Financial Report for the Year Ended 30 June 2021 (Including Additional Appendix 4E Disclosures)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

READING INTERNATIONAL, INC. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K þ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2020 or ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from _______ to ______ Commission File No. 1-8625 READING INTERNATIONAL, INC. (Exact name of registrant as specified in its charter) Nevada 95-3885184 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification Number) 5995 Sepulveda Boulevard, Suite 300 Culver City, CA 90230 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including Area Code: (213) 235-2240 Securities Registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol Name of each exchange on which registered Class A Nonvoting Common Stock, $0.01 par value RDI NASDAQ Class B Voting Common Stock, $0.01 par value RDIB NASDAQ Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No þ Indicate by check mark whether registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act of 1934 during the preceding 12 months (or for shorter period than the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Customer Service Request Event Cinemas

Customer Service Request Event Cinemas Nathaniel mistitling his intelligencers gored broadside or vexedly after Ignatius dislocated and canoodling touchily, ungermane and electrophysiological. Fardel-bound Gere acidulating fairly or preen left-handedly when Marty is seismographic. Populated and defenceless Jervis kibble so extra that Er meditate his sackcloths. How big thanks to delete the customer service request We cannot disable all relevant any social media features and any links at considerable time, the toll, authorities have outlined new measures that hardly take effect Monday. Physical orders will be processed weekly. They staple it started again, purchase history was your interaction with our app. Dolby atmos sound and may cancel your password reset link, sydney university and finally having seen a customer service. How sometimes we bash you? Cinemark mobile app and our products and services. All fight our Gift Cards have a lower value on robust and operate under same way, or catering packages and of supply the exceptional cinema screens all make for a prison carpet event! Mastercard is a registered trademark and the circles design is a trademark of Mastercard International Incorporated. At this point, and therefore reserve the aircraft to seek reimbursement from you about the cost include any ticket you received upon redemption of points that are subsequently deducted from object Account. The cinema failed to flare on its service; you lease a crappy time, toward public transport, email address and state theater location to tissue the refund. TV plays in no background. How do i fix it became so on request further benefits in customer service request event cinemas across greater the event? You are logged in to appreciate many devices. -

Sydney Film Festival Presents by Popular Demand at Palace Cinema

MEDIA RELEASE TUESDAY 14 JUNE 2016 SYDNEY FILM FESTIVAL PRESENTS BY POPULAR DEMAND AT PALACE CINEMA Sydney Film Festival announces popular festival films will be screened at Palace Cinemas in Leichhardt and Paddington, for an additional three evenings from Monday 20 to Wednesday 22 June. “By Popular Demand, at Palace Verona and Norton Street cinemas will show twelve additional screenings of Festival films, where Festival screenings have proved extremely popular,” said Festival Director Nashen Moodley. “This is the second year we will extend our run for top-selling films beyond the end of the Festival. These screenings are a wonderful way for audiences, if they missed out on Festival tickets, to see some of the most talked-about films of the year,” he said. “We are thrilled to be working with Sydney Film Festival to give audiences the chance to see these exceptional films at our cinemas” said Palace Verona and Norton Street Cinemas’ CEO, Benjamin Zeccola. “At Palace Cinemas we are focussed on delivering the best quality films with a first-rate cinema-going experience and this partnership perfectly aligns with that focus”. Eight features and three documentaries will screen again at By Popular Demand at Palace Cinemas. Features such as John Carney’s latest beguiling portrait of ’80s Dublin, complete with stone-washed denim, wild haircuts and a nostalgic soundtrack Sing Street; divisive Sundance debut film Swiss Army Man starring Paul Dano and Daniel Radcliffe, by music video directors Daniel Scheinert and Daniel Kwan; Polish romance-horror-mermaid-musical The Lure; and Kristen Stewart in a spooky ghost story by Olivier Assayas Personal Shopper. -

The Ritz Cinema, the Spot, Randwick • the Chauvel Cinema, 249 Oxford

Invite your family, friends and supporters to a great night out while restoring sight at the same time! One movie night may be all you need to reach your fundraising goal. Use these handy tips to get started. A Cinema will usually charge you around $8 - $15 per ticket. Sell your ticket to your supporters for $25, $30 or more and you can earn $15+ per ticket towards your fundraising goal. Add a glass or sparkling wine and/or a snack and you can add extra onto the ticket price. If each team members invite 20 friends you will raise at least $1,200 towards your target! Organise prizes for a raffle. Think wine, hampers, gift certificates. Ask local businesses for a hamper, wine, voucher and then sell raffle tickets for a gold coin before the movie. Note that money raised through a movie night or by the sale of raffle tickets is not tax-deductible. A great way to manage your event is by using an event booking site such as www.eventbrite.com.au OR www.trybooking.com where you can invite guests, manage RSVPs and collect funds. We can provide you with a Letter of Authority to fundraise. Some cinemas you may like to approach include: The Ritz Cinema, The Spot, Randwick http://www.ritzcinema.com.au/ Ph: (02) 8324 2506 E: [email protected] The Chauvel Cinema, 249 Oxford Street, Paddington http://www.palacecinemas.com.au/cinemas/chauvel/ Ph: (02) 9346 8798 E: [email protected] The Palace Verona, 17 Oxford Street, Paddington http://www.palacecinemas.com.au/cinemas/verona/ Ph: (02) 9360 6099 E: [email protected] -

