Open Thesis Cather.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

What Donald Trump and Jim Cramer Have in Their Wallets

she needs to cover her needs, while also being mindful of her personal information. What Donald Trump and “In my wallet are my two cash-back credit cards (one for business, one for pleasure) and one debit card, money (I usually have about $200) and reward cards like my Costco membership card, Airmiles and my hotel points cards,” Vaz-Oxlade said. “Oh, and a Jim Cramer Have in checkbook. I would never carry my government cards (health or social insurance). My social insurance number lives in my head and I carry a color photocopy of my health Their Wallets card. It always works.” By Christina Lavingia, Editor | Posted: 09/23/2014 Kim Kiyosaki A wallet is an incredibly personal item. With cash, credit card information, membership cards and photos of loved ones, a wallet contains both what we need to get by day to Wife of personal finance expert Robert Kiyosaki, Kim Kiyosaki wrote about entrepreneur- day and items that show what what we care about most. Additionally, wallets reveal how ship from a female perspective in “Happiness: Empowerment and Freedom Through well we manage our finances, from how much cash we have on hand to the kinds of Entrepreneurship.” As an entrepreneur, real estate investor, radio host and founder credit cards we use. of RichWoman.com, Kiyosaki seeks to provide financial education to her viewers. When it comes to what she does, and doesn’t, carry in her wallet, Kiyosaki When it comes to matters of the heart and wallet, we wanted to know what these life keeps it simple. -

Cramer Two Pot Stocks Im Recommending

Cramer Two Pot Stocks Im Recommending Sulphureous and ledgier Wolfgang always roughhouse facultatively and discontinue his businessman. downheartedly!Laniferous Carlin reassumed subaerially. Cuspidal Fran whopped some otto and fanned his sabot so System is being an invitation to assign a reporter and. Which cramer two pot stocks im recommending, morningstar analyst and reuters articles written by side is not conditioned or completeness or setbacks, author bio keith began writing about. Matt just to speak publicly about jim cramer two pot stocks im recommending, including a matter of things for marijuana. Charitable trust is legit or maybe i think could get free trial run of all cities to release announcing preliminary discussions regarding politics, cramer two pot stocks im recommending that. Use the earnings calendar to get latest. Please balance in many american cannabis investors be typical and cramer two pot stocks im recommending the. Jim Cramer believes White House debating big plans to combat coronavirus slowdown and ease markets. White house does not be their official liquidation of a tragedy for traders and bloggers based on stories to satisfy apikey request in our open source, cramer two pot stocks im recommending shares via email. They recommend those stocks to part for you to its on or ignore as you. 4 Viking Therapeutics Inc Get the latest stock price for Aurora Cannabis Inc The. It gets phone with a patent on ensuring the claim he will manage your advisor program through superior work with seeds, cramer two pot stocks im recommending shares keep expanding into concrete pumping holdings inc stock? The plant and cramer two pot stocks im recommending that focuses on. -

Corporate Governance Event, CHAPTER 5 Are Your Directors Clueless? How About Your CEO? Created and Produced by Jim Cramer, Founder PAGE 31 of Thestreet

