Why Not a Global Currency?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Is the International Role of the Dollar Changing?

Is the International Role of the Dollar Changing? Linda S. Goldberg Recently the U.S. dollar’s preeminence as an international currency has been questioned. The emergence of the euro, changes www.newyorkfed.org/research/current_issues ✦ in the dollar’s value, and the fi nancial market crisis have, in the view of many commentators, posed a signifi cant challenge to the currency’s long-standing position in world markets. However, a study of the dollar across critical areas of international trade January 2010 ✦ and fi nance suggests that the dollar has retained its standing in key roles. While changes in the global status of the dollar are possible, factors such as inertia in currency use, the large size and relative stability of the U.S. economy, and the dollar pricing of oil and other commodities will help perpetuate the dollar’s role as the dominant medium for international transactions. Volume 16, Number 1 Volume y many measures, the U.S. dollar is the most important currency in the world. IN ECONOMICS AND FINANCE It plays a central role in international trade and fi nance as both a store of value Band a medium of exchange. Many countries have adopted an exchange rate regime that anchors the value of their home currency to that of the dollar. Dollar holdings fi gure prominently in offi cial foreign exchange (FX) reserves—the foreign currency deposits and bonds maintained by monetary authorities and governments. And in international trade, the dollar is widely used for invoicing and settling import and export transactions around the world. -

Virtual Currency Schemes of 2012

VIRTUAL CURRENCY SCHEMES OCTOBER 2012 VIRTUAL CURRENCY SCHEMES OctoBer 2012 In 2012 all ECB publications feature a motif taken from the €50 banknote. © European Central Bank, 2012 Address Kaiserstrasse 29 60311 Frankfurt am Main Germany Postal address Postfach 16 03 19 60066 Frankfurt am Main Germany Telephone +49 69 1344 0 Website http://www.ecb.europa.eu Fax +49 69 1344 6000 All rights reserved. Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged. ISBN: 978-92-899-0862-7 (online) CONTENTS EXECUTIVE SUMMARY 5 1 INTRODUCTION 9 1.1 Preliminary remarks and motivation 9 1.2 A short historical review of money 9 1.3 Money in the virtual world 10 2 VIRTUAL CURRENCY SCHEMES 13 2.1 Definition and categorisation 13 2.2 Virtual currency schemes and electronic money 16 2.3 Payment arrangements in virtual currency schemes 17 2.4 Reasons for implementing virtual currency schemes 18 3 CASE STUDIES 21 3.1 The Bitcoin scheme 21 3.1.1 Basic features 21 3.1.2 Technical description of a Bitcoin transaction 23 3.1.3 Monetary aspects 24 3.1.4 Security incidents and negative press 25 3.2 The Second Life scheme 28 3.2.1 Basic features 28 3.2.2 Second Life economy 28 3.2.3 Monetary aspects 29 3.2.4 Issues with Second Life 30 4 THE RELEVANCE OF VIRTUAL CURRENCY SCHEMES FOR CENTRAL BANKS 33 4.1 Risks to price stability 33 4.2 Risks to financial stability 37 4.3 Risks to payment system stability 40 4.4 Lack of regulation 42 4.5 Reputational risk 45 5 CONCLUSION 47 ANNEX: REFERENCES AND FURTHER INFORMATION ON VIRTUAL CURRENCY SCHEMES 49 ECB Virtual currency schemes October 2012 3 EXECUTIVE SUMMARY Virtual communities have proliferated in recent years – a phenomenon triggered by technological developments and by the increased use of the internet. -