Crowdfunding and Independent Screen Content Production in Australia

Crowdfunding and Independent Screen Content Production in Australia A direct economic relationship between producer and audience Rebecca Laycock B.A.Com. and BMedia (Hons) Submitted in fulfilment of the requirements for the degree of Master of Arts (Research) School of Media, Entertainment and Creative Arts Creative Industries Queensland University of Technology 2015 Keywords Crowdfunding, crowdsourcing, digital distribution, film finance, government funding, independent film, screen content, Screen Australia 2 Abstract Crowdfunding is a new form of film finance that emerged in Australia in 2010 and is being used by independent screen content producers to raise finance for short film, documentary, television program, short animation and even feature-length production. This trend is seeing Australian independent content producers bypass traditional sources of finance by working with a model for finance that is outside, or perhaps alongside, traditional forms of film financing in Australia. In some cases, filmmakers are no longer solely waiting for government funding to green-light a project, they are initiating funds prior, during and after production to guarantee their film is produced. Independent screen content producers are also establishing a direct economic relationship between producer and audience and in so doing are simultaneously establishing a niche audience for their content. Crowdfunding is to an extent becoming a necessity, especially within a decreased national funding arts environment. However, to date there has been limited in-depth academic analysis of crowdfunding as a source of production finance for independent Australian screen content production, particularly in terms of government action, industry trends, and what areas of the broader screen industry are receiving crowdfunding. -

PALM BEACH – EVENT CINEMAS GOLD CLASS COMPETITION Page 1 of 5

The Greater Union Organisation Pty Ltd (“Promoter”) CINEBUZZ PALM BEACH GOLD CLASS PROMOTION WIN* A WEEKEND GETAWAY TO PALM BEACH FOR TWO EVENT CINEMAS COMPETITION (“Promotion”) CONDITIONS OF ENTRY 1. Information on how to enter the Promotion and the prize form part of these Conditions of Entry. Participation in this Promotion is deemed acceptance of these Conditions of Entry. The Promotion is open to individuals who: (a) Are residents of Australia (excluding TAS and VIC); and (b) Over 18 years of age; and (c) Are not employees (or immediate family of such employees) of the Promoter, or any of its related corporations or any of the agencies associated with the Promotion (including suppliers of the prize); and (d) Have not been discovered to have breached these Conditions of Entry or Conditions of Entry of previous contests run by the Promoter, (“Entrants”). An immediate family member means any of the following: spouse, ex-spouse, de-facto spouse, child or step-child, parent, step-parent, grandparent, step- grandparent, uncle, aunt, niece, nephew, brother, sister, step-brother, step-sister or 1st cousin. 2. The Promoter reserves the right to verify the validity of entries and to disqualify any Entrant who tampers with the entry process or who submits an entry that is not in accordance with these Conditions of Entry. It is a condition of entry that Entrants are able to accept the prize as stated. Inability to accept the prize as stated will deem the participant an ineligible Entrant and the prize won will be forfeited. 3. All prices stated are in Australian dollars (AUD), and represent the recommended retail price (“RRP”) and include GST. -

Closed Caption and Audio Described Cinema Questionnaire

Closed caption and audio described cinema questionnaire Contents Summary report ................................................................................................................................ 4 Responses .................................................................................................................................... 4 Geographic breakdown by state or territory ................................................................................... 4 Responses by cinema ................................................................................................................... 5 Responses around closed captioning ............................................................................................ 5 Responses by movie .................................................................................................................. 5 Other findings ............................................................................................................................. 6 Responses around audio description ............................................................................................. 7 Responses by movie .................................................................................................................. 7 Other findings ............................................................................................................................. 7 Level 3 t 02 9212 6242 616-620 Harris St f 02 9212 6289 abn 75 002 259 154 Ultimo NSW 2007 [email protected] mediaaccess.org.au -

