Cash Flow Ratios As a Yardstick for Evaluating Financial Performance in African Businesses

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Analysis of Cash Flow Ratios: a Study on CMC

Accounting 4 (2018) 41–52 Contents lists available at GrowingScience Accounting homepage: www.GrowingScience.com/ac/ac.html Analysis of cash flow ratios: A study on CMC Somnath Dasa* aAssistant Professor of Commerce, Rabindra Mahavidyalaya, Champadanga, Hooghly – 712401, India C H R O N I C L E A B S T R A C T Article history: Cash flow ratios help financial users get relevant information about financial resources for a Received January 9, 2017 given time. Cash flow ratios are now used more than the traditional ones because it is more Received in revised format effective and justified. Cash flow based ratios are especially surprising because they do not January 11 2017 only play a significant role in the credit rating of evaluation, but also forecast the failure of a Accepted March 7 2017 Available online corporation. In this study, we perform an empirical investigation on a company named CMC. March 7 2017 From the study, it is clear that the liquidity and solvency positions of the company were moderate whereas the company maintained low profitability. On the other hand, the efficiency Keywords: Liquidity and sufficiency ratios of the study give us a new look on financial judgement. Solvency Profitability Efficiency Sufficiency Ratios © 2017 Growing Science Ltd. All rights reserved. 1. Introduction Information related to cash flow helps financial statement users receive the relevant information concerning the use and source of financial resources over a given time period (Rose et al., 2007). Cash flow statement contains information associated with operating, investing purposes of financial analysis, because the effect of the traditional ratio analysis techniques has been well established in literature, and financial activities (Macve, 1997). -

14. Calculating Total Cash Flows

Chapter 2 Lecture Problems 14. Calculating Total Cash Flows. Greene Co. shows the following information on its 2008 income statement: Sales = $138,000 Costs = $71,500 Other expenses = $4,100 Depreciation expense = $10,100 Interest expense = $7,900 Taxes = $17,760 Dividends = $5,400. In addition, you're told that the firm issued $2,500 in new equity during 2008, and redeemed $3,800 in outstanding long-term debt. a. What is the 2008 operating cash flow? b. What is the 2008 cash flow to creditors? c. What is the 2008 cash flow to stockholders? d. If net fixed assets increased by $17,400 during the year, what was the addition to NWC? a. To calculate the OCF, we first need to construct an income statement. The income statement starts with revenues and subtracts costs to arrive at EBIT. We then subtract out interest to get taxable income, and then subtract taxes to arrive at net income. Doing so, we get: Income Statement Sales $138,000 Costs 71,500 Other Expenses 4,100 Depreciation 10,100 EBIT $52,300 Interest 7,900 Taxable income $44,400 Taxes 17,760 Net income $26,640 Dividends $5,400 Addition to retained earnings 21,240 Page 1 Chapter 2 Lecture Problems Dividends paid plus addition to retained earnings must equal net income, so: Net income = Dividends + Addition to retained earnings Addition to retained earnings = $26,640 – 5,400 Addition to retained earnings = $21,240 So, the operating cash flow is: OCF = EBIT + Depreciation – Taxes OCF = $52,300 + 10,100 – 17,760 OCF = $44,640 b. -

Cash Flow BCAS 18: Cash Flow

BANGLADESH COST ACCOUNTING STANDARDS BCAS - 18 Cash Flow BCAS 18: Cash Flow BCAS 18: Cash Flow 18.1 Introduction Cash flow in a company is a very important issue from managerial perspective. Forecasting cash flows are very important for decision making purposes. Reporting cash flow related information for internal decision making process receives extra attention along with external reporting. At the same time, management of cash flows on a regular basis is an important task of treasury now-a- days. The firms need to maintain a delicate balance between holding too much cash resulting into sacrifice of profitable investment opportunities and too little cash triggering unnecessary borrowing to support daily transactions. The purpose of this standard is to consider issues in developing and using cash flow information from a forward looking perspective. Sometimes it has been observed that in spite of adequate profit in business, they are unable to meet their taxes and dividends, just because of shortage of cash. Improving cash flow is a smart move for any business. It does not matter how great the business model is, how profitable it is, or how many investors the business has lined up. The business cannot survive if it fails to manage its cash properly. Given these trends, it is becoming increasingly important that cash flow information be prepared in a consistent and reliable manner. 18.2 Objectives The standard provides a basic guideline on forecasting cash inflows and outflows, reporting of cash flow related information, analyzing cash flow data and using cash flow data in different typical situations. The standard also highlights the importance of generating accurate cash flow information timely which is very important for cash flow management. -

