Nifty Highlights

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

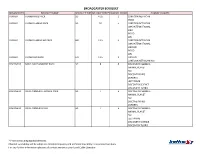

Declaration Under Sec 4(4)

KABLE FIRST INDIA PRIVATE LIMITED BANGALORE Declaration under Section 4(4) of the Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable Systems) Regulations, 2017 (No. 1 of 2017) 4(4) a: Target Market : States/Parts of State covered as "Coverage Area" Bangalore 4(4) b: Total Channel carrying capacity Distribution Network Location / States / Parts of State covered Capacity in SD Headend as "Coverage Area" Terms Bangalore Bangalore 543 Kindly Note : 1. Local Channels considered as 1 SD; 2. Consideration in SD Terms is clarified as 1 SD = 1 SD; 1 HD = 2SD; 3. Number of channels will vary within the area serviced by a distribution network location depending upon available Bandwidth Capacity. 4(4) c: List of Channels available on the network: Distribution Network Location: Bangalore Sl. No Service Name COUNT IN SD TERMS SD/HD 1 DD CHANDANA 1 SD 2 ZEE KANNADA 1 SD 3 COLORS KANNADA 1 SD 4 NAPTOL KANNADA 1 SD 5 COLORS SUPER 1 SD 6 STAR SUVARNA 1 SD 7 UDAYA TV 1 SD 8 BHIMA TV 1 SD 9 EXPRESS TV 1 SD 10 ZEE PICTURE 1 SD 11 PUBLIC MOVIES 1 SD 12 COLORS KANNADA CINEMA 1 SD 13 SUVARNA PLUS 1 SD 14 SIRI KANNADA 1 SD 15 UDAYA COMEDY 1 SD 16 UDAYA MOVIES 1 SD 17 PUBLIC MUSIC 1 SD 18 RAJ MUSIX KANNADA 1 SD 19 UDAYA MUSIC 1 SD 20 SUVARNA NEWS 1 SD 21 B TV News 1 SD 22 TV 9 KANNADA 1 SD 23 DIG VIJAY 1 SD 24 PUBLIC TV 1 SD 25 POWER TV 1 SD 26 NEWS18 KANNADA 1 SD 27 PRAJA TV NEWS 1 SD 28 TV 5 KANNADA NEWS 1 SD 29 RAJ NEWS KANNADA 1 SD 30 AAYUSH TV 1 SD 31 CHINTU TV 1 SD 32 ETV BAL BHARAT 1 SD 33 SRI SANKARA 1 SD 34 DD PODHIGAI 1 -

Tata Consultancy Services Ltd. TV18 Broadcast Ltd

Tata Consultancy Services TV18 BroadcastLtd. Ltd. RESULT UPDATE 12th October, 2017 RESULT UPDATE 19th April2017 India Equity Institutional Research II Result Update – Q2FY18 II 12th October, 2017 Page 2 TV 18 Broadcast Ltd. Niche Channels Started Bearing Fruit !! CMP Target Potential Upside Market Cap (INR Mn) Recommendation Sector INR 40 INR 57 42.5% 69,174 BUY Media Result highlights •TV18 reported its Q2 FY18 results, where revenues fell below our estimates but margins have improved on yoy basis •Revenue stood at INR 2,272 Mn, up 4% qoq and down 5% yoy •EBITDA (under Ind AS consolidated) stood at INR (1) Mn in Q2 FY18, an improvement over INR (109 Mn) in Q2 FY17 •PAT was recorded at INR 75 Mn in Q2 FY18, versus INR 51 Mn in Q2 FY17, primarily due to improvement in performance of JVs and gaining operating efficiency MARKET DATA KEY FINANCIALS Shares outs (Mn) 1714 Particulars (INR Mn) FY17 FY18E FY19E EquityCap (INR Mn) 3429 Net Sales 9794 10083 10,890 Mkt Cap (INR Mn) 69174 EBITDA 313 445 2,178 52 Wk H/L (INR) 50/33 PAT 191 1520 3,267 EPS 0.11 0.89 1.91 Volume Avg (3m K) 6444.5 OPM 3.2% 4.4% 20.0% Face Value (INR) 2 NPM 2.0% 15.1% 30.0% Bloomberg Code TV18 IN Source: Company, KRChoksey Research SHARE PRICE PERFORMANCE Highlights of Q2 FY18 (i) Revenues in Q2 FY18 were largely subdued, as the market is reviving from GST implications, and traders are still cautious to increase their spending for advertisements. -