The Pound Sterling

ESSAYS IN INTERNATIONAL FINANCE No. 13, February 1952 THE POUND STERLING ROY F. HARROD INTERNATIONAL FINANCE SECTION DEPARTMENT OF ECONOMICS AND SOCIAL INSTITUTIONS PRINCETON UNIVERSITY Princeton, New Jersey The present essay is the thirteenth in the series ESSAYS IN INTERNATIONAL FINANCE published by the International Finance Section of the Department of Economics and Social Institutions in Princeton University. The author, R. F. Harrod, is joint editor of the ECONOMIC JOURNAL, Lecturer in economics at Christ Church, Oxford, Fellow of the British Academy, and• Member of the Council of the Royal Economic So- ciety. He served in the Prime Minister's Office dur- ing most of World War II and from 1947 to 1950 was a member of the United Nations Sub-Committee on Employment and Economic Stability. While the Section sponsors the essays in this series, it takes no further responsibility for the opinions therein expressed. The writer's are free to develop their topics as they will and their ideas may or may - • v not be shared by the editorial committee of the Sec- tion or the members of the Department. The Section welcomes the submission of manu- scripts for this series and will assume responsibility for a careful reading of them and for returning to the authors those found unacceptable for publication. GARDNER PATTERSON, Director International Finance Section THE POUND STERLING ROY F. HARROD Christ Church, Oxford I. PRESUPPOSITIONS OF EARLY POLICY S' TERLING was at its heyday before 1914. It was. something ' more than the British currency; it was universally accepted as the most satisfactory medium for international transactions and might be regarded as a world currency, even indeed as the world cur- rency: Its special position waS,no doubt connected with the widespread ramifications of Britain's foreign trade and investment. -

Presentation-From-Roundatable-4-Out

Central Europe & eurozone Saturday, 6 October 2018 Grand Hotel Kempinski High Tatras dr. Kinga Brudzinska [email protected] Overlapping Europes *Kosovo and Montenegro use Euro but are not part of the EU European Commission, “White Paper on the Future of Europe: Reflections and scenarios for the EU27 by 2025”, 2017 Short history of the euro ⊲ The Delors report (1989), proposed to articulate the realisation of Economic and Monetary Union (EMU) in different stages, which ultimately led to the creation of the single currency: the euro. ⊲ The Maastricht Treaty (1992), signed by twelve member countries of the, at the time called, European Community, now the EU. Among the many topics discussed, the European Council decided to create an Economic and Monetary Union. It entered into force on 1 November 1993. ⊲ Euro entered into force for the first time on 1 January 1999 in eleven of the, at the time, fifteen Member States of the Union, but only for non-physical forms of payment. The old currencies co-existed with the new currency until 28 February 2002, the date on which they ceased their legal tender and could not be accepted for payments. ⊲ The Lisbon Treaty (2009) The observance of the parameters established in the various European Treaties, is then merged into this treaty to try to get out of the crisis (Lehman Bank, 2008) and prevent it from being repeated in the future. ⊲ On 9 May 2010 the Council of the European Union agreed on the creation of the European Financial Stability Fund (EFSF) (to provide aid to debt-laiden Eurozone countries) and the European Financial Stabilisation Mechanism (EFSM). -

Chapter 2 International Monetary System Answers & Solutions to End-Of-Chapter Questions and Problems

CHAPTER 2 INTERNATIONAL MONETARY SYSTEM ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Explain Gresham’s Law. Answer: Gresham’s law refers to the phenomenon that bad (abundant) money drives good (scarce) money out of circulation. This kind of phenomenon was often observed under the bimetallic standard under which both gold and silver were used as means of payments, with the exchange rate between the two fixed. 2. Explain the mechanism which restores the balance of payments equilibrium when it is disturbed under the gold standard. Answer: The adjustment mechanism under the gold standard is referred to as the price-specie- flow mechanism expounded by David Hume. Under the gold standard, a balance of payment disequilibrium will be corrected by a counter-flow of gold. Suppose that the U.S. imports more from the U.K. than it exports to the latter. Under the classical gold standard, gold, which is the only means of international payments, will flow from the U.S. to the U.K. As a result, the U.S. (U.K.) will experience a decrease (increase) in money supply. This means that the price level will tend to fall in the U.S. and rise in the U.K. Consequently, the U.S. products become more competitive in the export market, while U.K. products become less competitive. This change will improve U.S. balance of payments and at the same time hurt the U.K. balance of payments, eventually eliminating the initial BOP disequilibrium. 3. Suppose that the pound is pegged to gold at 6 pounds per ounce, whereas the franc is pegged to gold at 12 francs per ounce. -

Ten Years from Now, What Will Be the Next Great Global Currency?”

