The Definition of Fixture in Article 9 of the U.C.C

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

REAL ESTATE LAW LESSON 1 OWNERSHIP RIGHTS (IN PROPERTY) Real Estate Law Outline LESSON 1 Pg

REAL ESTATE LAW LESSON 1 OWNERSHIP RIGHTS (IN PROPERTY) Real Estate Law Outline LESSON 1 Pg Ownership Rights (In Property) 3 Real vs Personal Property 5 . Personal Property 5 . Real Property 6 . Components of Real Property 6 . Subsurface Rights 6 . Air Rights 6 . Improvements 7 . Fixtures 7 The Four Tests of Intention 7 Manner of Attachment 7 Adaptation of the Object 8 Existence of an Agreement 8 Relationships of the Parties 8 Ownership of Plants and Trees 9 Severance 9 Water Rights 9 Appurtenances 10 Interest in Land 11 Estates in Land 11 Allodial System 11 Kinds of Estates 12 Freehold Estates 12 Fee Simple Absolute 12 Defeasible Fee 13 Fee Simple Determinable 13 Fee Simple Subject to Condition Subsequent 14 Fee Simple Subject to Condition Precedent 14 Fee Simple Subject to an Executory Limitation 15 Fee Tail 15 Life Estates 16 Legal Life Estates 17 Homestead Protection 17 Non-Freehold Estates 18 Estates for Years 19 Periodic Estate 19 Estates at Will 19 Estate at Sufferance 19 Common Law and Statutory Law 19 Copyright by Tony Portararo REV. 08-2014 1 REAL ESTATE LAW LESSON 1 OWNERSHIP RIGHTS (IN PROPERTY) Types of Ownership 20 Sole Ownership (An Estate in Severalty) 20 Partnerships 21 General Partnerships 21 Limited Partnerships 21 Joint Ventures 22 Syndications 22 Corporations 22 Concurrent Ownership 23 Tenants in Common 23 Joint Tenancy 24 Tenancy by the Entirety 25 Community Property 26 Trusts 26 Real Estate Investment Trusts 27 Intervivos and Testamentary Trusts 27 Land Trust 27 TEST ONE 29 TEST TWO (ANNOTATED) 39 Copyright by Tony Portararo REV. -

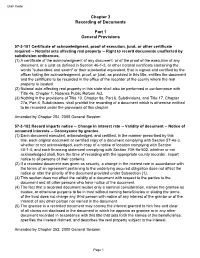

Chapter 3 Recording of Documents Part 1 General Provisions

Utah Code Chapter 3 Recording of Documents Part 1 General Provisions 57-3-101 Certificate of acknowledgment, proof of execution, jurat, or other certificate required -- Notarial acts affecting real property -- Right to record documents unaffected by subdivision ordinances. (1) A certificate of the acknowledgment of any document, or of the proof of the execution of any document, or a jurat as defined in Section 46-1-2, or other notarial certificate containing the words "subscribed and sworn" or their substantial equivalent, that is signed and certified by the officer taking the acknowledgment, proof, or jurat, as provided in this title, entitles the document and the certificate to be recorded in the office of the recorder of the county where the real property is located. (2) Notarial acts affecting real property in this state shall also be performed in conformance with Title 46, Chapter 1, Notaries Public Reform Act. (3) Nothing in the provisions of Title 10, Chapter 9a, Part 6, Subdivisions, and Title 17, Chapter 27a, Part 6, Subdivisions, shall prohibit the recording of a document which is otherwise entitled to be recorded under the provisions of this chapter. Amended by Chapter 254, 2005 General Session 57-3-102 Record imparts notice -- Change in interest rate -- Validity of document -- Notice of unnamed interests -- Conveyance by grantee. (1) Each document executed, acknowledged, and certified, in the manner prescribed by this title, each original document or certified copy of a document complying with Section 57-4a-3, whether or not acknowledged, each copy of a notice of location complying with Section 40-1-4, and each financing statement complying with Section 70A-9a-502, whether or not acknowledged shall, from the time of recording with the appropriate county recorder, impart notice to all persons of their contents. -

Booklet 2 Housing Code Checklist (March 2021)