Viacom18 Media Private Limited– Update on Material Event Rationale

April 29, 2021 Viacom18 Media Private Limited– Update on Material Event Summary of rating(s) outstanding Previous Rated Amount Current Rated Amount Instrument* Rating Outstanding (Rs. crore) (Rs. crore) Commercial Paper Programme 500.0 500.0 [ICRA]A1+ Short-term, Fund-based/Non 1,610.7 1,610.7 [ICRA]A1+ fund based Limits Total 2,110.7 2,110.7 *Instrument details are provided in Annexure-1 Rationale On February 17, 2020, Network18 intimated the stock exchanges regarding a scheme of amalgamation and arrangement amongst Network18, TV18, DEN Networks Limited (DEN) and Hathway Cable & Datacom Limited (Hathway). Under the scheme, DEN, Hathway and TV18 were to merge into Network18 with effect from February 1, 2020, subject to receipt of necessary approvals to consolidate Reliance Industries Limited’s (RIL, rated [ICRA]AAA (Stable) / [ICRA]A1+ and Baa2 Stable by Moody’s Investors Service) media and distribution business spread across multiple entities into Network18. The company again announced on April 20, 2021 that considering more than a year has passed from the time the Board considered the Scheme, the Board of the Company has decided not to proceed with the arrangement envisaged in the Scheme. ICRA has taken cognizance of the above and the rating remain unchanged at the earlier rating of [ICRA]A1+ as the parent company, TV18 would continue with the existing corporate structure. Please refer to the following link for the previous detailed rationale that captures Key rating drivers and their description, Liquidity position, Rating sensitivities,: Click here Analytical approach Analytical Approach Comments Corporate Credit Rating Methodology Applicable Rating Methodologies Rating Methodology for Media Broadcasting Industry Impact of Parent or Group Support on an Issuer’s Credit Rating Parent / Group Company: RIL Group. -

Corporate Presentation Media & Investments

Media & Investments Corporate Presentation FY19-20 OVERVIEW 2 Key Strengths Leading Media company in India with largest bouquet of channels (56 domestic channels and 16 international beams), and a substantial digital presence Market-leader in multiple genres (Business News #1, Hindi General News & Entertainment #2 Urban, Kids #1, English #1) Key “Network effect” and play on Vernacular media growth - Benefits of Strengths Regional portfolio across News (14) and Entertainment (9) channels Marquee Digital properties (MoneyControl, BookMyShow) & OTT video (VOOT) provides future-proof growth and content synergy Experienced & Professional management team, Strong promoters 3 Network18 group : TV & Digital media, specialized Print & Ticketing ~75% held by Independent Media Trust, of which RIL is Network18 Strategic Investment the sole beneficiary Entertainment Ticketing & Live Network18 has ~39% stake Digital News Broadcasting Print + Digital Magazines Business Finance News Auto Entertainment News & Niche Opinions Infotainment All in standalone entity Network18 holds ~92% in Moneycontrol. Network18 holds ~51% of subsidiary TV18. Others are in standalone entity. TV18 in turn owns 51% in Viacom18 and 51% in AETN18 (see next page for details) TV18 group – Broadcasting pure-play, across News & Entertainment ENTITY GENRE CHANNELS Business News (4 channels, 1 portal) Standalone entity TV18 TV18 General News Group (Hindi & English) Regional News 50% JV with Lokmat group (14 geographies) IBN Lokmat AETN18 Infotainment (Factual & Lifestyle) 51% subsidiary -

Corporate Presentation Media & Investments

Media & Investments Corporate Presentation FY20-21 OVERVIEW 2 Key Strengths Leading Media company in India with largest bouquet of channels (56 domestic channels and 16 international beams), and a substantial digital presence Market-leader in multiple genres (Global top 20 in news pay-apps; top 2 in Digital News in India, #1 Business News channel, top 3 in National News, #2 premium Hindi GEC, Kids #1, English #1) Key “Network effect” and play on Vernacular media growth - Benefits of Strengths Regional portfolio across News (14) and Entertainment (10) channels Marquee Digital properties (MoneyControl, BookMyShow) & OTT video (VOOT) provides future-proof growth and content synergy Experienced & Professional management team, Strong promoters 3 Network18 group : TV & Digital media, specialized Print & Ticketing ~73.15% held by Independent Media Trust, of Network18 Strategic Investment which RIL is the sole beneficiary (total promoter Entertainment holding is 75%) Ticketing & Live Network18 has ~39% stake Digital News Broadcasting Print + Digital Magazines Business Finance News Auto Entertainment News & Niche Opinions Infotainment All in standalone entity Network18 holds ~92% in e-Eighteen Network18 holds ~51% of subsidiary TV18. (Moneycontrol). Others are in standalone TV18 in turn owns 51% in Viacom18 and entity. 51% in AETN18 (see next page for details) TV18 group – Broadcasting pure-play, across News & Entertainment ENTITY GENRE CHANNELS Business News (4 channels, 1 portal) Standalone entity TV18 TV18 General News Group (Hindi & English) Regional News 50% JV with Lokmat group (14 geographies) IBN Lokmat AETN18 Infotainment (Factual & Lifestyle) 51% subsidiary - JV with A+E Networks Entertainment VIACOM18 (inc. Movie production / distribution & OTT) 51% subsidiary - JV with Viacom Inc Regional Entertain. -

