State of Washington Agenda

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Washington State Senate

Washington State Senate Chair Fitzgibbon, Thank you for your dedication to pursuing the Low Carbon Fuel Standard for our state. While we sometimes disagree on the methods, we all share a commitment to ensuring our state does its part in reducing our carbon footprint to address climate change. As you know, HB 1091 passed the Senate Thursday night on a vote of 27-20. Our five votes represent more than the margin of passage and it is crucial that you know the changes made to the legislation in the Senate were integral to our support for the bill. We worked closely with our partners in the Building Trades to make sure all voices were heard. As we likely head to conference, these are the Senate changes to the legislation that must stay in the final bill to earn our support: • Ensure that this policy does not dramatically increase the cost of fuel, which is a burden that will likely fall on consumers and disproportionately impact those who can least afford it. • Ensure that Washington State benefits from the jobs created by the additional money that will be spent by consumers on low carbon fuels. This includes new biofuel facilities in Washington and an assurance that some of the crops used to make those fuels come from our state. • The bill must maintain a link to the transportation package. • Maintain the legislative review beyond the 10% threshold so that elected officials can weigh the efficiency of the policy after implementation. Addressing our climate impacts doesn’t have to be just a bitter pill. -

Appendix B – Communications Received

APPENDIX B – COMMUNICATIONS RECEIVED This appendix contains all the communications received during the post-centerline release period from November 18, 2010 through December 31, 2011. In addition, the table below contains contact and organization names and the communication identification number assigned to each communication. The communication text in this appendix is ordered by the communication identification number. For reference, the table below is ordered by last name followed by illegible and anonymous signatures. Referenced attachments can be found by searching for the communication on the project website http://www.bpa.gov/corporate/I-5-EIS/search.cfm. Number Date Name - First Name - Last Organization 13665 7/20/2011 ANDREW ABBOTT 13665 7/20/2011 JACK ABERNATHY 13665 7/20/2011 CRYSTAL L ADAMS 13395 1/29/2011 PHIL AKELY 13667 7/20/2011 AMBER ALEXANDER 13665 7/20/2011 BOB ALEXANDER 13665 7/20/2011 CHEE ALLISON 13755 10/6/2011 ROBERT AMMONS 13683 8/3/2011 CANDICE D ANDERSON 13418 2/10/2011 CURTIS L ANDERSON 13207 12/2/2010 M. ANDERSON 13073 11/22/2010 GINA L ANDREWS STATE OF WASHINGTON, RECREATION AND 13836 12/15/2011 JIM ANEST CONSERVATION OFFICE 13665 7/20/2011 TRAVIS APP 13665 7/20/2011 BOB APPLING 13665 7/20/2011 JEREMY ARIONUS 13665 7/20/2011 CHUCK ARNST 13322 12/8/2010 DALE W AROLA 13321 12/9/2010 DALE W AROLA 13320 12/10/2010 DALE W AROLA 13527 1/28/2011 DALE W AROLA 13320 12/10/2010 DARREN F AROLA 13527 1/28/2011 DARREN F AROLA 13321 12/9/2010 DWAYNE D AROLA 13527 1/28/2011 DWAYNE D AROLA 13665 7/20/2011 BRIAN ASBURRY 13665 -

Washington State Senate 2016

WASHINGTON STATE SENATE 2016 Senator Jan Angel (R) District 26 INB 203A 360‐786‐7650 [email protected] Financial Institutions & Insurance, Vice Chair; Health Care; Trade & Economic Development Legislative Asst: Debbie Austin Senator Barbara Bailey (R) District 10 INB 109B 360‐786‐7618 [email protected] Higher Education, Chair; Health Care; Rules; Ways & Means Legislative Asst: Vicki Angelini Senator Michael Baumgartner (R) District 6 LEG 404 360‐786‐7610 [email protected] Commerce and Labor, Chair; Higher Education, Vice Chair; Health Care; Transportation Legislative Asst: Kaleb Hoffer Senator Randi Becker (R) District 2 INB 110 360‐786‐7602 [email protected] Health Care, Chair; Higher Education; Ways & Means Legislative Asst: Tiffani Sanné WASHINGTON STATE SENATE 2016 Senator Don Benton (R) District 17 LEG 409 360‐786‐7632 [email protected] Financial Institutions & Insurance, Chair; Government Operations and State Security , Vice Chair; Transportation, Vice Chair; Rules Legislative Asst: Alexander Bohler Senator Andy Billig (D) District 3 LEG 412 360‐786‐7604 [email protected] Early Learning & K‐12 Education; Rules; Ways & Means Legislative Asst: Kate Burke Senator John Braun (R) District 20 LEG 407 360‐786‐7638 [email protected] Commerce and Labor, Vice Chair; Trade & Economic Development, Vice Chair; Ways & Means, Vice Chair; Energy, Environment & Telecommunications Legislative Asst: Ruth Peterson Senator Sharon Brown (R) District 8 INB 202 360‐786‐7614 [email protected] Trade & Economic -

