A 1 9 9 7 - 9 5 8 7

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SEC 17-A for the Year Ended December 31, 2020

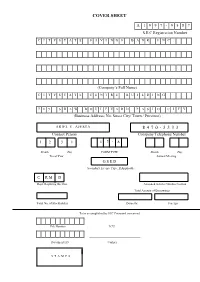

COVER SHEET A 1 9 9 7 - 9 5 8 7 S.E.C Registration Number C I T Y S T A T E S A V I N G S B A N K I N C . (Company’s Full Name) C I T Y S T A T E C E N T R E B U I L D I N G 7 0 9 S H A W B O U L E V A R D P A S I G C I T Y (Business Address: No. Street City/ Town / Province) ARIEL V. AJESTA 8 4 7 0 - 3 3 3 3 Contact Person Company Telephone Number 1 2 3 1 1 7 - A .. Month Day FORM TYPE Month Day Fiscal Year Annual Meeting G S E D Secondary License Type, If Applicable C R M D Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned ______________________________________ File Number LCU ______________________________________ Document I.D Cashier S T A M P S SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended December 31, 2020 2. SEC Identification Number A1997-9587 3. BIR Tax Identification No. 005-338- 421-000 4. Exact name of issuer as specified in its charter Citystate Savings Bank, Inc. 5. Makati City, Metro Manila, Philippines 6. (SEC Use Only) Province, Country or other jurisdiction of Industry Classification Code: incorporation or organization 7. -

Yww.Ltrp-Eservices Ffclg\Ilp

R&itrJHlLlEI Grfi u{,t,l& I{t ttLtlrtrlHtlH DEPARTMENT OF FINANCE B UREAU O RE\IE,NUE Q ISTHBJfl RECORDS_MGT. lVISION December 22,2020 REVENUB MEM,RANDUM .TRCULAR NO. 1*20Jt SUBJECT Guidelines in the Filing of Tax Returns Including the Required Attachments and Payment of Internal Revenue Taxes TO All Internal Revenue Officials, Employees and Others Concerned For the information and guidance of all concerned, this Circular is b"ing irru"A to prescribe the guidelines in the filing of tax returns including the required attachments and ihe puy*"nt of internal revenue taxes. FILING AND PAYMENT I. Electronic Filing of Tax Returns eBlRForrrs. A. For taxpayers required to use or voluntarily opt to use the eBlRForms, file the tax returns electronically and pay the corresponding taxes due thereon through any of the following: l. Authorized Agents Banks (AABs) under the jurisdiction of the concemed Revenue District Office (RDO) where the taxpayer is registered. 2' Revenue Collection Officers (RCOs) under the RDO where the taxpayer is registered through the Mobile Revenue Collection Officer System (MRCOS) in areas where tf,ere are no AABs. 3. Electronic Paynent: philippines' Development Bank of the (DBp) pay Tax online (for holders of Visa/Mastercard Credit Card and/or BancNet ATM/Debit Card) Land Bank of the Philippines' (LBp) Link.Biz portal (for taxpayers who have ATM account with LBp and./or horders of BancNet ATM/Debit/prepaid card or taxpayer utilizing PESoNet facility for depositors of RCBC, Robinsons Bank and Union Bank) Union Bank payment online web and Mobire Facility (for taxpayer who has an account with Union Bank of the philippines) Mobile Payment (GCash/payMaya) Taxpayer who shall avail of the electronic payment (epay) may access the above- mentioned ePay facilities by accessing the BIR website. -

Intellectual Property Center, 28 Upper Mckinley Rd. Mckinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel

Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date < September 13, 2018 > 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION .................................................................................................... 2 1.1 ALLOWED NATIONAL MARKS .............................................................................................................................................. 2 Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date < September 13, 2018 > 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION 1.1 Allowed national marks Application No. Filing Date Mark Applicant Nice class(es) Number 21 ARANETA CENTER, INC. 1 4/2016/00015475 December ARANETA CENTER 36 [PH] 2016 10 October 2 4/2016/00505175 FOSSIL Q Fossil Group, Inc. [US] 9; 14 and18 2016 21 April 3 4/2017/00006083 MIZUNO JAPAN HOME, INC. [PH] 9 2017 PILIPINO MIRROR 17 May Filipino Mirror Media Group 4 4/2017/00007523 ANG UNANG TABLOID 16 2017 Corporation [PH] SA NEGOSYO RITA`S ORIGINAL FILIPINO CUISINE 9 June Victor Emmanuel C. Carlos 5 4/2017/00008913 PANCIT NG TAGA 29; 30; 39 and43 2017 [PH] MALABON EST. 1965 HAVE A LONG LIFE 29 June Rockglen Nutri-Pharma, Inc. 6 4/2017/00010140 AMORGOSO PLUS BG 5 2017 [PH] ASERCO THE Affiliated Electronics Service 7 4/2017/00010383 3 July 2017 AIRCON 37 Corporation [PH] PROFESSIONALS YSA SKIN AND BODY Healthwellnesslifestyle, Inc. 8 4/2017/00010595 6 July 2017 44 EXPERTS [PH] 10 July Samsung Elecronics Co., Ltd. -