BROADCASTER BQ & ALC for UPLOAD.Xlsx

BROADCASTER BOUQUET BROADCASTER BOUQUET NAME BOUQUET TYPE BOUQUET DRP* CHANNEL COUNT CHANNEL NAMES TURNER TURNER KIDS PACK SD 4.25 2 CARTOON NETWORK POGO TURNER TURNER FAMILY PACK SD 10 5 CARTOON NETWORK CNN INTERNATIONAL HBO POGO WB TURNER TURNER FAMILY HD PACK HD 12.5 5 CARTOON NETWORK CNN INTERNATIONAL HBO HD POGO WB TURNER TURNER HD PACK HD 12.5 2 HBO HD CARTOON NETWORK HD+ DISCOVERY BASIC INFOTAINMENT PACK SD 8 8 DISCOVERY CHANNEL ANIMAL PLANET TLC DISCOVERY KIDS DSPORTS JEET PRIME DISCOVERY SCIENCE DISCOVERY TURBO DISCOVERY INFOTAINMENT + SPORTS PACK SD 7 5 DISCOVERY CHANNEL ANIMAL PLANET TLC DISCOVERY KIDS DSPORTS DISCOVERY INFOTAINMENT PACK SD 7 6 DISCOVERY CHANNEL ANIMAL PLANET TLC JEET PRIME DISCOVERY SCIENCE DISCOVERY TURBO * Price is excluding applicable taxes. Channel availability will be subject to Headend capacity and technical feasibility in respective locations. For any further information please call contact center or your Local Cable Operator BROADCASTER BOUQUET BROADCASTER BOUQUET NAME BOUQUET TYPE BOUQUET DRP* CHANNEL COUNT CHANNEL NAMES DISCOVERY KIDS INFOTAINMENT PACK SD 6 4 DISCOVERY CHANNEL ANIMAL PLANET TLC DISCOVERY KIDS DISCOVERY BASIC INFOTAINMENT TAMIL PACK SD 8 9 DISCOVERY CHANNEL ANIMAL PLANET TLC DISCOVERY KIDS DSPORTS JEET PRIME DISCOVERY SCIENCE DISCOVERY TURBO DISCOVERY TAMIL DISCOVERY INFOTAINMENT + SPORTS TAMIL PACK SD 7 6 DISCOVERY CHANNEL ANIMAL PLANET TLC DISCOVERY KIDS DSPORTS DISCOVERY TAMIL DISCOVERY INFOTAINMENT TAMIL PACK SD 7 7 DISCOVERY CHANNEL ANIMAL PLANET TLC JEET PRIME DISCOVERY TAMIL DISCOVERY TURBO DISCOVERY SCIENCE DISCOVERY KIDS INFOTAINMENT TAMIL PACK SD 6 5 DISCOVERY CHANNEL ANIMAL PLANET TLC DISCOVERY KIDS DISCOVERY TAMIL * Price is excluding applicable taxes. -

