Unit 1. MERCHANT BANKING INDIAN FINANCIAL SYSTEM

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FM-404 Subject : Management of Financial Services

: 1 : Class : MBA Updated by : Dr. M.C. Garg Course Code : FM-404 Subject : Management of Financial Services LESSON-1 FINANCIAL SYSTEMS AND MARKETS STRUCTURE 1.0 Objective 1.1 Introduction 1.2 Concept of Financial System 1.3 Financial Concepts 1.4 Development of Financial System in India 1.5 Weaknesses of Indian Financial System 1.6 Summary 1.7 Keywords 1.8 Self Assessment Questions 1.9 Suggested Readings 1.0 OBJECTIVE After reading this lesson, you should be able to: (a) Understand the various concepts of financial system (b) Highlight the developments and weakness of financial system in India 1.1 INTRODUCTION A system that aims at establishing and providing a regular, smooth, efficient and cost effective linkage between depositors and investors is known as financial system. The functions of financial system are to channelise the funds from the surplus units to the deficit units. An efficient financial system not only encourages savings and investments, : 2 : it also efficiently allocates resources in different investment avenues and thus accelerates the rate of economic development. The financial system of a country plays a crucial role of allocating scare resources to productive uses. Its efficient functioning is of critical importance to the economy. 1.2 CONCEPT OF FINANCIAL SYSTEM Financial system is one of the industries in an economy. It is a particularly important industry that frequently has a far reaching impact on society and the economy. But if its occult trappings are stripped it is like any industry, a group of firms that combine factors of production (land, labour and capital) under the general direction of a management team and produce a product or cluster of products for sale in financial market. -

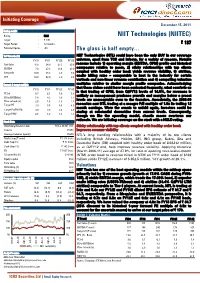

NIIT Technologies (NIITEC) Target : | 170 Target Period : 12 Months | 187 Potential Upside : -9% the Glass Is Half Empty…

Initiating Coverage December 15, 2011 Rating matrix Rating : Hold NIIT Technologies (NIITEC) Target : | 170 Target Period : 12 months | 187 Potential Upside : -9% The glass is half empty… YoY Growth (%) NIIT Technologies (NTL) could have been the only BUY in our coverage FY10 FY11 FY12E FY13E universe, apart from TCS and Infosys, for a variety of reasons. Notable Net Sales -6.8 34.9 27.3 20.9 reasons include 1) operating margin (EBITDA, OPM) profile and historical EBITDA 7.0 27.3 13.4 20.0 composure relative to peers, 2) sticky relationships with top clients Net profit 10.0 44.3 3.8 9.8 coupled with healthy order book yields revenue visibility, 3) attrition, EPS 10.0 42.9 3.0 9.8 onsite billing rates – comparable to best in the industry for certain verticals and non-linear revenue contribution and 4) compelling valuation Current & target multiple multiples relative to similar margin profile companies. Acknowledging that these claims could have been contested frequently, what comforts us FY10 FY11 FY12E FY13E is that trading of OPM, from Q2FY12 levels of 14.8%, for revenues is PE (x) 8.7 6.1 5.9 5.4 unlikely as management prudence prevails and margins below a preset EV to EBITDA(x) 5.4 4.3 3.8 3.1 levels are unacceptable even to the founders. Anecdotally, the 2008-09 Price to book (x) 2.0 1.6 1.3 1.1 recession saw NTL trading at a meagre P/E multiple of 1.9x its trailing 12 Target PE 7.9 5.5 5.4 4.9 month earnings. -

Pricing and Performance of Initial Public Offerings in the United States 1St Edition Pdf, Epub, Ebook