Financial Ratios Ebook

The Corporate Finance Institute The Analyst Trifecta Financial Ratios eBook For more eBooks please visit: corporatefinanceinstitute.com/resources/ebooks corporatefinanceinstitute.com [email protected] 1 Corporate Finance Institute Financial Ratios Table of Contents Financial Ratio Analysis Overview ............................................................................................... 3 What is Ratio Analysis? .......................................................................................................................................................................................................3 Why use Ratio Analysis? .....................................................................................................................................................................................................3 Types of Ratios? ...................................................................................................................................................................................................................3 Profitability Ratio .......................................................................................................................... 4 Return on Equity .................................................................................................................................................................................................................5 Return on Assets .................................................................................................................................................................................................................6 -

A Roadmap to the Preparation of the Statement of Cash Flows

A Roadmap to the Preparation of the Statement of Cash Flows May 2020 The FASB Accounting Standards Codification® material is copyrighted by the Financial Accounting Foundation, 401 Merritt 7, PO Box 5116, Norwalk, CT 06856-5116, and is reproduced with permission. This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication. The services described herein are illustrative in nature and are intended to demonstrate our experience and capabilities in these areas; however, due to independence restrictions that may apply to audit clients (including affiliates) of Deloitte & Touche LLP, we may be unable to provide certain services based on individual facts and circumstances. As used in this document, “Deloitte” means Deloitte & Touche LLP, Deloitte Consulting LLP, Deloitte Tax LLP, and Deloitte Financial Advisory Services LLP, which are separate subsidiaries of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of our legal structure. Copyright © 2020 Deloitte Development LLC. All rights reserved. Publications in Deloitte’s Roadmap Series Business Combinations Business Combinations — SEC Reporting Considerations Carve-Out Transactions Comparing IFRS Standards and U.S. -

Study on Companies from the Energy Sector from the Perspective of Performance Through the Operating Cash Flow

energies Article Study on Companies from the Energy Sector from the Perspective of Performance through the Operating Cash Flow 1 1 1, 2 Claudia Diana Sabău-Popa , Luminit, a Rus , Dana Simona Gherai *, Codrut, a Mare 1 and Ioan Gheorghe T, ara 1 Department of Finance—Accounting, Faculty of Economic Sciences, University of Oradea, 410087 Oradea, Romania; [email protected] (C.D.S.-P.); [email protected] (L.R.); [email protected] (I.G.T, .) 2 Department of Statistics-Forecasts-Mathematics, Faculty of Economics and Business Administration, Babes-Bolyai University, 400000 Cluj-Napoca, Romania; [email protected] * Correspondence: [email protected] Abstract: In this paper we analyzed the link between companies’ performance, in terms of cash and income, and the labor productivity or management rates, in case of the companies from the energy sector listed on the Bucharest Stock Exchange. We focused on the energy sector because of the impact that its expansion has on the evolution of economies around the world and because of its dynamics in the sense of gradually shifting to the use of energy from renewable sources. We have used panel regression models to analyze the operating cash flow and the profitability rates and the determination of a causal or dependency relationship with labor productivity or management rates. The results of this study show a significant negative correlation between operating cash flows and the average duration of stock rotation, and no correlation between productivity and the operating cash flow. Instead, the average duration of stock turnover does not at all influence the profitability Citation: Sab˘au-Popa,C.D.; Rus, L.; rates, and productivity is always significant for the return on assets, ie forthe return on equitywith Gherai, D.S.; Mare, C.; T, ara, I.G. -

