The Redback Cometh: Renminbi Internationalization & What to Do About It

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

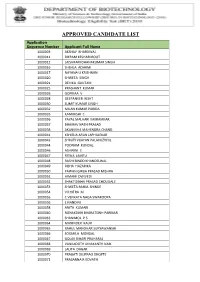

Approved Candidate List

APPROVED CANDIDATE LIST Application Sequence Number Applicant Full Name 1000003 AKSHAY BHARDWAJ 1000011 BIKRAM KESHARI ROUT 1000012 LAISHRAM DHANAKUMAR SINGH 1000016 SHEHLA ADHAMI 1000017 NAYANA U KRISHNAN 1000020 SHWETA SINGH 1000021 DEVIKA GAUTAM 1000025 PRASHANT KUMAR 1000026 GOPIKAA V 1000028 DEEPANKER BISHT 1000030 SUMIT KUMAR SINGH 1000032 MILAN KUMAR PARIDA 1000035 KAMAKSHI C 1000036 PAYAL MALHARI KAKRAMKAR 1000037 BHAIRAV NATH PRASAD 1000038 AKANKSHA MAHENDRA CHAND 1000041 KSHITIJA ARUN JAPHALEKAR 1000043 SHRUTI VIJAYAN PALAKUZHIYIL 1000044 POONAM KUNDAL 1000046 ASHWINI E 1000047 RITIKA JAINTU 1000048 RASHI BINOD KHANDELWAL 1000049 RISHA HAZARIKA 1000050 PAWAN GIRIJA PRASAD MISHRA 1000051 HIMANI DWIVEDI 1000052 SHAKTISINHA PRASAD CHOUGALE 1000053 SHWETA RAHUL SHINDE 1000054 VICHITRA M 1000055 C VENKATA NAGA SWAROOPA 1000056 E NANDINI 1000058 ANITA KUMARI 1000060 RONAKSINH BHARATSINH PARMAR 1000063 SHANIMOL P S 1000064 MANINDER KAUR 1000065 RAHUL MANOHAR SURYAWANSHI 1000066 SOUMILA MONDAL 1000067 GOLAK BIHARI PRAHARAJ 1000068 VANKADOTH UMAKANTH NAIK 1000069 LALITA DAGAR 1000070 PRAGATI DILIPRAO DHOPTE 1000071 PRASANNA R KOVATH 1000072 VYAS KUMAR 1000075 POOJA 1000077 NEHA THAKUR 1000078 SACHIN PANWAR 1000079 LEENA ARORA 1000081 PRITISH RAJ SHUKLA 1000083 JYOTI SHARMA 1000085 MALLEPOGU RAJESH 1000087 SANJANA G M 1000088 KHEM SINGH 1000089 AMULYA OF G 1000090 AKASH KUMAR 1000092 POORNIMA R 1000094 AFREEN RASHID 1000095 KAVITHA S 1000097 KAMAL KHAN 1000100 JAYSHREEBEN NATVARLAL PARMAR 1000102 SHRUTI SINHA 1000104 MANISHA GOSWAMI 1000105 -

