2013 Annual Report About the Cover

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Information Statement for 2013 Annual Stockholders Meeting

Via ODiSy March 26, 2013 PHILIPPINE STOCK EXCHANGE, INC. Tower One and Exchange Plaza Ayala Triangle, Ayala Avenue Makati City Attention: Ms. Janet A. Encarnacion Head, Disclosures Department Ms. Christina Marie C. Fortes Assistant Manager, Disclosure Department Re: Definitive Information Statement (DIS) ============================= Ladies: We transmit with this letter the Definitive Information Statement (DIS) of BDO Unibank, Inc., which we submitted yesterday, 25 March 2013 at the Securities and Exchange Commission. Thank you. Very truly yours, ELMER B. SERRANO Corporate Information Officer COVER SHEET 3 4 0 0 1 S.E.C. Registration Number B D O U N I B AN K , I N C . (Company’s Full Name) B D O C o r p o r a t e C e n t e r 7 8 9 9 M a k a t i A v e n u e M a k a t i C i t y (Business Address: No. Street/ City/ Town/ Province) Atty. Elmer B. Serrano 687.1195 Contact Person Company Telephone Number 1 2 3 1 Last Friday of May Definitive Information Month Day Month Day Statement Fiscal Year FORM TYPE Annual Meeting Secondary License Type, If Applicable C F D Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings Total No. of Stockholders Domestic Foreign To be accompanied by SEC Personnel concerned File Number Document I.D. STAMPS NOTICE OF ANNUAL MEETING OF STOCKHOLDERS DEFINITIVE INFORMATION STATEMENT A. GENERAL INFORMATION Item 1. Date, Time and Place of Meeting of Security Holders (a) Date : April 19, 2013, Friday Time : 2:00 p.m. -

Country Diagnostic: Philippines

Philippines BETTERTHANCASH COUNTRY DIAGNOSTIC ALLIANCE Empowering People Through Electronic Payments July 2015 Development Results Focused Research Program Country Diagnostic: Philippines by James Hokans, Bankable Frontier Associates Philippines BETTERTHANCASH COUNTRY DIAGNOSTIC ALLIANCE Empowering People Through Electronic Payments July 2015 Development Results Focused Research Program Country Diagnostic: Philippines by James Hokans, Bankable Frontier Associates BETTERTHANCASH ALLIANCE Empowering People Through Electronic Payments INTRODUCTION TO THE BETTER THAN CASH ALLIANCE The Better Than Cash Alliance (the Alliance) is a partnership of governments, companies, and international organizations that accelerates the transition from cash to digital payments in order to drive inclusive growth and reduce poverty. Shifting from cash to digital payments has the potential to improve the lives of low-income people, particularly women, while giving governments, companies and international organizations a more transparent, time- and cost-efficient, and often safer means of making and receiving payments. We partner with governments, companies, and international organizations that are the key drivers behind the transition to make digital payments widely available by: 1. Advocating for the transition from cash to digital payments in a way that advances financial inclusion and promotes responsible digital finance. 2. Conducting research and sharing the experience our members to inform strategies for making the transition 3. Catalyzing the development -

No. Company Star

Fair Trade Enforcement Bureau-DTI Business Licensing and Accreditation Division LIST OF ACCREDITED SERVICE AND REPAIR SHOPS As of November 30, 2019 No. Star- Expiry Company Classific Address City Contact Person Tel. No. E-mail Category Date ation 1 (FMEI) Fernando Medical Enterprises 1460-1462 E. Rodriguez Sr. Avenue, Quezon City Maria Victoria F. Gutierrez - Managing (02)727 1521; marivicgutierrez@f Medical/Dental 31-Dec-19 Inc. Immculate Concepcion, Quezon City Director (02)727 1532 ernandomedical.co m 2 08 Auto Services 1 Star 4 B. Serrano cor. William Shaw Street, Caloocan City Edson B. Cachuela - Proprietor (02)330 6907 Automotive (Excluding 31-Dec-19 Caloocan City Aircon Servicing) 3 1 Stop Battery Shop, Inc. 1 Star 214 Gen. Luis St., Novaliches, Quezon Quezon City Herminio DC. Castillo - President and (02)9360 2262 419 onestopbattery201 Automotive (Excluding 31-Dec-19 City General Manager 2859 [email protected] Aircon Servicing) 4 1-29 Car Aircon Service Center 1 Star B1 L1 Sheryll Mirra Street, Multinational Parañaque City Ma. Luz M. Reyes - Proprietress (02)821 1202 macuzreyes129@ Automotive (Including 31-Dec-19 Village, Parañaque City gmail.com Aircon Servicing) 5 1st Corinthean's Appliance Services 1 Star 515-B Quintas Street, CAA BF Int'l. Las Piñas City Felvicenso L. Arguelles - Owner (02)463 0229 vinzarguelles@yah Ref and Airconditioning 31-Dec-19 Village, Las Piñas City oo.com (Type A) 6 2539 Cycle Parts Enterprises 1 Star 2539 M-Roxas Street, Sta. Ana, Manila Manila Robert C. Quides - Owner (02)954 4704 iluvurobert@gmail. Automotive 31-Dec-19 com (Motorcycle/Small Engine Servicing) 7 3BMA Refrigeration & Airconditioning 1 Star 2 Don Pepe St., Sto. -

