SHAD WHITE State Auditor

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

AUDIT EXCEPTIONS REPORT for Fiscal Year 2021 SHAD WHITE

AUDIT EXCEPTIONS REPORT For Fiscal Year 2021 SHAD WHITE State Auditor Larry Ware Director, Investigations Division Debi Cox Deputy Director, Investigations Division Office of the State Auditor Financial and Compliance Division Investigations Law Enforcement Division Performance Audit Division A legally mandated account of misappropriated or misspent public funds and the actions taken by the Office of the State Auditor for their recovery and their return to the appropriate entities in Fiscal Year 2021. AUDIT EXCEPTIONS REPORT FISCAL YEAR 2021 PUBLISHED IN ACCORDANCE WITH THE REQUIREMENTS OF SECTIONS 7-7-77, 7-7-79, 7-7-217 AND 7-7-219 MISSISSIPPI CODE ANNOTATED (1972) Shad White STATE AUDITOR The Office of the State Auditor does not discriminate on the basis of race, religion, national origin, sex, age or disability. OFFICE OF THE STATE AUDITOR Shad White AUDITOR July 29, 2021 Honorable Tate Reeves, Governor Honorable Delbert Hosemann, Lieutenant Governor Honorable David McRae, Treasurer Honorable Philip Gunn, Speaker of the House Honorable Dean Kirby, President Pro Tempore of the Senate Honorable Jason White, Speaker Pro Tempore of the House Members of the Mississippi State Legislature Dear Ladies and Gentlemen: As you are aware, it is my duty to report to you the specific exceptions taken by the Office of the State Auditor during Fiscal Year 2021, as required by Sections 7-7-77, 7-7-79, 7-7-217 and 7-7- 219, Mississippi Code Annotated (1972). This letter is a summary of the Special Report on Audit Exceptions for Fiscal Year 2021. The full report can be accessed on the internet at http://www.osa.ms.gov/documents/investigative/inv2021.pdf. -

Vaccinations Are Delayed for Army in Europe As Cases Rise

SPORTS: COVID aftershocks MUSIC are still being felt Page 48 Dua Lipa, nominated for 6 Grammys, is GAMES: Mario takes an icon in the making an exciting turn Page 18 Page 16 AP predictions, Page 15 BOOKS: How the US lost the Pech Valley Page 27 stripes.com Volume 79 Edition 233 ©SS 2021 FRIDAY,MARCH 12, 2021 $1.00 VIRUS OUTBREAK Vaccinations are delayed for Army in Europe as cases rise BY JENNIFER H. SVAN Stars and Stripes KAISERSLAUTERN, Germa- ny — The largest U.S. military hospital overseas might have to cancel coronavirus vaccinations as of next week, as supplies dwin- dle and new deliveries are de- layed, it said. Most appointments to get a fol- low-up shot at Landstuhl Regional Medical Center near Ramstein Air Base could be canceled start- ing Tuesday morning and patients will be “rescheduled as soon as we are resupplied,” LRMC said in a LESS post on its Facebook page Wednesday. New supplies of the vaccine might not arrive for several weeks, it said. Only second doses are available for now, LRMC said. The delay contrasts with com- LUSTER mands in the U.S., the Asia-Pacific region and the Middle East, sever- al of whom have recently received large vaccine shipments. PAOLO BOVO/U.S. Army The Landstuhl holdup could put U.S. Army paratroopers participate in an Eagle Sokol 21 exercise at Pocek Range in Postonja, Slovenia, on Tuesday. The Ronald Reagan some patients who have already Institute’s “National Defense Survey” showed declining trust in the military in the past three years. -

