Review 6 Layout 1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Edrington-Annual-Report-2013.Pdf

New Frontiers Annual Report & Financial Statements for the year ended 31 March 2013 Annual Report and Financial Statements 2013 Financial Performance Contents Review Reports Financial Statements Group turnover Profit before tax* Shareholders’ earnings* Dividend per share 01 Financial Performance 20 Chairman’s Statement 42 Group Profit and Loss Account 03 New Frontiers 22 Chief Executive’s Review 43 Balance Sheets 13 £591.3m 13 £168.6m 13 £77.6m 13 34.0p 24 Financial Review 44 Group Cash Flow Statement 04 Innovation and Enterprise 26 Corporate Governance Statement 45 Other Statements 08 Emerging Markets 30 Corporate Social Responsibility Report 46 Accounting Policies 12 £556.1m 12 £148.8m 12 £70.5m 12 30.0p 12 Attracting Consumers 34 The Robertson Trust 49 Notes to the Financial Statements 16 Our Ambassadors 36 Directors and Advisers Edrington Locations 38 Directors’ Report 11 £553.4m 11 £141.5m 11 £65.0m 11 27.0p 40 Independent Auditors’ Report 10 £468.3m 10 £118.6m 10 £54.1m 10 23.2p WW6.3% 13.3% W10.1% W13.3% Increase in Group turnover Increase in profit before tax Increase in shareholders’ earnings Increase in dividends per share In the context of the Annual Report, the ‘Company’ refers collectively to The Edrington Group Limited, *excluding exceptional items *excluding exceptional items and its subsidiary and joint venture undertakings. Differentiation is made between Company and consolidated Group results in the financial statements and the related independent auditor’s report from page 40 onwards. 01 New Frontiers 2013 New Frontiers 2013 02 New Frontiers Edrington’s optimism about the Innovation and Enterprise future has driven an enterprising It lies at the heart of our business, from packaging technology, brand expressions spirit within the Company. -

Rhum Cocktail

RHUM COCKTAIL Delicate Fortifying ZEMIVARDIER THE RHUM JULEP Mount Gay XO, campari, Barbancourt 8, peach liqueur, sugar & sweet vermouth & bitters angostura bitters 18 18 RUM OLD FASHIONED RUM SOUR El Dorado 15, exotic syrup & bitters Angostura 1919, honey syrup, lemon juice, port wine 21 21 RUM MANHATTAN Plantation Grand Anejo, sweet vermouth, angostura & orange bitters 18 About Rum The origin of the word rum is unclear. The name may have derived from rumbullion, meaning “agreat tumult or uproar”. Some claim that the name is from the large drinking glasses used by Dutch seamen known as rummers. Other options include contractions of the words saccharum, latin for sugar, or arôme, French for aroma. In current usage, the name used for rum is often based on the rum’s place of origin. For rums from Spanish-speaking regions the word ron is used. A ron añejo indicates a rum that has been aged and is often used for premium products. Rhum is the term used for French-speaking regions, while rhum vieux is an aged French rum. Sugar cane, originally from Papua New Guinea, was taken to Asia, where it was cultivated and then carried to Africa, India and then Spain. European explorers were lured to the West Indies by legends of El Dorado, a city paved with gold. Ironically, the tall sweet grass that Columbus took to the Caribbean in 1493, and the sugar and rum made from that sugar cane, was ultimately worth more than all the lustrous metal taken from the Caribbean basin. According to some historians, the first molasses rum to be produced was from a Dutch emigrant named Pietr Blower in 1637. -

Ethics in Advertising and Marketing in the Dominican Republic: Interrogating Universal Principles of Truth, Human Dignity, and Corporate Social Responsibility