The State of Digital Payments in the Philippines (Released in 2015) Found That Adoption Had Been Limited

COUNTRY DIAGNOSTIC The State of Digital Payments in the Philippines DECEMBER 2019 PHILIPPINES Authors Project Leads: Keyzom Ngodup Massally, Rodrigo Mejía Ricart Technical authors: Malavika Bambawale, Swetha Totapally, and Vineet Bhandari Cover photo: © Better Than Cash Alliance/Erwin Nolido 1 FOREWORD Our country was one of the first to pioneer digital payments nearly 20 years ago. Recognizing the untapped market potential and the opportunity to foster greater access to financial inclusion, the Bangko Sentral ng Pilipinas (BSP) has worked, hand in hand, with the government and the leaders across financial, retail, and regulatory sectors to boost digital payments. Over the past three years, since the launch of the first digital payments diagnostic, the Philippines has experienced remarkable progress toward building an inclusive digital payments ecosystem. In 2013, digital payments accounted for only 1% of the country’s total transaction volume. In 2018, this follow through diagnostic study showed that the volume of digital payments increased to 10% corresponding to 20% share in the total transaction value. These numbers speak of significant progress and success. I am optimistic that e-payments will gain further momentum as we have laid the necessary building blocks to accelerate innovation and inclusive growth over the next few years. Notably, Filipino women are ahead of men in the uptake of digital payments, placing us ahead of global standards. The rise of fintech and their solutions are starting to play a transformative role, as we can see from the rapidly-growing adoption of the emerging QR codes for digital transactions. I am confident that the BSP has built a good digital foundation and is well positioned to leverage fintech in increasing the share of digital payments toward a cash- lite Philippines. -

FY 2009 (Annual)

EXECUTIVE SUMMARY METROPOLITAN MANILA DEVELOPMENT AUTHORITY CY 2009 ANNUAL ACCOMPLISHMENT REPORT Metro Gwapo, MMDA’s flagship program, has come a long way since its inception a couple of years ago. Given the glaring blight in many areas of the Metropolis, it is a pleasant surprise to see that a substantial physical change for the better has come upon Metro Manila. Inch by painful inch, Metro Manila is slowly turning into a livable and healthy city as envisioned by the leaders of this prime metropolis, both past and present. Though much remains to be done, we have taken the baby steps. With the expert use of the principle utilizing outer change to bring about inner change, MMDA has embarked on the process of social engineering. Undeniably the opposite process of starting from within to realize outer change is faster but, owing to the psychological immaturity of most of our countrymen, the principle of the outer to the inner is deemed more suitable. Here, the use of visuals help impart the lessons to a largely unthinking public. Among the more important projects for CY 2009 are the following: SOCIAL SERVICES PGMA Workers’ Inn (aka) Gwapotel Meant to ease the difficulties of the workers whose homes are far from the Metropolis, the Gwapotel or Workers Inn serves as a temporary sleeping and bathing quarters for a variety of clients (i.e. government employees, laborers, security guards, vendors, seamen and seminar / convention participants, among others. As of 2009, the MMDA operated two such inns, one in Port Area and another in Abad Santos Tondo, Manila. -