Shad White State Auditor

WAYNE COUNTY, MISSISSIPPI Audited Financial Statements and Special Reports For the Year Ended September 30, 2019 SHAD WHITE STATE AUDITOR Stephanie C. Palmertree, CPA Director, Financial & Compliance Audit Division Joe E. McKnight, CPA Director, County Audit Section A Report from the County Audit Section www.osa.state.ms.us The Office of the State Auditor does not discriminate on the basis of race, religion, national origin, sex, age or disability STATE OF MISSISSIPPI OFFICE OF THE STATE AUDITOR Shad White AUDITOR May 14, 2021 Members of the Board of Supervisors Wayne County, Mississippi Dear Board Members: I am pleased to submit to you the 2019 financial and compliance audit report for Wayne County. This audit was performed pursuant to Section 7-7-211(e), Mississippi Code Ann. (1972). The audit was performed in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States. I appreciate the cooperation and courtesy extended by the officials and employees of Wayne County throughout the audit. Thank you for working to move Mississippi forward by serving as a supervisor for Wayne County. If I or this office can be of any further assistance, please contact me or Joe McKnight of my staff at (601) 576-2674. Respectfully submitted, Shad White POST OFFICE BOX 956 • JACKSON, MISSISSIPPI 39205 • (601) 576-2800 • FAX (601) 576-2650 www.osa.ms.gov WAYNE COUNTY TABLE OF CONTENTS FINANCIAL SECTION .............................................................................................................................................................. 1 INDEPENDENT AUDITOR'S REPORT .................................................................................................................................... 3 FINANCIAL STATEMENTS .................................................................................................................................................... -

NEWTON COUNTY, MISSISSIPPI Audited Financial Statements and Special Reports for the Year Ended September 30, 2017

NEWTON COUNTY, MISSISSIPPI Audited Financial Statements and Special Reports For the Year Ended September 30, 2017 SHAD WHITE STATE AUDITOR Stephanie C. Palmertree, CPA Director, Financial & Compliance Audit Division Joe E. McKnight, CPA Director, County Audit Section A Report from the County Audit Section www.osa.state.ms.us The Office of the State Auditor does not discriminate on the basis of race, religion, national origin, sex, age or disability STATE OF MISSISSIPPI OFFICE OF THE STATE AUDITOR Shad White AUDITOR July 18, 2019 Members of the Board of Supervisors Newton County, Mississippi Dear Board Members: I am pleased to submit to you the 2017 financial and compliance audit report for Newton County. This audit was performed pursuant to Section 7-7-211(e), Mississippi Code Ann. (1972). The audit was performed in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States. I appreciate the cooperation and courtesy extended by the officials and employees of Newton County throughout the audit. Thank you for working to move Mississippi forward by serving as a supervisor for County. If I or this office can be of any further assistance, please contact me or Joe McKnight of my staff at (601) 576-2674. Respectfully submitted, Shad White POST OFFICE BOX 956 • JACKSON, MISSISSIPPI 39205 • (601) 576-2800 • FAX (601) 576-2650 www.osa.ms.gov NEWTON COUNTY TABLE OF CONTENTS FINANCIAL SECTION ............................................................................................................................................................ 1 INDEPENDENT AUDITOR’S REPORT ................................................................................................................................. 3 FINANCIAL STATEMENTS .................................................................................................................................................. -

TABLE 4.27 State Auditors: 2019

AUDITORS AND COMPTROLLERS TABLE 4.27 State Auditors: 2019 Legal Method Maximum State or other basis for of U.S. State consecutive jurisdiction State Agency Agency head Title office selection Term of office citizen resident terms allowed Department of Examiners of Alabama Rachel Riddle Chief Examiner S LC 7 yrs. « … None Public Accounts Alaska Division of Legislative Audit Kris Curtis Legislative Auditor C, S L (a) … … None Arizona Office of the Auditor General Lindsey Perry Auditor General S LC 5 yrs. … … None Arkansas Division of Legislative Audit Roger A. Norman Legislative Auditor S LC Indefinite « « None California Bureau of State Audits Elaine M. Howle State Auditor S G 4 yrs. « … None Colorado Office of the State Auditor Dianne E. Ray State Auditor C,S LC 5 yrs. … … None Office of the Auditors of John C. Geragosian and Connecticut State Auditors S L 4 yrs. … … None Public Accounts Robert Kane Office of the Auditor Delaware Kathleen McGuiness Auditor of Accounts C, S E 4 yrs. « « None of Accounts Florida Office of the Auditor General Sherrill F. Norman Auditor General C, S L (a) … … None Department of Audits Georgia Greg S. Griffin State Auditor S L Indefinite … … None and Accounts Hawaii Office of the Auditor Les Kondo State Auditor C L 8 yrs. … « None Legislative Services Office— Idaho April J. Renfro Division Manager S LC (b) … … None Legislative Audits Illinois Office of the Auditor General Frank Mautino Auditor General C, S L 10 yrs. … … None Indiana State Board of Accounts Paul D. Joyce State Examiner S GLC 4 yrs. … … None Iowa Office of the Auditor of State Rob Sand Auditor of State C, S E 4 yrs. -

