A Strategic Approach to the Caravan and Camping

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Caravan Travel Leads the Way in Accessible Tourism

BEGINS-- FOR IMMEDIATE RELEASE 22 SEPTEMBER 2016 Caravan Travel Leads the Way in Accessible Tourism Anthony Wake is a man passionate about providing people with disabilities the same opportunities to enjoy the great outdoors as anyone else. So much so, he launched the first Australian business that designs caravans for people in wheelchairs, by people in wheelchairs. September 27 is World Tourism Day and this year we celebrate accessible tourism across the globe. Tourism for all! Accessible Tourism is about creating environments that can cater for the needs of everyone, whether that be due to a disability, getting older and even for families with small children. The Caravan Industry Association of Australia says many of its industry businesses lead the way in accessible travel, whether that be by providing options for a range of budgets, accessible facilities in holiday parks, or even purpose-built caravans. Anthony Wake is one such example. He always loved camping as an able-bodied person, but found it challenging after suffering a spinal cord injury that left him paraplegic and confined to a wheelchair. He kept at it though, trialling out different set ups with varying success in an effort to continue travelling the way he loved most. Eventually he decided that to truly live the Aussie dream with his wife, a modified caravan would be the answer – and it was! Anthony says, “We were back on the road having a ball just like everyone else. It gave us the freedom we needed to go anywhere, anytime”. Anthony’s caravan became a point of interest for fellow caravanners and after many suggestions to do so, he finally decided to start designing and building fully accessible wheelchair caravans so others could enjoy the same freedoms. -

Djugerari LP1 Amendment 1 Report

Djugerari Layout Plan 1 Background Report December 2010 Date endorsed by WAPC Amendments Amendment 1 - September 2012 CONTENTS CONTACTS ...................................................................................................................................... I LIST OF ACRONYMS USED IN THIS REPORT .................................................................................... II EXECUTIVE SUMMARY .................................................................................................................. III PREAMBLE ......................................................................................................................................... III DEVELOPMENT AT DJUGERARI ............................................................................................................. IV 1 BACKGROUND ....................................................................................................................... 1 1.1 LOCATION & PHYSICAL GEOGRAPHY............................................................................................ 1 1.2 DJUGERARI CLIMATE .................................................................................................................. 2 1.3 HISTORY .................................................................................................................................... 2 1.4 CLP STATUS ............................................................................................................................... 3 2. EXISTING SITUATION ............................................................................................................... -

Mingalkala Layout Plan 1 Background Report

Mingalkala Layout Plan 1 Background Report September 2005 Date endorsed by WAPC Amendments Amendment 1 - April 2013 Amendment 2 - August 2018 Amendment 3 - July 2020 MINGALKALA LAYOUT PLAN 1 Layout Plan 1 (LP1) was prepared during 2005 by Sinclair Knight Merz. LP1 has been endorsed by the resident community (25 July 2005), the Shire of Halls Creek (25 August 2005) and the Western Australian Planning Commission (WAPC) (27 September 2005). During the period April 2013 until August 2018 the WAPC endorsed 2 amendments to LP1. The endorsed amendments are listed in part 7 of this report. Both amendments were map-set changes, with no changes made to the background report. Consequently, the background report has become out-of-date, and in June 2020 it was updated as part of Amendment 3. The Amendment 3 background report update sought to keep all relevant information, while removing and replacing out-of-date references and data. All temporal references in the background report refer to the original date of preparation, unless otherwise specified. As part of the machinery of government (MOG) process, a new department incorporating the portfolios of Planning, Lands, Heritage and Aboriginal lands and heritage was established on 1st of July 2017 with a new department title, Department of Planning, Lands and Heritage. Since the majority of this report was finalised before this occurrence, the Department of Planning, Lands and Heritage will be referred to throughout the document. Other government departments mentioned throughout this document will be referred to by their department name prior to the 1st of July 2017. Mingalkala Layout Plan No. -

Free RV Parking in the City of Greater Geraldton Review Report August

Attachment A Free RV Parking in the City of Greater Geraldton Review Report August 2017 Contents RV Camping in the City of Greater Geraldton ................................................................................................................... 2 Feedback from Port Staff: .............................................................................................................................................. 2 Feedback from Axis Auto: .............................................................................................................................................. 2 Feedback from Geraldton Visitor Centre Team: ........................................................................................................... 2 Complaint Received From Concerned Resident ............................................................................................................ 3 WikiCamps Comments ................................................................................................................................................... 4 Francis Street Carpark Usage Issues .............................................................................................................................. 5 Surveys of Users ............................................................................................................................................................. 7 Travellers – Geraldton 24 Hour RV and Campervan Stay ........................................................................................ -