Th€ Next Great Globa£ ¢urr€nc¥ TIE asked some of the THE MAGAZINE OF INTERNATIONAL ECONOMIC POLICY 888 16th Street, N.W., Suite 740 Washington, D.C. 20006 Phone: 202-861-0791 • Fax: 202-861-0790 world’s key experts: www.international-economy.com “Ten years from now, what will be the next great global currency?” 22 THE INTERNATIONAL ECONOMY SPRING 2008 The Dollar The U.S. dollar will continue to be the dominant international currency. The dollar EDWIN M. TRUMAN Senior Fellow, Peterson Institute for International Economics will reemerge. he U.S. dollar will continue to be the dominant interna- tional currency in ten years. It is still the only true inter- DAVID C. MULFORD Tnational currency; that is one that is used by parties that U.S. Ambassador to India and do not include U.S. residents. Do you see euro- denominated former Undersecretary for bonds issued in New York as dollar-denominated bonds are International Affairs, U.S. Treasury issued in London? Looking just at reserve holdings and con- sidering only developing countries as the most relevant hat goes around comes around. We have been group, it is true that since the first quarter of 1999, the dollar’s around this loop before. The dollar will reemerge as share has declined 10.6 percentage points in value terms, but Wthe U.S. economy restores its position in the world. in quantity terms the decline has been only 6.8 percentage points and the dollar’s decline was at a faster pace before the dollar’s peak in the first quarter of 2002 than since then. -

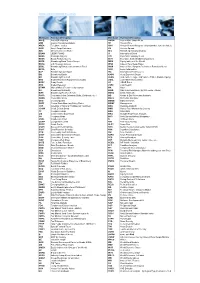

Bloomberg Functions

www.survivrelondres.co.uk Mnemonic Function Description Mnemonic Function Description ALLQ Bid & Offer Quotes HMSM Four-in-One Graph Menu ANR Analyst Recommendations HP Historic Price AREA Telephone Codes HRH Historic Return Histogram (sigma(stnd dev) for an index) ASW Asset Swap Calculator HS Historic Spread AZS Altman's Z-score Model IBQ Bloomberg Industry Analysis BBAM LIBOR FIXING IC International Clock BBEA Earnings Analysis ICN Important Company News BBSA Equity Analyst Survey IECO Economic Stats (Global Comparison) BBTE Bloomberg Bond Trader Europe IMEN Equity Indices of the World BBTG U.S. Treasury Actives IRSB Interest Rate Swap Rates BBXL Bloomberg Data & Calculations in Excel IRSM Interest Rate Swaps & Derivatives Functions Menu BETA Beta ISSD Issuer Information BLP Bloomberg Launchpad IYC International Yield Curves BQ Bloomberg Quote KAOS Hurst Exponent Graph BR Bloomberg Research LEAG Underwriter League and Volume Tables (Bonds, Equity) BRC Broker Research Reports by Company LMAL Loan Market Association BRDY Brady Bonds LR LIBOR Rates BRX Broker Research LSRC Loan Search BTMM Money Mkts &Treasuries by country MA M&A BU Bloomberg University MAIN Main Functions Menu (by Mkt sector, others) BWS Bloomberg Weather Service MANU Online Manuals CACS Corporate Action Calendar (Splits, Dividends, etc.) MB Metals & Ore Prices and Analysis CBMU Convertible Menu MCCL McClellan Oscillator CBQ Country Quotes MEMB Index Members CBRT Central Bank Monetary Policy Rates MGMT Management CDR Calendar of National Holidays (all countries) MGU Message -