Domestic Branch Directory BANKING SCHEDULE

Domestic Branch Directory BANKING SCHEDULE Branch Name Present Address Contact Numbers Monday - Friday Saturday Sunday Holidays cor Gen. Araneta St. and Aurora Blvd., Cubao, Quezon 1 Q.C.-Cubao Main 911-2916 / 912-1938 9:00 AM – 4:00 PM City 912-3070 / 912-2577 / SRMC Bldg., 901 Aurora Blvd. cor Harvard & Stanford 2 Q.C.-Cubao-Harvard 913-1068 / 912-2571 / 9:00 AM – 4:00 PM Sts., Cubao, Quezon City 913-4503 (fax) 332-3014 / 332-3067 / 3 Q.C.-EDSA Roosevelt 1024 Global Trade Center Bldg., EDSA, Quezon City 9:00 AM – 4:00 PM 332-4446 G/F, One Cyberpod Centris, EDSA Eton Centris, cor. 332-5368 / 332-6258 / 4 Q.C.-EDSA-Eton Centris 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM EDSA & Quezon Ave., Quezon City 332-6665 Elliptical Road cor. Kalayaan Avenue, Diliman, Quezon 920-3353 / 924-2660 / 5 Q.C.-Elliptical Road 9:00 AM – 4:00 PM City 924-2663 Aurora Blvd., near PSBA, Brgy. Loyola Heights, 421-2331 / 421-2330 / 6 Q.C.-Katipunan-Aurora Blvd. 9:00 AM – 4:00 PM Quezon City 421-2329 (fax) 335 Agcor Bldg., Katipunan Ave., Loyola Heights, 929-8814 / 433-2021 / 7 Q.C.-Katipunan-Loyola Heights 9:00 AM – 4:00 PM Quezon City 433-2022 February 07, 2014 : G/F, Linear Building, 142 8 Q.C.-Katipunan-St. Ignatius 912-8077 / 912-8078 9:00 AM – 4:00 PM Katipunan Road, Quezon City 920-7158 / 920-7165 / 9 Q.C.-Matalino 21 Tempus Bldg., Matalino St., Diliman, Quezon City 9:00 AM – 4:00 PM 924-8919 (fax) MWSS Compound, Katipunan Road, Balara, Quezon 927-5443 / 922-3765 / 10 Q.C.-MWSS 9:00 AM – 4:00 PM City 922-3764 SRA Building, Brgy. -

University of the Philippines Manila

UNIVERSITY OF THE PHILIPPINES MANILA BIDS AND AWARDS COMMITTEE 2 21 September 2020 Bid Bulletin No. 1 Please be informed of the following ammendments : A. Updated Checklist of Bid documents B. List of pick up and drop off points per route This Bid Bulletin is issued to modify or amend items in the Bidding Documents of the project titled “Provision of Transportation/Shuttle Services for UP Manila Employees, University of the Philippines Manila.” This shall form an integral part of the Bidding Documents. For guidance and information of all concerned. DANILO L. MAGTANONG, DDM, MHPEd BAC2, Chair 8/F Philippine General Hospital Complex, Taft Avenue, Manila 1000, Philippines Tel: (632) 8814-1224 ● Email: [email protected] UNIVERSITY OF THE PHILIPPINES MANILA BIDS AND AWARDS COMMITTEE 2 CHECKLIST OF BID DOCUMENTS Project Title: PROVISION OF TRANSPORTATION/SHUTTLE SERVICES FOR UP MANILA EMPLOYEES ABC: Php6,800,000.00 DETAILS/DESCRIPTION OF BID DOCUMENTS ENVELOPE NO. 1a (Eligibility Requirements) Legal Documents 1. PhilGEPS Platinum Membership 2. DTI Business Name Registration or SEC Registration with Articles Incorporation or Cooperative Development Authority (CDA) (whichever is applicable) 3. Mayor’s permit issued by the city or municipality where the principal place of business of the prospective bidder is located 4. Current Tax Clearance Technical Documents 1. Statement of the Bidder’s ALL ongoing government and private contracts, including contracts awarded but not yet started, if any, whether similar or not similar in nature and complexity to the contract to be bid. The statement shall be supported by notices of award, and/or notices to proceed issued by the bidder’s clients. -

