiveness. 2 The Chairman’s Message 4 The President’s Message 6 At a Glance 16 Operational Highlights 38 Q& A with the President 40 The Year Ahead 42 2009 Board of Trustees bbeginegin 44 Ayala Foundation Management and Staff 2009 45 Report of Independent Auditors 80 Acknowledgments 87 Directory 88 Mission and Vision Dear stakeholders, We at Ayala Foundation are aware of the enormity of our mission: to eradicate the myriad forms that poverty takes. Over the last 48 years, we have worked hard to design and implement programs in areas where we could maximize our reach and create enormous impact. -

Philip Arnold P. Tuaño

Philip Arnold P. Tuaño ORGANIZATIONAL EXPERIENCE YEARS IN SERVICE ADDRESS Independent Board • 3 years 96 Scout Fernandez, Barangay Sacred Heart, Quezon City DUTIES AS BOARD TRUSTEE ▪ Attends Board and Committee meetings. ▪ Actively participates to the formulation and/or review of KMBA’s strategic directions PHONE and development plans. 639285214334 ▪ Review and approve operational, financial reports and other critical information related to the management of the association. ▪ Participates in any decision-making activities, conduct of performance assessment based on operational and financial targets vs actual achievement, addresses conflict of EMAIL interests, and ensures that the association’s risks are within threshold and are [email protected] acceptable. ▪ Oversee the day to day management activities. ▪ Introduces new policies, standards and procedures for purposes of organizational development. ▪ Approves and ratify management proposals and/or recommendations, policies, appointments, events, and activities. ▪ Attend seminars, program development programs, and related trainings necessary for Board Trustees. TRAININGS ATTENDED 1. Governance& anti money laundering act workshop June 5-7, 2019, Manila Prince Hotel 2. Management Forum July 22-24, 2019 at B Hotel 3. Leadership training January 26-27 Bayview Park Hotel 4. National Microinsurance Forum January 30, 2020 5. Investing in the time of COVID 19 April 17, 2020 6. Briefer on ARISE Philippine Act July 6, 2020 7. Learning session on Social Media Marketing 101 July 27, 2020 8. Webinar on Progreso Bond July 30, 2020 9. Briefer on Train Package 4 PIFITA August 7, 2020 10. Enhancing Mi-MBAs performance management system Sept 7, 2020 11. Learning Session-Center Meeting and social distancing Sept 21, 2020 EDUCATION 2015 • Ph. -

Infusing Reform in Elections

INFUSING REFORM IN ELECTIONS The Partisan Electoral Engagement of Reform Movements in Post-Martial Law Philippines Ateneo School of Government (ASoG) Paciico Ortiz Hall Fr. Arrupe Road, Social Development Complex Ateneo de Manila University Campus Katipunan Avenue, Loyola Heights Quezon City 1108 Telefax : (632) 920-29-20 Local line : (632) 426-60-01 local 4644 Email : [email protected] Website : www.asg.ateneo.edu Friedrich-Ebert-Stiftung (FES) Philippine Ofice Unit 2601, Discovery Centre #25 ADB Avenue, Ortigas Center Pasig City 1600 Tel : (632) 637-71-86 | (632) 634-69-19 Fax : (632) 632-0697 Website : www.fes.org.ph Printed and bound in the Philippines INFUSING REFORM IN ELECTIONS The Partisan Electoral Engagement of Reform Movements in Post-Martial Law Philippines JOY ACERON Case Writers RAFAELA MAE DAVID GLENFORD LEONILLO VALERIE BUENAVENTURA POLITICAL DEMOCRACY AND REFORM (PODER) Infusing Reform in Elections The Partisan Electoral Engagement of Reform Movements in Post-Martial Law Philippines © 2012 Ateneo School of Government (ASoG) Friedrich-Ebert-Stiftung (FES) Philippine Ofice The views expressed in this book are those of the authors and do not necessarily represent the views of ASoG and FES. ISBN: 978-971-92495-8-0 All rights reserved. No part of this book may be used or reproduced in any manner whatsoever without written permission except in the case of brief quotations embodied in critical articles and reviews. Photos, news clippings, video grabs, newspaper and Internet stories used are copyright of their authors -

