2020 Comprehensive Annual Financial Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Northeast Harbor Library Archives GXS Collection Finding Aid

Northeast Harbor Library Archives GXS Collection Finding Aid Creator: Anonymous collector Dates: 1800s and 1900s Extent: 1 linear foot Accession Number: 2016.6.1 Record Numbers: None. Collection Processed by: Hannah Stevens Scope and Content Note: This collection is an assortment of ephemera relating to coastal Maine, Maine history, and inns, motels, hotels, and homes on Mount Desert Island and Hancock County. The collection is divided into 7 series: Books and Souvenir Booklets, Maps and Blueprints, Acadia National Park, Hotels/Inns/Schools/Homes/Buildings, Ephemera, Photos and Postcards. Note: this collection will continue to be added to as we make space in the archive room. Source of Acquisition: Donated by anonymous donor via Willie Granston as proxy, June 2016. Access Restrictions: This collection is open to research. The collection is subject to all copyright laws. Biographical Information: None. Box 1 Books and Souvenir Booklets Folder 1 Glimpses of Camden, Maine, 1904, J. R. Prescott, 28 pages Glimpses of Camden On the Coast of Maine, 1916, John R. Prescott, 1 volume (unpaged): all illustrations Folder 2 A Souvenir of Bar Harbor and Mount Desert Island, Maine, 190?, W. H. Sherman, 68 pages : chiefly illustrations Folder 3 Bar Harbor and Mount Desert Island, 1888, William Berry Lapham, 72 pages: illustrations Folder 4 unidentified book about Maine homes and churches in the early days, commentary about home design, coastal living, farming, and general livelihood. 32 pages missing covers. Folder 5 The Summer State of Maine, Holman D Waldron and Harry D Young, ca. 1893, Tourist booklet in the shape of the state of Maine; cover illustration is map of Maine, 24 pages Folder 31 Looking at Katahdin, the artists' inspiration, booklet about exhibit at L.C. -

Maine Campus March 22 1928 Maine Campus Staff

The University of Maine DigitalCommons@UMaine Maine Campus Archives University of Maine Publications Spring 3-22-1928 Maine Campus March 22 1928 Maine Campus Staff Follow this and additional works at: https://digitalcommons.library.umaine.edu/mainecampus Repository Citation Staff, Maine Campus, "Maine Campus March 22 1928" (1928). Maine Campus Archives. 3384. https://digitalcommons.library.umaine.edu/mainecampus/3384 This Other is brought to you for free and open access by DigitalCommons@UMaine. It has been accepted for inclusion in Maine Campus Archives by an authorized administrator of DigitalCommons@UMaine. For more information, please contact [email protected]. L. ue Meeting Tije ofiftitthr Canyttil Al meeting; Published Weekly by the Students of the University of Maine of Maine ten warm No. 21 MAINE, MARCH 22, 1928 trticipatieg Vol. XXIX ORONO, P indicates (I numbers. WIN COMpeted HEBRON ACADEMY AND BLUE BOOK OF SPORTS ENGLISH DEPARTMENT SENIOR ENGINEERS MAINE DEBATERS OVER leloted to- HARBOR HIGH WIN HONORS BILL KENYON ANNOUNCES NAMES OF ON INSPECTION TRIP• DOUBLE VICTORY ;iould be a BAR ion with a "Who's Who in Sportdom," a blue boa HIGH RANKING MAJORS COLBY CONTESTANTS BASKETBALL TOURNEY Civil. Electrical, Newt. Thk. of sports, published by the National lb, — SI-- partments oi t Iwtutcal. y logical Society has inserted the name kit and Nlechanical Engineering are on their THREE- are in WATERVILLE AND ORONO JUDGES St se%eral FAST AND INTERESTING GAMES William C. ("Bill') Kenyon on its roll MARGUERITE STANLEY, annual inspection trip. The men at onsideral4 of honor. lb tst. al and have their headquarters FAVOR BLUE REPRESENTATIVES ARE PLAYED IN BOTH YEAR STUDENT, LEADS began March red. -