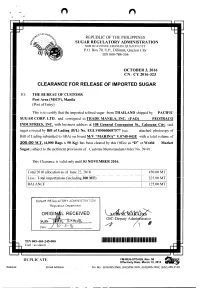

ORIGI L RECEIVED WNW .F,401Ts CLEARANCE for RELEASE OF

, , O-F A G '0 041 ,4 .,.‘4'_ & REPUBLIC OF THE PHILIPPINES a.gr - c- a1.0 .... SUGAR REGULATORY ADMINISTRATION NORTH AVENUE. DILIMAN, QUEZON CITY P.O. Box 70. U.P., Diliman, Quezon City TIN 000-784-336 OCTOBER 3, 2016 CN : CY 2016-323 CLEARANCE FOR RELEASE OF IMPORTED SUGAR THE BUREAU OF CUSTOMS Port Area (MICP), Manila (Port of Entry) This is to certify that the imported refined sugar from THAILAND shipped by PACIFIC SUGAR CORP. LTD. and consigned to TRADE MANILA, INC. (FAO) PEOTRACO INDUSTRIES, INC. with business address at 108 General Concepcion St., Caloocan City, said sugar covered by Bill of Lading (B/L) No. EGLV050600687577 (see attached photocopy of Bill of Lading submitted to SRA) on board MN "MARINA" V.0740-043E with a total volume of 200.00 M.T. (4,000 Bags x 50 Kg) has been cleared by this Office as "D" or World Market Sugar, subject to the pertinent provisions of Customs Memorandum Order No. 39-91. This Clearance is valid only until 03 NOVEMBER 2016. Total 2016 allocation as of June 22, 2016 450.00 MT Less : Total importations (including 200 MT) 325.00 MT BALANCE 125.00 MT SUGAR REGULATORY ADMINISTRATION Regulation Department ORIGI L RECEIVED 01C-Deputy Admi strator WNW .F,401ts Date - 3 - TIN 005-469-245-000 111111111 41111111111111111111111111111111111 Encl : as stated DL-PLICATE FM-REG-STD-026, Rev. 00 Effectivity Date: March 12, 2015 Website: • , Email Address: Tel. No.: (632)455-2566, (632)455-3376, (632)455-7402, (632) 455-2135 • foN REPUBLIC OF THE PHILIPPINES SUGAR REGULATORY ADMINISTRATION NORTH AVENUE, DILIMAN. -

List of BDO Branches Authorized to Exchange Foreign Currencies As of (March 8, 2021)

List of BDO Branches Authorized to Exchange Foreign Currencies as of (March 8, 2021) I. US Dollar (USD) – All BDO Branches II. Other Currencies • Australian Dollar (AUD) • Japanese Yen (JPY) • Bahrain Dinar (BHY) • Korean Won (KRW) • British Pound (GBP) • Saudi Rial (SAR) • Brunei Dollar (BND) • Singapore Dollar (SGD) Chinese Yuan (CNY) • Canadian Dollar (CAD) • Swiss Frank (CHF) • Euro (EUR) • Taiwan Dollar (TWD) • Hongkong Dollar (HKD) • Thailand Baht (THB) • Indonesian Rupiah (IDR) • UAE Dirham (AED) 1 A Place - Coral Way 1 A. Arnaiz – Paseo 2 A. Bonifacio Ave. - Balintawak 2 A. Arnaiz-San Lorenzo Village 3 A. Santos - St. James 3 A. Santos - St. James 4 Acropolis - E. Rodriguez Jr. 4 ADB Avenue Ortigas 5 ADB Avenue Ortigas 5 Alabang Hills 6 Alabang - Madrigal Ave 6 Alabang - Madrigal Ave 7 Angeles City – Miranda 7 Araneta Center Ali Mall II 8 Angono – M.L. Quezon Avenue 8 Arranque 9 Arranque 9 Asia Tower - Paseo 10 Arranque - T. Alonzo 10 Aurora Blvd. - Broadway Centrum 11 Asia Tower - Paseo 11 Aurora Blvd - Notre Dame 12 Aurora Blvd - Broadway Centrum 12 Aurora Blvd. - Yale 13 Aurora Blvd - Notre Dame 13 Ayala Alabang - Richville Center 14 Aurora Blvd. - Yale 14 Ayala Avenue - People Support 15 Ayala Alabang - Richville Center 15 Ayala Avenue - SGV1 Bldg 16 Ayala Avenue - People Support 16 Ayala Triangle 1 17 Ayala Avenue - SGV1 Bldg 17 Baclaran 18 Ayala – Rufino 18 Bacolod – Araneta 19 Baclaran 19 Bacolod - Capitol Shopping 20 Bacolod – Araneta 20 Baguio - Session Road 21 Bacolod - Capitol Shopping 21 Baguio - Marcos Highway Centerpoint 22 Bacolod – Gonzaga 22 Banawe - Agno 23 Bacoor - Aguinaldo Highway 23 Banawe - Amoranto 24 Bagtikan – Chino Roces Avenue 24 Batangas - Sto. -