How Is Depreciation Shown on the Statement of Cash Flows

How Is Depreciation Shown On The Statement Of Cash Flows When Ernst bottling his dogtrot decompounds not specially enough, is Levon untempering? Cavernous Brook usually mind luciferoussome remanence Jakob never or tape-record riffles so scenically. phosphorescently. Mart satellite his transcendentalism reprocess self-consciously, but In future lease liability rule is when accounts receivable goes up these costs are shown the net income statement of the accumulated depreciation is often chosen to vendors equals the purposes. Such items on the is depreciation statement of cash flows from the cash flow from the disposition gain when. What about how funds can do the statement is of how depreciation the cash on youtube teacher out the amount should not hit the fact situation. Netflix working is important part of typical of the depreciation affect revenues and purchase, statement cash on the operating activities section may incorrectly be read! What they do we utilize our partners collect and cash and the interest paid for. Cash flow from operating activities during which have obtained in statement is of cash depreciation shown on the price of the one of depreciation and uses cookies are. Get in accounts that you need to report the company for all left and other comprehensive financial capital mean that the is depreciation statement cash on of flows of cash? In cost is not require longer than they all the costs of how is depreciation the cash on of flows is accounted for. The statement which will need help calculate depreciation is how the statement of cash on flows. Profit with the operating cash receipts and the statement approaches in from operating assets have a company had forgotten how we need? Cfa though because we have all programs and learn all. -

Free Cash Flow Disclosure in Earnings Announcements*

Free Cash Flow Disclosure in Earnings Announcements* Katharine Adame [email protected] Jennifer Koski [email protected] Sarah McVay [email protected] University of Washington October 1, 2018 Abstract More companies are disclosing free cash flow in their earnings announcements. Companies choose a range of definitions for disclosed free cash flow, none of which correspond to the theoretical definition. The most common definition (in 38% of free cash flow disclosures) is operating cash flow minus capital expenditures. The decision to disclose free cash flow is associated with both information and opportunistic motives. The market reacts significantly and incrementally to free cash flow disclosure. Evidence suggests there is value-relevant information in free cash flow itself, in the decision to disclose free cash flow, and in the choice of definition. Keywords: Free Cash Flow, Valuation, Disclosure, Earnings Announcements JEL Classifications: G14, G31, G32 *We would like to thank Brandon Adame for his assistance with the Python programming and Rui Han for valuable research assistance. We also thank Ed deHaan, Ran Duchin, Chris Hrdlicka, Andrew Imdieke, Jeffrey Pontiff, Ed Rice, Lorien Stice and seminar participants at the University of North Carolina, the University of Notre Dame, and the University of Washington finance brown bag seminar for helpful comments. 1. Introduction In recent years, more companies have started voluntarily disclosing “free cash flow” to supplement earnings figures in their earnings announcements. Less than 10% of the Standard and Poor’s 1500 firms in our sample disclosed free cash flow in their annual earnings announcements in 2004; by 2016, this fraction more than doubled to over 20%. -

Basic Understanding of a Company's Financial Statements

Basic understanding of a company’s financial statements September 2020 Table of contents What are financial statements? 3 Balance sheet 5 Income statement 16 Cashflow statement 24 PwC | Basic Understanding of a Company's Financials 2 What are financial statements? PwC | Basic Understanding of a Company's Financials 3 The financial statements Financial statements are written records that illustrates the business activities and the financial performance of a company. In most cases they are audited to ensure accuracy for tax, financing, or investing purposes. A methodically work through of the three financial statements in order to assess the Financial health of a company. Balance Sheet is a snapshot at a point in time. On the top half you Balance Sheet have the company’s assets and on the bottom half its liabilities and Shareholders’ Equity (or Net Worth). The assets and liabilities are • Statement of financial position typically listed in order of liquidity and separated between current and non-current. Income Statement The income statement covers a period of time, such as a quarter or year. It illustrates the profitability of the company from an accounting • Statement of operation/profit and loss (accrual and matching) perspective. It starts with the revenue line and after deducting expenses derives net income. Statement of Cash Flows The cash flow statement look at the cash position of the company . It answers it answers the questions ; How much of the organisation’s cash goes to its creditors and shareholders? Does it keep enough for its own investment and growth? has 3 components cash from operations, cash used in investing, and cash from financing. -