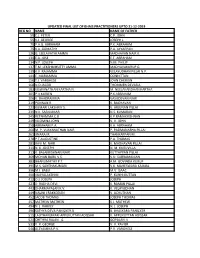

Reg No Name Name of Father 50 C.J. Peter C.P. John 55 K.J. George Joseph J

UPDATED FINAL LIST OF BHMS PRACTITIONERS UPTO 31-12-2019 REG NO NAME NAME OF FATHER 50 C.J. PETER C.P. JOHN 55 K.J. GEORGE JOSEPH J. 70 P.A.G. ABRAHAM P.K. ABRAHAM 75 K.A. GOMATHY P.A. AYYAPPAN 126 G. LEELAVATHI AMMA MADHAVAN NAIR K. 131 E.A. JOSE E.T. ABRAHAM 134 N.P. JOSEPH N.M. PHILIP 137 T.M. LEKSHMIKUTTY AMMA MADHAVAKURUP G. 139 K.V. RAJAMMA VELAYUDHAN PILLAI N.P. 141 E. MARIAMMA OONNITTAN 156 T.J. VARGHESE JOHN CHERIAN 168 N.D.JACOB THOMMEN DEVASIA 183 VISWANATHAN KARTHA N. M. NEELAKANDHAN KARTHA 205 P.A.KURIEN P.K.ABRAHAM 206 V. BHADRAMMA VASUDEVAN NAIR 219 PONNAN R. K. RAGHAVAN 223 KUMARI LAKSHMY S. V. ARJUNAN PILLAI 235 N.K. SASIKUMAR N.S. KUMARAN 245 RETNAMMA.C.B K.P.RAMAKRISHNAN 249 VILOMINA JOHN V. V. JOHN 258 ABRAHAM P.A. K.A. ABRAHAM 260 M. P. VIJAYANATHAN NAIR P. PADMANABHA PILLAI 261 JINARAJ R. THANKAPPAN M. 278 P.T.AUGUSTINE P.A. THOMAS 281 RAVI M. NAIR K. MADHAVAN PILLAI 311 N. K. JOSEPH N. M. KURUVILLA 313 K. BALAKRISHNAN NAIR KUTTAPPAN PILLAI 369 MOHAN BABU V.S. V.U. SUBRAMANIAN 383 BHANUMATHY P.T. A.M. GOVINDA KURUP 395 M.S. SANTHAKUMARI V.K. MAHESWARA KAIMAL 396 M.I. BABU M.V. ISAAC 400 VIJAYALAKSHMI P. KUNHI KUTTAN 412 O.J. JOSEPH JOSEPH 423 D. RADHA DEVI K. RAMAN PILLAI 443 DHARMAPALAN K.V. K. VELAYUDHAN 449 NALINI ERAKKODAN V. ACHUTHAN 452 JACOB THOMAS JOSEPH THOMAS 457 MATHEW MATHEW K.J. -

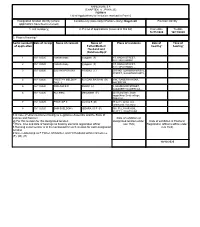

ANNEXURE 5.8 (CHAPTER V , PARA 25) FORM 9 List of Applications For

ANNEXURE 5.8 (CHAPTER V , PARA 25) FORM 9 List of Applications for inclusion received in Form 6 Designated location identity (where Constituency (Assembly/£Parliamentary): Nagercoil Revision identity applications have been received) 1. List number@ 2. Period of applications (covered in this list) From date To date 16/11/2020 16/11/2020 3. Place of hearing * Serial number$ Date of receipt Name of claimant Name of Place of residence Date of Time of of application Father/Mother/ hearing* hearing* Husband and (Relationship)# 1 16/11/2020 Nabisha baby Iyyappan (F) 4/7, KADAI STREET, KATTUPUTHOOR, , 2 16/11/2020 Nabisha baby Iyyappan (F) 4/7, KADAI STREET, KATTUPUTHOOR, , 3 16/11/2020 SUJITHA PRAVIYA PRABHU (F) 20/104B, AZHAMMAN KOVIL STREET, BHOOTHAPANDY, , 4 16/11/2020 PREETHY MELDISH SUNDAR SINGH M (H) 3/86, GANESH NAGAR, PAUL J NAGERCOIL, , 5 16/11/2020 RESHMA B R ROBIN (H) 2, SAMBAVAR STREET, VADASERY NAGERCOIL, , 6 16/11/2020 Arul arasu Mariyadass (F) 253,Ruby illam, Scott nagar,Near Scott college, Nagercoil, , 7 16/11/2020 PRATHAP C Vanitha S (M) 85 A 7/1, Annai tiles compound, Kurusday, , 8 16/11/2020 SAM SHELDON J JEBARAJ G P (F) 568, PILLAYAR KOIL STREET, NAGERCOIL, , £ In case of Union territories having no Legislative Assembly and the State of Jammu and Kashmir Date of exhibition at @ For this revision for this designated location designated location under Date of exhibition at Electoral * Place, time and date of hearings as fixed by electoral registration officer rule 15(b) Registration Officer’s Office under $ Running serial number is to be maintained for each revision for each designated rule 16(b) location # Give relationship as F-Father, M=Mother, and H=Husband within brackets i.e. -