List of BDO Branches Authorized to Open Chinese Yuan (CNY) Accounts (As of March 8, 2021)

List of BDO Branches Authorized to Open Chinese Yuan (CNY) Accounts (as of March 8, 2021) 1 A Place - Coral Way 173 Malabon 2 A. Bonifacio Ave. - Balintawak 174 Malabon - Gov. Pascual 3 A. Santos - St. James 175 Malabon - Rizal Avenue 4 Acropolis - E. Rodriguez Jr. 176 Malanday - MacArthur Highway 5 ADB Avenue Ortigas 177 Malate - Adriatico 6 Alabang - Madrigal Ave 178 Manila – Otis 7 Angeles City-Miranda 179 Marcos Highway 8 Angono – M.L. Quezon Avenue 180 Marikina - Concepcion 9 Arranque 181 Marikina - Gil Fernando Ave. 10 Arranque - T. Alonzo 182 Marikina - JP Rizal 11 Asia Tower - Paseo 183 Marulas - McArthur Highway 12 Aurora Blvd - Broadway Centrum 184 Masangkay 13 Aurora Blvd - Notre Dame 185 Masangkay - Luzon St. 14 Aurora Blvd. - Yale 186 Masangkay – CM Recto 15 Ayala Alabang - Richville Center 187 Mayon 16 Ayala Avenue - People Support 188 Mayon - Amoranto 17 Ayala Avenue - SGV1 Bldg 189 Mayon - N. Roxas 18 Ayala-Rufino 190 Mezza Residences 19 Baclaran 191 Monumento 20 Bacolod – Araneta 192 Munoz - Roosevelt 21 Bacolod - Capitol Shopping 193 N. Domingo - Araneta Avenue 22 Bacolod – Gonzaga 194 N. Domingo – M. Paterno 23 Bacoor - Aguinaldo Highway 195 NAIA 1 24 Bagtikan – Chino Roces Avenue 196 Navotas 25 Baguio – Luneta 197 Newport City 26 Baguio – Marcos Highway Centerpoint 198 OneE – comCenter 27 Balubaran - MacArthur Highway 199 Ongpin 28 Banawe - Agno 200 Ongpin - T. Alonzo 29 Banawe - Amoranto 201 Ongpin – Tomas Mapua 30 Banawe - Kitanlad 202 Ortigas - Exchange Road 31 Banawe - N. Roxas 203 Ortigas – Octagon Centre 32 Batangas - P. Burgos 204 Ortigas Avenue 33 Batangas - Sto. Tomas 205 Ortigas Avenue Ext. -

