Aequitas Estones Private Limited: [ICRA]BB- (Stable)/ [ICRA]A4 Assigned

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of SSP.Pdf

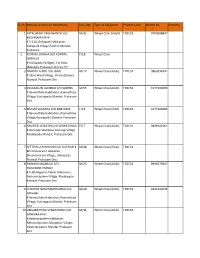

List of Self-Sealing Permission granted by the Commissioner of Customs (Preventive), Vijayawada [ From 01.01.2018 to 31.07.2018] Sl.N Names of Authorised Sigantories for SSP No. Date of Issue Name of Applicant Address of Applicant IEC GSTIN Address of Sealing Premises o. sealing allotted of SSP 1 2 3 4 5 6 7 8 9 1 Siri Smelters & Energy plot no. 262/B & 263/A, APIIC Growth Centre, Bobbili (i) Sajja Jyothsna Sree (ii) Sajja Venkateswara plot no. 262/B & 263/A, APIIC Growth 0912015829 37AAPCS2941A1ZE 90/2017 02.01.2018 Private Limited -535558 Rao Centre, Bobbili -535558 2 PLR Foods Private Sy. No. 354/1E, Ranganatha Mitta Village, Sodum 0911001352 37AAFCP9113P1ZU [1] P. Sudhir Reddy [2] P Indira Reddy Sy. No. 354/1E, Ranganatha Mitta Village, 02.01.2018 Limited Mandal & Post, Chittoor District - 517123, AP Sodum Mandal & Post, Chittoor District - 01/2018 517123, AP 3 Kalyan Aqua & Marine SY. No. 143, 144/1 to 3, Keerthipadu Village, 2604000857 37AADCK2221M1ZK [1] Putchakayala Seshadri Choudhary, SY. No. 143, 144/1 to 3, Keerthipadu 02.01.2018 Exports India (P) Ltd Maddipadu Mandal, Prakasam District - 523211, AP Director Village, Maddipadu Mandal, Prakasam 02.2018 District - 523211, AP 4 Chakri Fisheries Private SY. No. 143, 144/1 to 3, Keerthipadu Village, 2614000230 37AAFCC6232L1ZH [1] Putchakayala Sireesha, Director SY. No. 143, 144/1 to 3, Keerthipadu 02.01.2018 Limited Maddipadu Mandal, Prakasam District - 523211, AP Village, Maddipadu Mandal, Prakasam 03/2018 District - 523211, AP 5 Hind Granite Pvt. Ltd, Sy. No. 1024, 1028/4, Chimakurthy Village & Mandal, 0916502091 37AADCH8796E1Z4 [1] D. -

Stressed Asset Management Branch Flat No.104, 1Sr Floor H.No.6-3-639/640/642 Golden Edifice Complex Khairathabad

Stressed Asset Management Branch Flat No.104, 1sr Floor H.No.6-3-639/640/642 Golden Edifice Complex Khairathabad Hyderabad – 500 004 Tel: 040-23322157 E mail: [email protected] E –Auction sale notice under SARFAESI Act 2002 * Sale of immovable assets under the Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (hereinafter referred to as the Act). Notice is hereby given to the public in general and to the Borrower/s and Guarantor/s in particular that the under mentioned property mortgaged to Syndicate Bank, the possession of which had been taken by the Authorised Officer of the Bank under Section 13(4) of the Act will be sold by E- Auction as mentioned below for recovery of under mentioned dues and applicable interest, charges and costs etc as detailed below. The property described below is being sold on “AS IS WHERE IS, WHATEVER THERE IS AND WITHOUT RECOURSE BASIS” under the rule no. 8 & 9 of the Security Interest (Enforcement) Rules (hereinafter referred to as the rules) for the recovery of the dues detailed as under: Borrower: Guarantors/Mortgagors: M/s Sri Priyanka Raw and Boiled Rice Mill 1. Sri Pidaparthi Bala Bhaskar Reddy Plot No. 303, 304, 309 & 310 Plot No.303,304,309 & 310 APIIC Growth Centre, Gundlapalli APIIC Growth Centre, Gundlapalli Maddipadu Mandal, Prakasam District. Maddipadu Mandal, Prakasam District. And Rep. By Partners: Sri Pidaparthi Bala Bhaskar Reddy 1.Sri Pidaparthi Bala Bhaskar Reddy S/o Ramachandra Reddy S/o Ramachandra Reddy H.No.6-318 (C), Sri Saibaba Nagar H No 6-318(C), Sri Saibaba Nagar Kurnool Road Kurnool Road Ongole Ongole, Prakasam Dist Prakasam District Page 1 of 8 2.Smt Pidaparthi Pavani W/o Pidaparthi Bala Bhaskar Reddy 2. -