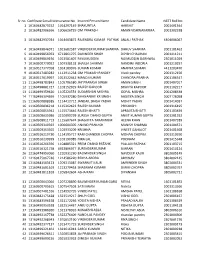

Investor First Name Investor Middle Name Investor Last Name Father

Investor First Name Investor Middle Name Investor Last Name Father/Husband First Name Father/Husband Middle Name Father/Husband Last Name Address Country State District Pin Code Folio No. DP.ID-CL.ID. Account No. Invest Type Amount Transferred Proposed Date of Transfer to IEPF PAN Number Aadhar Number 74/153 GANDHI NAGAR A ARULMOZHI NA INDIA Tamil Nadu 636102 IN301774-10480786-0000 Amount for unclaimed and unpaid dividend 160.00 15-Sep-2019 ATTUR 1/26, VALLAL SEETHAKATHI SALAI A CHELLAPPA NA KILAKARAI (PO), INDIA Tamil Nadu 623517 12010900-00960311-TE00 Amount for unclaimed and unpaid dividend 60.00 15-Sep-2019 RAMANATHAPURAM KILAKARAI OLD NO E 109 NEW NO D A IRUDAYAM NA 6 DALMIA COLONY INDIA Tamil Nadu 621651 IN301637-40636357-0000 Amount for unclaimed and unpaid dividend 20.00 15-Sep-2019 KALAKUDI VIA LALGUDI OPP ANANDA PRINTERS I A J RAMACHANDRA JAYARAMACHAR STAGE DEVRAJ URS INDIA Karnataka 577201 IN300360-10245686-0000 Amount for unclaimed and unpaid dividend 8.00 15-Sep-2019 ACNPR4902M NAGAR SHIMOGA NEW NO.12 3RD CROSS STREET VADIVEL NAGAR A J VIJAYAKUMAR NA INDIA Tamil Nadu 632001 12010600-01683966-TE00 Amount for unclaimed and unpaid dividend 100.00 15-Sep-2019 SANKARAN PALAYAM VELLORE THIRUMANGALAM A M NIZAR NA OZHUKUPARAKKAL P O INDIA Kerala 691533 12023900-00295421-TE00 Amount for unclaimed and unpaid dividend 20.00 15-Sep-2019 AYUR AYUR FLAT - 503 SAI DATTA A MALLIKARJUNAPPA ANAGABHUSHANAPPA TOWERS RAMNAGAR INDIA Andhra Pradesh 515001 IN302863-10200863-0000 Amount for unclaimed and unpaid dividend 80.00 15-Sep-2019 AGYPA3274E -

IN-ABSENTIA CANDIDATES Course Faculty: FACULTY of SURGERY and SURGICAL SPECIALITIES

THE TAMILNADU Dr.M.G.R MEDICAL UNIVERSITY 69,ANNA SALAI, GUINDY, CHENNAI - 600 032. 27th Convocation APR-2015 - LIST OF IN-ABSENTIA CANDIDATES Course Faculty: FACULTY OF SURGERY AND SURGICAL SPECIALITIES S.No Reg.No Name of the Candidate Sex Date of Birth Month & Yr. Seat No. of Passing Course: 141605.Ph.D. ORTHOPAEDICS Institution : 000.THE TAMIL NADU DR. M.G.R. MEDICAL UNIVERSITY CHENNAI 1 45415/2002 THOMAS GEORGE Male 14-04-1956 NOV-2012 Course: 141903.Ph.D. PAEDIATRIC AND PAEDIATRIC SPECIALITIES Institution : 000.THE TAMIL NADU DR. M.G.R. MEDICAL UNIVERSITY CHENNAI 2 16303/2008 POOVAZHAGI V Female 01-06-1967 NOV-2014 Course: 141801.Ph.D. PHARMACOGNOSY AND PHARMACOLOGY Institution : 000.THE TAMIL NADU DR. M.G.R. MEDICAL UNIVERSITY CHENNAI 3 10362/2010 VIJAYALAKSHMI A Female 14-07-1975 JUL-2014 Course: 141103.Ph.D. PHARMACEUTICAL CHEMISTRY Institution : 000.THE TAMIL NADU DR. M.G.R. MEDICAL UNIVERSITY CHENNAI 4 23516/2008 PRIYADARSINI R Female 17-04-1979 JAN-2015 5 35144/2008 LATHA S.T. Female 16-03-1973 DEC-2014 Course: 141111.Ph.D. PHARMACEUTICAL ANALYSIS Institution : 000.THE TAMIL NADU DR. M.G.R. MEDICAL UNIVERSITY CHENNAI 6 22919/2008 SAMINATHAN J Male 02-08-1980 FEB-2015 Course: 141104.Ph.D. PHARMACOLOGY Institution : 000.THE TAMIL NADU DR. M.G.R. MEDICAL UNIVERSITY CHENNAI 7 38032/2010 KULKARNI ABHIJEET SHASHIKANT Male 07-09-1983 JAN-2015 Course: 141101.Ph.D. PHARMACEUTICAL SCIENCES Institution : 000.THE TAMIL NADU DR. M.G.R. MEDICAL UNIVERSITY CHENNAI 8 21954/2008 AVINASH BALASHEB GANGURDE Male 25-05-1980 SEP-2014 Course: 141105.Ph.D PHARMACEUTICS Institution : 000.THE TAMIL NADU DR. -