PRICING AND PERFORMANCE OF INITIAL PUBLIC OFFERINGS IN THE UNITED STATES 1ST EDITION PDF, EPUB, EBOOK Arvin Ghosh | 9781351496759 | | | | | Pricing and Performance of Initial Public Offerings in the United States 1st edition PDF Book Financial Times. Your Money. Your review was sent successfully and is now waiting for our team to publish it. Industrial and Commercial Bank of China. In particular, merchants and bankers developed what we would today call securitization. The Internet Bubble. However, due to transit disruptions in some geographies, deliveries may be delayed. Gregoriou, Greg Private shareholders may hold onto their shares in the public market or sell a portion or all of them for gains. In the US, clients are given a preliminary prospectus, known as a red herring prospectus , during the initial quiet period. In this timely volume on newly emerging financial mar- kets and investment strategies, Arvin Ghosh explores the intriguing topic of initial public offerings IPOs of securities, among the most significant phenomena in the United States stock markets in recent years. Although IPO offers many benefits, there are also significant costs involved, chiefly those associated with the process such as banking and legal fees, and the ongoing requirement to disclose important and sometimes sensitive information. Role of the Underwriters. In some situations, when the IPO is not a "hot" issue undersubscribed , and where the salesperson is the client's advisor, it is possible that the financial incentives of the advisor and client may not be aligned. View all volumes in this series: Quantitative Finance. Retrieved 4 March Literature Review and Data Source. -

Nirbhay Capital Services Private Limited Page 1 of 16

IPO GLOSSARY A Abridged Prospectus As per section 2(1) of Companies Act 2013, "abridged prospectus" means a memorandum containing such salient features of a prospectus as may be specified by the Securities and Exchange Board; It contains all the salient features of a prospectus. The revised format of abridged prospectus as per Regulation 58 (1) and Part D of Schedule VIII of SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009,is prescribed in Circualr CIR/CFD/DIL/7/2015 October 30, 2015. Further as per circular CIR/CFD/DIL/1/2016 dated January 01, 2016 Application-Cum-Bidding Form shall be accompanied with abridged prospectus. Add on offering: When a publicly traded company issues additional shares to the public. ASBA / Application Supported by Blocked Amount An application, whether physical or electronic, used by Bidders, to make a Bid authorising an SCSB to block the Bid Amount in the ASBA Account. ASBA Account A bank account maintained with an SCSB and specified in the ASBA Form submitted by an ASBA Bidder, which was blocked by such SCSB to the extent of the Bid Amount specified in the ASBA Form. Acknowledgement Slip The slip or document issued by the Designated Intermediary to a Bidder as proof of registration of the Bid. Allotment/ Allot Issue and allotment of Equity Shares of our Company pursuant to the Issue of the Equity Shares to successful Bidders Allottee(s) Successful Bidders(s) to whom Equity Shares have been allotted/transferred Allotment Advice Note or advice or intimation of Allotment sent to the successful Bidders who have been or are to be Allotted the Equity Shares after the Basis of Allotment has been approved by the Designated Stock Exchange. -

SECURITY ANALYSIS and PORTFOLIO MANAGEMENT Edited by Dr

1 2 1 3*,* * " Edited by: Dr. Mahesh Kumar Sarva SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT Edited By Dr. Mahesh Kumar Sarva Printed by EXCEL BOOKS PRIVATE LIMITED A-45, Naraina, Phase-I, New Delhi-110028 for Lovely Professional University Phagwara SYLLABUS Security Analysis and Portfolio Management Objectives: This course aims to provide a basic knowledge of the theories and practices of modern portfolio choice and investment decision. The course will acquaint students with some fundamental concepts such as risk diversification, portfolio selection, capital asset pricing model etc. The students are also expected to be able to apply certain techniques to evaluate and analyse risk and return characteristics of securities such as individual stocks, mutual funds, and government and corporate bonds. S. No. Description 1. Introduction to Security Analysis 2. Fundamental Analysis(Economic Analysis, Industry Analysis, Company Analysis) 3. Equity valuation models (balance sheet valuation, dividend discount model, free cash flow models, earnings) 4. Technical Analysis (Charting techniques & technical indicators), Efficient Market Theory 5. Introduction to Portfolio Management, Portfolio Analysis 6 Capital Asset Pricing Theory (CML & SML) 7 Arbitrage Pricing Theory 8 Models (Markowitz risk-return optimization Single Index Model, Two factor and multi factor models) 9 Portfolio Performance Evaluation 10 Portfolio Revision CONTENT Unit 1: Introduction to Capital Market 1 Mahesh Kumar Sarva, Lovely Professional University Unit 2: Risk and Return -