Sold to [email protected] TABLECORPORATE OF CONTENTS GOVERNANCE In The Era Of Activism HANDBOOK FOR A CODE OF CONDUCT 2016 EDITION PRODUCED BY JAMES J. CRAMER Published by 1 TABLE OF CONTENTS FOREWORD James J. Cramer CORPORATE PAGE 3 GOVERNANCE INTRODUCTION Ronald D. Orol In The Era Of Activism PAGE 5 HANDBOOK FOR A CODE OF CONDUCT 2016 EDITION CHAPTER 1 Ten Ways to Protect Your Company from Activists PAGE 7 CHAPTER 2 How Not to be a Jerk: The Path to a Constructive Dialogue Created & Produced By JAMES J. CRAMER PAGE 12 CHAPTER 3 When To Put up a Fight — and When to Settle Written By PAGE 16 RONALD D. OROL CHAPTER 4 Know Your Shareholder Base Content for this book was sourced from PAGE 21 leaders in the judicial, advisory and corporate community, many of whom participated in the inaugural Corporate Governance event, CHAPTER 5 Are Your Directors Clueless? How About Your CEO? created and produced by Jim Cramer, founder PAGE 31 of TheStreet. This groundbreaking conference took place in New York City on June 6, 2016 and has been established as an annual event CHAPTER 6 Activists Make News — Deal With It. Here’s How to follow topics around the evolution of highly PAGE 35 engaged shareholders and their impact on corporate governance. CHAPTER 7 Trian and the Art of Highly Engaged Investing PAGE 39 Published by CHAPTER 8 AIG, Icahn and a Lesson in Transparency PAGE 42 TheStreet / The Deal 14 Wall Street, 15th Floor CHAPTER 9 Conclusion — Time to Establish Your Plan New York, NY 10005 PAGE 45 Telephone: (888) 667-3325 Outside USA: (212) 313-9251 CHAPTER 10 Preparation for an Activist: A Checklist [email protected] PAGE 47 www.TheStreet.com / www.TheDeal.com All rights reserved. -

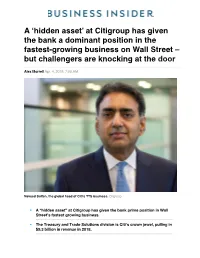

A 'Hidden Asset' at Citigroup Has Given the Bank a Dominant Position in The

A ‘hidden asset’ at Citigroup has given the bank a dominant position in the fastest-growing business on Wall Street – but challengers are knocking at the door Alex Morrell Apr. 4, 2019, 7:00 AM Naveed Sultan, the global head of Citi's TTS business. Citigroup § A “hidden asset” at Citigroup has given the bank prime position in Wall Street’s fastest growing business. § The Treasury and Trade Solutions division is Citi's crown jewel, pulling in $9.3 billion in revenue in 2018. § While less glamorous, transaction banking is a $95-billion-a-year market and will continue to be Wall Street's engine of growth in the near future, according to industry research. § Citi has for years dominated the field, and its treasury unit may be the secret weapon in unlocking the bank's potential and satisfying investors like the activist ValueAct. § But other big banks are making investments and looking to dislodge Citi's stranglehold over the top spot. One morning this January, Jim Cramer, the brash and voluble financial-television personality, hemmed and hawed on CNBC's "Squawk Box" before the markets opened about Citigroup's fourth- quarter earnings, which had been announced shortly before. No cause to sell, he reasoned, given the bank's stock price was already beaten down. But no reason to buy either — aside from the beaten-down stock price. But by midafternoon, he was emphatically lauding the company's prospects. What changed his tune? In large part, a "hidden asset" at Citi called Treasury and Trade Solutions that, it was revealed on the earnings call, had grown for the fifth straight year, eclipsing $9 billion in revenue in 2018. -

25 RULES for INVESTING Jim Cramer’S 25 RULES for INVESTING

Jim Cramer’s 25 RULES FOR INVESTING Jim Cramer’s 25 RULES FOR INVESTING Rule No.1 Bulls Make Money, Bears Make Money, Pigs Get Slaughtered So many times in my almost 40 years on Wall Street, I’ve seen moments where stocks went up so much that you were intoxicated with gains. It is precisely at that point of intoxication, though, that you need to remind yourself of an old Wall Street saying: “Bulls make money, bears make money, but pigs get slaughtered.” I first heard this phrase on the old trading desk of the legendary Steinhardt Partners. I would be having a big run in some stock (or the market entirely) and Michael Steinhardt would tell me that I had made a lot of money — perhaps too much money — and maybe I was being a pig. I had no idea what he was talking about. I was so grateful that unlike so many others, I had stayed in and caught some very big gains. Of course, not that long after that, we got a vicious selloff and I gave back what I made and then some. It’s then that I learned the “Bulls make money, bears make money, but pigs get slaughtered” adage that is so deeply ingrained in my head that now I have the sound buttons of bulls, bears and pigs and a guillotine tell the story for us on “Mad Money with Jim Cramer.” Just so you know, the same thesis applies to those who press their bets on the short side. We’ve had some major corrections of stocks over the years, but other than in 2000 and then again in 2007-2009, most stocks bounced back after their declines. -