Cin Company DIN Director Page 1

Cin Company DIN Director U01100KL2007PTC020727 NADACKAL PLANTATIONS PRIVATE LIMITED 1379983 JOY PAUL U01100KL2007PTC020727 NADACKAL PLANTATIONS PRIVATE LIMITED 3165523 JANCY JOY U01100KL2009PTC024908 UDUMALAI PLANTATIONS PRIVATE LIMITED 2735531 NAZAR KOOTINTAKAYIL U01100KL2009PTC024908 UDUMALAI PLANTATIONS PRIVATE LIMITED 2735571 SALEEM UMMER U01100KL2009PTC024908 UDUMALAI PLANTATIONS PRIVATE LIMITED 2735632 KAMALUDHEEN THOPPIL ANDEPUTTIL MOHAMED U01100KL2009PTC024908 UDUMALAI PLANTATIONS PRIVATE LIMITED 2921624 RASHEED GEOGREEN FARMS AND PROPERTY U01100KL2010PLC026651 DEVELOPERSLIMITED 1811199 RAJESH KRISHNA GEOGREEN FARMS AND PROPERTY U01100KL2010PLC026651 DEVELOPERSLIMITED 2840813 SAJI KEZHAPLAKKAL GEOGREEN FARMS AND PROPERTY U01100KL2010PLC026651 DEVELOPERSLIMITED 2924333 DINESH SUBRAHMANIAN MERRY LAND PLANTATIONS & DEVELOPERSPRIVATE MADHAVAN PATTAYIL U01100KL2010PTC025528 LIMITED 2861460 CHOYIMUKKIL MERRY LAND PLANTATIONS & DEVELOPERSPRIVATE MOHANDAS KOYAPPA U01100KL2010PTC025528 LIMITED 2861596 PUTHUKATTIL U01100KL2010PTC026186 PRUDENT AGRO FARMS PRIVATE LIMITED 1266984 ABDUL SALAM FAIZAL U01100KL2010PTC026186 PRUDENT AGRO FARMS PRIVATE LIMITED 1267028 NOWFAL SALAM MADHU KORASSERRY U01100KL2010PTC026389 CIEL AGRO FARMS ANDPLANTATION PRIVATELIMITED 3031200 KAMALAKSHAN U01100KL2010PTC026389 CIEL AGRO FARMS ANDPLANTATION PRIVATELIMITED 3031206 MELVIN REBELLO U01100KL2010PTC026389 CIEL AGRO FARMS ANDPLANTATION PRIVATELIMITED 3039991 PRAKASH KESAVAN U01100KL2010PTC027098 KUTHANUR PLANTATIONS PRIVATE LIMITED 155090 RAMESH NAIR U01100KL2010PTC027098 -

-

Trends in Trade and Investment Policies in the MENA Region

MENA-OECD Working Group on Investment and Trade MENA-OECD Working Group on Investment and Trade Background Note Trends in trade and investment policies in the MENA region This background note was prepared by Dr. Nasser Saidi ([email protected]) and Aathira Prasad ([email protected]) of Nasser Saidi & Associates (https://nassersaidi.com). The viewpoints and proposals in this note are the authors’ own. 27-28 November 2018 Dead Sea, Jordan This document, as well as any data and map included herein, are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area. │3 Trends in trade and investment policies in the MENA region 1. MENA Trade and Investment in the global context ...................................................................... 9 2. MENA trade and investment: trends and patterns ...................................................................... 19 2.1. Main characteristics of trade in the MENA region ..................................................................... 19 2.2. Consequences of export concentration and dependence ............................................................. 21 2.3. MENA investment flows ............................................................................................................ 23 3. Main barriers to trade and investment.......................................................................................... 27 4. Recent reforms ................................................................................................................................ -