ADIP CAMP in PROCESS.Xlsx

Sl. NoName & Address of Beneficiary Sex/ Age Type of Appliance Product Code Mobile No Remarks 1PATKUMARI YWSHWANTH S/O M/32 Wheel Chair (Adult) TD2C51 9709308847 KRISHNAMURTHI # 1-114, Gollapudi Habitation, Gollapudi Village,Parchur Mandal, Prakasam 2 KOMMU SIRISHA D/O KOMMU F/18 Wheel Chair ISRAYELU # Enikapadu (Village), S.N Padu (Mandal), Prakasam District.A.P 3 DANDELLA ANIL S/O JAAN M /17 Wheel Chair(Adult) TD2C51 9866994341 # 32nd Ward Village, Chirala(Urban) Mandal, Prakasam Dist. 4 KOLAKALURI JAYARAO S/O SAMYEL M /55 Wheel Chair(Adult) TD2C51 9177404693 # Ravinuthala Habitation, Ravinuthala Village, Korisapadu Mandal, Prakasam Dist. 5 BEJJAM SUKANYA D/O BABYRANI F/15 Wheel Chair(Child) TD2C51 9177404693 # Ravinuthala Habitation, Ravinuthala Village,Korisapadu Mandal, Prakasam Dist. 6 RAVIPATI DORATHI D/O VENKATARAO F/17 Wheel C h a i r ( A dul t ) TD2C51 9849242261 # Annangi Habitation,Annangi Village Maddipadu Mandal, Prakasam Dist. 7SETTIPALLI RAGHAIAH S/O KOTAIAH # M/48 Wheel Chair(Adult) TD2C51 Bheemavaram Habitation, Bheemavaram Village, Ulavapadu Mandal, Prakasam Dist. 8PAINAM NAGARAJU S/O M/23 Wheel Chair(Adult) TD2C51 9949275947 HANUMANTHARAO # 5-58,Naganna Palem Habitation, Rachavaripalem Village, Maddipadu Mandal, Prakasam Dist. 9CHAPPIDI HANUMANTHARAO S/O M/40 Wheel Chair(Adult) TD2C51 9441442036 PAPAIAH # Ravinuthala Habitation, Ravinuthala Village, Korisapadu Mandal, Prakasam Dist. 10LINGABATHINA VENKATARAO S/O M/31 Wheel Chair(Adult) TD2C51 SANKARA RAO # Badevaripalem Habitation, Nekunampuram,Allaspokur Village, Valetivaripalem Mandal, Prakasam Dist. 11 RAVURI JAYANTH BABU S/O VEERAIAH M /56 Wheel C h a i r ( A dul t ) TD2C51 # 2-47, Pichikala Gudipadu Habitation, Pichikala Gudipadu Village, Korisapadu Mandal, Prakasam Dist. -

District Census Handbook, Prakasam, Part XII-A & B, Series-2

CENSUS OF INDIA 1991 SERIES 2 ANDHRA PRADESH DISTRICT CENSUS HANDBOOK PRAKASAM PARTS XII - A It B VILLAGE It TOWN DIRECTORY VILLAGE" TOWNWISE PRIMARY CENSUS ABSTRACT DIRECTORATE OF CENSUS OPERATIONS ANDHRA PRADESH PUBLISHED BY THE GOVERNMENT OF ANDHRA PRADESH 1995 iF 0 R EW 0 R D publication of the District Census Handbooks (DCHs) was initiated ,after the 1951 Census and is continuing since then with some innovations/modifications after each decennial Census. This is the most valuable district level publication brought out by the Census Organisation on behalf of each State Govt./ Uni~n Territory a~ministratio~. It Intc: al'ia. Provides data/information on some of the basIc demographiC and socia-economic characteristics and on the availability of certain important civic amenities/facilities in each village and town of the respective districts. This publication has thus proved to' be of immense utility to the planners., administrators, academicians and researchers. The scope of the DCH was initially confined to certain important census tables on population, economic and socio-cultural aspects as also the Primary Census Abstract (PCA) of each village and town (ward wise) of the district. The DCHs published after the 1961 Census contained a descriptive account of the district, administrative statistics, census tables and Village' and Town Directories including PCA. After the 1971 Census, two parts of the District Census Handbooks (Part-A comprising Village and Town Directories and Part-B comprising, Village and Town PCA) were released in all the States and Union Territories. The thnd Part (C) of the District Census Handbooks comprising administrative statistics and district census tables, which was also to be brought out, could not be published in many States/UTs due to considerable delay in compilation of relevant material. -