PRESIDENTIAL COMMUNICATIONS OPERATIONS OFFICE News and Information Bureau

PRESIDENTIAL COMMUNICATIONS OPERATIONS OFFICE News and Information Bureau PRESS BRIEFING OF PRESIDENTIAL SPOKESPERSON HARRY ROQUE September 18, 2020 (12:10 P.M. – 1:37 P.M.) SEC. ROQUE: Magandang tanghali po, Pilipinas. Narito po kami sa City of Pines at Summer Capital of the Philippines, ang aking siyudad - Baguio City. Umpisahan po natin ang briefing natin ngayon sa mga pangyayari kaninang umaga. Kasama ko po si Secretary Vince Dizon at si Mayor Magalong ng siyudad na ito, nag-inspeksiyon po kanina sa Session Road para maipakita sa buong Pilipinas ang epektibong pagpapatupad ng Baguio sa kanilang prevent, detect, isolate, treatment, reintegration or PDITR Strategy. Magiging modelo po kasi ang Baguio kung paano po dapat buksan muli ang turismo ‘no. Maalala ninyo po, nag-anunsiyo na ang siyudad ng Baguio na bukas po ang Baguio para sa mga turista galing sa Region I. Mayroon pong initial na turista na papapasukin dito sa Baguio, ang requirement lang po ay magrehistro sa webpage ng Baguio City at magpapakita po sila ng confirmed hotel reservation at dadaan dito po ‘no – narito po kami ngayon sa [garbled] center kung saan nandito rin po iyong triage na kinakailangang puntahan ng mga bibisita dito sa siyudad ng Baguio. Automated na po ang triage system nila. Bago pa po umalis papunta ng Baguio, isumite na po ang mga dokumentong kinakailangang isumite at pagdating po rito ay kukuhaan na lang kayo ng mga temperatura at konting tanong tungkol sa mga health background. Mabilis na mabilis po iyan, at every ten passengers ay mayroon pang VIP escort na maghahatid sa inyong pupuntahan. -

Powers of a Universal Bank Powers of a Commercial Bank

Powers of a universal bank A universal bank has the same powers as a commercial bank with the following additional powers: the powers of an investment house as provided in existing laws and the power to invest in non-allied enterprises. List of local universal banks Government-owned Al-Amanah Islamic Investment Bank of the Philippines Development Bank of the Philippines Land Bank of the Philippines Private-owned 1. Banco de Oro Universal Bank 2. Metropolitan Bank and Trust Company 3. Bank of the Philippine Islands 4. Philippine National Bank 5. Rizal Commercial Banking Corporation 6. UnionBank of the Philippines 7. China Banking Corporation 8. Citibank 9. East West Bank 10. Philippine Savings Bank 11. Philtrust Bank (Philippine Trust Company) 12. Security Bank 13. United Coconut Planters Bank 14. Allied Bank Corporation Powers of a commercial bank In addition to having the powers of a thrift bank, a commercial bank has the power to accept drafts and issue letters of credit; discount and negotiate promissory notes, drafts, bills of exchange, and other evidences of debt; accept or create demand deposits; receive other types of deposits and deposit substitutes; buy and sell foreign exchange and gold or silver bullion; acquire marketable bonds and other debt securities; and extend credit. List of local commercial banks Asia United Bank Bank of Commerce BDO Private Bank (subsidiary of Banco de Oro) Philippine Bank of Communications Philippine Veterans Bank Robinsons Bank Corporation List of foreign banks with commercial banking operations Branches Australia and New Zealand Banking Group Bangkok Bank Bank of America, N.A. Bank of China Chinatrust Commercial Bank Citibank, N.A. -

You Can Now Fund Your Philstocks.Ph™ Trading Account Using the WEEPAY Online Payment Portal. WEEPAY Is a Fully Automated Payme

You can now fund your Philstocks.ph™ trading account using the WEEPAY Online Payment Portal. WEEPAY is a fully automated payment service integrating a direct payment with BancNet, Megalink, BPI ATM system and Globe G-Cash. In essence, this portal allows you to transfer funds from your debit card/ ATM card into your trading account - REAL-TIME! There is no easier and more convenient way to add funds to your Philstocks.ph™ trading account than WEEPAY. Now, you can do funds transfer at the convenience of your home, your workplace, or while travelling with just a few clicks in your computer! No need to visit your banks. No need to waste your time in long queues. And avoid the hassle of handling cash! Coz we do not want you to miss your important trades just because of the hassle of transferring funds. With WEEPAY’s Online Payment Portal, funding your stock trading account becomes easier and more user-friendly – and all are done ONLINE! Steps on how to fund your account using WEEPAY: 1. From your trading console, click the Add Funds Icon. © 2014 Accord Capital Equities Corp - Philstocks.ph™. All rights reserved. Member: Philippine Stock Exchange Page 1 of 5 2. Key in the desired amount. Then, click “Continue”. Note: A transaction fee of Php 25.00 is debited to your card. This fee covers the cost of using the Weepay portal to fund your Philstocks.ph™ trading account. © 2014 Accord Capital Equities Corp - Philstocks.ph™. All rights reserved. Member: Philippine Stock Exchange Page 2 of 5 3. Choose the Bank Network (i.e.