LIC HOUSING FINANCE LIMITED List of Candidates Selected for Written Examination - Recruitment of IT Professional (2021) Date: 03.02.2021 APPLICATION NO

LIC HOUSING FINANCE LIMITED List of Candidates Selected for Written Examination - Recruitment of IT Professional (2021) Date: 03.02.2021 APPLICATION NO. APPLICANT NAME FATHER / HUSBAND NAME APPLIED FOR AA47980 AARTI MEHTA PARVESH DATABASE ADMINISTRATOR ENGINEER AJ65982 AJAY SIDHARTH AJAY KUMAR DATABASE ADMINISTRATOR ENGINEER AK23678 AKASH GITE MANOHAR DATABASE ADMINISTRATOR ENGINEER AN30796 ANGURAJ RM RAMACHANDRAN DATABASE ADMINISTRATOR ENGINEER AN73812 ANKIT VAJPAYI GYAN CHANDRA BAJPAI DATABASE ADMINISTRATOR ENGINEER AN18923 ANKITA JENA ANTARJYAMI DAS DATABASE ADMINISTRATOR ENGINEER CH56489 CHETAN BRAMHANKAR HARISHCHANDRA DATABASE ADMINISTRATOR ENGINEER DH52384 DHANASHREE PARCHAND NARHARI DATABASE ADMINISTRATOR ENGINEER DI89625 DIPTI SHARMA MR. SHIV SHARAN SHARMA DATABASE ADMINISTRATOR ENGINEER HE26437 HEMA PRIYANKA RANGASAMY DATABASE ADMINISTRATOR ENGINEER HE06572 HEMANT JAIN MOHANLAL DATABASE ADMINISTRATOR ENGINEER IN28349 INDRAJIT DAS NIHAR RANJAN DAS DATABASE ADMINISTRATOR ENGINEER KA79054 KAMALANATHAN BALASUBRAMANIAN BALASUBRAMANIAN S DATABASE ADMINISTRATOR ENGINEER KA92614 KAUSTUBH SINGH S.P SINGH DATABASE ADMINISTRATOR ENGINEER KI50236 KIRAN DERE PRAKASH DATABASE ADMINISTRATOR ENGINEER LA59023 LAVESH PATIL GOKUL DATABASE ADMINISTRATOR ENGINEER LO20847 LOKCHANDAR EKAMBARAM EKAMBARAM S DATABASE ADMINISTRATOR ENGINEER MA29015 MANCHALA LAKSHMANA RAO MANCHALA MOHANA RAO DATABASE ADMINISTRATOR ENGINEER MA02749 MANPREET SAINI NIRMAL SINGH SAINI DATABASE ADMINISTRATOR ENGINEER MA03124 MATHAVAN KRISHNASAMY KRISHNASAMY DATABASE ADMINISTRATOR -

Foreign Policy in Transition Under Modi

JULY 2019 Looking Back, Looking Ahead: Foreign Policy In Transition Under Modi Harsh V Pant and Kabir Taneja, Editors Photo: Atul Loke/Getty Images Observer Research Foundation (ORF) is a public policy think-tank that aims to influence formulation of policies for building a strong and prosperous India. ORF pursues these goals by providing informed and productive inputs, in-depth research, and stimulating discussions. ISBN: 978-93-89094-56-5 ISBN Digital: 978-93-89094-54-1 © 2019 Observer Research Foundation. All rights reserved. No part of this publication may be reproduced, copied, archived, retained or transmitted through print, speech or electronic media without prior written approval from ORF. Attribution: Harsh V Pant and Kabir Taneja, Editors, “Looking Back and Looking Ahead: Indian Foreign Policy in Transition Under Modi”, ORF Special Report No. 93, July 2019, Observer Research Foundation. ISBN: 978-93-89094-56-5 ISBN Digital: 978-93-89094-54-1 © 2019 Observer Research Foundation. All rights reserved. No part of this publication may be reproduced, copied, archived, retained or transmitted through print, speech or electronic media without prior written approval from ORF. Looking Back, Looking Ahead: Foreign Policy in Transition Under Modi CONTENTS INTRODUCTION Harsh V. Pant ......................................................................................................................... 4 1 INDIA AND MAJOR POWERS United States of America Kashish Parpiani and Harsh V. Pant .............................................................................. -