ETHICS IN ADVERTISING AND MARKETING IN THE DOMINICAN REPUBLIC: INTERROGATING UNIVERSAL PRINCIPLES OF TRUTH, HUMAN DIGNITY, AND CORPORATE SOCIAL RESPONSIBILITY BY SALVADOR RAYMUNDO VICTOR DISSERTATION Submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Communications in the Graduate College of the University of Illinois at Urbana-Champaign, 2012 Urbana, Illinois Doctoral Committee: Associate Professor William E. Berry, Chair and Director of Research Professor Clifford G. Christians Professor Norman K. Denzin Professor John C. Nerone ABSTRACT This research project has explored and critically examined the intersections between the use of concepts, principles and codes of ethics by advertising practitioners and marketing executives and the standards of practice for mass mediated and integrated marketing communications in the Dominican Republic. A qualitative inquiry approach was considered appropriate for answering the investigation queries. The extensive literature review of the historical media and advertising developments in the country, in conjunction with universal ethics theory, facilitated the structuring of the research questions which addressed the factors affecting the forces that shaped the advertising discourse; the predominant philosophy and moral standard ruling the advertising industry; the ethical guidelines followed by the practitioners; and the compliance with the universal principles of truth, human dignity and social responsibility. A multi- methods research strategy was utilized. In this qualitative inquiry, data were gathered and triangulated using participant observation and in-depth, semi- structured interviews, supplemented by the review of documents and archival records. Twenty industry leaders were interviewed individually in two cities of the country, Santo Domingo and Santiago. These sites account for 98% of the nation-states’ advertising industry. -

SUBMISSION from the EDRINGTON GROUP Key Facts at A

SUBMISSION FROM THE EDRINGTON GROUP Key facts at a glance • Scotland’s leading international premium spirits company • Key brands: The Famous Grouse; Cutty Sark; The Macallan; Highland Park; Brugal • Headquarters – Glasgow • Employs 839 people (Scotch whisky operations) • Turnover £291.5million • Products sold in over 100 countries 1. The name Edrington has long been synonymous with premium iconic Scotch whisky brands, market leaders in their field, which are valued and treasured by connoisseurs. 2. The Famous Grouse is the best selling whisky in Scotland and has held that distinction for the last 27 years. 3. The Macallan single malt is the world's "most precious whisky" while its stable- mate, Highland Park, has been named "best spirit in the world." 4. Cutty Sark was the first light coloured whisky of exceptional quality and today is a leading brand in southern Europe. 5. This illustrious collection of authentic brands has now been enhanced by Brugal, one of the largest international golden rum brands and the market leader in its home market, the Dominican Republic. In February 2008, Edrington acquired a majority shareholding in Brugal & Co., C. por A. 6. This agreement diversifies the Group's drinks portfolio beyond Scotch whisky for the first time and gives it access to one of the fastest growing spirit categories globally. It is also seen as a natural fit as the Group continues to develop its core brands through premiumisation, innovation and by targeting markets with stronger growth potential. 7. The origins of the Group, based in Glasgow and today one of Scotland's largest commercial companies, stretch back to the 1850's when W.A. -

LIBOR Transition - Legislative Solutions

LIBOR Transition - Legislative Solutions FIA Conference LIBOR: Where Are We and Where Are We Going? April 28-29, 2021 Authors Deborah North, Partner David Wakeling, Partner James Bryson Leland Smith Tough legacy proposals Overview of Proposed Legislative Measures Targeting “tough legacy” contracts Potential legislative solutions in UK and US, as well as published legislation in the EU and NY ‒ UK proposals remain moving targets ‒ NY solution is law; US federal solution likely ‒ UK goes to source ‒ US and EU change contract terms ‒ Mapping the differences ‒ Safe harbors Others? © Allen & Overy LLP | LIBOR Transition – Legislative Solutions 1 Tough legacy proposals Mapping Differences Based on Current Proposals EU (Regulation (EU) 2021/168 of the European Parliament and of the Council amending Regulation (EU) 2016/1011(EU BMR), Proposal US (NY) dated February10, 2021 (and effective from February 13, 2021) UK (Financial Services Bill) Scope USD LIBOR only. Potentially all LIBORs. Currently expected to be certain tenors of GBP, JPY, and All NY law contracts with no Contracts USD LIBOR (subject to further consultation). fallbacks or fallbacks to LIBOR- a) without fallbacks All contracts which reference the relevant LIBOR. FCA based rates (e.g. last quoted b) no suitable fallbacks (fallbacks deemed unsuitable if: (i) don't cover discretion to effect LIBOR methodology changes as it LIBOR/dealer polls). appears on screen page. Widest extra-territorial impact (but permanent cessation; (ii) their application requires further consent Fallbacks to a non-LIBOR from third parties that has been denied; or (iii) its application no may be trumped by the contractual fallbacks or the US/EU legislation to the extent of their territorial reach). -

