Dufry Finance

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Autogrill Group 2008 Sustainability Report

Autogrill Group 2008 Sustainability Report 2008 Sustainability Report Autogrill Group Contents Introduction 02 How to read the Sustainability Report 03 Results and objectives 06 Message of the CEO 07 The Autogrill Group 08 The Group’s development 010 Vision, Mission and Strategy 011 The concession business 012 Business sectors 017 The brands 018 The organization model Autogrill’s sustainability 020 The road to sustainability 022 The Code of Ethics 023 Afuture, a project and philosophy for a sustainable future 026 The Corporate Governance system 035 Clear policies towards stakeholders 036 SA8000 Ethical Certification 037 Awards and recognitions in 2008 037 Sustainability rating The economic dimension of sustainability 038 039 Highlights: main economic indicators 042 Sales by sector and channel 045 Autogrill on the financial markets 046 Shareholders 046 Economic value generated and distributed The social dimension of sustainability 048 051 Highlights: main social indicators 052 Human resources management and valorization 067 Consumer transparency 074 Partner relationships 079 Investing in the community The environmental dimension of sustainability 086 089 Highlights: main environmental indicators 090 Managing the relation with the environment 093 Impact of activities on the environment 100 Sales point innovation 103 Training and communication The GRI-G3 indicators 104 The Independent Auditors’ Report 111 Glossary 113 Contents The Autogrill Group Introduction Each year the Sustainability Report (hereinafter referred to as “Report”) attempts to provide its readers with a greater understanding of the complex relationships that make up the Auto- grill world. The significant growth over the past few years has transformed the Autogrill Group (referred to as “Autogrill,” “Company,” or “Group”) into a highly recognized organization, synony- mous not only with complete and quality products, but also with a style and a way of being for ever changing people, cultures and markets, making the most of each unique element. -

Stoxx® All Europe Total Market Index

TOTAL MARKET INDICES 1 STOXX® ALL EUROPE TOTAL MARKET INDEX Stated objective Key facts The STOXX Total Market (TMI) Indices cover 95% of the free-float » With 95% coverage of the free-float market cap of the relevant market cap of the relevant investable stock universe by region or investable stock universe per region, the index forms a unique country. The STOXX Global TMI serves as the basis for all regional benchmark for a truly global investment approach and country TMI indices. All TMI indices offer exposure to global equity markets with the broadest diversification within the STOXX equity universe in terms of regions, currencies and sectors. Descriptive statistics Index Market cap (USD bn.) Components (USD bn.) Component weight (%) Turnover (%) Full Free-float Mean Median Largest Smallest Largest Smallest Last 12 months STOXX All Europe Total Market Index 13,768.8 10,453.0 7.2 1.7 250.9 0.0 2.4 0.0 3.0 STOXX Global Total Market Index 54,569.6 44,271.7 6.1 1.3 618.0 0.0 1.4 0.0 3.4 Supersector weighting (top 10) Country weighting Risk and return figures1 Index returns Return (%) Annualized return (%) Last month YTD 1Y 3Y 5Y Last month YTD 1Y 3Y 5Y STOXX All Europe Total Market Index 0.3 2.0 18.1 43.3 55.0 3.8 3.0 17.7 12.4 8.9 STOXX Global Total Market Index 2.3 7.7 21.7 49.4 78.4 30.7 11.5 21.2 13.9 11.9 Index volatility and risk Annualized volatility (%) Annualized Sharpe ratio2 STOXX All Europe Total Market Index 11.0 11.2 11.6 19.9 21.1 -1.0 0.3 1.3 0.6 0.4 STOXX Global Total Market Index 8.2 7.9 8.1 12.8 22.5 1.1 1.4 2.3 1.0 0.5 Index to benchmark Correlation Tracking error (%) STOXX All Europe Total Market Index 0.9 0.9 0.9 0.9 0.9 5.8 6.1 6.3 10.0 10.2 Index to benchmark Beta Annualized information ratio STOXX All Europe Total Market Index 1.2 1.2 1.2 1.4 1.3 -3.5 -1.3 -0.6 -0.0 -0.2 1 For information on data calculation, please refer to STOXX calculation reference guide. -