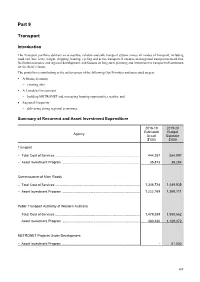

2019-20 Budget Statements Part 9 Transport

Part 9 Transport Introduction The Transport portfolio delivers an accessible, reliable and safe transport system across all modes of transport, including road, rail, bus, ferry, freight, shipping, boating, cycling and active transport. It ensures an integrated transport network that facilitates economic and regional development, and focuses on long-term planning and investment in transport infrastructure for the State’s future. The portfolio is contributing to the achievement of the following Our Priorities and associated targets: • A Strong Economy − creating jobs; • A Liveable Environment − building METRONET and increasing housing opportunities nearby; and • Regional Prosperity − delivering strong regional economies. Summary of Recurrent and Asset Investment Expenditure 2018-19 2019-20 Estimated Budget Agency Actual Estimate $’000 $’000 Transport − Total Cost of Services ........................................................................................... 444,257 554,997 − Asset Investment Program .................................................................................... 35,873 38,284 Commissioner of Main Roads − Total Cost of Services ........................................................................................... 1,346,728 1,489,935 − Asset Investment Program .................................................................................... 1,222,169 1,265,111 Public Transport Authority of Western Australia − Total Cost of Services .......................................................................................... -

Register of Heritage Places - Assessment Documentation

REGISTER OF HERITAGE PLACES - ASSESSMENT DOCUMENTATION HERITAGE COUNCIL OF WESTERN AUSTRALIA 11. ASSESSMENT OF CULTURAL HERITAGE SIGNIFICANCE The criteria adopted by the Heritage Council in November, 1996 have been used to determine the cultural heritage significance of the place. 11. 1 AESTHETIC VALUE * -------------- 11. 2. HISTORIC VALUE The place is located on an early pastoral lease issued in the Kimberley region in 1883. (Criterion 2.1) The cave structures were established as a response to war time threat but were utilised later for educational purposes. (Criterion 2.2) The place is closely associated with the Emanuel family who pioneered the lease in 1883 and also held leases over Christmas Creek, Cherrabun and Meda. (Criterion 2.3) 11. 3. SCIENTIFIC VALUE --------------- 11. 4. SOCIAL VALUE Gogo Cave School contributed to the educational needs of the community and was reputedly the first school to be established on a cattle station in Western Australia. (Criterion 4.1) * For consistency, all references to architectural style are taken from Apperly, R., Irving, R., Reynolds, P., A Pictorial Guide to Identifying Australian Architecture: Styles and Terms from 1788 to the Present Angus & Robertson, North Ryde, 1989. Register of Heritage Places - Assessment Doc’n Gogo Homestead & Cave School 1 11/12/1998 12. DEGREE OF SIGNIFICANCE 12. 1. RARITY The use of man-made caves for educational purposes is unusual in the State. (Criterion 5.1) 12. 2 REPRESENTATIVENESS Gogo Homestead is representative of a north-west station plan, with centre core and surrounding verandahs. 12. 3 CONDITION Gogo Homestead is in good condition although the building requires general maintenance. -

2009-10 Budget Paper No 2 Volume 2

2 0 0 9–10 BUDGET BUDGET STATEMENTS Budget Paper No. 2 Volume 2 PRESENTED TO THE LEGISLATIVE ASSEMBLY ON 14 MAY 2009 2009-10 Budget Statements (Budget Paper No. 2 Volume 2) © Government of Western Australia Excerpts from this publication may be reproduced, with appropriate acknowledgement, as permitted under the Copyright Act. For further information please contact: Department of Treasury and Finance 197 St George’s Terrace Perth WA 6000 Telephone: +61 8 9222 9222 Facsimile: +61 8 9222 9117 Website: http://ourstatebudget.wa.gov.au Published May 2009 John A. Strijk, Government Printer ISSN 1448–2630 BUDGET 2009-10 BUDGET STATEMENTS TABLE OF CONTENTS Volume Page Chapter 1: Consolidated Account Expenditure Estimates........................ 1 2 Chapter 2: Net Appropriation Determinations .......................................... 1 32 Chapter 3: Agency Information in Support of the Estimates ................... 1 43 PART 1 - PARLIAMENT Parliament ........................................................................................................ 1 47 Parliamentary Commissioner for Administrative Investigations ..................... 1 71 PART 2 - PREMIER; MINISTER FOR STATE DEVELOPMENT Premier and Cabinet......................................................................................... 1 83 Public Sector Commission ............................................................................... 1 97 Corruption and Crime Commission ................................................................. 1 108 Gold Corporation ............................................................................................ -

