Why Is Wechat Pay So Popular?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Chinese Online Payment Platforms for Their Individual Needs

SNAPSHOT GUIDE TO ONLINE PAYMENT PLATFORMS FOR CHINESE VISITORS JULY 2017 OVERVIEW The use of online payment platforms has reshaped the way people pay for goods and services in China. Over the past five years, financial transactions are increasingly being handled through the use of advanced technology in a smartphone device, creating a fast and easy way for customers to pay for goods and services. While there are over 700 million registered users of online payment platforms in China – who complete approximately 380 million transactions a day – use of these platforms in Australia is relatively limited. In the year ending March 2017, 1.2 million Chinese visited Australia (up 12% from the previous year). Chinese visitors to Australia are the highest spending ($9.2 billion in 2016, or around $8,000 per visitor). Integrating online payment platforms recognised by Chinese visitors into business operations provides Australian businesses significant revenue yield opportunities and options better aligned to customer expectations. ONLINE PAYMENT PLATFORMS Also known as a digital wallet or e-wallet, these platforms are linked to a bank account, where transactions are processed without the use of a bank card i.e. similar to the way PayPal works. Online payment platforms can be used for purchases online or in-person. How an online payment platform works: Using a payment platform app, the customer generates a one- time QR code on their smartphone. The merchant uses a small device to scan the QR code given by the customer to process payment for the purchase of goods or services. In Australia, funds are in the merchant’s account within two business days after the date of transaction. -

Is China's New Payment System the Future?

THE BROOKINGS INSTITUTION | JUNE 2019 Is China’s new payment system the future? Aaron Klein BROOKINGS INSTITUTION ECONOMIC STUDIES AT BROOKINGS Contents About the Author ......................................................................................................................3 Statement of Independence .....................................................................................................3 Acknowledgements ...................................................................................................................3 Executive Summary ................................................................................................................. 4 Introduction .............................................................................................................................. 5 Understanding the Chinese System: Starting Points ............................................................ 6 Figure 1: QR Codes as means of payment in China ................................................. 7 China’s Transformation .......................................................................................................... 8 How Alipay and WeChat Pay work ..................................................................................... 9 Figure 2: QR codes being used as payment methods ............................................. 9 The parking garage metaphor ............................................................................................ 10 How to Fund a Chinese Digital Wallet .......................................................................... -

Mobile Wallet Guide

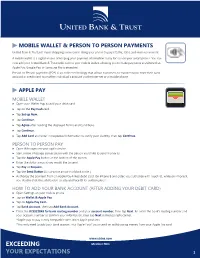

MOBILE WALLET & PERSON TO PERSON PAYMENTS United Bank & Trust just made shopping even easier! Using your phone to pay is faster, safer, and more convenient. A mobile wallet is a digital means of keeping your payment information ready for use on your smart-phone. You can now add your United Bank & Trust debit card to your mobile wallet, allowing you to make payments anywhere that Apple Pay, Google Pay, or Samsung Pay is accepted. Person-to-Person payments (P2P) is an online technology that allows customers to transfer funds from their bank account or credit card to another individual’s account via the Internet or a mobile phone. APPLE PAY MOBILE WALLET ▶ Open your Wallet App to add your debit card. ▶ Tap on the Pay Cash card. ▶ Tap Set up Now. ▶ Tap Continue. ▶ Tap Agree after reading the displayed Terms and Conditions. ▶ Tap Continue. ▶ Tap Add Card and enter in requested information to verify your identity, then tapContinue. PERSON TO PERSON PAY ▶ Open iMessages on your apple device. ▶ Start a new iMessage conversation with the person you’d like to send money to. ▶ Tap the Apple Pay button at the bottom of the screen. ▶ Enter the dollar amount you would like to send. ▶ Tap Pay or Request. ▶ Tap the Send Button (it is a white arrow in a black circle.) ▶ Authorize the payment from an Apple Pay-linked debit card. On iPhone 8 and older, you authorize with Touch ID, while on iPhone X, you double-click the side button to activate Face ID for authorization. HOW TO ADD YOUR BANK ACCOUNT (AFTER ADDING YOUR DEBIT CARD) ▶ Open Settings on your mobile phone. -