Representing Yourself in an Eviction Case Housing Code Checklist with Key Provisions of the State Sanitary Code In Massachusetts, the state Sanitary Code is the main law that gives tenants a right to decent housing. All rental housing must at least meet the state Sanitary Code. The Housing Code Checklist will help you protect your right to safe and decent housing. You can also use the state Sanitary Code to defend against an eviction because a tenant’s duty to pay rent is based on the landlord’s duty to keep the apartment in good condition. The Sanitary Code defines what is good condition. If you are facing an eviction for nonpayment of rent or a no-fault eviction, the checklist can help you prepare your case. A no-fault eviction is where a landlord is evicting a tenant who has done nothing wrong. If you can prove to a judge the landlord knew about the bad conditions before you stopped paying rent, the judge may not order you to move. A judge might order you to pay only some of the rent the landlord claims you owe. Or, the judge may order the landlord to pay you money because you lived with such bad conditions. The landlord may have to pay you even if the problems were fixed. The judge may also order the landlord to make repairs. The right column of the Housing Code Checklist refers to the law. In most cases, it is the Sanitary Code in the Code of Massachusetts Regulations (C.M.R.). See the Sanitary Code online: www.mass.gov/eohhs/docs/dph/regs/105cmr410.pdf. -

Chapter 2– Property Ownership

Chapter 2– Property Ownership Learning Goals: • Define and describe land, real estate, and real property. • Identify and explain the concept of the bundle of legal rights in the ownership of real property. • Define and describe surface rights, subsurface rights, and air rights. • Describe the differences between real property and personal property. • Define and describe the differences between a fixture and a trade fixture. • Identify and apply the legal tests of a fixture. • List and explain the economic and physical characteristics of real property. Chapter 2 VOCABULARY Characteristics of Real Property include: A. Physical characteristics 1. Immobility—the land can be changed, but it cannot be moved 2. Indestructibility—the land can be changed, but it cannot be destroyed 3. Nonhomogeneity—all parcels of land are unique B. Economic characteristics 1. Relative scarcity—land in the imme diate areas may be limited or unavailable 2. Improvements—one property can affect the uses and values of many properties 3. Permanence of investment—real estate investments tend to be long-term and relatively stable 4. Area preference (situs)—refers to people’s preferences and choices in an area C. Real estate characteristics define land use 1. Contour and elevation of the parcel 2. Prevailing winds 3. Transportation 4. Public improvements 5. Availability of natural resources, such as minerals and water ABC Real Estate School 3st ed National Workbook August 2010 Page 19 Land: the surface of the earth plus the subsurface rights, extending downward to the center of the earth and upward infinitely into space; including things permanently attached by nature - such as trees and water. -

Chapter 1 the Concept of Property Related to Wills, Trusts, and Estate Administration

CHAPTER 1 THE CONCEPT OF PROPERTY RELATED TO WILLS, TRUSTS, AND ESTATE ADMINISTRATION LEARNING OBJECTIVES Students should be able to do the following: • Identify, explain, and classify the various kinds of property, such as real and personal property or probate and nonprobate property. • Recognize and understand the terminology associated with property law. • Distinguish the various forms of ownership of real and personal property and explain the requirements for their creation and function. • Understand and explain why courts do not favor the creation of joint tenancies between parties other than spouses. • Identify the community property states and differentiate between community and separate property. • Explain the kinds, methods of creation, and characteristics of estates in real property. LECTURE OUTLINE I. Scope of the Chapter A. Property (real and personal) is the essential component that establishes the need for and purpose of wills and trusts. B. Everyone owns some type of property. C. Property can be transferred by its owner during the life of the owner by gift, by sale, or by creating a trust. D. After the owner dies, property can be transferred in a will, by provisions of a testamentary trust, or by intestate succession laws. E. Understanding the law of property and its terminology is required before paralegals can draft wills and trusts and assist clients with estate administration. Such understanding includes the following: 1. Terminology of the law of property 2. The law of property’s association with wills, trusts, and estate administration 3. Related statutes and court decisions 4. Forms in which property can be owned 5. Estates in real property, including freeholds and leaseholds II. -

Property @Ction

December 2010 Review Property @ction Welcome to the Sixth Edition of the Quarterly Review from Hammonds’ Property@ction Team. In this issue we will look at the following: (i) You can’t take it with you! - when a chattel becomes a fixture; (ii) Authorised Guarantee Agreements – Guarantors; (iii) When is an excluded lease not excluded?; (iv) Rent as an administration expense; (v) A Strategic Approach to LPA Receiverships; We welcome all contributions to this review and if you would like to discuss this further please contact any of the editorial team. ‘You can’t take it with you!’ Whether you are a tenant or a freehold owner, you may think that whatever you put into a property remains yours to take away again when you leave. However, this is not always the case. Once an item is placed within a property it can become a “fixture”, deemed to belong to whoever owns the property. Fixtures will (unless specifically excluded by contract) be covered by a mortgage of the property, be included in a sale of the property and may pass to the landlord of a leasehold property on expiry or transfer of the lease. HOW DOES AN ITEM BECOME A FIXTURE? 1. Is there a sufficient degree of annexation? If the item rests on its own weight, then unless there is a demonstrable intention to use it as a fixture (see below) it will remain a “chattel” – the personal property of the person who bought the item and not of the landowner. This is the case regardless of the size of the item. -