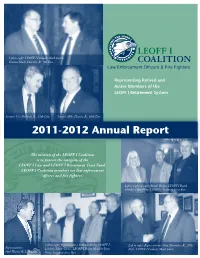

LEOFF I Coalition 2011-2012 Annual Report

Left to right: LEOFF I Lobbyist Mark Curtis, Senator Mark Schoesler, R., 9th Dist. Law Enforcement Officers & Fire Fighters Representing Retired and Active Members of the LEOFF I Retirement System Senator Tim Sheldon, D., 35th Dist. Senator Mike Hewitt, R., 16th Dist. 2011-2012 Annual Report The mission of the LEOFF I Coalition is to protect the integrity of the LEOFF I Law and LEOFF I Retirement Trust Fund. LEOFF I Coalition members are law enforcement officers and fire fighters. Left to right: Senator Randi Becker, LEOFF I Board Member Dave Peery, LEOFF I Treasurer Jerry Birt Left to right: Representative Barbara Bailey, LEOFF I Left to right: Representative Gary Alexander, R., 20th Representative Lobbyist Mark Curtis, LEOFF I Board Member Dave Dist., LEOFF I Lobbyist Mark Curtis Paul Harris, R.,17th Dist. Peery, Treasurer Jerry Birt LEOFF I Coalition Annual Report Law Enforcement Officers & Fire Fighters LEOFF I Coalition Board Another Year and We Still Have President Don Daniels Washington State Law Our Pension Enforcement Association Retired Seattle PD By President Don Daniels Lobbyist/Secretary Mark Curtis nother year has passed, and 2011-2012 Annual Report [email protected] Wa. State Retired Deputy we’ve fought another battle to Sheriff’s & Police Officers Assoc. protect our pension benefits and Retired Thurston County A thankfully we have won another victory. Sheriff’s Office For the second year in a row, the Treasurer Jerry Birt LEOFF I community has beaten back [email protected] attempts to merge the LEOFF I and Retired Seattle Fire Dept. LEOFF 2 pension systems. HB 2350 and SB 6563 were bad bills for us. -

WASHINGTON STATE SENATE 2018 Legislative Scorecard Environment

Environment Washington WASHINGTON STATE SENATE 2018 Legislative Scorecard Environment Washington is a citizen advocacy group that combines independent research, practical ideas and tough-minded advocacy to Senator Energy Efficient Banning Invasive Healthy Food Oil Transportation Toxic Chemicals in Orca Protection Act Nonnative Fish overcome the opposition of powerful special Party District 1. Buildings 2. Atlantic Salmon 3. Packaging 4. Safety 5. Firefighting Foam 6. 9. 2018 Score interests and win real results for Washington’s Jan Angel R 26 - + - + + - + 57% environment. We have compiled this legislative Barbara Bailey R 10 - - - + - - + 29% scorecard as a tool to educate Washington citizens Michael Baumgartner R 6 - - - + E - + 43% Randi Becker R 2 - - - + - - - 14% about the voting records of their elected officials. Andy Billig D 3 + + + + + + + 100% John Braun R 20 - - + + + + - 57% Sharon Brown R 8 - - - - + - - 14% Votes in this Scorecard Reuven Carlyle D 36 + A + + + + + 100% Of the thousands of bills voted on in the Washington Maralyn Chase D 32 + + + + + + + 100% House and Senate, we identified a few key votes Annette Cleveland D 49 + + + + + + + 100% that will have the greatest impact on Washington’s Steve Conway D 29 + + + + + + + 100% environment and public health. Short descriptions Jeannie Darneille D 27 + + + + + + + 100% of each bill can be found on the reverse and more Manka Dhingra D 45 + + + + + + + 100% details are available on our website. Doug Ericksen R 42 - - - + - + + 43% Joe Fain R 47 + + + + + + + 100% www.EnvironmentWashington.org -