Just Like He Arrived

www.mississippilink.com VOL. 26, NO. 17 FEBRUARY 13 - 19, 2020 50¢ Connecting the dots: Players in massive IHL Board of Trustees welfare embezzlement case got millions names Thomas Hudson as JSU’s acting president from taxpayers, but helped few Jackson State University The Board of Trustees of State Institutions of Higher Learning named Thomas Hudson as Act- ing President of Jackson State University at its meeting held Monday in Jackson, effective immediately. Hudson currently serves as special assistant to the president and chief diversity of- fi cer at Jackson State. Davis Smith New New McGrew Dibiase As special assistant to the president and chief diversity of- fi cer, Hudson has served on the By Anna Wolfe Hudson expenditures show. states broad discretion to spend that barely acknowledged peo- executive cabinet and provided Mississippi Today “Our main goal is getting the money – about $130 million ple walking by asking for help,” guidance to senior leadership on As chief operating offi cer, A downtown Jackson re- them off TANF,” Will Lamkin, a year in Mississippi. said state Rep. Chris Bell, D- all topics related to the univer- Hudson implemented cost- source center funded by mil- operation coordinator for the In 2018, the state used just 5.4 Jackson. sity’s future. saving measures that resulted lions of state welfare dollars was center, said Wednesday morn- percent of the money on cash as- By the end of fi scal year 2018, “We are extremely pleased in a 10 percent decrease in the quiet Wednesday morning. Blue ing, referring to the Temporary sistance – historically known as Human Services had paid Mis- that Thomas Hudson has agreed university’s operational budget, bins labeled “fresh produce” in a Assistance for Needy Families welfare – for poor families. -

Committee's Report

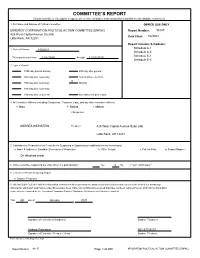

COMMITTEE’S REPORT (filed by committees that support or oppose one or more candidates and/or propositions and that are not candidate committees) 1. Full Name and Address of Political Committee OFFICE USE ONLY ENTERGY CORPORATION POLITICAL ACTION COMMITTEE (ENPAC) Report Number: 94147 425 West Capitol Avenue Ste24B Date Filed: 1/8/2021 Little Rock, AR 72201 Report Includes Schedules: Schedule A-1 2. Date of Primary 1/8/2021 Schedule A-3 Schedule E-1 This report covers from 12/1/2020 through 12/31/2020 Schedule E-3 3. Type of Report: 180th day prior to primary 40th day after general 90th day prior to primary Annual (future election) X 30th day prior to primary Monthly 10th day prior to primary 10th day prior to general Amendment to prior report 4. All Committee Officers (including Chairperson, Treasurer, if any, and any other committee officers) a. Name b. Position c. Address Chairperson , ANDREA WEINSTEIN Treasurer 425 West Capitol Avenue Suite 24B Little Rock, AR 72201 5. Candidates or Propositions the Committee is Supporting or Opposing (use additional sheets if necessary) a. Name & Address of Candidate/Description of Proposition b. Office Sought c. Political Party d. Support/Oppose On attached sheet 6. Is the Committee supporting the entire ticket of a political party? Yes X No If “yes”, which party? 7. a. Name of Person Preparing Report b. Daytime Telephone 8. WE HEREBY CERTIFY that the information contained in this report and the attached schedules is true and correct to the best of our knowledge , information and belief, and that no expenditures have been made nor contributions received that have not been reported herein, and that no information required to be reported by the Louisiana Campaign Finance Disclosure Act has been deliberately omitted . -