Lakshmi Industries

+91-8048372613 Lakshmi Industries https://www.indiamart.com/lakshmi-industries-ongole/ Lakshmi Industries was established in the year 1990. We are leading Manufacture & Supplier of Granite Cutting Machine, EOT Cranes etc. We have emerged as the remarkable manufacturer, and suppliers of EOT Cranes. Used for lifting structure steels ... About Us Lakshmi Industries was established in the year 1990. We are leading Manufacture & Supplier of Granite Cutting Machine, EOT Cranes etc. We have emerged as the remarkable manufacturer, and suppliers of EOT Cranes. Used for lifting structure steels in construction sites, the offered cranes are manufactured finest raw material and contemporary technology. These cranes are acknowledged for its reliable operations, durable finish standards. The offered cranes are developed by our industry experts following high definition engineering principles to ensure their adherence to the quality endorse of the industry. Each and every range is precisely engineered using quality tested raw materials as per the national as well as international quality standards. Our clients appreciate our product line for its load bearing capacity, application specific design and consistent performance. Our range finds its application in several industries. For more information, please visit https://www.indiamart.com/lakshmi-industries-ongole/aboutus.html GANTRY CRANE P r o d u c t s & S e r v i c e s Over Hanging Gantry Crane Semi Gantry Crane Heavy Duty Gantry Crane Gantry Crane EOT CRANE P r o d u c t s & S e r v i c e s Double -

Aequitas Exports Private Limited: Ratings Reaffirmed Rationale Key

July 23, 2021 Aequitas Exports Private Limited: Ratings reaffirmed Summary of rating action Previous Rated Amount Current Rated Amount Instrument* Rating Action (Rs. crore) (Rs. crore) Long Term - Fund Based TL 6.00 6.00 [ICRA]BB- (Stable); Reaffirmed Long Term - Fund Based/ CC 1.00 1.00 [ICRA]BB- (Stable); Reaffirmed Short Term - Fund Based 18.00 23.00 [ICRA]A4; Reaffirmed Short Term – Unallocated 5.00 0.00 - Total 30.00 30.00 *Instrument details are provided in Annexure-1 Rationale The ratings are constrained by Aequitas Exports Private Limited’s (AEPL) small scale of operations in the granite processing industry with revenues of Rs. 51.0 crore in FY2021. The ratings are also constrained by AEPL’s stretched liquidity position, as reflected by high utilisation of working capital limits owing to high inventory levels and sizeable advances extended to raw granite block suppliers. Further, AEPL has a moderate financial risk profile, characterised by a gearing of 1.7 times as on March 31, 2021, and an interest coverage of 2.2 times in FY2021. ICRA also notes the vulnerability of revenues to the macroeconomic factors like the performance of the housing real estate sector in export markets and the highly fragmented granite processing industry with intense competition, leading to moderate profit margins. The ratings, however, favourably factor in AEPL’s experienced management, with long track record of operations in the granite industry and easy availability of raw materials as the processing unit is located in proximity to granite quarries in the Ongole region, Andhra Pradesh. Key rating drivers and their description Credit strengths Experience of promoters in the granite processing industry – The promoters have more than a decade of experience in the granite processing and trading industry. -