14 Greek Fraport AG Airports

AVIATION PROJECT CASE STUDY 14 Greek Fraport AG Airports A leading player in the global airport business, more than 176 million passengers use airports where Fraport owns more than a 50% stake in. This includes 14 regional airports in Greece, from the Aktion National Airport to Zakynthos, that Fraport manages. As part of a major project to modernise these airports, Fraport asked for our help. The challenge • All 14 of the Greek airports Fraport manages had outdated lighting systems that weren’t compliant with the European Aviation Safety Agency (EASA) regulations. And this needed fixing – fast. • This meant new mast positions and heights for all 14 airports needed to be planned, taking into account: o OLS (Obstacle Limitation Surfaces) restrictions. o Wingtip clearance for various types of aircraft. o Keeping civil works needed for new cabling as low as possible. Find out more: midstreamlighting.com or call +44 (0) 207 584 8310 At a glance Sector: Aviation LED floodlights installed: 1,000 Customer: Fraport AG Type: Titan Series Number of airports: 14 Lux average values: 30 Lux Installation height: Variable: 12m to 40m Energy Savings: 55% on average Project date: 2018 Our solution Working with Intrakt, Fraport’s main contractor, we designed and delivered a completely new, compliant lighting system for each airport. Using our Titan 560 lighting, which was the perfect match between power and weight, meant: • Increased high colour rendering led to improved safety. • Shadow areas between planes were reduced through the new tower positioning. This guaranteed a better working environment for ground staff. • Energy use could be cut – by 55% on average. -

Breaking News

Breaking News Nuovi Covered Warrant di UniCredit quotati su SeDeX www.investimenti.unicredit.it Scopri la nuova emissione di UniCredit! Dal 16 Gennaio 2015, 516 nuovi Covered Warrant di UniCredit su Azioni italiane ed internazionali! Prezzi di mercato UniCredit amplia ulteriormente la propria I sottostanti italiani gamma di Covered Warrant con 424 nuovi A2A, Acea, Ansaldo, Atlantia, Autogrill, I Covered Warrant si possono acquistare e prodotti su azioni italiane e 92 nuovi prodotti Azimut, Banca popolare Emilia Romagna, vendere sul mercato SeDeX di Borsa Italiana, Banca Popolare di Milano, Banco Popolare, dove sono quotati dalle 9.00 alle 17.25. su azioni estere (europee ed americane) per Brunello Cucinelli, Buzzi Unicem, Campari Per monitorare il prezzo dei tuoi Covered Warrant mettere a disposizione dei Traders soluzioni a ,CNH Indistrial , Diasorin, Enel, Enel Green e Certificate e dei relativi sottostanti puoi Power, Eni, Erg, Exor, Ferragamo, Fiat-FCA, breve termine dotate di leva finanziaria consultare: aggiornate alle ultime condizioni di mercato Finmeccanica, Generali, Geox, Gtech, Hera, Intesa Sanpaolo, Luxottica, Mediaset, www.investimenti.unicredit.it molto volatili. Mediobanca, Mediolanum, Moncler, www.onemarkets.it L’emissione è focalizzata su 46 azioni italiane, Parmalat, Prismian, Saipem, Saras, Snam Numero Verde 800.01.11.22: per avere con scadenze trimestrali sul 2015, ma anche la rete gas, STM, Telecom Italia, Tenaris, un aggiornamento automatico delle Terna, Tod’s, UBI, Unipol Sai, World Duty nuova scadenza di Marzo 2016. I nuovi strike quotazioni e parlare con gli Specialisti del Free e Yoox. sono in linea con le attuali condizioni di Servizio Clienti mercato. 250 sono i Covered Warrant rialzisti I Sottostanti esteri Reuters alla pagina TRADINGLAB (Call) e 174 sono quelli ribassisti (Put). -