Republic of the Philippines Strengthening Resilience, Fostering Inclusive Growth

Republic of the Philippines Strengthening Resilience, Fostering Inclusive Growth Disclaimer: If you are not the intended recipient, any unauthorized disclosure, copying, dissemination or use of any of the information is strictly prohibited. This presentation contains data sourced from various Philippine government, multilateral/bilateral and private sector websites/reports as of 15 March 2019. These sources have been cited where possible. Table of Contents I. Strengthened Credit Profile 3 II. Favorable Macroeconomic Trends 6 III. Demonstrated External Resiliency 12 IV. Sound and Stable Financial System 15 V. Sound and Strengthened Government Finances 17 VI. Accelerated Infrastructure Development 24 VII. Firm Institutional Foundations Through Structural Reforms 27 VIII. Socioeconomic Agenda of the Duterte Administration 31 IX. The President and the Economic Team 33 2 Strengthened Credit Profile Duterte Administration: Reform-Minded Leadership Focused on Delivering Results Transformative policies anchored on domestic-led growth and continuing structural reforms One of the fastest growing economies in the Asia Pacific region • Rapid and more broad-based economic growth o GDP growth of 6.2% in 2018 led by investments, which contributed 4.0 ppt to growth Continued sound o 20 years of uninterrupted economic expansion macroeconomic Moderate inflation pressures in 2018 Resilient external payments position amid global uncertainties management yields Structural current account flows from steady remittances (3.17% yoy in 2018 and 4.4% yoy in Jan 2019), and rising revenues from IT-BPO (2.9% yoy in 2018) and strong results tourism sectors (4.2% yoy in 2018) Sound banking system Business optimism in the Philippines highest in Southeast Asia and 6th among 35 economies covered according to Grant Thornton’s International Business Report H2 2018 Economic Update Increasing net FDIs on account of improved investment environment. -

Information As of 1 July 2019 Has Been Used in Preparation of This Directory

Information as of 1 July 2019 has been used in preparation of this directory. PREFACE Key To Abbreviations Adm. Admiral Admin. Administrative, Administration Asst. Assistant Brig. Brigadier Capt. Captain Cdr. Commander Cdte. Comandante Chmn. Chairman, Chairwoman Col. Colonel Ctte. Committee Del. Delegate Dep. Deputy Dept. Department Dir. Director Div. Division Dr. Doctor Eng. Engineer Fd. Mar. Field Marshal Fed. Federal Gen. General Govt. Government Intl. International Lt. Lieutenant Maj. Major Mar. Marshal Mbr. Member Min. Minister, Ministry NDE No Diplomatic Exchange Org. Organization Pres. President Prof. Professor RAdm. Rear Admiral Ret. Retired Sec. Secretary VAdm. Vice Admiral VMar. Vice Marshal Afghanistan Last Updated: 24 Jun 2019 Pres. Ashraf GHANI CEO Abdullah ABDULLAH, Dr. First Vice Pres. Abdul Rashid DOSTAM Second Vice Pres. Sarwar DANESH First Deputy CEO Khyal Mohammad KHAN Min. of Agriculture, Irrigation, & Livestock Nasir Ahmad DURRANI Min. of Border & Tribal Affairs Gul Agha SHERZAI Min. of Commerce & Industry Ajmal AHMADY (Acting) Min. of Counternarcotics Salamat AZIMI Min. of Defense Asadullah KHALID (Acting) Min. of Economy Mohammad Mustafa MASTOOR Min. of Education Mohammad Mirwais BALKHI (Acting) Min. of Energy & Water Tahir SHARAN (Acting) Min. of Finance Mohammad Humayun QAYOUMI (Acting) Min. of Foreign Affairs Salahuddin RABBANI Min. of Hajj & Islamic Affairs Faiz Mohammad OSMANI Min. of Higher Education Abdul Tawab BALAKARZAI (Acting) Min. of Information & Culture Hasina SAFI (Acting) Min. of Interior Mohammad Masood ANDARABI (Acting) Min. of Justice Abdul Basir ANWAR Min. of Martyred, Disabled, Labor, & Social Affairs Sayed Anwar SADAT (Acting) Min. of Mines & Petroleum Nargis NEHAN (Acting) Min. of Parliamentary Affairs Faruq WARDAK Min. of Public Health Ferozuddin FEROZ Min. -

