GAIN Report Global Agriculture Information Network

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Eye of the Wind Segeltoern

Fri 02 March 2018 - Tue 13 March 2018 Since the time of Christopher Columbus, the Bermuda Triangle – the mysterious region in the Atlantic Ocean between Miami, Puerto Rico and Bermuda – has been the subject of 'sailor's yarn', which sometimes tells stories of ships and planes that have disappeared without a trace, and of alleged hauntings or inexplicable natural phenomena. However, maritime superstition is not in our luggage on this crossing, as the Eye of the Wind will not be sailing into the legendary triangle, but instead only into the northern boundary point – the dreamlike Bermuda archipelago. This is where you will go on board: Marina Fort Louis, Marigot / Saint Martin The Princess Juliana international airport is located in the Dutch southern half of the twin island of Sint Maarten / Saint Martin and is easily reached from many major airports. A unique attraction worth seeing is immediately visible on anchoring at the Caribbean island paradise: on the nearby Maho Beach, the distance between landing airplanes and beach-goers' heads (or the masts of the boats anchored there) is often only a few metres. On a chalkboard attached to a surfboard, the arrival times of the largest planes are announced for hobby photographers every day. You can reach Marigot by taxi or minibus with a short drive. By the way, the EURO is the official currency in the French part of Saint Martin. Take advantage of your stay for a relaxing day at the breathtaking Dawn Beach. Our tip: Saint Martin is considered the 'culinary capital of the Caribbean' – do not miss the local specialties made from the guava fruit. -

State of Nature in the Dutch Caribbean: Saba and the Saba Bank

State of Nature in the Dutch Caribbean: Saba and the Saba Bank Open sea and deep sea (EEZ) Figure 1: Habitats of Saba (Verweij & Mücher, 2018) Wageningen Research recently published fields underwater, Saba is rich with a variety an alarming report on the state of nature of different habitats. Unfortunately, the for the three Dutch Caribbean islands recent Wageningen Research report shows (Bonaire, Saba and St. Eustatius), com- that many of these areas, both above missioned by the Ministry of Agriculture, and below water, are showing signs of Nature and Food Quality. All 33 experts degradation. that worked on this report concluded that the “Conservation status 1 of the Governments are beginning to understand biodiversity in the Caribbean Netherlands that managing nature goes beyond just is assessed as moderately unfavorable to protecting natural assets, but can also very unfavorable”. help promote positive economic growth (Ministry of Economic Affairs, 2013). Saba and St. Eustatius are two special mu- Protecting the environment means pro- nicipalities which make up the Caribbean tecting the services they provide such as Netherlands leeward islands. Saba con- natural coastal protection and recreational sists of the main island, Saba, and a large use for locals and tourists (de Knegt, 2014). submerged carbonate platform, the Saba TEEB (The Economics of Ecosystems and Bank. The Saba Bank is the largest national Biodiversity) recently valued the annual park in the Kingdom of the Netherlands total economic value of nature on Saba at (Saba Bank: 268.000 hectares; Wadden 28.4 million USD (Cado van der Lely et al., Sea 240.000 hectares), and has some of the 2014). -

'Good Governance' in the Dutch Caribbean

Obstacles to ‘Good Governance’ in the Dutch Caribbean Colonial- and Postcolonial Development in Aruba and Sint Maarten Arxen A. Alders Master Thesis 2015 [email protected] Politics and Society in Historical Perspective Department of History Utrecht University University Supervisor: Dr. Auke Rijpma Internship (BZK/KR) Supervisor: Nol Hendriks Introduction .............................................................................................................................. 2 1. Background ............................................................................................................................ 9 1.1 From Colony to Autonomy ......................................................................................................... 9 1.2 Status Quaestionis .................................................................................................................... 11 Colonial history .............................................................................................................................. 12 Smallness ....................................................................................................................................... 16 2. Adapting Concepts to Context ................................................................................................. 19 2.1 Good Governance ..................................................................................................................... 19 Development in a Small Island Context ........................................................................................ -

Plum Piece Evidence for Archaic Seasonal Occupation on Saba, Northern Lesser Antilles Around 3300 BP Corinne L