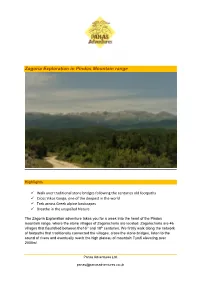

Zagoria Exploration in Pindos Mountain Range

Zagoria Exploration in Pindos Mountain range Highlights ✓ Walk over traditional stone bridges following the centuries old footpaths ✓ Cross Vikos Gorge, one of the deepest in the world ✓ Trek across Greek alpine landscapes ✓ Breathe in the unspoiled Nature The Zagoria Exploration adventure takes you for a week into the heart of the Pindos mountain range, where the stone villages of Zagorochoria are located. Zagorochoria are 46 villages that flourished between the16th and 18th centuries. We firstly walk along the network of footpaths that traditionally connected the villages, cross the stone bridges, listen to the sound of rivers and eventually reach the high plateau of mountain Tymfi elevating over 2000m! Panas Adventures Ltd. [email protected] Full Itinerary While we aim to follow the itinerary as it’s printed below, a degree of flexibility is necessary. This is in order to accommodate weather interference and unexpected opportunities! Day 1: Arrival Day Meet at Nikolas Guesthouse in Koukouli village. Zagorochoria are located high up in the mountains and we will have the chance to enjoy the tranquillity that nature can offer us away from the hustle and bustle. Today, we will check-in, settle down in our new surroundings and enjoy dinner all together! * A free of charge mini-bus group transfer may be provided, depending on the arrival times and locations of the group. Please, check the Transfer section that follows below. Day 2: Walk from Koukouli to Vitsa, Dilofo and Kipoi stone villages Today we explore the heart of Central Zagoria. We cross the valleys along the rivers, pass the stone bridges and walk the old footpaths which have connected the stone villages for many centuries. -

Annual Report 2017

ANNUAL REPORT 2017 FOCUS STORY MEMORABLE CUSTOMER SHOPPING EXPERIENCE WITH THE NEW GENERATION STORE: read the focus story on the digital strategy on page 30 – 35. 3 DUFRY GROUP – A LEADING GLOBAL TRAVEL RETAILER DUFRY AG (SIX: DUFN; BM&FBOVESPA: DAGB33) IS A LEADING GLOBAL TRAVEL RETAILER OPERATING OVER 2,200 DUTY-FREE AND DUTY-PAID SHOPS IN AIRPORTS, CRUISE LINES, SEAPORTS, RAILWAY STATIONS AND DOWNTOWN TOURIST AREAS. DUFRY EMPLOYS OVER 29,000 (FTE) PEOPLE. THE COMPANY, HEADQUARTERED IN BASEL, SWITZERLAND, OPERATES IN 64 COUNTRIES ON ALL FIVE CONTINENTS. ANNUAL REPORT 2017 CONTENT MANAGEMENT REPORT Dufry at a Glance 6 – 7 1 Highlights 2017 8 – 9 Message from the Chairman of the Board of Directors 10 – 13 Statement of the Chief Executive Officer 14 – 18 Organizational Structure 19 Board of Directors 20 – 21 Group Executive Committee 22 – 23 Dufry Investment Case 24 – 25 Dufry Strategy 26 – 79 Dufry Divisions 46 – 65 SUSTAINABILITY REPORT Sustainability 80 – 92 2 Community Engagement 93 – 98 FINANCIAL REPORT Report of the Chief Financial Officer 102– 105 3 Financial Statements 107 – 212 Consolidated Financial Statements 108 – 201 Financial Statements Dufry AG 202 – 211 GOVERNANCE REPORT Corporate Governance 213 – 236 4 Remuneration Report 237 – 250 Information for Investors and Media 252 – 253 Address Details of Headquarters 253 5 1 Management Report DUFRY ANNUAL REPORT 2017 DUFRY AT A GLANCE TURNOVER GROSS PROFIT IN MILLIONS OF CHF IN MILLIONS OF CHF MARGIN 8,800 5,000 8,400 4,900 71 % 4,800 70 % 7,800 4,500 69 % 7,200 4,200 68 % 6,600 -