The Whisky Sale

THE WHISKY SALE Wednesday 6 June 2018 Edinburgh THE WHISKY SALE | Edinburgh | Wednesday 6 June 2018 | Edinburgh Wednesday 24753 THE WHISKY SALE Wednesday 6 June 2018 at 11am 22 Queen Street, Edinburgh VIEWING ENQUIRIES CUSTOMER SERVICES IMPORTANT INFORMATION Tuesday 5 June Martin Green Monday to Friday 8.30am The United States Government 10am to 4pm +44 (0) 7775 842 626 to 6.00pm has banned the import of ivory Wednesday 6 June +44 (0) 131 225 2266 +44 (0) 20 7447 7447 into the USA. Lots containing 9am to 11am [email protected] Please see page 2 for bidder ivory are indicated by the information including after-sale symbol Ф printed beside the SALE NUMBER Press Enquiries: collection and shipment lot number in this catalogue. 24753 [email protected] +44 (0) 20 7468 5871 ILLUSTRATIONS CATALOGUE Front cover: Lots 52 Back cover: Lot 146 £10.00 Inside front cover: Lot 16 BIDS Inside back cover: Lot 75 +44 (0) 20 7447 7447 +44 (0) 20 7447 7401 fax [email protected] Please note that bids should be submitted no later than 4pm on the day prior to the sale. New bidders must also provide proof of identity when submitting bids. Failure to do this may result in your bid not being processed. Bidding by telephone will only be accepted on a lot with the lower estimate of £500. Live online bidding is available for this sale Please email [email protected] with ‘live bidding’ in the subject line 48 hours before the auction to register for this service Bonhams 1793 Limited Bonhams International Board Bonhams UK Ltd Directors Registered No. -

2019 Scotch Whisky

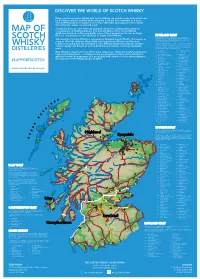

©2019 scotch whisky association DISCOVER THE WORLD OF SCOTCH WHISKY Many countries produce whisky, but Scotch Whisky can only be made in Scotland and by definition must be distilled and matured in Scotland for a minimum of 3 years. Scotch Whisky has been made for more than 500 years and uses just a few natural raw materials - water, cereals and yeast. Scotland is home to over 130 malt and grain distilleries, making it the greatest MAP OF concentration of whisky producers in the world. Many of the Scotch Whisky distilleries featured on this map bottle some of their production for sale as Single Malt (i.e. the product of one distillery) or Single Grain Whisky. HIGHLAND MALT The Highland region is geographically the largest Scotch Whisky SCOTCH producing region. The rugged landscape, changeable climate and, in The majority of Scotch Whisky is consumed as Blended Scotch Whisky. This means as some cases, coastal locations are reflected in the character of its many as 60 of the different Single Malt and Single Grain Whiskies are blended whiskies, which embrace wide variations. As a group, Highland whiskies are rounded, robust and dry in character together, ensuring that the individual Scotch Whiskies harmonise with one another with a hint of smokiness/peatiness. Those near the sea carry a salty WHISKY and the quality and flavour of each individual blend remains consistent down the tang; in the far north the whiskies are notably heathery and slightly spicy in character; while in the more sheltered east and middle of the DISTILLERIES years. region, the whiskies have a more fruity character. -