ADIP CAMP in PROCESS.Xlsx

Sl. Name & Address of Beneficiary Sex/ Age Type of Appliance Product Code Mobile No Remarks No 1 KOLLIPALLA SRAVANA D/O KASIRAJU F / 12 B K A m pu t u t e +AFO RL OZ 02/01/02/02 9000019528 # Vodarevu Habitation, Epurupalem Size II Village, Chirala Mandal,Prakasam Dist 2ANNANGI SITA D/O ANNANGI PEDA F/13 Left AFO ANJAIAH Yarrabalem.Korisapadu(M), Madigapalli,Korisapadu Mandal, Prakasam 3 VALLEPU BRAHMAIAH S/O KOTAIAH M / 29 R i g h t AF O w it h Stick RL OZ 03/01 + Dhenuvakonda TD 1N 24 Habitation,Dhenuvakonda Village, Addanki Mandal, Prakasam Dist. 4ALLAM DHANALAKSHMI D/O F/28 Lt.KAFO RL OZ 07/02 8985057989 MADHAVA RAO # 35-132, Addanki (North) Habitation,Addanki Village, Addanki Mandal, Prakasam Dist. 5KANDA SURENDRA BABU S/O M/ 38 Lt.KAFO RL OZ 07/02 SIVAPRASAD # 2-89,Parchur Habitation, Parchur Village, Parchur Mandal, Prakasam Dist. -523169 6 ANISETTY VENUBABU S/O RAMAIAH M / 22 Bil . K AF O w it h RL OZ 07/01 07/02 9705437544 # Kunkalamarru Habitation, Bil.Elbow Crutches + Kunkalamarru Village, Karamchedu TD1N24-01 Mandal,Prakasam Dist. 7MUNNAM ANKIREDDY S/O M/27 Left KAFO with RL OZ 07/02 + 8790478403 EDUKONDALU Elbow Crutches TD1N24-02 # Kotha Kavurivaripalem Habitation, Gavinivaripalem Village, Chirala Mandal, Prakasam Dist. 8KOTHURI LAKSHMISUNITHA D/O M/27 Right KAFO with RL OZ /02/01 8341123711 SRINIVASARAO Axilliary Crutches +TD1N39-02 # 122-1, Parchur Habitation, Parchur Village, Parchur Mandal, Prakasam Dist. 9KUDUMULAPALLI VERANJAMMA D/O F/25 Right KAFO with RL OZ 07 -1-24 9912283009 VERANJAMMA Elbow Crutches # Mylavaram Habitation,Mylavaram Villlage, Addanki Mandal, Prakasam District. -

District Survey Report Prakasam District

DEPARTMENT OF MINES AND GEOLOGY Government of Andhra Pradesh DISTRICT SURVEY REPORT PRAKASAM DISTRICT Prepared by ISO 9001:2015 ANDHRA PRADESH SPACE APPLICATIONS CENTRE (APSAC) Planning Department, Govt. of Andhra Pradesh 2018 ACKNOWLEDGEMENTS APSAC wishes to place on record its sincere thanks to Sri B.Sreedhar IAS, Secre- tary to the Government (Mines) and the Director, Department of Mines and Geolo- gy, Govt. of Andhra Pradesh for entrusting the work for preparation of District Sur- vey Reports of Andhra Pradesh. The team gratefully acknowledge the help of the Commissioner, Horticulture Department, Govt of Andhra Pradesh and the Director, Directorate of Economics and Statistics, Planning Department, Govt. of Andhra Pradesh for providing valuable statistical data and literature. The Project team is also thankful to all Joint Directors, Deputy Directors, Assistant Directors and the staff of Mines and Geology Department for their overall support and guidance dur- ing the execution of this work. Also sincere thanks are due to the scientific staff of APSAC who has generated all the thematic maps. VICE CHAIRMAN APSAC Contents 1. Salient Features of Prakasam District ...................................................................................... 1 1.1 Administrative Setup ................................................................................................................ 1 1.2 Drainage ........................................................................................................................................ -

Hand Book of Statistics 2014 Prakasam District

HAND BOOK OF STATISTICS 2014 PRAKASAM DISTRICT CHIEF PLANNING OFFICER Prakasam District Ongole HAND BOOK OF STATISTICS 2014 PRAKASAM DISTRICT Compiled and Published by: CHIEF PLANNING OFFICER Prakasam District Ongole Smt. Sujata Sharma., I.A.S., Dated: .05.2012 Collector & Dist. Magistrate, PRAKASAM DISTRICT. P R E F A C E The “HAND BOOK OF STATISTICS” for the year 2014 presents factual information on the Socio Economic front in the various sectors of the District Economy. The new Hand Book of Statistics, 2014 is a part of series of publications made every year. Basic Data and Statistical information is prime requisite in building up strategic plans for the rapid Socio-Economic development at Macro and Micro levels. It is useful to General Public, Research Scholars, Bankers, Administrators and a host of others. I am extremely thankful to all the District Officers for their co-operation in furnishing the required data to bring out this publication. I appreciate the efforts made by Sri P.B.K.Murthy, Chief Planning Officer, Ongole and his staff members in bringing out this “Hand Book of Statistics” for the year 2014. Constructive suggestions for improvement of this publication and coverage of different Statistical Data would be appreciated. (Smt. Sujata Sharma) HAND BOOK OF STATISTICS - PRAKASAM DISTRICT - 2013-14 INDEX TABLE ITEM PAGE NO. NO. 1 SALIENT FEATURES OF PRAKASAM DISTRICT I - VI 2 COMPARISION OF DISTRICT WITH STATE FOR THE YEAR 2013-14 VII - XI 3 ADMINISTRATIVE DIVISIONS IN THE DISTRICT - 2013-14 XII - XIII 4 PUBLIC REPRESENTATIVES/ -