Washington State 2015 Gas Tax Increase

Washington Senate Bill (2015) Title of Bill: Senate Bill 5987 Purpose: A $16 billion, 16-year transportation plan, which included an 11.9 cents-per-gallon gas tax increase—gradually implemented beginning Aug. 1, 2015, and fully applied on July 1, 2016—and an increase in transportation-related fees, including those for overweight vehicles. The bill also permits Sound Transit residents to vote on a plan to increase taxes for an additional $15 billion in order to expand the region’s light rail system. Status of Amendment: Passed Washington Senate Bill 5987 (2015) Signed into law: July 15, 2015 Senate House FOR 37 54 AGAINST 7 44 History State Gas Tax Before SB 5987, drivers in Washington state paid a flat excise tax on gasoline of 37.5 cents-per-gallon. That amount was last set in 2005, when the state legislature approved a 9.5 cents-per-gallon state gas tax increase (phased in over four years). The package, including an increase in vehicle weight fees, was estimated to raise $8.5 billion over a 16-year period. Previous gas tax increases were implemented in 2003, 1991, and 1990. Gas Tax Distribution & Transportation Funding Sources Washington state’s highway and ferry system is funded through a combination of motor vehicle fuel taxes (23%); vehicle licenses, permits, and fees (12%); federal funds (26%); bonding (23%), and other sources such as tolling, ferry fares, and local funding (16%).i The transportation budget pays for “maintaining, preserving, and improving the highway system; operating ferries; motor vehicle registration; and enforcing traffic laws on the state highway system.” ii The state’s gas tax of 37.5 cents-per-gallon was constitutionally dedicated for ‘highway purposes’ in the 18th Amendment (November 1944). -

General Election November3

VOTERS’ PAMPHLET Washington State Elections & Cowlitz County General Election November 3 2020 2020 Official Publication Ballots mailed to voters by October 16 (800) 448-4881 | sos.wa.gov 2 A message from Assistant Secretary of State Mark Neary On behalf of the Office of the Secretary of State, I am pleased to present the 2020 General Election Voters’ Pamphlet. We offer this comprehensive guide as a reference to help you find information on the candidates and statewide measures that appear on your ballot. This general election gives you the opportunity to have a say in our government at the local, state, and national levels, and to choose who will serve as our nation’s next president. In order to have your voice heard, you must be registered to vote. Voter registration forms that are mailed or completed online must be received by October 26, and we encourage you to check your registration information today at VoteWA.gov. If you are reading this message after October 26 and you are not registered, have moved since the last time you voted, or did not receive a ballot, you can go to your local elections office or voting center during regular business hours through 8 p.m. on Election Day to register to vote and receive a ballot. Once you have completed your ballot, you can send it via U.S. mail — no postage needed — but remember, all ballots must be postmarked by November 3. A late postmark could disqualify your ballot. The USPS recommends that you mail a week before Election Day. -

General Election November3

VOTERS’ PAMPHLET Washington State Elections & San Juan County General Election November 3 2020 2020 Official Publication Ballots mailed to voters by October 16 (800) 448-4881 | sos.wa.gov 2 A message from Assistant Secretary of State Mark Neary On behalf of the Office of the Secretary of State, I am pleased to present the 2020 General Election Voters’ Pamphlet. We offer this comprehensive guide as a reference to help you find information on the candidates and statewide measures that appear on your ballot. This general election gives you the opportunity to have a say in our government at the local, state, and national levels, and to choose who will serve as our nation’s next president. In order to have your voice heard, you must be registered to vote. Voter registration forms that are mailed or completed online must be received by October 26, and we encourage you to check your registration information today at VoteWA.gov. If you are reading this message after October 26 and you are not registered, have moved since the last time you voted, or did not receive a ballot, you can go to your local elections office or voting center during regular business hours through 8 p.m. on Election Day to register to vote and receive a ballot. Once you have completed your ballot, you can send it via U.S. mail — no postage needed — but remember, all ballots must be postmarked by November 3. A late postmark could disqualify your ballot. The USPS recommends that you mail a week before Election Day. -

We2.0 Washington Education Association Volume 50, Number 3 – Summer 2012

we2.0 Washington Education Association Volume 50, Number 3 – Summer 2012 2012 ELECTION A vote for our future “His first opportunity to get involved in politics started as a parent in the Selah School District to fight for education. … If you compare Jay Inslee to the other candidate who is running, he understands people. He understands fighting for and allowing us to preserve our collective bargaining rights. … Who’s going to be able to protect our bargaining rights and be able to allow us to fight for kids?” Kendell Millbauer Middle school social studies teacher Richland Summer 2012 1 am an optimist. I think I inherited my glass- Our compensation, up for discussion next half-full tendencies alongside the educator legislative session, is a good illustration of the geneI that runs in my family. And I have to say, it’s linkage between funding and policy. Back in 2009, come in handy lately. I’ve been working in public the Quality Education Council set the road map education for 42 years, and I’ve never experienced a for education policy and funding in motion. It From year quite like this — the pace has accelerated, the was reaffirmed by the Legislature in 2010, and the demands are high, the issues relentless. McCleary decision cites these steps as legislative intent regarding funding. Mary I know you feel it too. As I’ve been out visiting with councils Meaning money and reforms and members this fall, everyone ‘We care so much are linked, and how those play has been talking about Chicago, forward relies on the people we “Won’t Back Down,” the about this election elect. -