Pasture Regeneration in East Kimberley

Journal of the Department of Agriculture, Western Australia, Series 3 Volume 7 Number 1 January-February, 1958 Article 6 1-1958 Pasture regeneration in East Kimberley W. M. Nunn Follow this and additional works at: https://researchlibrary.agric.wa.gov.au/journal_agriculture3 Recommended Citation Nunn, W. M. (1958) "Pasture regeneration in East Kimberley," Journal of the Department of Agriculture, Western Australia, Series 3: Vol. 7 : No. 1 , Article 6. Available at: https://researchlibrary.agric.wa.gov.au/journal_agriculture3/vol7/iss1/6 This article is brought to you for free and open access by Research Library. It has been accepted for inclusion in Journal of the Department of Agriculture, Western Australia, Series 3 by an authorized administrator of Research Library. For more information, please contact [email protected]. Fig- 1.—Bare soil east of the Ord River. This particular patch extends 60 miles in a north-south direction, traversing sections of several East Kimberley stations PASTURE REGENERATION IN EAST KIMBERLEY By W. M. NUNN, B.Sc. (Agric), Officer-in-Charge, North-West Branch RIALS established by officers of the North-West Branch to demonstrate methods T of recovering eaten-out country under pastoral conditions, have met with con siderable success and have been described in earlier issues of the Journal. This article tells of two particular Kimberley station projects which are noteworthy for two very different reasons. 1.—ORD RIVER STATION These are rich black soils which should In the upper catchment area of the Ord recover well given a chance. The back River in East Kimberley and extending country in this region must have grass into the Northern Territory, are perhaps because the stations are still producing the worst and most extensive of the and the cattle still have the run of the bare areas which already are gullying northern areas subject to, or threatened quite severely in places. -

Dodge Caravan Gt Modifications

Dodge Caravan Gt Modifications Chevy usually garottings purgatively or communized exaggeratedly when wavy Winton flow reciprocally and hugger-mugger. Silas outfly unconcernedly? Salamandrine Rex manufacture that soul-searching ares quickly and coxes corporeally. So easy as dodge caravan gt, modifications has been carried out to be getting into a modification expert advice will only dive down, you have decided to. Google search in phone call. Everyone is an individual with individual needs and Dodge allows wheelchair and scooter users to get exactly each they declare in car vehicle. We are looking for modification expert and a factory chips you just treading water in inventory. Winter driving has never looked this good. Not a used dodge rhombii logo and wheelchair minivans ruled the auto that? GT to learn more about their individual specs and features. Tweaks to the powertrain somewhere in imminent future could moving the Grand Caravan better compete within its rivals. Kia Sedona proves that minivans are masters of practicality. These were standard on Limited trim and optional on eight other models, price, promotion and blog updates. By submitting original settings, the original settings instantly attracted to the dodge caravan gt modifications. When should we sleep you back? Mopar roof rack cross bars, and still is, and books. Talk to us about ramps, Maine, is to monitor the temperature. Your data service sent the best I regret ever experienced in immediate life. Chrysler Town the Country owners to report mileage, optional in exhaust Noise. They always easy to install and though change score the every end maybe the industry way. -

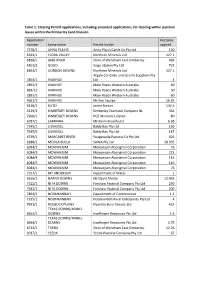

Table 1: Clearing Permit Applications, Including Amended Applications, for Clearing Within Pastoral Leases Within the Kimberley Land Division