ADIP CAMP in PROCESS.Xlsx

Sl. No Name & Address of Beneficiary Sex/ Age Type of Appliance Product Code Mobile No Remarks 1BURLA RAAGAVEMDRARAAVU S/O M/10 TDOE15-02 9949107833 SANKARAO # Pittuvari Palem Habitation,Epurupalem Village, Chirala Mandal, Prakasam Dist. 2RAVIPATI RAMAMURTHY S/O M/65 08594-243342 NAGABHUSHANEM # 1-72 A, Thimaraju Palem Street- Colony, Parchur Village, Parchur Mandal, Prakasam Dist. 3GANDIKOTA GAYATRI D/O GANDIKOTA F/06 PEDA PAPAIAH # Pothukatla Street, Pothukatla Colony, Veeranna Palem Village, Parchur Mandal, Prakasam Mandal. 4ENAGANTI SAI AMEER S/O E. M/19 SUBHANSAHEB # 4-2-91/2, Srinivasa Nagar Colony, 1st Lane,Bapatla,Bapatla, Guntur, Prakasam 5JANKI REDDY S/O J.KOTI REDY, M/19 # Bapatla ,Ongole, Prakasam Dist. 6BUDDA NAVEEN KUMAR S/O VENKATA M/14 RAO # 1- 44/1, Pamidivaripalem Habitation, Pusuluru Village, Pedanandipadu Mandal, Guntur Dist. 7SAYAD SUBANI S/O SATTAR M/18 # 2nd Ward,2nd Ward, Ongole(Urban), Prakasam Dist. 8 S.SAIKRISHNA S/O S.PEDDA PANAIAH M/20 #Guntur, Bapatla, Ongole,Prakasam Dist. 9MUKKILU IMMANIYEL S/O SRINIVASA M/ 11 RAO # Duggirala Habitation, Duggirala Village, Duggirala Mandal,Guntur. 10P.GUNA RAO S/O VENKAT RAO M/19 # Bapatla 11MUNNAGI VAMSI KRISHNA S/O SIVA M/18 SUBRAMANYAM # 10-200 A, Munusuub Gari Veedhi, Old Mangalagiri,Mangalagiri, T.B Sanitorium,Guntur, Andhra Pradesh- 522503. 12 B.SANDYA RAO S/O B.KRISHNA RAO M/18 # Bapatla. 13 YADLAPALLI ANKAMMA S/O BRAHMAIAH M / 70 # 6-56, Pumidipadu Street-Colony, Pamidipadu Thanda,Pamidi Padu Village, Korisapadu Mandal, Prakasam Dist. 14AVULA GAJALIKSHMI W/O SURIBABU F/60 # 7-50, Pamidipadu Street, Pamidipadu Colony, Pamidipadu- Thanda- Village, Korisapadu Mandal, Prakasam Dist. -