Independent Expenditures and Electioneering Communications

2008 Election Financing Fact Book Compiled by Washington State Public Disclosure Commission Olympia, Washington Suemary Trobaugh, Editor The Public Disclosure Commission’s office is located at: 711 Capitol Way, Room (206) Olympia WA 98504 (360) 753-1111 - Fax: (360) 753-1112 www.pdc.wa.gov FOREWORD The 2008 Election Financing Fact Book is the sixteenth in a series of comparable biennial reports produced since 1978 by the Washington Sate Public Disclosure Commission, pursuant to the Commission’s authority in RCW 42.17.370(3) to publish reports and statistics concerning campaign finance so that the information may be fully disclosed to the public. This Fact Book also depicts the political finance activity of the ninth regular legislative election held following the implementation of Initiative 134. Material in this book is based on campaign finance reports filed by candidates and political committees disclosing activity through January 12, 2009. For the most part, these reports have not been audited by PDC staff. Every effort has been made to assure that the data as well as the summary charts and graphs accurately reflect the filed information. The total expenditures by legislative candidates, who reported spending money, are summarized as follows: In 1994, 316 candidates spent $10,516,508 In 1996, 313 candidates spent $13,064,270 In 1998, 267 candidates spent $12,994,043 In 2000, 303 candidates spent $16,257,511 In 2002, 258 candidates spent $15,847,338 In 2004, 257 candidates spent $18,904,376 In 2006, 216 candidates spent $18,850,341 In 2008, 244 candidates spent $21,306,132 From 2004 to 2008 the average expenditure by major party general election legislative candidates with opposition increased approximately 4% from $97,124 to $100,915*. -

2011-2012 Legislative Scorecard

2011-2012 LEGISLATIVE SCORECARD 2011-2012 Legislative Scorecard | 1 DEAR SCORECARD READER Welcome to the 2011-2012 Washington Conservation Voters Scorecard, your trusted guide to environmental politics in Washington. The Scorecard tells the story of the Legislature’s record over the past two years, holding individual members accountable for their environmental votes. Unfortunately we can’t record the votes that didn’t happen. The past two years have largely been defensive, and we have had to work tirelessly to prevent rollbacks on our most basic environmental protections. WCV helped stop over 75 bad bills from receiving floor votes in 2012. The credit, however, goes to you: citizen activists who have demonstrated their strength in amaz- ing ways over the past two years, providing effective grassroots pressure at critical moments. We recognize that state budget shortfalls have placed pressure on environ- mental and natural resource programs, but the lack of progress on issues like Puget Sound restoration and climate change can also be attributed to a troubling lack of bipartisan strength on our issues. If we are ever to succeed on tackling some of our State’s hardest-to-solve problems, it will be because of a commitment to problem-solving on both sides of the political aisle. WCV is committed to ensuring that our shared environmental values are turned into legislative priorities. As a bipartisan organization, we will continue to build strong environmental leaders in both parties, working together to cre- ate a strong economy and healthy environment for our state. Together with Washington Environmental Council, our legislative partner, we will continue to collaborate with the 25 organizations in the Environmental Priorities Coalition to deliver achievements on the issues you care about. -

Voters' Pamphlet PERMIT NO

State of Washington & WhatcomCounty Name County Here Voters’ Pamphlet November 5, 2013 General Election Your ballot will arrive by October 22 (800) 448-4881 | www.vote.wa.gov PublishedPublished byby thethe OfficeOffice ofof thethe SecretarySecretary ofof StateState && theCounty Whatcom Name County Here Auditor 2 Introduction to the 2013 Voters’ Pamphlet Welcome! This pamphlet contains information about two initiatives to the Legislature and five tax advisory votes appearing on your ballot. You will also find several pages designed to assist you with voting and the election process. This election largely features local races and measures. Voters will determine the outcome of local measures and elect officials to serve on city councils, school boards, fire and port commissions. These are elections that have a significant impact on our local communities and ultimately shape our state. The cover of this pamphlet highlights our latest exhibit at the State Capitol celebrating Washington innovators who dared to dream big. Grand Coulee to Grunge: eight stories that changed the world, recounts feats in agriculture, business, science, and technology that put the Evergreen State on the world stage. As Washington expanded in the 1900s, so did our impact on the world. From cities that were built with Northwest timber to the development of a weapon that would end a world war, our state helped shape the 20th century. Today, people around the world celebrate Washington lives and legacies. From a Starbucks store in Malaysia to a 747 airplane in Antarctica, Washington is everywhere. The fruits of our labor appear on dinner tables across the world and the music of Hendrix and Nirvana is heard on radio stations from Sydney to Stockholm.