Full Page Photo

TVml January 19, 2021 National Stock Exchange of India Limited, BSE Limited Exchange Plaza, Plot No. C/1, P J Towers , Dalal Street , G-Block, Bandra-Kurla Complex, Mumbai - 400 001 Bandra (E), Mumbai-400051 Trading Symbol : TV18BRDCST SCRIP CODE: 532800 Sub: Investors' Update - Unaudited Financial Results (Standalone and Consolidated) for the quarter and nine months ended December 31, 2020 Dear Sirs, This is with reference to the captioned Investors' Update filed by the Company. We noticed that inadvertently the consolidated numbers in the "Investors Update" file uploaded earlier were missing. Accordingly, we are attaching herewith the revised file. Please take the same on record. Thanking you, Yours faithfully, For TV18 Broadcast Limited Wd.:,..)('V"..f:.#·t~r__ c} \. I Ratnesh Rukhariyar Company Secretary Encl: as above TV18 Broadcast Limited (CI N- L74300MH2005PLC281753) Regd. office: First Floor, Em pire Complex, 414- Senapati Bapat M ar g, Lower Pare l, M um b ai-400013 T +9 1 22 40019000, 6666 7777 W www.nw18.comE:investors.tv18 @nw18.com A listed subsidiary of Network18 EARNINGS RELEASE: Q3 2020-21 Mumbai, 19th January, 2021 – TV18 Broadcast Limited today announced its results for the quarter and nine months ended 31st December 2020. Summary Consolidated Financials Q3FY21 Q3FY20 Growth 9mFY21 9mFY20 Growth Consolidated Operating Revenue (Rs Cr) 1,361 1,425 -5% 3,150 3,750 -16% Consolidated Operating EBITDA (Rs Cr) 321 281 14% 529 463 14% Operating EBITDA margin 23.6% 19.7% 16.8% 12.3% Highlights for the quarter Q3 Operating EBITDA up 14% YoY, Operating Margin continued to grow to a healthy ~24%. -

EARNINGS RELEASE: Q4 2016-17 Summary Consolidated Financials

A listed subsidiary of Network18 EARNINGS RELEASE: Q4 2016-17 Mumbai, 19th April, 2017 – TV18 Broadcast Limited today announced its results for the quarter and year ended 31st March, 2017. Summary Consolidated Financials Q4 Q4 Growth Growth Particulars (in Rs Crores) FY17 FY16 FY17 FY16 YoY% YoY% Revenue (incl. proportionate share of JVs) 715.4 669.3 7% 2,676.9 2,494.8 7% Segment profit (incl. prop. share of JVs) 22.1 96.7 -77% 61.5 236.3 -74% Adjusted Segment profit (incl. prop. share of JVs)* 92.6 96.7 -4% 308.3 236.3 30% Revenue (as per Ind AS) 278.9 301.6 -8% 979.4 924.9 6% Operating profit (as per Ind AS) 26.4 91.6 -71% 31.3 130.9 -76% Adjusted Operating profit (as per Ind AS)* 60.9 91.6 -33% 138.2 130.9 6% (*) - Adjusted for the impact of new initiatives launched within a year /one-time expense TV18 posted consolidated revenues of Rs. 2,677 crores (including proportionate share of JVs) in FY17, a 7% YoY growth, driven by entertainment and national news. Segment profits were impacted by investments in new initiatives in regional and digital, and a pullback in advertising spends in the latter half of the year. However, adjusted for the investments in new initiatives and one-time expenses, segment profits at Rs. 308 crores were up 30% YoY. Highlights for the quarter ¾ Tepid ad-industry environment dragged revenues, especially in regional markets. The media industry is still facing impact of deferment of advertising spends that kicked-in from November-December 2016 on likely slow-down in consumer spending. -

VICTORY DIGITAL NETWORK PRIVATE. LIMITED., No.1946, 2Nd Floor, Sonalika Tractors Building, Opp: Jain Bajaj, Landmark, State Bank of India, P.B