TOC 2018 Directory.Indd

TABLE OF CONTENTS I. THE NATIONAL GOVERNMENT A. EXECUTIVE BRANCH Offi ce of the President 3 Offi ce of the Vice President 6 Presidential Communications Operations Offi ce 7 Other Executive Offi ces 9 Department of Agrarian Reform 13 Department of Agriculture 16 Department of Budget and Management 20 Department of Education 26 Department of Energy 30 Department of Environment and Natural Resources 32 Department of Finance 36 Department of Foreign Aff airs 39 Department of Health 48 Department of Information and Communications Technology 53 Department of the Interior and Local Government 55 Department of Justice 59 Department of Labor and Employment 62 Department of National Defense 66 Department of Public Works and Highways 68 Department of Science and Technology 71 Department of Social Welfare and Development 76 Department of Tourism 80 Department of Trade and Industry 83 Department of Transportation 87 National Economic and Development Authority 90 Constitutional Offi ces l Civil Service Commission 97 l Commission on Audit 99 l Commission on Elections 102 l Commission on Human Rights 104 l Offi ce of the Ombudsman 106 Government-Owned and/or-Controlled Corporations 111 State Universities and Colleges 120 B. LEGISLATIVE BRANCH Senate of the Philippines 135 House of Representatives 140 C. JUDICIAL BRANCH Supreme Court of the Philippines 153 Court of Appeals 154 Court of Tax Appeals 156 Sandiganbayan 157 II. LOCAL GOVERNMENT UNITS Provincial Governments 161 City Governments 167 Municipal Governments 175 Autonomous Region in Muslim Mindanao 228 III. DIPLOMATIC AND CONSULAR MISSIONS 235 IV. UNITED NATIONS AGENCIES AND OTHER 260 INTERNATIONAL ORGANIZATIONS EXECUTIVE BRANCH EXECUTIVE BRANCH The Executive Branch implements national policies and performs the executive and administrative functions of the National Government. -

Housing ‘Super Body’

NATIONAL HUMAN SETTLEMENTS BOARD Housing ‘super body’ CONFIRMED National Shelter Month: Marawi City: From P7 DHSUD runs after scammers P12 ashes to progress P28 Editor’s Note 3 It is with great pleasure to welcome you, dear readers, to the 2nd issue of The Shelter. Much has happened since June and we cannot wait to share all the Contents Secretary’s Corner Department of Human Settlements and Urban Development has accom plished in very little time. Topping it off is the inaugural meeting of the National Human Settle 3 SECRETARY’S CORNER ments Board (NHSB) in October, which coinciding with the celebration of the 4 - 5 PROFILES Banner 2020 for DHSUD National Shelter Month, which is our main story in this issue. COMMUNITY BUILDING his year, the Department of Human standards in public service, we signed a And of course, who can forget the confirmation of our good Secretary 6 DHSUD-SHDA partnership Settlements and Urban Develop- Joint Memorandum Circular (JMC) with Eduardo Del Rosario, who got the Commission on Appointment’s nod last Resettlement of PAPs in railway projects underway November to become the first-ever head of the DHSUD. Tment (DHSUD) had its hands full as the Anti-Red Tape Authority (ARTA) Our private partners from SHDA (Subdivision and Housing Developers FEATURE it launched several projects and programs that streamlined the documentation st Association) is also with us for the 2nd issue highlighting our partnership. 7 Making history: SEDDR is 1 ever DHSUD chief despite the limitations brought about processes for common towers to improve DHSUD joins ‘Build Back Better’ Task Force Much like before, we received updates from our Regional Offices and Key by the COVID-19 pandemic, all with the the country’s Information and Commu- Shelter Agencies on their past and current initiatives. -

CALD Hong Kong Conference

CONFERENCE REPORT TABLE OF CONTENTS Concept Paper 1 Programme of Events 6 Profile of Speakers and Session Chairs 16 Executive Summary 28 Conference Report CALD-EFN Asia Joint Session Emily Lau 30 Saumura Tioulong 32 Sin Chung-kai 33 Parth Shah 33 Jay Kun Yoo 33 Sethaput Suthiwart-Narueput 34 CALD-LI Conference Juli Minoves-Triquell 35 Oyun Sanjaasuren 36 Martin Lee 37 World Café on the Conference Theme 37 Updates on Political Developments in Taiwan, Thailand, and Hong Kong Bi-khim Hsiao 39 Kasit Piromya 41 James To 42 CALD Women’s Caucus Seminar on Migrant Workers Monovithya Kem 43 Henedina Abad 44 Session on Migrant Workers Rights as Human Rights Chito Gascon 46 Rajiva Wijesinha 47 Open Forum 48 UN Mechanism on Protection of Migrant Workers 49 CONCEPT PAPER The heart of the liberal philosophy is a belief in the dignity of the individual, in his freedom to make the most of his capacities and opportunities according to his own lights…This implies a belief in the equality of man in one sense; in their inequality in another. Milton Friedman Capitalism and Freedom (1962) Recipient of Nobel Prize in Economic Sciences (1976) …inequality is not inevitable… It is not the result of the laws of nature or the laws of economics. Rather, it is something that we create, by our policies, by what we do… It is plain that the only true and sustainable prosperity is shared prosperity. Joseph Stiglitz Speech in the AFL-CIO Convention (2013) Recipient of Nobel Prize in Economic Sciences (2001) …liberal economic policies, especially free trade, have been much more successful at producing lasting growth than policies of state intervention.