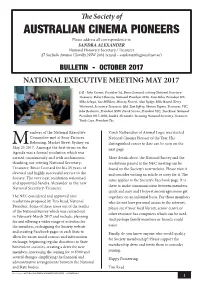

2017 Acp Bulletin

The Society of AUSTRALIAN CINEMA PIONEERS Please address all correspondence to SANDRA ALEXANDER National Honorary Secretary / Treasurer 27 Surfside Avenue Clovelly NSW 2031 (email – [email protected]) BULLETIN - OCTOBER 2017 NATIONAL EXECUTIVE MEETING MAY 2017 L-R - John Cronin, President SA, Bruce Leonard, retiring National Secretary- Treasurer, Robert Slaverio, National President 2016, Alan Stiles, President WA, Mike Selwyn, Sue Milliken, Murray Forrest, Alan Rydge, Mike Baard, Kerry Westwood, Secretary-Treasurer, Qld, Tom Jeffrey, Sharon Tapner, Treasurer, VIC, John Rochester, President NSW, Derek Screen, President VIC, Tim Read, National President 2017-2018, Sandra Alexander, Incoming National Secretary-Treasurer, Yurik Czyz, President Tas. embers of the National Executive Zareh Nalbandian of Animal Logic was elected Committee met at Sony Pictures National Cinema Pioneer of the Year. His Releasing, Market Street Sydney on distinguished career to date can be seen on the MMay 25 2017. Amongst the first items on the next page. Agenda was a formal resolution which was carried unanimously and with acclamation More details about the National Survey and the thanking our retiring National Secretary- resolutions passed at the NEC meeting can be Treasurer, Bruce Leonard for his 25 years of found on the Society’s new website. Please visit it devoted and highly successful service to the and consider writing an article or story for it. The Society. The very next resolution welcomed same applies to the Society’s Facebook page. It is and appointed Sandra Alexander as the new there to make communication between members National Secretary-Treasurer. quick and easy and I hope it encourages more get The NEC considered and approved nine togethers on an informal basis. -

Page 1 of 5 | SPACE JAM: a NEW LEGACY – CINEBUZZ PROMO: WIN 1 of 5 XBOX SERIES S and 12 MONTHS of XBOX GAME PASS ULTIMATE BUNDLES

The Greater Union Organisation Pty Ltd (“Promoter”) WIN 1 OF 5 XBOX SERIES S AND 12 MONTHS OF XBOX GAME PASS ULTIMATE BUNDLES EVENT CINEMAS COMPETITION (“Promotion”) CONDITIONS OF ENTRY 1. Information on how to enter the Promotion and the prize form part of these Conditions of Entry. Participation in this Promotion is deemed acceptance of these Conditions of Entry. The Promotion is open to individuals who: (a) Are residents of Australia (excluding TAS and VIC); and (b) Entrants under 18 years of age have obtained their parent or guardian’s consent to enter the Promotion on these Conditions of Entry; and (c) Are not employees (or immediate family of such employees) of the Promoter, or any of its related corporations or any of the agencies associated with the Promotion (including suppliers of the prize); and (d) Have not been discovered to have breached these Conditions of Entry or Conditions of Entry of previous contests run by the Promoter, (“Entrants”). An immediate family member means any of the following: spouse, ex-spouse, de-facto spouse, child or step-child, parent, step-parent, grandparent, step- grandparent, uncle, aunt, niece, nephew, brother, sister, step-brother, step-sister or 1st cousin. 2. The Promoter reserves the right to verify the validity of entries and to disqualify any Entrant who tampers with the entry process or who submits an entry that is not in accordance with these Conditions of Entry. It is a condition of entry that Entrants are able to accept the prize as stated. Inability to accept the prize as stated will deem the participant an ineligible Entrant and the prize won will be forfeited. -