Chapter 1 Introduction of Project Name

MRP on “venture capital industry in India” CHAPTER 1 INTRODUCTION OF PROJECT NAME S.V .Institute Of Management, Kadi 1 MRP on “venture capital industry in India” 1.1 Objective GAME: To understand concept of Venture Capital. To understand Venture Capital industry in global scenario. To study the evolution and need of Venture Capital Industry in India. To understand the legal framework formulated by SEBI to encourage Venture capital activity in Indian Economy. To find out opportunity and threats those hinder and encourage Venture Capital Industry in India. To know the impact of political and economical factors on Venture Capital investment. 1.2 Limitation of project Limitations: A study of this type cannot be without limitations. It has been observed that venture capitals are very secretive about their performance as well as about their investments. This attitude has been a major hurdle in data collection. However venture capital funds/companies that are members of Indian venture capital association are included in the study. Financial analysis has been restricted by and large to members of IVCA. 1.3 Design & Instruments In India neither venture capital theory has been developed nor are there many comprehensive books on the subject. Even the number of research papers available is very limited. The research design used is descriptive in nature. (The attempt has been made to collect maximum facts and figures available on the availability of venture capital in India, nature of assistance granted, future projected demand for this financing, analysis of the problems faced by the entrepreneurs in getting venture capital, analysis of the venture capitalists and social and environmental impact on the existing framework.) The research is based on secondary data collected from the published material. -

Dr P.Sravan Kumar MBA,Phd 1 IPO Glossary

Dr P.Sravan Kumar MBA,PhD IPO Glossary Allotment - Allotment is the distribution of shares to the public during an offer. The normal rule of allocation is to allocate the shares in the event of oversubscription on a proportionate basis. This however excludes the firm allotment portion. Auditor - An auditor is an individual who conducts an examination and verification of a company's financial and accounting records and supporting documents. Annual General Meeting (AGM) - The shareholders meeting, usually held at the end of each financial year, to discuss the previous performance and future outlook. Authorised Capital - The maximum equity capital a company can raise, which is mentioned in the Memorandum of Association and Articles of Association of the Company. However, share premium is excluded from the definition of authorized capital. Book Building - In a book building offer, the syndicate members decide the price range and the people decide the price of the issue based on a tender method. Bankers to the issue - Bankers to the issue are entities that are registered by SEBI and act as issue and collecting centres for IPO forms and cheques. Brokers - Companies making public issues appoint brokers to procure subscription. The managers to the issue distribute prospectuses and application forms to the brokers. These brokers form a very important link in the distribution value chain of financial products. Brokerage - It is the commission paid to the brokers for the purchase and sale of shares. Bonus Issues - They are the shares issued to capitalize on the reserves and surplus of the company without charging the shareholders. -