Stock Options

STOCK OPTIONS ID UNDERLYING SHARE MULTIPLIER A2A A2A 5,000 ACE ACEA 500 STS ANSALDO STS (8) 500 ATL ATLANTIA 500 AGL AUTOGRILL (9) 500 AZM AZIMUT HOLDING (7) 500 BGN BANCA GENERALI 100 BMPS BANCA MONTE DEI PASCHI DI SIENA (1) 50 PMI BANCA POPOLARE DI MILANO (11) 5,000 BPE BANCA POPOLARE EMILIA ROMAGNA 1,000 BP BANCO POPOLARE (10) 100 BRE BREMBO 100 BC BRUNELLO CUCINELLI 100 BZU BUZZI UNICEM 100 CIR CIR 1,000 CNHI CNH INDUSTRIAL 500 DAN DANIELI & C. 100 CPR DAVIDE CAMPARI 1,000 DLG DE' LONGHI 500 DIA DIASORIN 500 ENEL ENEL 500 EGPW ENEL GREEN POWER 1,000 ENI ENI 500 ERG ERG 500 EXO EXOR 100 F FIAT (2) 500 FNC FINMECCANICA 500 G GENERALI 100 GEO GEOX 500 GTK GTECH 100 HER HERA 1,000 ISP INTESA SANPAOLO (ORDINARY SHARES) (3) 1,000 ISPR INTESA SANPAOLO (SAVING SHARES) 1,000 IRE IREN 1,000 IT ITALCEMENTI 100 LUX LUXOTTICA GROUP 500 MS MEDIASET 1,000 MB MEDIOBANCA 500 MED MEDIOLANUM 500 MONC MONCLER 500 MN MONDADORI 1,000 PLT PARMALAT 1,000 PC PIRELLI & C. 500 PRY PRYSMIAN 100 SFL SAFILO GROUP 100 SPM SAIPEM 500 SFER SALVATORE FERRAGAMO 500 SRS SARAS 1,000 SIS SIAS 500 SRG SNAM RETE GAS 1,000 STM STMICROELECRONICS (4) 500 TIT TELECOM ITALIA (ORDINARY SHARES) 1,000 TITR TELECOM ITALIA (SAVING SHARES) 1,000 TEN TENARIS 500 TRN TERNA 5,000 TOD TOD'S 100 UBI UBI BANCA 500 UCG UNICREDIT (5) 1,000 UNI UNIPOL (6) 500 US UNIPOL SAI 1,000 WDF WORLD DUTY FREE 500 YOOX YOOX 100 1 The series with a final "X" have an underlying of 50 Banca Monte dei Paschi di Siena shares The series with a final "Y" have an underlying of 10 Banca Monte dei Paschi di Siena -