2019 Mississippi Legislative Guide

2019 MISSISSIPPI LEGISLATIVE GUIDE GOVERNOR :: PUBLIC SERVICE COMMISSIONERS Phil Bryant P.O. Box 1174, Jackson, MS 39215 601-359-3150; FAX: 601-359-3741 FIRST DISTRICT (CENTRAL) [email protected] Cecil Brown P.O. Box 139, Jackson, MS 39205 601-961-5430 SECOND DISTRICT (SOUTHERN) Sam Britton LIEUTENANT GOVERNOR 601-961-5400 Tate Reeves THIRD DISTRICT (NORTHERN) 601-359-3200; FAX: 601-359-4054 Brandon Presley [email protected] 601-961-5450 P.O. Box 1018, Jackson, MS 39215 :: TRANSPORTATION COMMISSION 601-359-7000 401 North West St., Jackson, MS 39215 CENTRAL TRANSPORTATION COMMISSIONER SECRETARY OF STATE Dick Hall Delbert Hosemann 601-359-7035 601-359-1350; FAX: 601-359-1499 SOUTHERN TRANSPORTATION COMMISSIONER [email protected] Tom King 401 Mississippi St., Jackson, MS 39201 601-583-0859 NORTHERN TRANSPORTATION COMMISSIONER Mike Tagert ATTORNEY GENERAL 662-680-3323 Jim Hood :: STATE GAMING COMMISSION 601-359-3680; FAX: 601-359-3441 Allen Godfrey, Exec. Director [email protected] 601-576-3800 550 High St., Ste.1200, Jackson, MS 39201 [email protected] P.O. Box 23577, Jackson, MS 39225-3577 :: STATE DEPARTMENT OF REVENUE STATE TREASURER Herb Frierson, Commissioner Lynn Fitch 601-923-7700 601-359-3600; FAX: 601-359-2001 P.O. Box 1033, Jackson, MS 39215 [email protected] :: DEPARTMENT OF CORRECTIONS P.O. Box 138, Jackson, MS 39205 Pelicia Hall, Commissioner 601-359-5600 633 N. State St., Jackson, MS 39202 STATE AUDITOR :: DEPARTMENT OF EDUCATION Shad White Carey M. Wright, State Superintendent of Education 601-576-2800; FAX 601-576-2687 601-359-3513 [email protected] P.O. -

Shad White State Auditor

JACKSON COUNTY, MISSISSIPPI Audited Financial Statements and Special Reports For the Year Ended September 30, 2019 SHAD WHITE STATE AUDITOR Stephanie C. Palmertree, CPA Director, Financial and Compliance Audit Division Joe E. McKnight, CPA Director, County Audit Section A Report from the County Audit Section www.osa.state.ms.us The Office of the State Auditor does not discriminate on the basis of race, religion, national origin, sex, age or disability. STATE OF MISSISSIPPI OFFICE OF THE STATE AUDITOR Shad White AUDITOR September 3, 2020 Members of the Board of Supervisors Jackson County, Mississippi Dear Board Members: I am pleased to submit to you the 2019 financial and compliance audit report for Jackson County. This audit was performed pursuant to Section 7-7-211(e), Mississippi Code Ann. (1972). The audit was performed in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States. I appreciate the cooperation and courtesy extended by the officials and employees of Jackson County throughout the audit. Thank you for working to move Mississippi forward by serving as a supervisor for Jackson County. If I or this office can be of any further assistance, please contact me or Joe McKnight of my staff at (601) 576-2674. Respectfully submitted, Shad White POST OFFICE BOX 956 • JACKSON, MISSISSIPPI 39205 • (601) 576-2800 • FAX (601) 576-2650 www.osa.ms.gov JACKSON COUNTY TABLE OF CONTENTS FINANCIAL SECTION .............................................................................................................................................................. 1 INDEPENDENT AUDITOR'S REPORT .................................................................................................................................... 3 FINANCIAL STATEMENTS .................................................................................................................................................... -