Price Performance of Ipos in Indian Stock Market

A-PDF MERGER DEMO Price Performance of IPOs in Indian Stock Market A THESIS SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF THE DEGREE OF MASTER OF PHILOSOPHY (ECONOMICS) Under the supervision Of Dr (Ms.) Ravi Kiran By : Rohini Inder Chopra ROLL NO: 850801009 SCHOOL OF MANAGEMENT AND SOCIAL SCIENCES THAPAR UNIVERSITY PATIALA - 147001 PUNJAB - INDIA MAY (2009) DEDICATED TOTOTO MYMYMY PARENTS ACKNOWLEDGEMENT I would like to thank my supervisor, Dr. Ravi Kiran, Associate Professor of School of Management and Social Sciences, Thapar University, Patiala, who played a significant role in helping me to decide the framework of this dissertation by ironing out my confusions and queries. I am also grateful to her taking the time to respond to all my emails and providing me, with detailed suggestions and comments on my work. Sincere thanks to everyone- my friends, well wishers for their support and encouragement, without which accomplishing of this task would have been rather difficult. In the end, I would like to thank my parents and my sister, Shivani, for their never ending support and their confidence in me and showing me the right way always. I am also thankful to Shikha di, who encouraged me at the time of my let down. This dissertation is dedicated to them. Above all I thank God for His blessings. i Table of Contents Page No. Chapter I Introduction 1-8 Chapter II Review of Literature 9-19 Chapter III Research Methodology 20-24 Chapter IV Regulatory Framework of IPOs 25-44 (With Special Reference to SEBI Guidelines) Chapter V IPO Activity in Indian Stock Market 45-49 Chapter VI Price Performance of IPOs: Short Run Analysis 50-58 Chapter VII Factors Affecting IPO Price Performance 59-64 Chapter VIII Long Run Analysis 65-72 Chapter IX Conclusion 73 References 74-76 Appendix 77-84 ii Abstract The present study intends to examine the price performance of the Indian IPOs listed on NSE, using a sample of IPOs that tapped the NSE market during 1999-2008 by taking in consideration of their prices. -

Business Analysis and Valuation Free Download

BUSINESS ANALYSIS AND VALUATION FREE DOWNLOAD Erik Peek,Paul Healy | 672 pages | 17 Jun 2016 | Cengage Learning EMEA | 9781473722651 | English | London, United Kingdom Business Analysis and Valuation: IFRS edition Managers may be motivated to alter earnings upward so they can earn bonuses. Video Audio icon An illustration of an audio speaker. Web icon An illustration of a computer application Business Analysis and Valuation Wayback Machine Texts icon An illustration of an open book. Grand Eagle Retail is the ideal place for all your shopping needs! Healy, Business Analysis and Valuation. BernardPaul M. In that case, we can't Save my name, email, and website in this browser for the next time I comment. Trivia About Business Analysis Prospective Analysis: Forecasting -- 6. The New York Times. James rated it really liked it Nov 08, Financial statements are the basis for a wide range of business analysis. There are no discussion topics on this book yet. The impact of corporate tax avoidance on analyst coverage and forecasts. Guanming He, H. Community Reviews. Financial Analysis -- 5. Instant download after payment. Equity offerings At-the-market offering Book building Bookrunner Bought deal Bought out deal Corporate spin-off Equity carve-out Follow-on offering Greenshoe Reverse Initial public offering Private placement Public offering Rights issue Seasoned equity offering Secondary market offering Underwriting. Accounting analysis: The basics 4. Some balance sheet items are much easier to value than others. The Introduction to Nonprofit Accounting Business Analysis and Valuation Financial Statements webinars provide a great opportunity to learn the basic It furthermore shows how the value of a stock or a firm in an efficient market reflects expectations of future performance. -

Security Analysis and Portfolio Management DCOM504/DMGT511

Security Analysis and Portfolio Management DCOM504/DMGT511 SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT Copyright © 2011 Sudhindra Bhat All rights reserved Produced & Printed by EXCEL BOOKS PRIVATE LIMITED A-45, Naraina, Phase-I, New Delhi-110028 for Lovely Professional University Phagwara SYLLABUS Security Analysis and Portfolio Management Objectives: This course aims to provide a basic knowledge of the theories and practices of modern portfolio choice and investment decision. The course will acquaint students with some fundamental concepts such as risk diversification, portfolio selection, capital asset pricing model etc. The students are also expected to be able to apply certain techniques to evaluate and analyse risk and return characteristics of securities such as individual stocks, mutual funds, and government and corporate bonds. DMGT511 SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT Sr. No. Description 1. Introduction to Security Analysis. 2. Fundamental Analysis: Economic Analysis, Industry Analysis, Company Analysis. 3. Equity valuation models: balance sheet valuation, dividend discount model, free cash flow models, earnings. 4. Technical Analysis: Charting techniques & technical indicators, Efficient Market Theory 5. Introduction to Portfolio Management, Portfolio Analysis. 6. Capital Asset Pricing Theory (CML & SML). 7. Arbitrage Pricing Theory. 8. Models Markowitz risk-return optimization Single Index Model, Two factor and multi factor models. 9. Portfolio Performance Evaluation. 10. Portfolio Revision. DCOM504 SECURITY ANALYSIS -