Cost of the Malts

Kingston Single Malt Society www.kingstonsinglemaltsociety.com A social club for the appreciation of Single Malt Whisky since 1998 JULY 27th, 2020 VOLUME 14; NUMBER 1c ---------------------------- COST OF THE MALTS GLENMORANGIE 18 YEAR OLD HIGHLAND SINGLE MALT SCOTCH WHISKY LCBO 398784 | 750 mL bottle Price $199.20 Spirits, Whisky/Whiskey 43.0% Alcohol/Vol. GLENMORANGIE SIGNET LCBO 327452 | 750 mL bottle Price: $336.20 Spirits, Scotch Whisky 46.0% Alcohol/Vol. NEW BEN NEVIS 10 YEARS OLD LCBO 432281 | 700 mL bottle Price: $85.00 Spirits, Whisky/Whiskey, Scotch Single Malts 46.0% Alcohol/Vol. OLD BEN NEVIS 10 YEARS OLD LCBO 432281 | 700 mL bottle Price: $85.00 Spirits, Whisky/Whiskey, Scotch Single Malts 46.5% Alcohol/Vol. DISTILLER’S ART BLAIR ATHOL 14 YEAR OLD Distilled: 2003; Bottled: 2018; Bottle # 076 of 397; LCBO 614783 | 700 mL bottle Spirits, Price: $173.85 Whisky/Whiskey 48.0% Alcohol/Vol. BUNNAHABHAIN 2003 AMONTILLADO CASK FINISH Distilled: 20/02/2003; Bottled: 26/02/2016; ---------------------------- LIMITED TO 1710 BOTTLES; VINTAGES 807462 | 700 mL bottle Price: $225.95 Spirits, Scotch Whisky 57.45% MENU Alcohol/Vol. 1st and 2nd and Welcome Nosing: ---------------------------- GLENMORANGIE 18 GLENMORANGIE SIGNET Upcoming Dinner Dates (introduced by: Dave Finucan) Upcoming Dinner Dates 1st Course: Grilled Corn & Bacon Gazpacho August 10th 2020 - Distell Tasting - with Crème Fraîche and Roasted Red Pepper Bunnahabhain / Tobermory / Ledaig - Mike Brisebois th th Friday August 28 2020 - 13 Annual Premium Night rd 3 Nosing: NEW BEN -

Das Land Des Whiskys Eine Einführung in Die Fünf Whisky-Regionen Schottlands Schottland

Das Land des Whiskys Eine Einführung in die fünf Whisky-Regionen Schottlands Schottland Highland Speyside Islay Lowland Campbeltown Whisky Die Kunst der Whisky- Keine gleicht der anderen – jede Brennerei wurde in Schottland Brennerei ist stolz auf ihre eigene über Jahrhunderte mit Liebe Geschichte, ihre einzigartige perfektioniert. Alles begann damit, Lage und ihre ganz eigene Art, dass regengetränkte Gerste den Whisky herzustellen, die mit frischem Wasser aus den sich im Laufe der Zeit entwickelt glasklaren schottischen Quellen, und verfeinert hat. Besuchen Sie Flüssen und Bächen in eine eine Brennerei und erfahren Sie trinkbare Spirituose verwandelt mehr über die Umgebung und die wurde. Menschen, die den Geschmack des schottischen Whiskys formen, Bis zum heutigen Tag setzen den Sie genießen. Wenn Sie Brennereien im ganzen Land sich am Ende der Brennerei- die Tradition fort und nutzen seit Führung zurücklehnen und Jahrhunderten pures Quellwasser bei einem Gläschen unseres aus den gleichen Quellen. größten Exportschlagers entspannen, halten Sie in Ihrem Vom Wasser und der Form des Glas gewissermaßen die Essenz Destillierapparats bis zum Holz Schottlands in der Hand. des Fasses, in dem der Whisky reift – es gibt viele Faktoren, Schottland ist weltweit das Land die den schottischen Whisky mit den meisten Brennereien und so besonders machen und lässt sich in fünf verschiedene die einzelnen Brennereien so Whisky-Regionen unterteilen: unterschiedlich. Islay, Speyside, Highland, Lowland und Campbeltown. Erfahren Sie mehr über Schottland: www.visitscotland.com/de Unterkünfte suchen und buchen: www.visitscotland.com/de-de/unterkunft/ 02 03 Islay Unter all den kleinen Inseln vor frischem Quellwasser und der Schottlands Westküste ist Islay von den einheimischen Bauern etwas ganz Besonderes. -

APAC IBOR Transition Benchmarking Study

R E P O R T APAC IBOR Transition Benchmarking Study. July 2020 Banking & Finance. 0 0 sia-partners.com 0 0 Content 6 • Executive summary 8 • Summary of APAC IBOR transitions 9 • APAC IBOR deep dives 10 Hong Kong 11 Singapore 13 Japan 15 Australia 16 New Zealand 17 Thailand 18 Philippines 19 Indonesia 20 Malaysia 21 South Korea 22 • Benchmarking study findings 23 • Planning the next 12 months 24 • How Sia Partners can help 0 0 Editorial team. Maximilien Bouchet Domitille Mozat Ernest Yuen Nikhilesh Pagrut Joyce Chan 0 0 Foreword. Financial benchmarks play a significant role in the global financial system. They are referenced in a multitude of financial contracts, from derivatives and securities to consumer and business loans. Many interest rate benchmarks such as the London Interbank Offered Rate (LIBOR) are calculated based on submissions from a panel of banks. However, since the global financial crisis in 2008, there was a notable decline in the liquidity of the unsecured money markets combined with incidents of benchmark manipulation. In July 2013, IOSCO Principles for Financial Benchmarks have been published to improve their robustness and integrity. One year later, the Financial Stability Board Official Sector Steering Group released a report titled “Reforming Major Interest Rate Benchmarks”, recommending relevant authorities and market participants to develop and adopt appropriate alternative reference rates (ARRs), including risk- free rates (RFRs). In July 2017, the UK Financial Conduct Authority (FCA), announced that by the end of 2021 the FCA would no longer compel panel banks to submit quotes for LIBOR. And in March 2020, in response to the Covid-19 outbreak, the FCA stressed that the assumption of an end of the LIBOR publication after 2021 has not changed. -