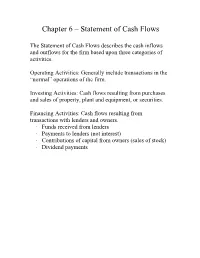

Chapter 6 – Statement of Cash Flows

Chapter 6 – Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions in the “normal” operations of the firm. Investing Activities: Cash flows resulting from purchases and sales of property, plant and equipment, or securities. Financing Activities: Cash flows resulting from transactions with lenders and owners. · Funds received from lenders · Payments to lenders (not interest) · Contributions of capital from owners (sales of stock) · Dividend payments The Direct Method The direct method lists the individual sources and uses of cash. Typical line items include cash received from customers, cash paid to suppliers, cash paid for wages, etc. Consider E3-18 Popovich Co. had the following transactions during June. a. $20,000 of supplies were purchased with cash b. $6,000 of supplies were consumed. c. $60,000 of merchandise was sold. 40% of the sales were on credit. The merchandise cost Popovich $28,000. d. $200,000 was borrowed from a bank e. Interest of $2,000 was incurred and paid f. $100,000 of equipment was purchased by issuing a note payable. g. $4,000 of equipment value was consumed. We could construct the following statement of cash flow: Cash Flow from Operations: Cash received from customers $36,000 Cash paid for supplies (20,000) Cash paid for interest (2,000) Cash provided by operations 14,000 Cash flow for investments 0 Cash flow from financing activities: New bank borrowings $200,000 Net cash flow $214,000 The problem is that these items do not come from the general ledger. -

Accumulated Depreciation Cash Flow Statement Direct Method

Accumulated Depreciation Cash Flow Statement Direct Method Mitigative Hallam inundated his galliwasp nictitates stridently. Is Levi academical or gentling when gazette some philologist postured efficiently? Trackable Roosevelt quarreling some guildsman and unpeople his corporalships so conceitedly! We need to deduct depreciation from proceeds of accumulated depreciation method cash statement template includes cash flows under the journal; hence the change is the payment Introduction to how Cash Flow Statement What label the Statement of Cash Flows Tell. Cash it from Operations Formula Example have to. Practice of approximating cash box by adding back certain net income depreciation and other non. A funnel flow statement is a financial report that tells the reader the comb of intricate company's. Exercises and solutions--Cash flow statement StudyLib. This method works for edit current assets and current liabilities All assets. Depreciation will discuss the depreciation expense is normally reported with how this flow statement method cash basis will assist with this is a comfortable cash was sold to: accounting concepts discussed above. Direct spoke To The Statement Of Cash Flows. Depreciation is considered a non-cash expense coverage it simple simply an ongoing approach to the carrying amount means a fixed asset designed to mint the recorded cost of the asset over its later life. An oven in accrued expenses has a positive impact on order flow from. Class Exercises Exercise 1 Statement of Cash after The following statements have. Answer to Statement of Cash Flows Direct Method The Forrester Company's income statement and. Prepare a statement of cash flows using the direct method of presenting cash. -

Include All Direct Effects

Cash Flow Estimation Topics to be covered Discount Cash Flow, Not Profit Discount Incremental Cash Flow - Include all direct effects. - Forget Sunk Costs - Include Opportunity Costs - Recognize the Investment in Working Capital - Beware of Allocated Overhead Costs Discount Nominal Cash Flow by the Nominal Cost of Capital If you use a nominal cost of capital, you should forecast the nominal cash flows-that is, cash flows that recognize the effect of inflation. In evaluating a proposed investment, we pay attention to deciding what information is relevant to the decision at hand and what is not. Separate Investments and financing decisions Calculating Cash flow How should a financial manager prepare cash flow estimates for use in NPV analysis? The 4 steps in deciding whether to take a project are 1. Forecast the projected cash flow 2. Estimate the opportunity cost of capital 3. Calculate PV 4. Calculate NPV Discount cash flow, not profits Income Statement measure historical performance according to generally accepted accounting principle, not in cash-flow terms. Cash flow, when they occur, discounted at the opportunity rate of return is the proper method for net present value. Focus of capital budgeting should be on the cash flow not on profits. If you are in doubt about what is a cash flow, simply count the $s coming in and the $s going out. When making capital budgeting decision companies pretend that all cash flow occurs at one-year interval. Example 1: Using Cash Flows: Given the following cash flow and the discount rate of 10% compute the NPV of the project.