National Register of Historic Places

NATIONAL REGISTER OF HISTORIC PLACES IN HANCOCK COUNTY, MAINE PLACE NAME STREET ADDRESS TOWN BRICK SCHOOL HOUSE SCHOOL HOUSE HILL AURORA TURRETS, THE EDEN STREET BAR HARBOR REDWOOD BARBERRY LANE BAR HARBOR HIGHSEAS SCHOONER HEAD ROAD BAR HARBOR CARRIAGE PATHS, BRIDGES AND GATEHOUSES ACADIA NATIONAL PARK+VICINITY BAR HARBOR EEGONOS 145 EDEN STREET BAR HARBOR CRITERION THEATRE 35 COTTAGE STREET BAR HARBOR WEST STREET HISTORIC DISTRICT WEST BET BILLINGS AVE+ EDEN ST BAR HARBOR SPROUL'S CAFE 128 MAIN STREET BAR HARBOR REVERIE COVE HARBORLANE BAR HARBOR ABBE, ROBERT, MUSEUM OF STONE AGE ANTIQUITY OFF ME 3 BAR HARBOR "NANAU" LOWER MAIN STREET BAR HARBOR JESUP MEMORIAL LIBRARY 34 MT DESERT ROAD BAR HARBOR KANE, JOHN INNES, COTTAGE OFF HANCOCK STREET BAR HARBOR US POST OFFICE - BAR HARBOR MAIN COTTAGE STREET BAR HARBOR SAINT SAVIOUR'S EPISCOPAL CHURCH & RECTORY 41 MT DESERT STREET BAR HARBOR COVER FARM OFF ME 3 (HULLS COVE) BAR HARBOR (FORMER) ST EDWARDS CONVENT 33 LEDGELAWN AVENUE BAR HARBOR HULLS COVE SCHOOL HOUSE CROOK ROAD & ROUTE 3 BAR HARBOR CHURCH OF OUR FATHER ME ROUTE 3 BAR HARBOR CLEFTSTONE 92 EDEN STREET BAR HARBOR STONE BARN FARM CROOKED RD AT NORWAY DRIVE BAR HARBOR FISHER, JONATHAN, MEMORIAL ME 15 (OUTER MAIN STREET) BLUE HILL HINCKLEY, WARD, HOUSE ADDRESS RESTRICTED BLUE HILL BARNCASTLE SOUTH STREET BLUE HILL BLUE HILL HISTORIC DISTRICT ME 15, ME 172, ME 176 & ME 177 BLUE HILL PETERS, JOHN, HOUSE OFF ME 176 BLUE HILL EAST BLUE HILL LIBRARY MILLIKEN ROAD BLUE HILL GODDARD SITE ADDRESS RESTRICTED BROOKLIN BROOKLIN IOOF HALL SR 175 -

New England Mathematics League

We group schools together for the purpose of regional awards. These regional groupings will be identified in the next Score Report Summary OCTOBER 2019 HIGH SCHOOL SCORE REPORT SUMMARY County/School Name #1 TOT County/School Name #1 TOT CONNECTICUT Berkshire Fairfield Buxton School 16 16 Brookfield HS 26 26 Mt. Greylock Reg. HS 19 19 Convent of the Sacred Heart 23 23 Wahconah Reg. HS Darien HS 26 26 Bristol Immaculate HS AL-Noor Academy 7 7 King School 24 24 Bishop Connolly HS 10 10 Masuk HS 22 22 Coyle & Cassidy HS 10 10 Ridgefield HS 25 25 Mansfield HS 22 22 St. Joseph HS North Attleboro HS 20 20 Stamford HS 20 20 Essex Stratford HS 16 16 Bishop Fenwick HS 17 17 Hartford Brooks School 26 26 Academy of Aerospace & 24 24 Peabody Veterans Mem. HS East Granby HS 16 16 Phillips Academy 27 27 Farmington HS 26 26 The Governor's Academy 25 25 Granby Memorial HS 13 13 Franklin Simsbury High School 23 23 Deerfield Academy 25 25 St. Paul Catholic HS 11 11 Eaglebrook School Suffield Academy 26 26 Hampshire Litchfield Williston Northamp. Sch 26 26 Canterbury School 23 23 Middlesex Hotchkiss School 25 25 AMSA Charter School 25 25 Kent School 25 25 Beaver Country Day Sch 15 15 New Milford HS 19 19 Belmont Hill School Northwestern Regional HS 23 23 Buckingham Browne & Nichols 25 25 Taft School 28 28 Burlington HS The Gunnery 17 17 Cambridge Rindge & Latin Sch Middlesex Cambridge Sch of Weston 22 22 Franklin Academy 24 24 Chelmsford HS 22 22 Middletown HS 17 17 Framingham HS 21 21 New Haven Jonas Clarke Middle School 28 28 Cheshire Academy 25 25 Lowell Catholic High School Cheshire HS 23 23 Malden Catholic HS Daniel Hand HS 25 25 Maynard HS 15 15 East Haven HS Natick HS 18 18 Oxford High School 14 14 Newton Country Day Sch 22 22 Sacred Heart Academy Reading Memorial HS New London Somerville HS 22 22 St. -