VICTORY DIGITAL NETWORK PRIVATE. LIMITED., No.1946, 2nd Floor, Sonalika Tractors Building, Opp: Jain Bajaj, Landmark, State Bank of India, P.B. Road, DAVANGERE-577006 A-LA-CARTE CHANNELS AND PACKAGES SELECTION FORM Name Address Mobile No. CUST ID STB/VC No. Reference No. V I C T C O D E Price Details: - Please select your option, Minimum Network Capacity Fee will be Rs.130+18% GST for first 100 Channels and Rs.20+18% GST for 25 Channels. BASIC-1 100 Channels NCF 153.40 BASIC-2 25 Channels NCF 23.60 PAY CHANNELS A-LA-CARTE PRICE WITH 18% GST CHANNEL NAME √ Rs. CHANNEL NAME √ Rs. CHANNEL NAME √ Rs. UDAYA TV 20.06 MOVIES NOW 11.80 DISCOVERY KIDS 03.54 UDAYA MOVIES 18.88 ROMEDY NOW 07.08 HUNGAMA 07.08 UDAYA MUSIC 07.08 SONY PIX 11.80 ZEE CINEMALU 11.80 UDAYA COMEDY 07.08 ZEE CAFÉ 17.70 STAR MAA 22.42 CHINTU 07.08 COLORS INFINITY 08.26 ETV TELUGU 20.06 STAR SUVARNA 22.42 COMEDY CENTRAL 08.26 GEMINI 22.42 SUVARNA PLUS 05.90 AXN 05.90 GEMINI MOVIES 20.06 STAR SPORTS KAN 22.42 BBC WORLD NEWS 01.18 GEMINI MUSIC 04.72 COLORS KANNADA 22.42 TIMES NOW 03.54 GEMINI COMEDY 05.90 COLORS KAN CINEMA 02.36 ET NOW 03.54 ZEE TELUGU 22.42 COLORS SUPER 03.54 MIRROR NOW 02.36 MAA MOVIES 11.80 ZEE KANNADA 22.42 CNN NEWS18 00.59 MAA GOLD 02.36 NEWS18 KANNADA 00.29 CNBC TV18 04.72 MAA MUSIC 01.18 STAR PLUS 22.42 ZEE BUSINESS 00.11 KUSHI 04.72 SONY 22.42 ZEE NEWS 00.11 SUN TV 22.42 STAR BHARAT 11.80 NDTV 24X7 03.54 STAR VIJAY 22.42 COLORS 22.42 NDTV PROFIT 01.18 SUN MUSIC 07.08 SONY SAB 22.42 NDTV INDIA 01.18 KTV 22.42 ZEE TV 22.42 AAJ TAK 00.89 ADITYA 10.62 & TV -

Hathway Recommended Pack

HATHWAY RECOMMENDED PACK KARNATAKA Prices are excluding taxes INFINITY HD MRP : ₹ 668 (142 PAY CHANNELS + KARNATAKA FTA) Total Pay Channels 78 SD + 64 HD (Excluding tax) LANG - GENRE CHANNEL_NAME SD/HD Bengali - Gec SONY AATH SD English - Gec STAR WORLD HD HD English - Gec STAR WORLD PREMIERE HD HD English - Gec ZEE CAFE HD HD English - Infotainment TLC HD HD English - Kids BABY TV HD HD English - Kids NICK JR SD English - Movie &FLIX HD HD English - Movie &PRIVE HD HD English - Movie HBO HD HD English - Movie MN+ HD HD English - Movie MNX HD HD English - Movie MOVIES NOW HD HD English - Movie ROMEDY NOW HD HD English - Movie SONY PIX HD HD English - Movie STAR MOVIES HD HD English - Movie STAR MOVIES SELECT HD HD English - Movie WB SD English - Music VH1 HD HD English - News BBC WORLD NEWS SD English - News CNBC TV18 SD English - News CNN INTERNATIONAL SD English - News CNN NEWS18 SD English - News ET NOW SD English - News INDIA TODAY SD English - News MIRROR NOW SD English - News NDTV 24X7 SD English - News NDTV PROFIT SD English - News TIMES NOW SD English - News TIMES NOW WORLD HD HD English - Sports EUROSPORT HD HD Hindi - Gec &TV HD HD Hindi - Gec BIG MAGIC SD Page 1 of 98 Hindi - Gec COLORS HD HD Hindi - Gec COLORS RISHTEY SD Hindi - Gec INVESTIGATION DISCOVERY HD HD Hindi - Gec SONY HD HD Hindi - Gec SONY PAL SD Hindi - Gec SONY SAB HD HD Hindi - Gec ZEE ANMOL SD Hindi - Gec ZEE TV HD HD Hindi - Infotainment HISTORY TV18 HD HD Hindi - Kids CARTOON NETWORK SD Hindi - Kids NICK SD Hindi - Kids NICK HD+ HD Hindi - Kids POGO SD Hindi -