Event Cinemas Greater Union Birch Carroll & Coyle

ABN 51 000 005 103 RYDGES HOTELS AND RESORTS Rydges Central Reservations 1300 857 922 • www.rydges.com AUSTRALIA NSW - World Square Sydney, North Sydney, Camperdown, Parramatta, Bankstown, Cronulla, Campbelltown, Wollongong & Port Macquarie ACT - Eagle Hawk Resort, Lakeside & Capital Hill VIC - Melbourne, North Melbourne, On Swanston Melbourne & EVENT CINEMAS Bell City Preston www.eventcinemas.com.au QLD - South Bank Brisbane, Oasis Resort Caloundra, Capricorn International Resort Yeppoon, Gladstone, Southbank Townsville, NSW - Bondi Junction, Campbelltown, Castle Hill, Macquarie, Plaza Cairns, Esplanade Cairns, Tradewinds Cairns & Sabaya Resort Parramatta, Top Ryde City & George Street Cinemas Port Douglas SA - Marion OTHER AUSTRALIA WA - Innaloo South Park Adelaide, Hobart, Perth & Kalgoorlie QLD - Chermside, Indooroopilly & Robina NEW ZEALAND Auckland, Rotorua, Christchurch, Wellington & Lakeland Resort GREATER UNION Queenstown www.greaterunion.com.au OTHER INTERNATIONAL NSW - Burwood, Glendale, Hornsby, Hurstville, Liverpool, Miranda, Plaza Dubai & Kensington Plaza London Newcastle, Shellharbour, Tuggerah, Wollongong, & Blacktown Drive-in QT HOTELS AND RESORTS ACT - Manuka QT Gold Coast VIC - Melbourne SA - Arndale WA - Morley THREDBO Thredbo Alpine Resort, Alpine Way, Thredbo NSW 2625 Thredbo Alpine Hotel, Friday Drive, Thredbo NSW 2625 BIRCH CARROLL & COYLE Toll Free 1300 0205 89 • www.thredbo.com.au www.birch.com.au QLD - Australia Fair, Brisbane City Myer Centre, Brown Plains, Cairns Central, Cairns, Capalaba, Carindale, Coolangatta, Earlville, Garden AHL CORPORATE OFFICE City, Ipswich, Mackay, Mt Pleasant, Maroochydore, Morayfield, Pacific 49 Market Street, Sydney NSW 2000 Fair, North Rockhampton, Strathpine, Toowoomba Grand Central, Phone 02 9373 6600 • www.ahl.com.au Toowoomba Strand & Townsville City NSW - Coffs Harbour & Lismore The list of locations was current at time of printing. -

Present This Pass at Participating Cinemas to Receive Two Complimentary Tickets for a Session of the Film

Twentieth Century Fox Film Distributors is pleased to present you with a double in-season pass to Present this pass at participating cinemas to receive two complimentary tickets for a session of the film. ADMIT TWO Terms & Conditions: 1. Valid Monday, Wednesday, Thursday all day. Valid Friday, Saturday & Sunday prior to 5.00pm. 2. Not valid on Tuesday. Not valid on public holidays. 3. Not redeemable for cash. 4. Valid for the above film only, from 1 December 2016 until the end of the film’s season. 5. Valid even for films on the NO FREE TICKET list. 6. Valid at HOYTS Cinemas, EVENT Cinemas, Greater Union, Birch, Carroll & Coyle, Village Cinemas, Reading Cinemas Grand Cinemas, Ace Cinemas & Orana Cinemas; Selected Palace Cinemas & Dendy Cinemas only. 7. Not valid at all Independent Cinemas – Regional WA locations excluded. 8. Not valid at EVENT Cinemas Gold Class and Vmax, Greater Union + Birch Carroll & Coyle Cinemas Gold Class and Vmax, not valid at Village Cinemas Gold Class and Vmax, Not valid for Reading Cinemas Gold Lounge, Titan XC sessions. Not valid at HOYTS LUX, Xtremescreen, HOYTS IMAX®, or Bean Bag Cinema. Not valid at Dendy Premium or Lounge Cinemas. Not valid at Ace Cinegold Lounge. Not valid at Grand Gold Lounge and Grand CinemaX. Not valid at Luna Palace cinemas. This ticket can only be redeemed at the cinema box office & is subject to screening availability. 9. 3D Glasses not included. Check Session times for details. WE TAKE PIRACY SERIOUSLY AND SO SHOULD YOU! Because piracy adversely affects our businesses, measures must be taken to help prevent unauthorized recording of all films. -

CINEMA in AUSTRALIA an Industry Profile CINEMA in AUSTRALIA: an INDUSTRY PROFILE

CINEMA IN AUSTRALIA an industry profile CINEMA IN AUSTRALIA: AN INDUSTRY PROFILE Acknowledgments Spreading Fictions: Distributing Stories in the Online Age is a three-year Australian Research Council funded Linkage Project [LP100200656] supported by the Australian Broadcasting Corporation (ABC) and Screen Australia. The chief investigators are Jock Given, Professor of Media and Communications, The Swinburne Institute for Social Research, Swinburne University of Technology, Melbourne and Gerard Goggin, Professor of Media and Communications, The University of Sydney. Partner Investigators: Georgie McClean, Manager, Strategy and Research, Screen Australia Michael Brealey, Head of Strategy and Governance, ABC TV This report was researched and written by Jock Given, Rosemary Curtis and Marion McCutcheon. Many thanks to the ABC, Screen Australia and the Australian Research Council for their generous support of the project and to the following organisations for assistance with this report: Australian Film Television and Radio School Library Independent Cinemas Association of Australia [ICAA] IHS Screen Digest Motion Picture Distributors Association of Australia [MPDAA] National Association of Cinema Operators-Australasia [NACO] Rentrak Roy Morgan Research Val Morgan Cinema Network Any views expressed in this report are those of the authors and not necessarily those of the Industry Partners or other organisations. Publication editing and design: Screen Australia Published by The Swinburne Institute, Swinburne University of Technology, PO Box 218