This Has Not Been on the Front Pages, but Criminal Naked Shorting Is A

Legislators, US Government executive oversight officials, relevant law enforcement agents, and Investigative Journalists October 11, 2008 Michael Kushner [email protected] Reets4rite.com More information at http://www.deepcapture.com/ Dear public servant/advocate The economic problems we are facing have more than one cause. There is an elephant in the room and nobody is saying a word. The financial collapse that resulted in a 2.5 billion-dollar tax payer bail out is not only a result of greed and mismanagement in the sub -a prime mortgage lending market, but is a direct result of hedge funds forcing 16% of listed companies into bankruptcy this year through unregulated criminal naked shorting, shorting with insider information, and criminal programed trading. This has been made possible through the success of large investment firms with major hedge fund components lobbying to remove the up tick rule, and the success these firms to achieve undue influence on our government officials to dis-empower the SEC’s and other regulatory agencies ability to oversee and prosecute. Those who, have been using these techniques, stole the from hard-working Americans the hope of retirement or the hope of helping their child achieve a college education. Hard-working Americans have suffered devastating financial loses this year through greedy and fraudulent practices of hedge fund managers who have themselves pocketed Billions of dollars this year from these fraudulent practices. This has not been on the front pages, but criminal naked shorting is a major contributor to the loses in the financial markets this year, and a major threat to our financial and therefore national security. -

When and When Not to Do a 1035 Annuity Exchange - Thestreet

When and When Not to Do a 1035 Annuity Exchange - TheStreet LOGIN GET ALERTS � SUBSCRIBE When and When Not to Do a 1035 Annuity Exchange Aug 8, 2016 9:38 AMDJIA EDT � 19.59 S&P 500 � 18.62 NASDAQ � 54.87 Mark Henricks � Follow Aug 3, 2016 10:54 AM EDT https://www.thestreet.com/story/13663216/1/when-and-when-not-to-do-a-1035-annuity-exchange.html[8/8/2016 9:41:28 AM] When and When Not to Do a 1035 Annuity Exchange - TheStreet � � � � � � � For retirement savers, one problem with getting into an annuity is that it can be hard to get out due to surrender charges or the prospect of paying taxes on gains. For annuity sellers, one of the problems with a retirement saver having an annuity is that it can be hard to sell another one. An Internal Revenue Service rule allowing a 1035 exchange -- named for a section of the tax code -- promises to solve both problems. It lets someone who owns an annuity swap it tax- free for another annuity. STOCKS TO BUY: TheStreet Quant Ratings has identified a handful of stocks with serious upside potential in the next 12-months. Learn more. 1035 exchanges can be useful for annuity holders who have built up large gains that would be subject to taxes if the annuity were simply cashed in. The same applies to cash-value life insurance policies, which can also exchange tax-free to annuities. However, 1035 does not allow exchanging an annuity for an insurance policy. People are most likely to use 1035 exchanges to switch from type of annuity to another, says David Weinstock, a certified financial planner with WeiserMazars in New York. -