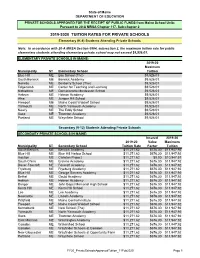

2019-2020 TUITION RATES for PRIVATE SCHOOLS Elementary (K-8) Students Attending Private Schools

State of Maine DEPARTMENT OF EDUCATION PRIVATE SCHOOLS APPROVED FOR THE RECEIPT OF PUBLIC FUNDS from Maine School Units Pursuant to 20-A MRSA Chapter 117, Sub-chapter 2 2019-2020 TUITION RATES FOR PRIVATE SCHOOLS Elementary (K-8) Students Attending Private Schools Note: In accordance with 20-A MRSA Section 5804, subsection 2, the maximum tuition rate for public elementary students attending elementary private school may not exceed $9,526.01. ELEMENTARY PRIVATE SCHOOLS IN MAINE: 2019-20 Maximum Municipality ST Elementary School Tuition Blue Hill ME Bay School (The) $9,526.01 South Berwick ME Berwick Academy $9,526.01 Norway ME Boxberry School (The) $9,526.01 Edgecomb ME Center for Teaching and Learning $9,526.01 Nobleboro ME Damariscotta Montessori School $9,526.01 Hebron ME Hebron Academy $9,526.01 Alna ME Juniper Hill School $9,526.01 Freeport ME Maine Coast Waldorf School $9,526.01 Yarmouth ME North Yarmouth Academy $9,526.01 Newry ME The Eddy School $9,526.01 Saco ME Thornton Academy $9,526.01 Portland ME Waynflete School $9,526.01 Secondary (9-12) Students Attending Private Schools SECONDARY PRIVATE SCHOOLS IN MAINE: Insured 2019-20 2019-20 Value Maximum Municipality ST Secondary School Tuition Rate Factor Tuition South Berwick ME Berwick Academy $11,271.62 $676.30 $11,947.92 Blue Hill ME Blue Hill Harbor School $11,271.62 $676.30 $11,947.92 Houlton ME Carleton Project $11,271.62 $0.00 $10,947.57 South China ME Erskine Academy $11,271.62 $676.30 $11,947.92 Dover-Foxcroft ME Foxcroft Academy $11,271.62 $676.30 $11,947.92 Fryeburg ME -

Petit Manan National Wildlife Refuge (Maine Coastal Islands National Wildlife Refuge)

Amended Environmental Assessment Public Hunting On Petit Manan National Wildlife Refuge (Maine Coastal Islands National Wildlife Refuge) Addison, Jonesport, Machiasport, Milbridge, Roque Bluffs, Steuben -Washington County; Bar Harbor, Gouldsboro, Swan’s Island, Tremont, Winter Harbor - Hancock County; Criehaven Twp., Friendship, St. George - Knox County; Boothbay, South Bristol - Lincoln County; Phippsburg, Sagadahoc County; Harpswell - Cumberland County, Maine February 2007 U.S. Department of the Interior Fish and Wildlife Service Maine Coastal Islands National Wildlife Refuge P.O. Box 279 Milbridge, ME 04658 Table of Contents I. Purpose and Need for Action.................................................................................. 5 II Proposal.................................................................................................................... 6 III Location.................................................................................................................... 6 IV Alternatives Including the Proposed Action......................................................... 9 A. Alternative 1 - Refuge closed to all Hunting…………………………………… 9 B. Alternative 2 - Proposed Action…………………………………………………9 C. Alternative 3 – Hunt Conducted Under Permit System……………………….. 10 V Affected Environment............................................................................................10 A. Brief History, Purpose, and Objectives of the Refuge.........................................10 Physical Resources………………………………………………………....11 -