Suggestive Combinations

Suggestive Combinations For Territory of Karnataka Price Sno Pack Name (excluding taxes) 1 Bangalore, Karnataka Pack 220 220.00 2 Bangalore, Karnataka Pack 230 230.00 3 Bangalore, Karnataka Pack 233 233.00 4 Bangalore, Karnataka Pack 274 274.00 5 Bangalore, Karnataka Pack 296 296.00 6 Bangalore, Karnataka Pack 415 415.00 Suggestive Combo- Bangalore, Karnataka Pack 220 Colors Kannada, Colors Super, Colors Tamil, Udaya TV, Udaya Comedy, Star Suvarna, Zoom General Entertainment Colors Kannada Cinema, Udaya Movies, Suvarna Plus Movies Udaya Music Music CNBC TV18, CNN News18, News18 Kannada, News18 Urdu, Times Now, ET Now, Mirror Now, Aaj Tak, Tez, India Today News and Current Affairs FYI TV 18, The History Channel, National Geographic, Nat Geo Wild, Discovery Channel, Animal Planet, TLC Infotainment Nick, Nick Jr, Sonic, Chintu TV, Discovery Kids, Cartoon Network, Pogo, SONY YAY! Kids Star Sports 1 Kannada, Star Sports 2, Star Sports 3, Star Sports First Sports Note :: Channels availability would vary for different locations. This suggestive combo is along with BST. These suggestive packs are only an indicative one for the consumers guidance. Consumers can opt any channel of their choice. Suggestive Combo- Bangalore, Karnataka Pack 230 Maa TV, Gemini TV, Gemini Comedy, Gemini Life, Zee Telugu, Zee Keralam, Zoom General Entertainment Maa Movies, Maa Gold, Gemini Movies, Zee Action, Zee Cinemalu Movies Maa Music, Gemini Music, Zee ETC Music Zee News, Zee Hindustan, WION, Times Now, ET Now, Mirror Now, Aaj Tak, Tez, India Today News and Current Affairs National Geographic, Nat Geo Wild, Living Foodz, Discovery Channel, Animal Planet, TLC Infotainment Kushi TV, Discovery Kids, Cartoon Network, Pogo, SONY YAY! Kids Star Sports 1 Telugu, Star Sports 2, Star Sports 3, Star Sports First Sports Note :: Channels availability would vary for different locations. -

List of Pay Channels

List of Pay Channels SL# CHANNEL NAMES SD/HD LANGUAGE GENRE BROADCASTER NAME DRP 1 & FLIX SD ENGLISH MOVIES ZEE 15.00 2 & FLIX HD HD ENGLISH MOVIES ZEE 19.00 3 & PICTURES SD HINDI MOVIES ZEE 10.00 4 & PRIVE HD HD ENGLISH MOVIES ZEE 19.00 5 & TV SD HINDI GEC ZEE 12.00 6 24 GHANTA SD BENGALI GEC ZEE 0.10 7 AAJ TAK SD HINDI NEWS TV TODAY 0.75 8 ADITHYA TV SD TAMIL MOVIES SUN 9.00 9 ANIMAL PLANET SD ENGLISH INFO & LIFESTYLE DISCOVERY 2.00 10 ANIMAL PLANET HD HD ENGLISH INFO & LIFESTYLE DISCOVERY 3.00 11 ASIANET SD MALAYALAM GEC STAR 19.00 12 ASIANET HD HD MALAYALAM GEC STAR 19.00 13 ASIANET MOVIES SD MALAYALAM MOVIES STAR 15.00 14 ASIANET PLUS SD MALAYALAM GEC STAR 5.00 15 AXN SD ENGLISH GEC SONY 5.00 16 AXN HD HD ENGLISH GEC SONY 7.00 17 BBC WORLD SD ENGLISH NEWS BBC 1.00 18 BINDASS SD HINDI GEC DISNEY 1.00 19 CARTOON NETWORK SD ENGLISH KIDS TURNER 4.25 20 CHINTU TV SD KANNADA KIDS SUN 6.00 21 CHUTTI TV SD TAMIL KIDS SUN 6.00 22 CNBC AWAAZ SD HINDI NEWS TV18 1.00 23 CNBC TV18 SD ENGLISH NEWS TV18 4.00 24 CNBC TV18 HD HD ENGLISH NEWS TV18 1.00 25 CNN SD ENGLISH NEWS TURNER 0.50 26 CNN NEWS18 SD ENGLISH NEWS TV18 0.50 27 COLORS SD HINDI GEC TV18 19.00 28 COLORS BANGLA SD BENGALI GEC TV18 7.00 29 COLORS BANGLA HD HD BENGALI GEC TV18 14.00 30 COLORS GUJRATHI SD GUJARATI GEC TV18 5.00 31 COLORS INFINITY SD ENGLISH GEC TV18 7.00 32 COLORS INFINITY HD HD ENGLISH GEC TV18 9.00 33 COLORS KANNADA SD KANNADA GEC TV18 19.00 34 COLORS KANNADA CINEMA SD KANNADA MOVIES TV18 2.00 35 COLORS KANNADA HD HD KANNADA GEC TV18 19.00 36 COLORS MARATHI SD MARATHI