India's Open Payments Competition Can Spread

India’s open payments competition can spread to other markets By Eric Grover PaymentsSource October 3, 2017 India promises to be an epic payments battleground between traditional payment systems and tech giants, and perhaps a harbinger for emerging markets in general. Traditional retail payment systems such as Mastercard and Visa enjoy powerful network effects and market position in Europe and North America. But they were restricted in China, mobile commerce phenoms Alipay and WeChat Pay, and card network monopoly China UnionPay sewed up the market. The world’s largest in-play payments market India, however, is a wide open creative and competitive ferment, with Indian consumers and merchants the ultimate winners. With backing from Ant Financial, Paytm is just one of many well-heeled competitors battling in India's wide open payments market. Card networks including national champion RuPay, U.S. tech titans, Chinese fintech powers, MNOs, and an etailer are among the major players in India. MasterCard and Visa bring the power of their global networks tailored to the subcontinent to bear. Unlike in the U.S., they face formidable and nontraditional competitors on near equal footing. For U.S. tech behemoths, India is irresistible. Like the global payment networks they’ve largely been boxed out of China. In mature European and North American markets consumers and merchants are well served by existing payment systems and banks. Consequently, American tech titans haven’t attempted to build payment networks. Instead they use and facilitate access to existing systems, thereby increasing consumer engagement on and the value of their platforms. Tech platforms such as Google, Apple, Facebook and Amazon enjoy network effects in markets where the winner takes all or there are only a couple winners. -

How Access Your Debit Card Using Apple, Google Or Samsung Pay

How Access your Debit Card using Apple, Google or Samsung Pay Apple Pay Open “Wallet” which is pre-installed on your phone. Tap the + button at the top-right of the screen to add one. If you don't have Touch ID setup yet, you'll be walked through registering your fingerprints. Next, use the camera viewfinder to scan in your card. Just center it in the frame and Apple Pay will grab all of the details, or you can enter them manually. Like with the other payment options, you'll need to verify your card using a text message or email code sent to you from your bank. Enter that and you're all set. To use Apple Pay while your phone is locked, just double tap the home button. It'll bring up your favorite debit or credit card, or you can select others at the bottom of the screen. Hold your finger to Touch ID as you tap the phone on an Apple Pay-approved reader. Google Pay Download Google Pay from the Google Play App Store. Open the app and tap "Add Credit or Debit card." You can choose cards already associated with your Google Account or add a new one. Agree to the terms and conditions that pop up. Then verify your card via email (you'll receive a number to enter into the app) That's it! Now, the next time you see a card reader with the Google Pay logo, just open the app, choose your card, and tap to pay. Samsung Pay Open up Samsung Pay, which should be pre-installed on your Samsung smartphone. -

Samsung Galaxy Note 5 N920R6 User Manual

SMART PHONE User Manual Please read this manual before operating your device and keep it for future reference. Legal Notices Warning: This product contains chemicals known to Disclaimer of Warranties; the State of California to cause cancer, birth defects, or other reproductive harm. For more information, Exclusion of Liability please call 1-800-SAMSUNG (726-7864). EXCEPT AS SET FORTH IN THE EXPRESS WARRANTY CONTAINED ON THE WARRANTY PAGE ENCLOSED WITH THE PRODUCT, THE Intellectual Property PURCHASER TAKES THE PRODUCT “AS IS”, AND All Intellectual Property, as defined below, owned SAMSUNG MAKES NO EXPRESS OR IMPLIED by or which is otherwise the property of Samsung WARRANTY OF ANY KIND WHATSOEVER WITH or its respective suppliers relating to the SAMSUNG RESPECT TO THE PRODUCT, INCLUDING BUT Phone, including but not limited to, accessories, NOT LIMITED TO THE MERCHANTABILITY OF THE parts, or software relating there to (the “Phone PRODUCT OR ITS FITNESS FOR ANY PARTICULAR System”), is proprietary to Samsung and protected PURPOSE OR USE; THE DESIGN, CONDITION OR under federal laws, state laws, and international QUALITY OF THE PRODUCT; THE PERFORMANCE treaty provisions. Intellectual Property includes, OF THE PRODUCT; THE WORKMANSHIP OF THE but is not limited to, inventions (patentable or PRODUCT OR THE COMPONENTS CONTAINED unpatentable), patents, trade secrets, copyrights, THEREIN; OR COMPLIANCE OF THE PRODUCT software, computer programs, and related WITH THE REQUIREMENTS OF ANY LAW, RULE, documentation and other works of authorship. You SPECIFICATION OR CONTRACT PERTAINING may not infringe or otherwise violate the rights THERETO. NOTHING CONTAINED IN THE secured by the Intellectual Property. Moreover, INSTRUCTION MANUAL SHALL BE CONSTRUED you agree that you will not (and will not attempt TO CREATE AN EXPRESS OR IMPLIED WARRANTY to) modify, prepare derivative works of, reverse OF ANY KIND WHATSOEVER WITH RESPECT TO engineer, decompile, disassemble, or otherwise THE PRODUCT. -