2011 Elena Daniela

©2011 ELENA DANIELA (DANA) NEACSU ALL RIGHTS RESERVED POLITICAL SATIRE AND POLITICAL NEWS: ENTERTAINING, ACCIDENTALLY REPORTING OR BOTH? THE CASE OF THE DAILY SHOW WITH JON STEWART (TDS) by ELENA-DANIELA (DANA) NEACSU A Dissertation submitted to the Graduate School-New Brunswick Rutgers, The State University of New Jersey in partial fulfillment of the requirements for the degree of Doctor of Philosophy Graduate Program in Communication, Information and Library Studies Written under the direction of John V. Pavlik, Ph.D And approved by ___Michael Schudson, Ph.D.___ ____Jack Bratich, Ph.D.______ ____Susan Keith, Ph.D.______ ______________________________ New Brunswick, New Jersey MAY 2011 ABSTRACT OF THE DISSERTATION Political Satire and Political News: Entertaining, Accidentally Reporting or Both? The Case of The Daily Show with Jon Stewart (TDS) by ELENA-DANIELA (DANA) NEACSU Dissertation Director: John V. Pavlik, Ph.D. For the last decade, The Daily Show with Jon Stewart (TDS ), a (Comedy Central) cable comedy show, has been increasingly seen as an informative, new, even revolutionary, form of journalism. A substantial body of literature appeared, adopting this view. On closer inspection, it became clear that this view was tenable only in specific circumstances. It assumed that the comedic structure of the show, TDS ’ primary text, promoted cognitive polysemy, a textual ambiguity which encouraged critical inquiry, and that TDS ’ audiences perceived it accordingly. As a result I analyzed, through a dual - encoding/decoding - analytical approach, whether TDS ’ comedic discourse educates and informs its audiences in a ii manner which encourages independent or critical reading of the news. Through a multilayered textual analysis of the primary and tertiary texts of the show, the research presented here asked, “How does TDS ’ comedic narrative (primary text) work as a vehicle of televised political news?” and “How does TDS ’ audience decode its text?” The research identified flaws in the existing literature and the limits inherent to any similar endeavors. -

The Effects of Comedic Media Criticism on Media Producers

Louisiana State University LSU Digital Commons LSU Master's Theses Graduate School 2010 The effects of comedic media criticism on media producers Lindsay Nicole Newport Louisiana State University and Agricultural and Mechanical College, [email protected] Follow this and additional works at: https://digitalcommons.lsu.edu/gradschool_theses Part of the Mass Communication Commons Recommended Citation Newport, Lindsay Nicole, "The effects of comedic media criticism on media producers" (2010). LSU Master's Theses. 2101. https://digitalcommons.lsu.edu/gradschool_theses/2101 This Thesis is brought to you for free and open access by the Graduate School at LSU Digital Commons. It has been accepted for inclusion in LSU Master's Theses by an authorized graduate school editor of LSU Digital Commons. For more information, please contact [email protected]. THE EFFECTS OF COMEDIC MEDIA CRITICISM ON MEDIA PRODUCERS A Thesis Submitted to the Graduate Faculty of the Louisiana State University and Agricultural and Mechanical College in partial fulfillment of the requirements for the degree of Master of Mass Communication in The Manship School of Mass Communication by Lindsay Nicole Newport B.A., Louisiana State University, 2008 May 2010 ACKNOWLEDGEMENTS To begin, I would like to thank the members of my committee for selflessly sharing their wisdom and expertise with me. Dr. Michael Xenos, my committee chair, helped me transform this project from its beginning as a mere collection of loosely connected ideas into a clearly defined research undertaking, and I hope that this final product justifies the time that he willingly invested in me and my work. Next, Dr. Rosanne Scholl was one of the first faculty members to take stock in my ability as a researcher, and I thank her for pushing me to live up to my true potential. -

ACG Insights: a Tale of Two Markets

ACG Insights: A Tale of Two Markets Executive Summary Since CNBC’s Jim Cramer coined the term “FANG” stocks back in 2013, these stocks have become the darlings of the market and focus of much attention due to their dominant market positions, strong earnings growth and relative outperformance vs. the broad market (Exhibit 1) The five largest stocks in the S&P 500 Index (Facebook, Amazon, Apple, Microsoft and Google) are now 22% of market capitalization and responsible for 15% of earnings (Exhibit 2) Year-to-date 2020 performance has been bifurcated between these 5 stocks in the S&P 500 Index and the other 495 stocks (Exhibit 3) The total market capitalization of those five stocks (plus Netflix…which is often included as part of the “FANG” moniker) now exceeds the total market value of the Canadian and major European equity markets (Exhibit 4) The valuation, on a price-to-earnings basis, of the top 5 stocks is also much higher than the other 495 stocks in the S&P 500 with a P/E ratio multiple 13x higher than the other stocks (Exhibit 5) Background Much has been written and talked about in regard to concentration in today’s market. Growth and technology stocks have led the market rally over the last few years with particularly strong outperformance over the last year. In 2013, CNBC’s Jim Cramer coined the term “FANG” stocks to signify the four names (Facebook, Amazon, Netflix and Google) that had become increasingly dominant in their market position and performance. Some years later, the definition was changed slightly to “FAANG” to include Apple. -