Biological Summary of Islands Within Maine Coastal Islands National Wildlife

Maine Coastal Islands NWR Biological Summary of Islands within Maine Coastal Islands National Wildlife Refuge December 2018 Maine Coastal Islands NWR Maine Coastal Islands NWR Maine Coastal Islands NWR Island Summary Contents Spectacle Island ..........................................................................................................................6 Cross Island ................................................................................................................................7 Scotch Island ...............................................................................................................................9 Outer Double Head Shot Island ................................................................................................. 10 Inner Double Head Shot Island .................................................................................................. 11 Mink Island ............................................................................................................................... 12 Old Man Island ......................................................................................................................... 13 Libby Island .............................................................................................................................. 15 Stone Island & Stone Island Ledge ............................................................................................ 17 Eastern Brothers ....................................................................................................................... -

Global Recognition List August

Accept PTE Academic: pearsonpte.com/accept Africa Egypt • Global Academic Foundation - Hosting university of Hertfordshire • Misr University for Science & Technology Libya • International School Benghazi Nigeria • Stratford Academy Somalia • Admas University South Africa • University of Cape Town Uganda • College of Business & Development Studies Accept PTE Academic: pearsonpte.com/accept August 2021 Africa Technology & Technology • Abbey College Australia • Australian College of Sport & Australia • Abbott School of Business Fitness • Ability Education - Sydney • Australian College of Technology Australian Capital • Academies Australasia • Australian Department of • Academy of English Immigration and Border Protection Territory • Academy of Information • Australian Ideal College (AIC) • Australasian Osteopathic Technology • Australian Institute of Commerce Accreditation Council (AOAC) • Academy of Social Sciences and Language • Australian Capital Group (Capital • ACN - Australian Campus Network • Australian Institute of Music College) • Administrative Appeals Tribunal • Australian International College of • Australian National University • Advance English English (AICE) (ANU) • Alphacrucis College • Australian International High • Australian Nursing and Midwifery • Apex Institute of Education School Accreditation Council (ANMAC) • APM College of Business and • Australian Pacific College • Canberra Institute of Technology Communication • Australian Pilot Training Alliance • Canberra. Create your future - ACT • ARC - Accountants Resource -

2019 Top 200 Kindergarten Through Grade 12 Public and Private Schools by Number of Active SEVIS Records

2019 Top 200 Kindergarten through Grade 12 Public and Private Schools by Number of Active SEVIS Records School Name School Type Total SEVIS IDs in 2019 Archdiocese of Los Angeles Private 1,129 EF International Academy Private 918 Roman Catholic Diocese of Rockville Centre Private 731 CATS Academy Boston Private 659 Fairmont Private Schools Private 613 Montverde Academy Private 531 IMG ACADEMY Private 503 Broadfording Christian Academy Private 490 Archdiocese of Chicago Private 441 North Broward Preparatory School Private 432 American Learning Systems, Inc. Private 370 Keio Academy of New York Private 367 The Village School Private 355 Archdiocese of Philadelphia Private 353 Southlands Christian Schools Private 316 Layton Christian Academy Private 313 THORNTON ACADEMY Private 297 Windermere Preparatory School Private 276 Archdiocese of New York Private 261 St. Johnsbury Academy Private 260 Idyllwild Arts Academy Private 237 Anaheim Discovery Christian Schools Private 237 Diocese of Providence Catholic Schools Private 235 Hoosac School Private 231 Diocese of San Bernardino Private 228 Interlochen Arts Academy Private 227 Roman Catholic Schools of Archdiocese of Newark Private 221 Kent School Private 221 Northfield Mount Hermon Private 218 The Grier School Private 215 Cushing Academy Private 215 Diocese of Bridgeport Private 211 Fei Tian Academy of the Arts Private 210 Archdiocese of Hartford Private 208 Gateway Legacy Christian Academy Private 207 Word of Life Traditional School Private 204 The Culver Academies Private 204 Crean Lutheran -