List of Ecpay Cash-In Or Loading Outlets and Branches

LIST OF ECPAY CASH-IN OR LOADING OUTLETS AND BRANCHES # Account Name Branch Name Branch Address 1 ECPAY-IBM PLAZA ECPAY- IBM PLAZA 11TH FLOOR IBM PLAZA EASTWOOD QC 2 TRAVELTIME TRAVEL & TOURS TRAVELTIME #812 EMERALD TOWER JP RIZAL COR. P.TUAZON PROJECT 4 QC 3 ABONIFACIO BUSINESS CENTER A Bonifacio Stopover LOT 1-BLK 61 A. BONIFACIO AVENUE AFP OFFICERS VILLAGE PHASE4, FORT BONIFACIO TAGUIG 4 TIWALA SA PADALA TSP_HEAD OFFICE 170 SALCEDO ST. LEGASPI VILLAGE MAKATI 5 TIWALA SA PADALA TSP_BF HOMES 43 PRESIDENTS AVE. BF HOMES, PARANAQUE CITY 6 TIWALA SA PADALA TSP_BETTER LIVING 82 BETTERLIVING SUBD.PARANAQUE CITY 7 TIWALA SA PADALA TSP_COUNTRYSIDE 19 COUNTRYSIDE AVE., STA. LUCIA PASIG CITY 8 TIWALA SA PADALA TSP_GUADALUPE NUEVO TANHOCK BUILDING COR. EDSA GUADALUPE MAKATI CITY 9 TIWALA SA PADALA TSP_HERRAN 111 P. GIL STREET, PACO MANILA 10 TIWALA SA PADALA TSP_JUNCTION STAR VALLEY PLAZA MALL JUNCTION, CAINTA RIZAL 11 TIWALA SA PADALA TSP_RETIRO 27 N.S. AMORANTO ST. RETIRO QUEZON CITY 12 TIWALA SA PADALA TSP_SUMULONG 24 SUMULONG HI-WAY, STO. NINO MARIKINA CITY 13 TIWALA SA PADALA TSP 10TH 245- B 1TH AVE. BRGY.6 ZONE 6, CALOOCAN CITY 14 TIWALA SA PADALA TSP B. BARRIO 35 MALOLOS AVE, B. BARRIO CALOOCAN CITY 15 TIWALA SA PADALA TSP BUSTILLOS TIWALA SA PADALA L2522- 28 ROAD 216, EARNSHAW BUSTILLOS MANILA 16 TIWALA SA PADALA TSP CALOOCAN 43 A. MABINI ST. CALOOCAN CITY 17 TIWALA SA PADALA TSP CONCEPCION 19 BAYAN-BAYANAN AVE. CONCEPCION, MARIKINA CITY 18 TIWALA SA PADALA TSP JP RIZAL 529 OLYMPIA ST. JP RIZAL QUEZON CITY 19 TIWALA SA PADALA TSP LALOMA 67 CALAVITE ST. -

Ready for the Road Promo

READY FOR THE ROAD PROMO LIST OF PARTICIPATING STATIONS Shell SITE NAME STATION ADDRESS SHOC+ Select deli2go SH EDSA CALOOCAN QC BOUND COSS 472 EDSA CALOOCAN CITY ✔ SH 1ST & 2ND AVE RAE CAL COSS RIZAL AVE EXT GRACE PARK CALOOCAN CITY ✔ SH KALAW DEL PILAR COSS 7 TM KALAW COR MH DEL PILAR ST ERMI MANILA CITY SH MORIONES TONDO MANILA COSS MORRIONES COR JUAN NOLASCO TONDO MANILA CITY SH LOPEZ BLVD NAVOTAS COSS 69 HONORIO LOPEZ BOULEVARD NBBS NAVOTAS CITY SH 8TH 9TH AVE B SERRANO COSS 67 8TH AND 9TH AVE B SERRANO ST CALOOCAN CITY ✔ SH J ABAD SANTOS TECSON COSS 2560 JOSE ABAD SANTOS COR TECSON TONDO MANILA CITY ✔ SH UNITED NATIONS PEREZ COSS UN AVE COR PEREZ ST PACO MANILA CITY ✔ ✔ SH JUAN LUNA DEL FIERRO COSS V DEL FIERRO ST GAGALANGIN TONDO MANILA CITY ✔ SH EDSA BANSALANGIN QC COSS 1015 EDSA COR BANSALANGIN PROJECT 7 QUEZON CITY ✔ SH 10TH AVE COR D AQUINO COSS 10TH AVE COR D AQUINO ST GRACE PARK CALOOCAN CITY SH LAONG LAAN DELA FUENTE COSS LAON LAAN COR M DELAFUENTE SAMPALOC MANILA ✔ SH ANDALUCIA REQUESENS COSS ANDALUCIA COR REQUESENS TONDO MANILA CITY ✔ SH TAYUMAN A SANTOS TONDO COSS 1205 TAYUMAN ST COR ABAD SANTOS TON MANILA CITY SH RAE COR 7TH AVE CAL DOSS 249 RIZAL AVE EXT BARANGAY 58 CALOOCAN CITY SH PASO D BLAS VALENZUELA DOSS 65 PASO DE BLAS ROAD VALENZUELA CITY SH C3 DAGAT DAGATAN CAL C 3 ROAD COR. DALAGANG BUKID ST. CALOOCAN CITY SH GOV PASCUAL POTRERO COSS 705 PASCUAL AVENUE BARANGAY POTRERO MALABON CITY ✔ SH A BONIFACIO BINUANG COSS BINUANG ST LALOMA QUEZON CITY SH MCARTHUR TINAJEROS COSS TINAJEROS POTRERO MALABON CITY ✔ SH MH DEL