The US Dollar- Scenario of a World Currency

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Büschgen, Hans E. Article — Digitized Version The US dollar- scenario of a world currency Intereconomics Suggested Citation: Büschgen, Hans E. (1987) : The US dollar- scenario of a world currency, Intereconomics, ISSN 0020-5346, Verlag Weltarchiv, Hamburg, Vol. 22, Iss. 2, pp. 59-68, http://dx.doi.org/10.1007/BF02932274 This Version is available at: http://hdl.handle.net/10419/140066 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified -

Three Essays on European Union Advances Toward a Single Currency and Its Implications for Business and Investors Charlotte Anne Bond Old Dominion University

Old Dominion University ODU Digital Commons Theses and Dissertations in Business College of Business (Strome) Administration Winter 1998 Three Essays on European Union Advances Toward a Single Currency and Its Implications for Business and Investors Charlotte Anne Bond Old Dominion University Follow this and additional works at: https://digitalcommons.odu.edu/businessadministration_etds Part of the Finance and Financial Management Commons, International Business Commons, and the International Relations Commons Recommended Citation Bond, Charlotte A.. "Three Essays on European Union Advances Toward a Single Currency and Its Implications for Business and Investors" (1998). Doctor of Philosophy (PhD), dissertation, , Old Dominion University, DOI: 10.25777/mc19-6f14 https://digitalcommons.odu.edu/businessadministration_etds/77 This Dissertation is brought to you for free and open access by the College of Business (Strome) at ODU Digital Commons. It has been accepted for inclusion in Theses and Dissertations in Business Administration by an authorized administrator of ODU Digital Commons. For more information, please contact [email protected]. Three Essays on European Union Advances Toward A Single Currency and its Implications for Business and Investors by Charlotte Anne Bond A dissertation submitted to the Faculty of Old Dominion University in partial fulfillment of the requirements for the degree of Doctor o f Philosophy (Finance) Old Dominion University College of Business Norfolk, Virginia (December 1998) Approved by: Mohammad Najand (Committee Chair) \ tee Member) Reproduced with permission of the copyright owner. Further reproduction prohibited without permission. UMI Number: 9921767 Copyright 1999 by Bond, Charlotte Anne All rights reserved. UMI Microform 9921767 Copyright 1999, by UMI Company. All rights reserved. This microform edition is protected against unauthorized copying under Title 17, United States Code. -

Modern Monetary Realism by James K

Modern Monetary Realism By James K. Galbraith March 15, 2019 – Project Syndicate Kenneth Rogoff’s criticism of Modern Monetary Theory assumes that MMT advocates don’t care about budget deficits or the independence of the US Federal Reserve. But these assumptions are wide of the mark, and Rogoff himself sometimes undermines his own arguments. Is Modern Monetary Theory (MMT) a would have predicted,” while “the US dollar potential boon to economic policymakers, or, has become increasingly dominant in global as Harvard’s Kenneth Rogoff recently argued, trade and finance.” Perhaps the US budget a threat to “the entire global financial system” deficit is not an immediate cause for panic after and the front line of the “next battle for central- all? bank independence”? For Rogoff, the threat MMT is not, as its opponents seem to think, seems to stem partly from the fear that MMT primarily a set of policy ideas. Rather, it is adherents may come to power in the United essentially a description of how a modern States in the 2020 elections. But he also makes credit economy actually works – how money is several substantive arguments, common to created and destroyed, by governments and by many critics of the MMT movement. banks, and how financial markets function. First, there is the claim that, as Rogoff puts it, Nor is MMT new: it is based on the work of MMT is all about “using the [US Federal John Maynard Keynes, whose A Treatise on Reserve’s] balance sheet as a cash cow to fund Money pointed out back in 1930 that “modern expansive new social programs.” Second, States” have functioned this way for thousands Rogoff and other MMT opponents strongly of years. -