Sailing Holidays

2019 CATALOGUE GREECE Sailing Holidays skipperarmatori.com SKIPPERARMATORI SKIPPERARMATORI SAILING HOLIDAYS GREECE If you love the sea, sailing, nights in a deserted bay under a starry sky, docking your boat in a small fisherman’s harbour, eating seafood in a nice local inn, making new friends without ever getting bored... If you love all of this, then jump aboard with us! 2019 Over the years, we’ve hosted lots of friends who now love, just like us or even more, the sea and sailing. It’s not necessary to have experience to go on a cruise. The crew will be able to help with the sailing, including steering! 1 Itinerary 2 Itinerary 3 Itinerary IONIAN ISLANDS SARONIC ISLANDS DODECANESE ISLANDS Lefkada - Ithaca Aegina - Poros Kos - Leros Kefalonia - Zante Spetses - Hydra - Dokos Patmos - Lipsi Boarding in Lefkada Boarding in Athens Boarding in Kos ITINERARY Shared yachts with cabin charter Price page 2-3-4 Departure date Return date per* person The freedom to book for one or more people Lefkada / Athens / Kos Lefkada / Athens / Kos BOATS as well as cabins, sharing your experience 1 June 8 June € 690 with other people. 8 June 15 June € 690 page 5 15 June 22 June € 690 Your vessel can navigate the waters in a 22 June 29 June € 690 flotilla with other boats. 29 June 6 July € 650 HOW TO ARRIVE The most entertaining and preferred way to 6 July 13 July € 690 page 6-7-8 travel amongst our guests. 13 July 20 July € 690 from 1 June to 14 September 2019 20 July 27 July € 690 Private yacht 27 July 3 August € 690 FAQs 3 August 10 August € 690 A yacht just for you and your friends or page 9 Saturday 10 August 17 August € 750 family with 3, 4 or 5 double cabins. -

Autogrill Acquires the Remaining 49.95% of Aldeasa from Altadis and Successfully Acquires 100% of World Duty Free Europe from BAA

The Group becomes the world’s leading provider in the airport retail market Autogrill acquires the remaining 49.95% of Aldeasa from Altadis and successfully acquires 100% of World Duty Free Europe from BAA • The Enterprise Value of the two transactions is €1,070 million, representing a multiple of 12.2x on the combined pro-forma 2007 Ebitda pre-synergies • The two transactions will be funded through fully committed new debt facilities • The integration of Aldeasa, WDF and Alpha Group will enable the Autogrill Group to achieve synergies of about €40 million a year by 2011 • The two acquisitions will be Earnings Neutral in 2008 and Accretive from 2009 (post-exceptional items and excluding the impact of amortization) Milan, 10 March 2008 – Autogrill (Milan: AGL IM) is pleased to announce the acquisition of the remaining 49.95%1 of Aldeasa S.A. from Altadis S.A., bringing its stake in Aldeasa to 99.90%, and the acquisition of 100% of World Duty Free Europe Limited from BAA Limited. These acquisitions follow on from the purchase of 49.95% of Aldeasa in 2005 and of Alpha Group Plc. in 2007. These landmark transactions are a major step in the growth path of Autogrill, from a single country food service provider to a global travel service provider for “people on the move”. Autogrill strengthens its presence in the fast growing travel retail market segment, maintaining its operational and strategic focus. Aldeasa and WDF, together with Alpha Group, will create the world’s leading provider in the airport retail market, with the largest platform in Europe and room for further development in other growing markets. -

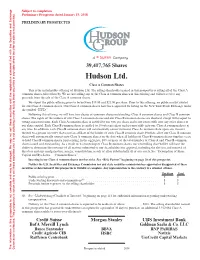

Hudson Ltd. Class a Common Shares This Is the Initial Public Offering of Hudson Ltd

Subject to completion Preliminary Prospectus dated January 19, 2018 PRELIMINARY PROSPECTUS 39,417,765 Shares Hudson Ltd. Class A Common Shares This is the initial public offering of Hudson Ltd. The selling shareholder named in this prospectus is selling all of the Class A common shares offered hereby. We are not selling any of the Class A common shares in this offering and will not receive any proceeds from the sale of the Class A common shares. We expect the public offering price to be between $19.00 and $21.00 per share. Prior to this offering, no public market existed for our Class A common shares. Our Class A common shares have been approved for listing on the New York Stock Exchange under the symbol “HUD.” Following this offering, we will have two classes of common shares outstanding: Class A common shares and Class B common shares. The rights of the holders of our Class A common shares and our Class B common shares are identical, except with respect to voting and conversion. Each Class A common share is entitled to one vote per share and is not convertible into any other shares of our share capital. Each Class B common share is entitled to 10 votes per share and is convertible into one Class A common share at any time. In addition, each Class B common share will automatically convert into one Class A common share upon any transfer thereof to a person or entity that is not an affiliate of the holder of such Class B common share. -