LIBOR Transition

JUNE 2021 LIBOR Transition AT A GLANCE WHAT IS LIBOR? Following guidance from the Financial Stability Board (FSB), regulatory led public/private working groups Interbank Offered Rates (IBORs), commonly referred were established to identify and promote adoption to as the London Interbank Offered Rate (LIBOR), are of robust alternate risk free rates (ARFRs) that were systemically important interest rate benchmarks, aimed based on substantial underlying transactions to at providing an indication of the average rates at which replace the various LIBOR currency rates. Most RFRs banks can obtain unsecured funding from each other were created as a response to the end of LIBOR; while in various currencies. Various regulatory authorities SONIA, which was historically referenced on overnight have announced their support for a reduced reliance on transactions, was reformed. IBORs, with cessation dates starting at the end of 2021, detailed in Figure 1. LIBOR has often been used in the industry as an interest rate benchmark rate for various LIBOR VERSUS RFR financial products ranging from capital markets to lending products including mortgages. LIBOR RFR In addition to LIBOR cessation, other benchmarks Term Term rate An overnight rate such as EONIA (Euro Overnight Index Average) will be benchmark e.g. (with no existing ceasing publication on 3 January 2022 and there are 3M, 6M, 1Y term structure)1 a number of other benchmarks that reference LIBOR in their calculations, which will be reformed, including View Forward-looking Backward-looking SOR (Singapore Dollar Offer Rate) and THBFIX (Thai Baht Fix). Secured? Unsecured Some based on a secured overnight rate, others WHAT ARE RISK FREE RATES (RFRS)? unsecured RFRs are interest rate benchmarks that seek to Credit Risk Embedded credit Near to risk free, measure the overnight cost of borrowing cash by risk component as there is no bank banks, underpinned by actual transactions. -

Speymalt – by Macallan Aged 14 Years

Spirit Single Malt Whisky Speymalt – by Macallan aged 14 years Country: Scotland Region: Craigellachie-Speyside Producer: Gordon and MacPhail Range: Speymalt Range Bottling: Gordon and Macphail Bottling Style: Single Malt Whisky Water Source: from Bore Holes Age: Distilled 2005 - Bottled 2019 Cask Type: Sherry Colour: Amber Flavour Profile: Fruity Allergens: not known Bottle size: 70cl - abv: 43.0% Speymalt Here we have Gordon & MacPhail's 2019 bottling of its wonderful Speymalt range! The Macallan single malt was distilled in 2005, and matured in sherry casks until 2019. Then, Gordon & MacPhail bottled it up at 43% ABV. Sherried Macallan is always a winner in my book. Speyside All Speyside whiskies are Highland whiskies; but, not all Highland malts are Speysiders. What is the difference, why the distinction of the Speyside region? The answer is quite simply the River Spey. From its source in the Cairngorms National Park, the river meanders 107 miles, disgorging into the Moray Firth at Spey Bay. Speyside, located in the middle of the Highland region, is also considered by many the heartland of Scotch production. Today, more than half of Scotland’s working distilleries are located in this region. Geographically, Speyside encompasses the area east and west of the River Spey, partly in tandem with the Morayshire county lines. There are several key towns in region. Forres, to the east, is home to Benromach Distillery and a short drive from Dallas Dhu, a mothballed distillery now transformed into a visitor destination. Westerly are the distilleries of Strathisla, Strathmill, Glen Keith, and Aultmore, all located in Keith. Centrally situated is Gordon and MacPhails, offices, and warehouses in the Royal Burgh of Elgin, also known for its mediaeval cathedral ruins.