Schoodic Scenic Byway Corridor Management Plan

SCHOODIC SCENIC BYWAY CORRIDOR MANAGEMENT PLAN Prepared for the Corridor Advisory Group and the Maine Department of Transportation By The Route 1 and Route 186 Corridor Planning Group and The Hancock County Planning Commission With financial assistance from the National Park Service and the Maine Department of Transportation (Printed: 10/04/2000) jhf c:\my documents\transportation\byway\rt1\doc\rt1cmp04.doc CONTENTS SCHOODIC SCENIC BYWAY - CORRIDOR MANAGEMENT PLAN ............................................ 4 SUMMARY ................................................................................................................................................. 4 WHY A BYWAY? WHY THIS BYWAY? ............................................................................................. 5 WHAT’S IT LIKE? TRAVELING THE SCHOODIC HARBOR BYWAY ....................................... 6 A BRIEF HISTORY ................................................................................................................................................. 6 OUR LIGHTHOUSES AND OTHER HIGHLIGHTS .............................................................................................. 8 A GUIDED TOUR .................................................................................................................................................. 10 WHERE ARE WE GOING? A VISION AND GOALS ....................................................................... 23 VISION .................................................................................................................................................................. -

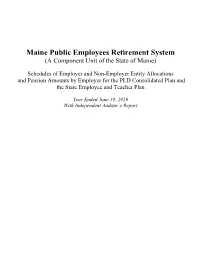

Maine Public Employees Retirement System (A Component Unit of the State of Maine)

Maine Public Employees Retirement System (A Component Unit of the State of Maine) Schedules of Employer and Non-Employer Entity Allocations and Pension Amounts by Employer for the PLD Consolidated Plan and the State Employee and Teacher Plan Year Ended June 30, 2019 With Independent Auditor’s Report MAINE PUBLIC EMPLOYEES RETIREMENT SYTEM SCHEDULES OF EMPLOYER AND NON-EMPLOYER ENTITY ALLOCATIONS AND PENSION AMOUNTS BY EMPLOYER FOR THE PLD CONSOLIDATED PLAN AND THE STATE EMPLOYEE AND TEACHER PLAN Year Ended June 30, 2019 TABLE OF CONTENTS Page Independent Auditor’s Report 1 – 2 Schedules of Employer Allocations and Pension Amounts by Employer for the PLD Consolidated Plan 3 – 25 Schedules of Employer Allocations and Pension Amounts by Employer for the State Employee and Teacher Plan – State Employee Portion 26 – 28 Schedules of Employer Allocations and Pension Amounts by Employer for the State Employee and Teacher Plan – Teacher Portion 29 – 43 Notes to Schedules 44 – 53 INDEPENDENT AUDITOR'S REPORT Board of Trustees of Maine Public Employees Retirement System We have audited the accompanying schedule of employer allocations of the Maine Public Employees Retirement System PLD Consolidated Plan and the schedules of employer and non-employer entity allocations of the Maine Public Employees Retirement System State Employee and Teacher Plan – State Employee Portion and the Maine Public Employees Retirement System State Employee and Teacher Plan – Teacher Portion for the year ended June 30, 2019 (collectively, the schedules of employer allocations), -

Maine State Legislature

MAINE STATE LEGISLATURE The following document is provided by the LAW AND LEGISLATIVE DIGITAL LIBRARY at the Maine State Law and Legislative Reference Library http://legislature.maine.gov/lawlib Reproduced from scanned originals with text recognition applied (searchable text may contain some errors and/or omissions) CONSOLIDATED REPORT NINETY-FOURTH LEGISLATURE Legislative Document No. 1534 H. P. 2073 House of Representatives, April 19, 1949 Reported by Mr. l\farsans from the Committee on Education and printed under Joint Rule No. IO. HARVEY R. PEASE, Clerk STATE OF MAINE IN THE YEAR OF OUR LORD NINETEEN HUNDRED FORTY-NINE RESOLVE, in Favor of Several Academies, Institutes and Seminaries. Appropriation for aid to academies. Resolved: That there be. and hereby is, appropriated. in favor of the several academies, institutes and seminaries hereinafter listed the sum of $33,700 from July I, 1949 to June 30, 1950 and the sum of $33.700 from July I, 1950 to June 30, 1951, said sum to be expended under the direction of the board of trustees of said institutions to the amount indicated. These several amounts are to be taken from the adjustment fund as provided by subsection r I of section 106 of chapter 37 of the re1·ised statutes: Anson Academy $1,900 Aroostook Central lnstitute 800 Berwick Academy I,000 Bridge Academy 500 Bridgewater Classical Academy 700 Bridgton Academy 800 Cherryfield Academy Coburn Classical Institute 1,400 Corinna Union Academy l,000 2 LEGISLATIVE DOCUMENT No. 1534 East Corinth Academy ·l,000 Erskine Academy I,400 Foxcroft