Mastercard with Samsung

MASTERCARD® WITH SAMSUNG PAY ISSUER FAQ 1. What has been announced? 6. How do consumers set up their MasterCard to make Samsung announced the official launch of its mobile payment payments with Samsung Pay? service, Samsung Pay, initially on the Samsung Galaxy S6 and Consumers will create a Samsung account and add a fi ngerprint and Samsung S6 edge, S6 edge+ and Galaxy Note5. Samsung Pay will backup PIN to the device Settings. They can use the phone’s camera broaden the reach for mobile payments at the POS and enable to scan the card information and then the account is secured with MasterCard® cardholders to use compatible Samsung devices for a fingerprint and backup PIN. Cardholders can load eligible Credit, everyday purchases, at both contactless (NFC) and magnetic stripe Debit, Prepaid, and Small Business cards that have been enabled on POS terminals in the U.S. MDES by participating Issuers for Samsung Pay. 2. When will Samsung Pay be available for consumers? 7. How does Samsung Pay address safety? The service is slated to be available in the U.S. on September 28, Safety features include tokenization and cryptogram validation via 2015, with a limited invitation-only Beta program prior. Samsung Pay MDES and cardholder validation via fingerprint authentication or is compatible with select cards and Samsung devices; see backup PIN. Samsung does not store or share any payment information www.samsung.com/pay for details. 8. Where can consumers use Samsung Pay? 3. What is MasterCard’s relationship with Samsung? Consumers can use Samsung Pay at merchants accepting contactless MasterCard is working with Samsung to deliver a seamless and payments as well as mag-stripe only terminals commonly deployed secure mobile payment experience at both contactless-enabled POS in-stores where a plastic card can be swiped. -

Samsung Galaxy GS9|GS9+ G960U|G965U User Manual

User manual Table of contents Features 1 Meet Bixby 1 Camera 1 Mobile continuity 1 Dark mode 1 Security 1 Expandable storage 1 Getting started 2 Galaxy S9 3 Galaxy S9+ 4 Assemble your device 5 Charge the battery 6 Start using your device 6 Use the Setup Wizard 6 Transfer data from an old device 7 Lock or unlock your device 8 Accounts 9 Set up voicemail 10 i UNL_G960U_G965U_EN_UM_TN_TA5_021820_FINAL Table of contents Navigation 11 Navigation bar 16 Customize your home screen 18 Bixby 26 Digital wellbeing and parental controls 27 Always On Display 28 Flexible security 29 Mobile continuity 33 Multi window 36 Edge screen 37 Enter text 44 Emergency mode 47 Apps 49 Using apps 50 Uninstall or disable apps 50 Search for apps 50 Sort apps 50 Create and use folders 51 Game Booster 51 ii Table of contents App settings 52 Samsung apps 54 Galaxy Essentials 54 Galaxy Store 54 Galaxy Wearable 54 Game Launcher 54 Samsung Health 55 Samsung Members 56 Samsung Notes 57 Samsung Pay 59 Smart Switch 60 SmartThings 61 Calculator 62 Calendar 63 Camera 65 Clock 71 Contacts 76 Email 81 Gallery 84 iii Table of contents Internet 90 Messages 93 My Files 95 Phone 97 Google apps 105 Chrome 105 Drive 105 Duo 105 Gmail 105 Google 105 Maps 106 Photos 106 Play Movies & TV 106 Play Music 106 Play Store 106 YouTube 106 Additional apps 107 Facebook 107 iv Table of contents Settings 108 Access Settings 109 Search for Settings 109 Connections 109 Wi-Fi 109 Bluetooth 111 Phone visibility 113 NFC and payment 113 Airplane mode 114 Data usage 114 Mobile hotspot 114 Tethering 116 -

What Is Samsung Pay?

Samsung Pay™ H A W A I I L A W Frequently Asked ENFORCEMENT FEDERAL CREDIT UNION Questions What is Samsung Pay? Samsung Pay is Samsung’s Mobile Wallet service that broadens the reach of mobile payments, by allowing HLEFCU MasterCard cardholders that enroll in the service to use compatible Samsung devices for everyday purchases at both contactless (NFC) and traditional magnetic stripe POS terminals. What devices are compatible with Samsung Pay? Samsung Pay is available to U.S. consumer on the Galaxy S6, Galaxy S6 edge, Galaxy S6 edge+, Galaxy S6 active, Galaxy Note5, and later devices. Galaxy S6, S6 edge, S6 edge+ and Note5 devices require the user to download an app to use Samsung Pay, while later devices will come preloaded with the required app. To download the app, visit the Google Play™ store. Is there a fee to use Samsung Pay? No, Samsung Pay is free; however, third party charges such as wireless carrier message and data rates may apply. Which HLEFCU cards will I be able to use with Samsung Pay? All HLEFCU Platinum MasterCard credit cards and MasterCard debit cards are available for use with Samsung Pay. How do I add my card to Samsung Pay? • Open the Samsung Pay app and, if you haven’t already done so, login to your Samsung account. • Touch Start to continue. • Then touch Use Fingerprint to assign your fingerprint as the verification method. If you do not already have your fingerprint on your device, you will be given a chance to add one at this time. • Create a Samsung Pay PIN and re-enter PIN to confirm. -