Brief Note on Industry- Glocell Chemical Industries Pvt

Glocell Chemical Industries Pvt. Ltd. BRIEF NOTE ON INDUSTRY- GLOCELL CHEMICAL INDUSTRIES PVT. LTD. M/s. Glocell Chemical Industries Pvt. Ltd. Name and location details of the Plot No. 541, APIIC, Industrial Growth Centre, project Gundlapalli (V), Maddipadu Mandal, Prakasam District, Andhra Pradesh state – 523 211 Mr. K. Govinda Rajulu (Managing Director) th Address of project proponent for Reg. Office Address: Parisrama Bhavan, 6 Floor, 5- correspondence 9-58/B, Fatehmaidan Road, Hyderabad, Telangana – 500 004 Proposing manufacturing unit of Bulk Drugs & Drug Objective of the project Intermediates in the place of existing Carboxy Methyl Cellulose (CMC) unit. Details of the products Mentioned in below Table. manufactured (Quantity /month) Proposed capacity 60 MT/Month Status of Organization Government/Semi Government/ Industrial land Public/Private Project Cost (Rs.) 950 Lakhs (9.5 Crores) Total Labor Force During operation – 100 Nature of land APIIC, Industrial Growth Centre - Gundlapalli (IDA/Revenue/Others) Area Details 2.41 Acres (9750 Sq. m) The Proposed Project is within the APIIC, Industrial Location and land use details of Growth Centre - Gundlapalli. The total area of the unit the area with schematic plan is 2.41 Acres (9750 Sq. m). Water Bodies Gundlakamma Reservoir – 0.65 Km (SW) Naganna Palem Pond – 4.68 Km (ESE) Male Vagu – 4.8 Km (ESE) Kadiyallola Cheruvu – 5.28 Km (SE) Medarametla Lake - 5.16 Km (NE) Details of the water bodies and Nalla Vagu – 6.15 Km (ENE) Reserve Forests around the Sibbinolla Cheruvu – 6.26 Km (SE) proposed industry within 10 Km Thurpu Vagu – 7.0 Km (ENE) Radius (Arial Distance) Tank near Venkatapuram village – 7.29 Km (NNE) Dhenuvukonda Lake - 7.11 Km (WNW) Chilakaleru River – 8.83 Km (WNW) Nekunambad Cheruvu – 8.97 Lm (WSW) Reserved Forests None within 10 Km radius Nearest Town/City/Headquarters Maddipadu – 7.16 Km (SSE) along with distance National Highway NH-05 (Guntur – Chennai Nearest Roadway Highway) – 2.21 Km (East) Nearest habitation Annangi village – 0.83 Km (SSE) Prepared By Rightsource Industrial Solutions Pvt. -

Sl. No. Date District Venue Address Concerned ESIC BO 1 24-Feb

DETAILS OF VENUE OF HEALTH CHECKUP - CUM - AWARENESS CAMPS DURING THE ESIC SPL FORTNIGHT PERIOD (24-02-2020 TO 10-03-2020) IN THE STATE OF ANDHRA PRADESH Sl. Date District Venue Address Concerned ESIC BO No. REGIONAL OFFICE - VIJAYAWADA 1 24-Feb EAST GODAVARI COROMANDAL INDIA PVT LTD., BEACH ROAD, KAKINADA KAKINADA BABA'S PROFESSIONAL DETECTIVE & SECURITY SERVICES, 4-45/6, 2 25-Feb EAST GODAVARI KAKINADA Valasapakala, Vakalapudi 533005 OCEAN SPARKLE LTD., 2-1-66, 2ND FLOOR,VENKATAPAti ARCADE, 3 26-Feb EAST GODAVARI KAKINADA ANAND THEATRE COMPLEX, KAKINADA 533003 CYIENT LIMITED, Plot No:1,2,3,4&5A,APIIC IT SEZ,, Sarpavaram, 4 27-Feb EAST GODAVARI KAKINADA Kakinada Rural Mandal, 533001 5 28-Feb EAST GODAVARI International Paper Mill, APPM, Rajahmundry (1000) RAJAHUMUNDRY 6 29-Feb EAST GODAVARI Mandapeta Rice Millers Association Hall (500) RAJAHUMUNDRY 7 01-Mar EAST GODAVARI RAK Ceramics, Samarlakota (ADB Road) (500) KAKINADA Satya Sea Foods, Near Hope Hospital, Panasapadu, Samalkot Mandal 8 02-Mar EAST GODAVARI KAKINADA (500) 9 03-Mar EAST GODAVARI Parry Sugars Refinary Indai Pvt LTd., Beach Road, Kakinada (500) KAKINADA Glaxo Smithkline Consumer Health Care Ltd, Dowaleswaram, Rjy 10 04-Mar EAST GODAVARI RAJAHUMUNDRY (Horlicks Factory0(750) International Paper APPM Unit, Kadiyam, Madhavarayudupalem, 11 05-Mar EAST GODAVARI RAJAHUMUNDRY Kadiyam (500) 12 06-Mar EAST GODAVARI Coastal Acqua Private Limited, Patharlagadda (V), Karapa 9M (500) KAKINADA Nagarjuna Agro Chem Industries Ltd, Eathakota (V), Ravulapalem (M) 13 07-Mar EAST GODAVARI RAJAHUMUNDRY (500) Sri Ramadas Motor Transport Ltd., Near Sarpavaram Junction, 14 08-Mar EAST GODAVARI KAKINADA Kakinada (500) DETAILS OF VENUE OF HEALTH CHECKUP - CUM - AWARENESS CAMPS DURING THE ESIC SPL FORTNIGHT PERIOD (24-02-2020 TO 10-03-2020) IN THE STATE OF ANDHRA PRADESH Sl.