Annual Report Presented by the Principal on the 48Th College Day

Annual Report presented by the Principal on the 48th College Day In the Name of Allah, the Most Beneficent, Most Merciful! May His Blessings be on the Holy Prophet (Peace Be Upon Him) and on all of us! Esteemed President, Respected Secretary, Respected Treasurer, Members of the Managing Committee, Distinguished Chief Guest Dr. Jebamalai Vinanchiarachi, Former Principal Adviser to the Director General, United Nations Industrial Development Organization (UNIDO), and Principal Adviser (present), Knowledge Management Associates Austria, learned colleagues, student friends and guests. It pleases me immensely to present the Annual Report on the activities of this esteemed institution during the Academic Year 2018-2019. This academic year was full of remarkable and unforgettable events that we can cherish forever. I thank with devotional fervor Almighty Allah for showing this institution the right path and guiding us safely to move on towards new zeniths. Every year our college reaches new altitudes. It gives me immense pleasure to extend a very warm welcome to the President of the College Managing Committee, Alhaj. P.S.A. Pallak Lebbe, the Secretary, Alhaj. T.E.S. Fathu Rabbani, the Treasurer, Alhaj. H.M. Shaik Abdul Cader and Executive Committee members of the Managing Committee, Alhaj. K.A. Meeran Mohideen, Alhaj. W.S. Syed Abdur Rahman, Alhaj. M.K.M. Mohamed Nazar, and Er. L.K.M.A. Muhammad Nawab Hussain. With the same cordiality I would like to welcome the Distinguished Chief Guest of this occation, Dr. Jebamalai Vinanchiarachi, other guests, the teaching staff, the non-teaching staff and the students. 1 48th Annual Day 2018-2019 I am immensely pleased to announce that the Autonomous Status of our college has been extended for five more years till 2023. -

TAMIL NADU AGRICULTURAL UNIVERSITY UNDER GRADUATE ADMISSION - RANKLIST 2020 Ranks Registrationno Studentname Aggregate Category 1 115845438 PRAVEEN KUMAR R

TAMIL NADU AGRICULTURAL UNIVERSITY UNDER GRADUATE ADMISSION - RANKLIST 2020 Ranks RegistrationNo StudentName Aggregate Category 1 115845438 PRAVEEN KUMAR R. 199.50 BC 2 115570484 GIRIVASAN T V 199.25 SC 3 104308964 PUSHKALA D.G. 199.00 BC 4 114705341 KAVYA R 198.00 BC 5 111490216 Siddharth K.S. 198.00 Open Competition 6 116510812 GOVARTHAN K. 198.00 BC 7 102747282 R SWATHI 197.50 BC 8 104532050 Darshini A 197.00 BC 9 108337650 MOHANAVENKATESH L 197.00 BC 10 113100986 POONKODI A.D. 196.68 BC 11 104104932 DIVYA R 196.25 BC 12 109482877 CHRISTINA S E 196.00 BC 13 116481578 Gokul Subash M. 196.00 BC 14 100754872 REDHANYA S 195.66 BC 15 115349231 SELVA SREE S. 195.50 Open Competition 16 110784137 EMIMA ELIZABETH G 195.50 BC 17 116310731 JAYAKIRUTHIKA M. 195.50 BC 18 114689775 MAHESHWARI R 195.00 BC 19 101113574 Madhusri ER 195.00 BC 20 105843695 SUBASREE V . 195.00 BC 21 106270941 PRADHISHA R 195.00 BC 22 102023013 SANGAMITHIRAI A. 195.00 MBC/DNC 23 103268279 Srimathi K. 195.00 BC 24 114425365 SHARAN SURYA S M 195.00 BC 25 105057936 MADHAVAN DHIVYA PRABA 194.66 BC 26 111629523 RAAHUL R J 194.50 BC 27 100540056 GOWSHIGA P. 194.50 BC 28 106325577 SHANMUGA DHARSHINI M.S. 194.50 SC 29 114768269 Sibhi P.S. 194.50 BC 30 104562264 ARAVINDHAN S. 194.25 BC 31 106661644 DEEPTHI P 194.00 BC 32 109271649 Rishi Kesavan B. 194.00 BC 33 103698859 Guru Raman C 194.00 Open Competition 34 108040968 JEEVITHA C.