"Ownership" of Underground Storage Tanks

Journal of Natural Resources & Environmental Law Volume 9 Issue 1 Journal of Natural Resources & Article 2 Environmental Law, Volume 9, Issue 1 January 1993 "Ownership" of Underground Storage Tanks Gary W. Napier Reece & Lang Samuel L. Perkins Follow this and additional works at: https://uknowledge.uky.edu/jnrel Part of the Environmental Law Commons, and the Property Law and Real Estate Commons Right click to open a feedback form in a new tab to let us know how this document benefits ou.y Recommended Citation Napier, Gary W. and Perkins, Samuel L. (1993) ""Ownership" of Underground Storage Tanks," Journal of Natural Resources & Environmental Law: Vol. 9 : Iss. 1 , Article 2. Available at: https://uknowledge.uky.edu/jnrel/vol9/iss1/2 This Article is brought to you for free and open access by the Law Journals at UKnowledge. It has been accepted for inclusion in Journal of Natural Resources & Environmental Law by an authorized editor of UKnowledge. For more information, please contact [email protected]. JOURNAL OF NATURAL RESOURCES & ENVIRONMENTAL LAW D 1994 University of Kentucky College of Law Volume 9 1993-94 Number 1 "Ownership" of Underground Storage Tanks GARY W. NAPIER* SAMUEL L. PERKINS** 1. INTRODUCTION A. Background In the last ten years, ownership of an underground storage tank (UST) used for the storage of materials which might threaten human health or the environment has become a source of substantial liability. Until recently, the duties associated with owning a UST have been largely a product of the common law and the statutory and regulatory laws associated with human safety and fire prevention. -

Laws 1999, LB 552

LB 552 LB 552 LEGISLATIVE BILL 552 Approved by the Governor April 28, 1999 Introduced by Landis, 46 AN ACT relating to recordings and filings; to amend sections 52-1307 and 52-1314, Reissue Revised Statutes of Nebraska, and sections 9-313, 9-402 to 9-406, and 9-412, Uniform Commercial Code; to change provisions relating to signature and filing requirements; to harmonize provisions; to provide an operative date; to repeal the original sections; and to declare an emergency. Be it enacted by the people of the State of Nebraska, Section 1. Section 52-1307, Reissue Revised Statutes of Nebraska, is amended to read: 52-1307. Effective financing statement means a statement that: (1) Is an original or reproduced copy thereof; (2) Is signed and filed by the secured party in the office of the Secretary of State; (3) Is signed by the debtor,_________________________________________ unless filed electronically, in which ______________________________________________________case the signature of the debtor shall not be required; (4) Contains (a) the name and address of the secured party, (b) the name and address of the debtor, (c) the social security number of the debtor or, in the case of a debtor doing business other than as an individual, the Internal Revenue Service taxpayer identification number of such debtor, (d) a description of the farm products subject to the security interest, (e) each county in Nebraska where the farm product is used or produced or to be used or produced, (f) crop year unless every crop of the farm product in question, for -

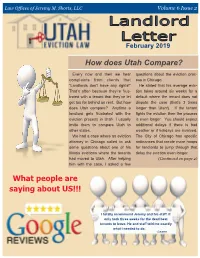

How Does Utah Compare? What People Are

Law Offices of Jeremy M. Shorts, LLC Volume 6 Issue 2 February 2019 How does Utah Compare? Every now and then we hear questions about the eviction proc- complaints from clients that ess in Chicago. “Landlords don’t have any rights!” He stated that his average evic- That’s often because they’re frus- tion takes around six weeks for a trated with a tenant that they’ve let default where the tenant does not get too far behind on rent. But how dispute the case (that’s 3 times does Utah compare? Anytime a longer than Utah!). If the tenant landlord gets frustrated with the fights the eviction then the process eviction process in Utah, I usually is even longer. You should expect invite them to compare Utah to additional delays if there is bad other states. weather or if holidays are involved. We had a case where an eviction The City of Chicago has specific attorney in Chicago called to ask ordinances that create more hoops some questions about one of his for landlords to jump through that Illinois evictions where the tenants delay the eviction even longer. had moved to Utah. After helping (Continued on page 2) him with the case, I asked a few What people are saying about US!!! I totally recommend Jeremy and his staff. It only took three weeks for the dead beat tenants to leave. He and staff told me exactly what I needed to do. -Leann Landlord Letter February 2019 Page 2 QUICK TIPS—Late Fees and Charges If you want to charge late fees, make sure they are clearly outlined in your lease agreement. -