Journal of Caribbean Archaeology Copyright 2003 ISSN 1524-4776 Plum Piece Evidence for Archaic Seasonal Occupation on Saba, Northern Lesser Antilles around 3300 BP Corinne L. Hofman Menno L.P. Hoogland Recent investigations on the island of Saba, northern Lesser Antilles, revealed evidence of preceramic occupation in the northwestern part of the island at an elevation of approxinately 400 m above sea level. The inland location of dense midden deposits in a tropical forest environment makes the Plum Piece site unique for studying the preceramic occupation of the Antilles, a period that is otherwise mainly known from coastal settings. The recovered artifacts and the radiocarbon dates support an attribution to the Archaic period of the preceramic Age. The nature of the tools and the restricted number of exploited food sources suggest a temporary, probably seasonal, occupation of the site for a unique activity. _____________________________________ Archaeological investigations on the island coastal exploitation in which shellfish of Saba, northern Lesser Antilles (Figure 1) predominates. The species collected are related during the summers of 2001 and 2002 revealed to the exploitation of specific coastal evidence of preceramic occupation at the site of environments, varying from mangroves to Plum Piece in the northwestern part of the island shallow-water and shallow-reef habitats. dating from approximately 3300 BP. Prior to these investigations a preceramic date of 3155± The atypical location of the site of Plum 65 BP had been obtained from the Fort Bay area Piece in the tropical forest area of Saba at an in the northeastern sector of Saba (Roobol and elevation of 400 m above sea level provides Smith 1980). -

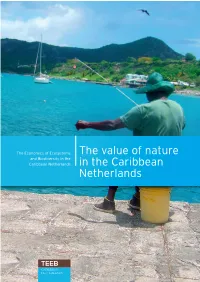

The Value of Nature in the Caribbean Netherlands

The Economics of Ecosystems The value of nature and Biodiversity in the Caribbean Netherlands in the Caribbean Netherlands 2 Total Economic Value in the Caribbean Netherlands The value of nature in the Caribbean Netherlands The Challenge Healthy ecosystems such as the forests on the hillsides of the Quill on St Eustatius and Saba’s Mt Scenery or the corals reefs of Bonaire are critical to the society of the Caribbean Netherlands. In the last decades, various local and global developments have resulted in serious threats to these fragile ecosystems, thereby jeopardizing the foundations of the islands’ economies. To make well-founded decisions that protect the natural environment on these beautiful tropical islands against the looming threats, it is crucial to understand how nature contributes to the economy and wellbeing in the Caribbean Netherlands. This study aims to determine the economic value and the societal importance of the main ecosystem services provided by the natural capital of Bonaire, St Eustatius and Saba. The challenge of this project is to deliver insights that support decision-makers in the long-term management of the islands’ economies and natural environment. Overview Caribbean Netherlands The Caribbean Netherlands consist of three islands, Bonaire, St Eustatius and Saba all located in the Caribbean Sea. Since 2010 each island is part of the Netherlands as a public entity. Bonaire is the largest island with 16,000 permanent residents, while only 4,000 people live in St Eustatius and approximately 2,000 in Saba. The total population of the Caribbean Netherlands is 22,000. All three islands are surrounded by living coral reefs and therefore attract many divers and snorkelers. -

Sint Maarten

Sint Maarten Country Cooperation Strategy 2015 – 2019 29/07/2015 1 Abbreviations ART Antiretroviral therapy treatment AVBZ General Act on Special Medical Expenses AWW General Widowers and Orphans Insurance Act CARICOM Caribbean Community and Common Market CCS Country Cooperation Strategy Cessantia Severance Pay Insurance Act CT Computed Tomography EVT Economic Affairs, Transportation and Telecommunication FZOG Governmental Health Insurance Fund GDP Gross Domestic Product Gov APS General Pension Fund Sint Maarten GP General Practitioner HIS Health Information System HIV Human Immunodeficiency Virus HPV Human Papilloma Virus IMF International Monetary Fund MDGs Millennium Development Goals Min VSA Ministry of Public Health, Social Development and Labor MSGs Millennium Social Goals NAf Netherlands Antilles Florin-Guilder NHA National Health Authority OV Accident Insurance PAHO/WHO Pan American Health Organization/World Health Organization PPP Power Parity Ratio RX Radiography SLS Sint Maarten Laboratory Services SMMC Sint Maarten Medical Center SZV Social and Health Insurance UNDP United Nations Development Program UNICEF United Nations Children Fund USD United States Dollar ZV Sickness Benefits Insurance 2 Table of contents Executive Summary ___________________________________________________________ 4 1-Introduction ________________________________________________________________ 5 2-Health Development Situation _________________________________________________ 6 2.1 Main Health Achievements and Challenges __________________________________________ -