Lemanik Sicav

LEMANIK SICAV SocieÂteÂd'Investissement aÁCapital Variable Unaudited Semi-Annual Report as at November 30, 2014 R.C.S.: Luxembourg B 44.893 No subscription can be received on the basis of this annual report. Subscriptions are only valid if made on the basis of the current prospectus supplemented by the latest annual report, the Key Investor Information Document (KIID) and the most recent semi-annual report, if published thereafter. LEMANIK SICAV TABLE OF CONTENTS Page ORGANISATION....................................................................................................................................... 5 STATEMENT OF NET ASSETS ................................................................................................................. 9 STATEMENT OF OPERATIONS AND CHANGES IN NET ASSETS .............................................................. 18 STATISTICAL INFORMATION ................................................................................................................... 27 LEMANIK SICAV - ASIAN OPPORTUNITY ................................................................................................. 45 STATEMENT OF INVESTMENTS AND OTHER NET ASSETS.................................................................. 45 GEOGRAPHICAL CLASSIFICATION OF INVESTMENTS ......................................................................... 51 INDUSTRIAL CLASSIFICATION OF INVESTMENTS ................................................................................ 52 LEMANIK SICAV - ITALY......................................................................................................................... -

Contract Specifications for Futures Contracts and Eurex14e Options Contracts at Eurex Deutschland and Eurex Zürich As of 18.01.2016 Page 1

Contract Specifications for Futures Contracts and Eurex14e Options Contracts at Eurex Deutschland and Eurex Zürich As of 18.01.2016 Page 1 ***************************************************************************** AMENDMENTS ARE MARKED AS FOLLOWS: INSERTIONS ARE UNDERLINED DELETIONS ARE CROSSED OUT ***************************************************************************** […] Annex A in relation to subsection 1.6 of the Contract Specifications: Futures on Shares of Product Group ID* Cash Contract Minimum Currency ID Market-ID* Size Price ** Change […] 3i Group PLC IIIF GB01 XLON 1000 0.0001 GBX Admiral Group PLC FLNH GB01 XLON 1000 0,0001 GBX Altice N.V. ATCF NL01 XMAS 100 0.0001 EUR AT&T INC. DTVF US02 XNAS 100 0.0001 USD Azimut Holding S.p.A. HDBI IT01 XMIL 1000 0.0001 EUR Balda AG BADF DE01 XETR 100 0.0001 EUR Banca Monte dei Paschi di Siena MPIG IT01 XMIL 1000 0.0001 EUR S.p.A. Baxter International Inc. BAXF US01 XNYS 100 0.0001 USD BHP Billiton PLC-Basket BLTF GB01 XLON 1000 0.0001 GBX C.M.B. (Cie Maritime Belge) SA Actions MAIF BE01 XBRU 100 0,0001 EUR Nouvelles au Port.o.N. DMG MORI SEIKI AG GLDF DE01 XETR 100 0.0001 EUR EMC Corp. [Mass.] EMCF US01 XNYS 100 0.0001 USD Eurazeo RFXH FR01 XPAR 100 0.0001 EUR Google Inc. GOOF US02 XNAS 100 0.0001 USD GTECH S. p. A. N4GG IT01 XMIL 1000 0.0001 EUR Hermes International S.A. HMIH FR01 XPAR 100 0.0001 EUR Inditex (bar) IXDK ES01 XMAD 100 0.0001 EUR Inditex(bar) S.A. IXDL ES01 XMAD 100 0.0001 EUR International Game Technology IGTF US01 XNYS 100 0.0001 USD Interparfums S.A.