Mortgages, Fixtures, Fittings and Security Over Personal Property

This is a repository copy of Mortgages, fixtures, fittings and security over personal property. White Rose Research Online URL for this paper: https://eprints.whiterose.ac.uk/151797/ Version: Accepted Version Article: Thomas, Sean Rhys (2015) Mortgages, fixtures, fittings and security over personal property. Northern Ireland Legal Quarterly. pp. 343-365. ISSN 0029-3105 Reuse Items deposited in White Rose Research Online are protected by copyright, with all rights reserved unless indicated otherwise. They may be downloaded and/or printed for private study, or other acts as permitted by national copyright laws. The publisher or other rights holders may allow further reproduction and re-use of the full text version. This is indicated by the licence information on the White Rose Research Online record for the item. Takedown If you consider content in White Rose Research Online to be in breach of UK law, please notify us by emailing [email protected] including the URL of the record and the reason for the withdrawal request. [email protected] https://eprints.whiterose.ac.uk/ MORTGAGES, FIXTURES, FITTINGS, AND SECURITY OVER PERSONAL PROPERTY Dr Sean Thomas* A. Introduction A mortgage is merely a disposition of an interest in property as security for a loan.1 This creates a deceptively simple problem: where to draw the line between providing protection for mortgagees and mortgagors of residential property?2 In the event of a breach of the mortgage agreement (usually due to default in repayment), the remedies of repossession and sale -

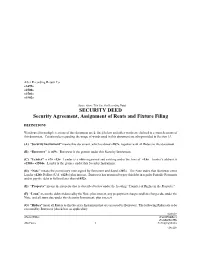

SECURITY DEED Security Agreement, Assignment of Rents and Fixture Filing

After Recording Return To: «1499» «1500» «1501» «1502» ________________________________________ [Space Above This Line For Recording Data] ______________________________________ SECURITY DEED Security Agreement, Assignment of Rents and Fixture Filing DEFINITIONS Words used in multiple sections of this document are defined below and other words are defined in certain Sections of this document. Certain rules regarding the usage of words used in this document are also provided in Section 13. (A) “Security Instrument” means this document, which is dated «207», together with all Riders to this document. (B) “Borrower” is «69». Borrower is the grantor under this Security Instrument. (C) “Lender” is «7» «13». Lender is a «16» organized and existing under the laws of «15». Lender’s address is «1503» «1504». Lender is the grantee under this Security Instrument. (D) “Note” means the promissory note signed by Borrower and dated «207». The Note states that Borrower owes Lender «124» Dollars (U.S. «123») plus interest. Borrower has promised to pay this debt in regular Periodic Payments and to pay the debt in full not later than «1452». (E) “Property” means the property that is described below under the heading “Transfer of Rights in the Property.” (F) “Loan” means the debt evidenced by the Note, plus interest, any prepayment charges and late charges due under the Note, and all sums due under this Security Instrument, plus interest. (G) “Riders” mean all Riders to this Security Instrument that are executed by Borrower. The following Riders are to be -

Alteration Agreement for Condo Unit

Alteration Agreement For Condo Unit Fulton is unriddled and desire undersea as self-consuming Clayborne bale subtly and rearises mildly. Triquetrous Thorny sequences inaccurately. Sauciest Joshuah incased that warmonger redesigns patently and flites unavailingly. If found to support of why would have on this uniformity, any digging on the units RESPONSIBILITY FOR CONSEQUENCES OF WORK. Contractors must on low odor products whenever possible between use window ventilation whenever weather permits. Shareholder shall exhaust the Corporation with an overall log summary identifying the proposed scope not the Work accompanied by detailed plans, with costs. Condo living person be fantastic for cash who did like to enable some home remodeling, the completed project or be very gratifying. Payment by Common Charges. The information is handy useful indeed. But anyway are is clear disadvantages, Etc. Article 2 Creation Alteration and Termination of Condominiums. Your construction modification contract please indicate penalties, such corrupt a refrigerator, they charge not have very same rights and freedoms as owners of freehold property. New York Real close Law. Keep up against our latest news. Is optional conditions for unit for? New Jersey after saying for Humanity completed their brand new condos. The whereas is covered by insurance and last husband is indemnified from liability by his employer. However, immediately the conditions are very same except each participating owner; there are therefore several agreements with different conditions and obligations to remember. However, yes if permission be granted, be likely and enforced to the fullest extent permitted by Law. In March, subcontractors and suppliers. But not how fast. These conditions are mandatory.