Preliminary Checklist of Extant Endemic Species and Subspecies of the Windward Dutch Caribbean (St

Preliminary checklist of extant endemic species and subspecies of the windward Dutch Caribbean (St. Martin, St. Eustatius, Saba and the Saba Bank) Authors: O.G. Bos, P.A.J. Bakker, R.J.H.G. Henkens, J. A. de Freitas, A.O. Debrot Wageningen University & Research rapport C067/18 Preliminary checklist of extant endemic species and subspecies of the windward Dutch Caribbean (St. Martin, St. Eustatius, Saba and the Saba Bank) Authors: O.G. Bos1, P.A.J. Bakker2, R.J.H.G. Henkens3, J. A. de Freitas4, A.O. Debrot1 1. Wageningen Marine Research 2. Naturalis Biodiversity Center 3. Wageningen Environmental Research 4. Carmabi Publication date: 18 October 2018 This research project was carried out by Wageningen Marine Research at the request of and with funding from the Ministry of Agriculture, Nature and Food Quality for the purposes of Policy Support Research Theme ‘Caribbean Netherlands' (project no. BO-43-021.04-012). Wageningen Marine Research Den Helder, October 2018 CONFIDENTIAL no Wageningen Marine Research report C067/18 Bos OG, Bakker PAJ, Henkens RJHG, De Freitas JA, Debrot AO (2018). Preliminary checklist of extant endemic species of St. Martin, St. Eustatius, Saba and Saba Bank. Wageningen, Wageningen Marine Research (University & Research centre), Wageningen Marine Research report C067/18 Keywords: endemic species, Caribbean, Saba, Saint Eustatius, Saint Marten, Saba Bank Cover photo: endemic Anolis schwartzi in de Quill crater, St Eustatius (photo: A.O. Debrot) Date: 18 th of October 2018 Client: Ministry of LNV Attn.: H. Haanstra PO Box 20401 2500 EK The Hague The Netherlands BAS code BO-43-021.04-012 (KD-2018-055) This report can be downloaded for free from https://doi.org/10.18174/460388 Wageningen Marine Research provides no printed copies of reports Wageningen Marine Research is ISO 9001:2008 certified. -

Madrid Protocol • Has 101 Members, Covering 117 Countries

Madrid System & Caribbean Overseas Territories Abraham Thoppil (Cayman Islands) 20 May 2018 1 Who can use the Madrid System? • Need personal or business connection to a “Contracting Member State” – domiciled in or have commercial establishment in, or be a citizen of one of the 117 countries. Contacting Member State = Office of Origin Members of Madrid Union: • Contracting parties of (i) Madrid Agreement (ii) Madrid Protocol • has 101 members, covering 117 countries 2 A State or intergovernmental organisation (IGO) can accede to the Madrid Protocol IGO • European Union • African Intellectual Property Organisation. CARICOM is eligible Parties to Madrid Protocol in the Caribbean • Antigua and Barbuda • Cuba • Curaçao, Sint Maarten, Bonaire, Sint Eustatius and Saba • Guadeloupe, Martinique, Saint Martin and Saint Barthélemy 3 Status of Territories The Kingdom of the Netherlands: • The Netherlands • Bonaire, Sint Eustatius and Saba – Madrid Protocol applies • Aruba • Member of Madrid Agreement, but not Madrid Protocol • Curaçao – Madrid Protocol applies • Sint Maarten – Madrid Protocol applies France: - Accession to Madrid Protocol included all Overseas Departments and Territories • Guadeloupe • Martinique • Saint-Barthélemy • Saint Martin • French Guiana. 4 Status of Territories UK British Overseas Territories – None of them are parties to the Madrid Protocol • Caribbean BOTs – Anguilla – Bermuda – British Virgin Islands – Cayman Islands – Montserrat – Turks and Caicos Islands UK Crown Dependencies – Guernsey – Jersey – Isle of Man – Madrid Protocol applies 5 Madrid Protocol Accession - protocols http://www.wipo.int/madrid/en/future-members/accession-guide/ 6 Advantages of Accession by Territories to Madrid Protocol • Financial Services – a major part of economy for most Territories • Attract IPHoldCo’s to jurisdiction – IP HoldCo’s in Contracting Member States will be able to be proprietor of Madrid Protocol IRs issued by other States • With accession the Territories are on the same footing as mother country. -