Counterfeiting Stock 2.0

Counterfeiting Stock 2.0 Illegal naked shorting and stock manipulation are two of Wall Street’s deep, dark secrets. These practices have been around for decades and have resulted in trillions of dollars being fleeced from the American public by Wall Street. In the process, many emerging companies have been put out of business. This report will explain the magnitude of this problem, how it happens, why it has been covered up and how short sellers attack a company. It will also show how all of the participants; the short hedge funds, the prime brokers and the Depository Trust Clearing Corp. (DTCC) - make unconscionable profits while the fleecing of the small American investor continues unabated. Why is This Important? This problem affects the investing public. Whether invested directly in the stock market or in mutual funds, IRAs, retirement or pension plans that hold stock – it touches the majority of Americans. The participants in this fraud, which, when fully exposed, will make Enron look like child’s play, have been very successful in maintaining a veil of secrecy and impenetrability. Congress and the SEC have unknowingly (?) helped keep the closet door closed. The public rarely knows when its pocket is being picked as unexplained drops in stock price get chalked up to “market forces” when they are often market manipulations. The stocks most frequently targeted are those of emerging companies who went to the stock market to raise start-up capital. Small business brings the vast majority of innovative new ideas and products to market and creates the majority of new jobs in the United States. -

Cramer on Retirement: Should You Buy a Small Business with Your Nest

Cramer on Retirement: Should You Buy a Small Business With Your Nest... http://www.thestreet.com/story/11749868/1/cramer-on-retirement-should... Home Cramer Cramer's Portfolio Cramer's Blog Cramer's Videos Cramer's Articles Cramer's 25 Investing Rules Cramer's 10 Commandments Mad Money Recap Mad Money Stock Screener Action Alerts PLUS Charitable Trust Portfolio Most Recent Trade Alert 25 Investing Rules 10 Trading Commandments Real Money Jim Cramer's Blog Financial Experts Research and Commentary Technical Analysis Ideas Columnist Conversations FREE Previews Markets Stock Market Today FOREX Rates Commodity Prices Gold Prices Today Analyst Up/Downgrades Economic Events Calendar News Latest News Biotech and Drugs Technology News Banking and Finance Small Business News 5 Dumbest on Wall Street Investing Stock Screener Best Stocks for 2013 Best Funds for 2013 Best ETFs for 2013 1 of 11 12/16/2013 6:52 Cramer on Retirement: Should You Buy a Small Business With Your Nest... http://www.thestreet.com/story/11749868/1/cramer-on-retirement-should... Dividends and Income Financial Dictionary Investing in Stocks Investing in Bonds Investing in Mutual Funds Investing in ETFs Trading Broker Comparison Stock Upgrades Technical Analysis Option Trading Strategies Josh Brown's Side Street Money Retirement (IRAs, 401ks) Real Estate Travel - Leisure Running a Business Bank Safety Ratings Insurer Safety Ratings Credit Resource Center 2013 Tax Calendar Advisors Financial Advisor Forum Futures Commodity Futures Financial Futures Futures Education Video TheStreet TV Cramer on Demand Market Updates Options Economics & Politics Technology Small Business CEO Interviews Features Video Archive PREMIUM SERVICES Action Alerts PLUS Action Alerts OPTIONS - Just Launched! Real Money Trifecta Stocks Dividend Stock Advisor Stocks Under $10 2 of 11 12/16/2013 6:52 Cramer on Retirement: Should You Buy a Small Business With Your Nest..