Payment Aspects of Financial Inclusion in the Fintech Era

Committee on Payments and Market Infrastructures World Bank Group Payment aspects of financial inclusion in the fintech era April 2020 This publication is available on the BIS website (www.bis.org). © Bank for International Settlements 2020. All rights reserved. Brief excerpts may be reproduced or translated provided the source is stated. ISBN 978-92-9259-345-2 (print) ISBN 978-92-9259-346-9 (online) Table of contents Foreword .................................................................................................................................................................... 1 Executive summary ................................................................................................................................................. 2 1. Introduction ....................................................................................................................................................... 4 2. Fintech developments of relevance to the payment aspects of financial inclusion ............. 6 2.1 New technologies ................................................................................................................................. 7 2.1.1 Application programming interfaces ......................................................................... 7 2.1.2 Big data analytics ............................................................................................................... 8 2.1.3 Biometric technologies ................................................................................................... -

Sustainable Development of a Mobile Payment Security Environment Using Fintech Solutions

sustainability Article Sustainable Development of a Mobile Payment Security Environment Using Fintech Solutions Yoonyoung Hwang 1, Sangwook Park 1,* and Nina Shin 2,* 1 School of Business, Seoul National University, Seoul 08826, Korea; [email protected] 2 School of Business, Sejong University, Seoul 05006, Korea * Correspondence: [email protected] (S.P.); [email protected] (N.S.) Abstract: Financial technology (fintech) services have come to differentiate themselves from tradi- tional financial services by offering unique, niche, and customized services. Mobile payment service (MPS) has emerged as the most crucial fintech service. While many studies have addressed the essential role of security when service providers and users choose to engage in financial transactions, the relationship between users distinct perceptions of security and MPS success determinants are yet to be examined. Thus, this study primarily aims to uncover the distinctive roles of platform and tech- nology security by investigating how users react differently to their varying understandings of the MPS usage environment. This study proposes a research model comprising two security dimensions (platform and technology) and three MPS success determinants (convenience, interoperability, and trust). We evaluated the proposed model empirically by using an online survey of 356 users. The survey accounts users experiences of the selected MPS. The results show that a security driven MPS can essentially enhance or deteriorate users positive perceptions of MPS success determinants while they use it for financial transactions. To further understand how this recent trend of user perception of security affects the overall MPS usage experience, this study provides theoretical insights into the roles of platform and technology securities. -

How Will Traditional Credit-Card Networks Fare in an Era of Alipay, Google Tez, PSD2 and W3C Payments?

How will traditional credit-card networks fare in an era of Alipay, Google Tez, PSD2 and W3C payments? Eric Grover April 20, 2018 988 Bella Rosa Drive Minden, NV 89423 * Views expressed are strictly the author’s. USA +1 775-392-0559 +1 775-552-9802 (fax) [email protected] Discussion topics • Retail-payment systems and credit cards state of play • Growth drivers • Tectonic shifts and attendant risks and opportunities • US • Europe • China • India • Closing thoughts Retail-payment systems • General-purpose retail-payment networks were the greatest payments and retail-banking innovation in the 20th century. • >300 retail-payment schemes worldwide • Global traditional payment networks • Mastercard • Visa • Tier-two global networks • American Express, • China UnionPay • Discover/Diners Club • JCB Retail-payment systems • Alternative networks building claims to critical mass • Alipay • Rolling up payments assets in Asia • Partnering with acquirers to build global acceptance • M-Pesa • PayPal • Trading margin for volume, modus vivendi with Mastercard, Visa and large credit-card issuers • Opening up, partnering with African MNOs • Paytm • WeChat Pay • Partnering with acquirers to build overseas acceptance • National systems – Axept, Pago Bancomat, BCC, Cartes Bancaires, Dankort, Elo, iDeal, Interac, Mir, Rupay, Star, Troy, Euro6000, Redsys, Sistema 4b, et al The global payments land grab • There have been campaigns and retreats by credit-card issuers building multinational businesses, e.g. Citi, Banco Santander, Discover, GE, HSBC, and Capital One. • Discover’s attempts overseas thus far have been unsuccessful • UK • Diners Club • Network reciprocity • Under Jeff Immelt GE was the worst-performer on the Dow –a) and Synchrony unwound its global franchise • Amex remains US-centric • Merchant acquiring and processing imperative to expand internationally.