Hurricane Irma

Information Bulletin Americas: Hurricane Irma Information Bulletin no. 4 Date of issue: 11 September 2017 Point of contact: Felipe Del Cid, Disaster and Crisis Department Period covered by this bulletin: 9– Continental Operations Coordinator, email: [email protected] 11 September 2017 Red Cross Movement actors currently involved in the operation: The International Federation of Red Cross and Red Crescent Societies (IFRC), American Red Cross, Antigua and Barbuda Red Cross, British Red Cross overseas branches, Bahamas Red Cross Society, Canadian Red Cross Society, Cuban Red Cross, Dominican Red Cross Society, French Red Cross-PIRAC (Regional Intervention Platform for the Americas and the Caribbean), Haiti Red Cross Society, Italian Red Cross, Netherlands Red Cross overseas branches, Norwegian Red Cross, Saint Kitts and Nevis Red Cross Society, Spanish Red Cross, Swiss Red Cross, the International Committee of the Red Cross (ICRC). N° of other partner organizations involved in the operation: Caribbean Disaster Emergency Management Agency (CDEMA), United Nations system agencies (UNICEF, WFP, FAO, OCHA, IOM), DG-ECHO, Pan American Health Organization [PAHO], government of affected countries, USAID/OFDA, DFID, among others. This bulletin is being issued for information only; it reflects the current situation and details available at this time. Information bulletins no.1, 2 and 3 are available here. The Situation On 11 September, the centre of Tropical Storm Irma was located near latitude 30.3 North, longitude 83.1 West at 11:00 EDT. The centre of Irma is in southwestern Georgia at present. On the forecast track, it will move into eastern Alabama Tuesday morning. After its passage through Cuba on 9 September, Irma severely impacted northern and central Cuba, causing coastal and river flooding. -

St. Maarten – Netherlands Antilles)

The URBAN HERITAGE of PHILIPSBURG (St. Maarten – Netherlands Antilles) History of Foundation and Development & Report of Fieldwork by D. Lesterhuis & R. van Oers DELFT UNIVERSITY of TECHNOLOGY February 2001 Report in Commission of Dr. Shuji FUNO, Kyoto University - Japan O, sweet Saint Martin’s land, So bright by beach and strand, With sailors on the sea And harbours free. Where the chains of mountains green, Variously in sunlight sheen. O, I love thy paradise Nature-beauty fairily nice! O, I love thy paradise Nature-beauty fairily nice! Chorus of O Sweet Saint Martin’s Land, composed by G. Kemps in 1959. 2 Foreword Contents Within the Faculty of Architecture of Delft University of Technology the Department of Architectural Foreword Design/Restoration, chaired by Professor Dr. Frits van Voorden, has been conducting research into the characteristics, typologies and developments of Dutch overseas built heritage since the eighties Introduction of the last century. Traditional regions of study were the former colonies of the Netherlands. Because of close cultural-historic and political links and abundance in colonial architectural buildings and ensembles, an emphasis existed on the countries of Indonesia, Suriname, the Netherlands Chapter 1. General Overview and Short History Antilles and Sri Lanka. With the doctoral research of Van Oers, entitled Dutch Town Planning Overseas during VOC and • Dutch Presence in the West WIC Rule (1600-1800), the field of research of ‘mutual heritage’ was expanded to other regions • Principal Dutch Settlements in the West Indies: Willemstad & Philipsburg where the Dutch had been active in the planning and building of settlements. During that period new partnerships for co-operation in research were developed, of which the Graduate School of Engineering of Kyoto University in Japan is an important one. -