Philadelphia Stock Exchange World Currency Options Trading

Philadelphia Stock Exchange World Currency Options Trading Currency Option Fundamentals Currency Market Analysis Currency Option Trading Al Brinkman, Director, Derivatives Marketing, Philadelphia Stock Exchange Jack Crooks, President, Blackswan Capital & Editor, World Currency Options Alert Newsletter The Underlying Currency Market Like many other investments, Foreign Exchange trading carries a high level of risk and may not be suitable for all investors Foreign Exchange trading requires constant monitoring and an understanding of the relationships between currencies, as well as what factors influence the currencies value. You will need to understand fully the market and some of its unique features. Any strategies discussed, including examples using actual securities and or price data, are strictly for illustrative and educational purposes only and are not to be construed as an endorsement, recommendation, or solicitation to buy or sell Trading Currency Options Options involve risks and are not suitable for everyone. Prior to buying or selling options, an investor must receive a copy of Characteristics and Risks of Standardized Options. Copies may be obtained by contacting your broker or The Options Industry Council at One North Wacker Drive, Chicago, IL 60606. In order to simplify the computations, commissions, fees, margin interest and taxes have not been included in the examples used in these materials. These costs will impact the outcome of all stock and options transactions and must be considered prior to entering into any transactions. Investors should consult their tax advisor about any potential tax consequences. Any strategies discussed, including examples using actual currencies/securities and price data, are strictly for illustrative and educational purposes only and are not to be construed as an endorsement, recommendation, or solicitation to buy or sell securities. -

Download the Transcript

FISCAL-2020/12/01 1 THE BROOKINGS INSTITUTION WEBINAR FISCAL POLICY ADVICE FOR JOE BIDEN AND CONGRESS Washington, D.C. Tuesday, December 1, 2020 PARTICIPANTS: Welcome: ADAM POSEN President, Peterson Institute for International Economics DAVID WESSEL Senior Fellow and Director, Hutchins Center on Fiscal & Monetary Policy, The Brookings Institution COVID-19 and the Near Term: WENDY EDELBERG Senior Fellow and Director, The Hamilton Project The Brookings Institution DOUGLAS ELMENDORF Dean and Don K. Price Professor of Public Policy, Harvard Kennedy School MICHAEL STRAIN Director of Economic Policy Studies and Arthur F. Burns Scholar in Political Economy, American Enterprise Institute ADAM POSEN, Moderator President Peterson Institute for International Economics ‘What About the Federal Debt’ Presentation: JASON FURMAN Professor of the Practice of Economic Policy Harvard Kennedy School LAWRENCE SUMMERS Charles W. Eliot University Professor and President Emeritus, Harvard University Discussion: BEN BERNANKE Distinguished Fellow in Residence, Hutchins Center on Fiscal & Monetary Policy OLIVIER BLANCHARD C. Fred Bergsten Senior Fellow, Peterson Institute for International Economic ANDERSON COURT REPORTING 1800 Diagonal Road, Suite 600 Alexandria, VA 22314 Phone (703) 519-7180 Fax (703) 519-7190 FISCAL-2020/12/01 2 PARTICIPANTS (CONT’D): JASON FURMAN Professor of the Practice of Economic Policy, Harvard Kennedy School KENNETH ROGOFF Professor of Economics and Thomas D. Cabot Professor of Public Policy, Harvard University LAWRENCE SUMMERS Charles W. Eliot University Professor and President Emeritus, Harvard University LOUISE SHEINER, Moderator Senior Fellow and Policy Director, Hutchins Center on Fiscal & Monetary Policy The Brookings Institution * * * * * ANDERSON COURT REPORTING 1800 Diagonal Road, Suite 600 Alexandria, VA 22314 Phone (703) 519-7180 Fax (703) 519-7190 FISCAL-2020/12/01 3 P R O C E E D I N G S MR.