2018 Election Analysis

2018 ELECTION ANALYSIS NOVEMBER 7, 2018 CORNERSTONE 2018 ELECTION ANALYSIS Table of Contents I. Overview 2 II. House 4 III. Senate 7 IV. Governors Races 10 V. Issue Areas 13 a. Agriculture 14 b. Appropriations 17 c. Cybersecurity 21 d. Defense 24 e. Education 27 f. Energy & Environment 29 g. Health 32 h. Homeland Security 35 i. International 37 j. Tax 39 k. Tech & Telecom 42 l. Trade 44 m. Transportation 47 VI. View from the States 50 a. Georgia 51 b. Illinois 53 c. Iowa 55 d. Louisiana 57 e. Maryland 59 f. Mississippi 61 g. Texas 63 VII. Appendix 65 a. House Election Results 66 b. Senate Election Results 70 c. Incoming & Outgoing Member List 72 d. CBO Budget Projections Chart 75 e. Key Trends 76 Disclaimer Cornerstone Government Affairs has assembled the following report to assist our clients in providing results from the 2018 midterm election and understanding the implication of those results. We are aware that some information in this report may quickly become dated, and this may have an effect on the validity of some of our forecasts. We offer this report to our clients and friends as our best effort to assist you in evaluating the challenges and opportunities ahead. This report will be updated periodically. November 7, 2018 (Version 1, 4:00 p.m. ET) 1 CORNERSTONE 2018 ELECTION ANALYSIS Overview Voters delivered a split verdict in a highly contested and contentious election. This was the first midterm election since 1982 in which the President’s party gained seats in one body of Congress while losing seats in the other. -

Neshoba County Fair COVID Testing Line Set up Here

SPORTS COOK OF THE WEEK LADY REBELS SPLIT GAMES WILSON HAS PASSION IN TOURNAMENT AT ECCC FOR BAKING CAKES Softball action — Page 5B Shandra Wilson— Page 1B Established 1881 — Oldest Business Institution in Neshoba County Philadelphia, Mississippi Wednesday, August 4, 2021 140th Year No. 31 **$1.00 PANDEMIC Millions in relief monies flowing here By SCOTT HAWKINS rescue plan approved earlier So far, Neshoba County has Things of that nature.” Philadelphia Mayor James about broadband, and we are [email protected] this year, but spending plans received $2,827,915 and That is just a starting point, A. Young said the city has trying to figure out how we can have not been finalized. Philadelphia has received however. Mayo said the Board received its first payment but tap some of those funds to Some of Philadelphia’s $1.6 Neshoba County is receiv- $870,046. Both will receive the of Supervisors has not yet put has not yet put any plan in enhance what we need in the million in federal COVID relief ing a total of $5.6 million and remaining monies next year. anything in stone. action for spending. city,” Young said of the federal monies the city has already Philadelphia $1.6 million both Neshoba County Adminis- “There have been requests, “We are working on a plan guidelines. received could go toward sewer in two payments. trator Jeff Mayo said officials but you still have the issue of to enhance sewer and waster “Right now, we are just in improvements and broadband The Mississippi Band of are still determining how to compliance with the federal law water and some other sewer the planning stages. -

Shad White State Auditor

NESHOBA COUNTY, MISSISSIPPI Audited Financial Statements and Special Reports For the Year Ended September 30, 2019 SHAD WHITE STATE AUDITOR Stephanie C. Palmertree, CPA Director, Financial and Compliance Audit Division Joe E. McKnight, CPA Director, County Audit Section A Report from the County Audit Section www.osa.state.ms.us The Office of the State Auditor does not discriminate on the basis of race, religion, national origin, sex, age or disability. STATE OF MISSISSIPPI OFFICE OF THE STATE AUDITOR Shad White AUDITOR November 16, 2020 Members of the Board of Supervisors Neshoba County, Mississippi Dear Board Members: I am pleased to submit to you the 2019 financial and compliance audit report for Neshoba County. This audit was performed pursuant to Section 7-7-211(e), Mississippi Code Ann. (1972). The audit was performed in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States. I appreciate the cooperation and courtesy extended by the officials and employees of Neshoba County throughout the audit. Thank you for working to move Mississippi forward by serving as a supervisor for Neshoba County. If I or this office can be of any further assistance, please contact me or Joe McKnight of my staff at (601) 576-2674. Respectfully submitted, Shad White POST OFFICE BOX 956 • JACKSON, MISSISSIPPI 39205 • (601) 576-2800 • FAX (601) 576-2650 www.osa.ms.gov NESHOBA COUNTY TABLE OF CONTENTS FINANCIAL SECTION .............................................................................................................................................................. 1 INDEPENDENT AUDITOR'S REPORT .................................................................................................................................... 3 FINANCIAL STATEMENTS ....................................................................................................................................................