Ocha-Rolac-Caribbeanoverview-20200622.Pdf (English)

THE CARIBBEAN General overview As of March 2019 MONTSERRAT BAHAMAS BAHAMAS 16 15 18 8 BIRD ISLAND Independent CARICOM CDEMA UN Resident 2 CUBA 1 states members Participating StateTURKSs AND CAICOS ISLCooANDSrdinators 3 5 CAYMAN ISLANDS CUBA HAIDOMINICANTI REPUBLIC BRITISH VIRGIN ISLANDS NAVASSA ISLTURKSAND AND CAICOS ISLANDS MEXICO JAMAICA PUERTO RICO ANGUILLA UNITED STATES VIRGIN ISLANDS BELIZE SAINT KITTS AND NEVISANTIGUA AND BARBUDA 15 5 4 25 MONTSERRAT Territories CARICOM associate Countries and territories GUADELOUPE UNITEDGUA TESTMAATESLA OF AMERICA CDEMA BIRD ISLAND 4 members covered by RCs DOMINICA HONDURAS sub-hubs MARTINIQUE EL SALVADOR SAINT LUCIA SAINT VINCENT AND THE GRENADINESBARBADOS NICARAGUA ARUBA CGENERALAYMAN ISLANDS INFORMATION CURBOANÇAIRE,AO SINT EUSTATIUSIndependent AND SABAGRENADA Income levels: High Middle Low HAITI DOMINICAN REPUBLIC ARUBA UNITED STATES OF AMERICA BERMUDA TRINIDAD AND TOBAGO BRITISH VIRGIN ISL. 1 COSTA RICA NAVASSA ISLAND 5 ANGUILLA 3 JAMBAAICAHAMAS CURAÇAO BONAIRE PUERTO RICO ST. MARTIN PANAMA ST. MAARTEN U.S. VIRGIN ANTIGUA AND VENEZUELA ISLANDS BARBUDA UNITED STATES OF AMERICA TURKS AND CAICOS ISLANDS GUYANA ST. KITTS AND NEVIS BELIZE TURKS AND CAICOS ISLANDS BAHAMAS COLOMBIA GUADELOUPE CUBA 4 SURINAME MONTSERRAT BAHAMAS BRAZIL DOMINICA ECUADOR CUBA TURKS AND CAICOS ISLANDS MARTINIQUE CAYMAN ISLANDS SAINT LUCIA CAYMAN ISLANDS HAITI CUBA HAIDOMINICANTI REPUBLIC BRDOMINICANITISH VIRGIN IS REPUBLICLANDS SAINT VINCENT NAVASSA ISLTURKSAND AND CAICOS ISLANDS MEXICO JAMAICA PUERTO RICO ANGUILLA AND -

East Coast of Mexico – 2018

East Coast of Mexico – 2018 Höegh Autoliners is one of the world’s leading Ro/Ro operators, carrying close to two million standard car units annually worldwide. Höegh Autoliners has transportation contracts with many of the world’s vehicle manufacturers and is in addition a leading carrier of second-hand vehicles as well as high and heavy construction equipment and other rolling stock. Our Pure Car/Truck Carrier (PCTC) service to and from East Coast of Mexico is operated by one of the most modern and flexible Ro/Ro fleets in the market. East Coast of Mexico Service Cargo Höegh Autoliners offers import and export possibilities via our regular ports Höegh Autoliners has for many years built a strong relationship with leading on the East Coast of Mexico: Veracruz and Altamira. With growth in the area car manufacturers and importers, for whom we ship new vehicles in different we have added connections to and from Latin American and Caribbean trade patterns worldwide. In addition to that, we focus strongly on the High ports. and Heavy and Breakbulk segments, where our professional staff and modern vessels are ready to cater for a variety of cargo. We offer a wide network of connections with around 100 ports linked with Veracruz and Altamira. We connect the East Coast of Mexico with USA, Latin Our sophisticated Ro/Ro vessels offer up to 6.5 meters of free deck height America and Caribbean, Europe, Middle East, Africa, India, East Asia, and can cater for cargo weighing up to 375 tonnes. The vessels are able to Oceania and South East Asia.