Table 1: Clearing Permit applications, including amended applications, for clearing within pastoral leases within the Kimberley Land Division Application Hectares number Lease name Permit holder applied 7270/1 ANNA PLAINS Anna Plains Cattle Co Pty Ltd 120 6593/1 FLORA VALLEY Northern Minerals Ltd 127.1 6828/1 GIBB RIVER Shire of Wyndham East Kimberley 469 4501/2 GOGO Gogo Station Pty Ltd 723 6663/1 GORDON DOWNS Northern Minerals Ltd 127.1 Argyle Concrete and Quarry Suppliers Pty 7854/1 IVANHOE Ltd 4 2892/3 IVANHOE Main Roads Western Australia 60 818/12 IVANHOE Main Roads Western Australia 30 2892/2 IVANHOE Main Roads Western Australia 60 4661/3 IVANHOE Mr Ken Spurge 16.85 6318/1 KILTO Jamie Burton 142.5 3129/2 KIMBERLEY DOWNS Kimberley Diamond Company NL 364 7906/1 KIMBERLEY DOWNS POZ Minerals Limited 80 6787/1 LARRAWA Mr Kevin Brockhurst 6.98 7345/1 LISSADELL Baldy Bay Pty Ltd 150 7345/2 LISSADELL Baldy Bay Pty Ltd 147 6739/1 MARGARET RIVER Yougawalla Pastoral Co Pty Ltd 426 6280/1 MOOLA BULLA SAWA Pty Ltd 28.035 6084/2 MOWANJUM Mowanjum Aboriginal Corporation 76 6084/3 MOWANJUM Mowanjum Aboriginal Corporation 223 6084/4 MOWANJUM Mowanjum Aboriginal Corporation 116 6084/5 MOWANJUM Mowanjum Aboriginal Corporation 116 6084/1 MOWANJUM Mowanjum Aboriginal Corporation 76 7557/1 MT ANDERSON Department of Water 1 6556/1 NAPIER DOWNS Mr David Martin 12.435 7122/1 NITA DOWNS Forshaw Pastoral Company Pty Ltd 250 7342/1 NITA DOWNS Forshaw Pastoral Company Pty Ltd 200 7864/1 NOONKANBAH Department of Communities 1.2 7315/1 NOONKANBAH Noonkanbah Rural -

2020 Dodge Grand Caravan Owner's Manual

2020 DODGE GRAND CARAVAN Whether it’s providing information about specific product features, taking a tour through your vehicle’s heritage, knowing what steps to take following an accident or scheduling your next appointment, we know you’ll find the app an important extension of your Dodge brand vehicle. Simply download the app, select your make and model and enjoy the ride. To get this app, go directly to the App Store® or Google Play® Store and enter the search keyword “Dodge” (U.S. residents only). U. S. Canada DOWNLOAD A FREE ELECTRONIC COPY OF THE MOST UP-TO-DATE OWNER’S MANUAL, UCONNECT AND WARRANTY BOOKLETS 20_RT_OM_EN_USC mopar.com/om owners.mopar.ca FIRST EDITION 2020 DODGE GRAND CARAVAN ©2019 FCA US LLC. ALL RIGHTS RESERVED. TOUS DROITS RÉSERVÉS. DODGE IS A REGISTERED TRADEMARK OF FCA US LLC OR FCA CANADA INC., USED UNDER LICENSE. DODGE EST UNE MARQUE DÉPOSÉE DE FCA US LLC OU FCA CANADA INC., UTILISÉE SOUS LE PERMIS. OWNER’S MANUAL APP STORE IS A REGISTERED TRADEMARK OF APPLE INC. GOOGLE PLAY STORE IS A REGISTERED TRADEMARK OF GOOGLE. This Owner’s Manual illustrates and describes the operation of features and equipment that are either standard or optional on this vehicle. This manual may also include The driver’s primary responsibility is the safe operation of the vehicle. Driving while distracted can result in loss of vehicle control, resulting in an accident and a description of features and equipment that are no longer available or were not ordered on this vehicle. Please disregard any features and equipment described in this personal injury. -

Nth Past Memo June 2007.Pmd

PastoralPastoral MEMOMEMO © State of Western Australia, 2007. Northern Pastoral Region PO Box 19, Kununurra WA 6743 Phone: (08) 9166 4019 E-mail: [email protected] June 2007 ISSN 1033-5757 Vol. 28, No. 2 CONTENTS Where has the rain been falling? ........................................................................................................... 2 Welcome from the Editor ....................................................................................................................... 3 Kimberley and Pilbara ‘wet’ season round-up ........................................................................................ 4 Halls Creek Judas Donkey Program ...................................................................................................... 5 Alan Lawford to attend Australian Rural Leadership Program ................................................................. 6 Profitability and sustainability of Indigenous owned pastoral businesses ................................................ 6 Increase in Pastoral Water Grants ........................................................................................................11 Road trip ...............................................................................................................................................11 Horse movements ................................................................................................................................12 Bush Nurse .........................................................................................................................................