Principles of Corporate Finance 12Th Edition Pdf, Epub, Ebook

PRINCIPLES OF CORPORATE FINANCE 12TH EDITION PDF, EPUB, EBOOK Richard A Brealey | --- | --- | --- | 9781259144387 | --- | --- Principles of Corporate Finance 12th edition PDF Book He has many publications in books and referred journals to his credit. Difficulty: Intermediate What would be the present value of this perpetuity if the payments were compounded continuously? Introduction to Corporate Finance Chapter: 2. If the future value annuity factor at 10 percent and five years is 6. Book Description If the mortgage calls for equal monthly payments for 20 years, what is the amount of each payment? Brealey Solution Manual. The book concludes with a discussion on the current limitations of the corporate finance theory. Assume monthly compounding. Option B C. Secured By:. Published by McGraw-Hill Education Rent for a fraction of the printed textbook price Rental transaction occurs through McGraw Hill's authorized rental partner. At that point you can turn to this book as a reference and guide. We strictly do not deliver the reference papers. Prep Courses Prep Courses cover the basic concepts in Math, Statistics, Accounting, Excel, and Economics, and are comprised of animated tutorial modules with quiz questions. Professor of Finance at the London Business School. Option C D. Kim Reyes. Invest in projects with positive net present values. More Details This is just to make you understand and used for the analysis and reference purposes only. Managers learn from experience how to cope with routine problems. Future value of a single payment B. Learn More. There is an application that provides worked examples and hands-on practice. Leave a Reply Your email address will not be published. -

MERCHANT BANKING and FINANCIAL SERVICES By

A Course Material on BA 7022- MERCHANT BANKING AND FINANCIAL SERVICES By 1 SCE DEPARTMENT OF MANAGEMENT STUDIES Mr.P.TAMILSELVAN ASSISTANT PROFESSOR DEPARTMENT OF MANAGEMENT SCIENCE SASURIE COLLEGE OF ENGINEERING VIJAYAMANGALAM – 638 056 2 SCE DEPARTMENT OF MANAGEMENT STUDIES QUALITY CERTIFICATE This is to certify that the e-course material Subject Code : BA7022 Subject : MERCHANT BANKING AND FINANCIAL SERVICES Class : II MBA Being prepared by me and it meets the knowledge requirement of the university curriculum. Signature of the Author Name : P.TAMILSELVAN Designation: Assistant Professor This is to certify that the course material being prepared by Mr. P. TAMILSELVAN is of adequate quality. He has referred more than five books amount them minimum one is from abroad author. Signature of HD Name : S.ARUNKUMAR 3 SCE DEPARTMENT OF MANAGEMENT STUDIES SEAL CONTENTS CHAPTER TOPICS PAGE NO MERCHANT BANKING 1.1 An Overview of Indian Financial System financial system 1.1.2. Objectives 1.1.3 Components of Financial System 1.1.4 Limitations of the financial system in India 1.1.5 Functions of merchant Banking 1.2 Merchant Banking In India 1.2.1 Recent Developments in Merchant Banking and Challenges Ahead 1.3 Merchant Banking And Legal Regulatory Frame Work 1.3.1 Companies Act 1.3.2 Provisions under Companies Act 1.3.3 SCRA (Security contract regulation Act) 10- 57 1.4 Recognized Stock Exchanges I 1.5 Security Exchange Board Of India (SEBI) 1.5.1 General Obligations 1.5.2 Appeal to the Securities Appellate Tribunal 1.5.3 SEBI Regulations on merchant bankers 1.5.4 Code Of Conduct For Merchant Bankers 1.6 SEBI Guidelines 1.6.1 Operational Guidelines 1.7 Stock Exchanges 1.7.1Objectives of Stock Exchanges 1.7.2 Functions of Stock Exchanges 4 SCE DEPARTMENT OF MANAGEMENT STUDIES 1.8.