Download Full Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bank Details Branch Name IFSC Code Bank Account Number GP

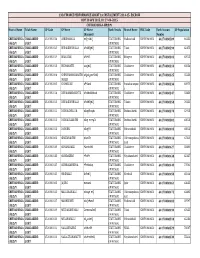

13th FINANCE PERFORMANCE GRANT 1st INSTALLMENT 2014-15- ESCROW RDP 20 GPS 2015, Dt: 27-04-2015 CHITRADURGA-ತದುಗ District Name Taluk Name GP Code GP Name GP Name Bank Details Branch Name IFSC Code Bank Account GP Population (Kannada) Number CHITRADURGA CHALLAKERE- 1510001034 ABBENAHALLI ಅೇನಹ STATE BANK Mallurahalli SBMY0040681 64170488289 64131 -ತದುಗ ಚಳ ೆ ೆ OF MYSORE CHITRADURGA CHALLAKERE- 1510001020 BEDAREDDIHALLI ೇಡ ೆಹ STATE BANK Talak SBMY0040681 64170488290 42475 -ತದುಗ ಚಳ ೆ ೆ OF MYSORE CHITRADURGA CHALLAKERE- 1510001019 BELAGERE ೆಳೆ ೆ STATE BANK Belagere SBMY0040681 64170488303 67013 -ತದುಗ ಚಳ ೆ ೆ OF MYSORE CHITRADURGA CHALLAKERE- 1510001018 BUDNAHATTI ಬುಡಹ STATE BANK Challakere SBMY0040681 64170488314 63534 -ತದುಗ ಚಳ ೆ ೆ OF MYSORE CHITRADURGA CHALLAKERE- 1510001004 CHENNAMMANAGATH ಚನಮಾಗಹ STATE BANK Challakere SBMY0040681 64170488325 55236 -ತದುಗ ಚಳ ೆ ೆ IHALLI OF MYSORE CHITRADURGA CHALLAKERE- 1510001005 CHOWLURU ≥ೌಳ¶ರು STATE BANK Parashurampur SBMY0040681 64170488336 63970 -ತದುಗ ಚಳ ೆ ೆ OF MYSORE a CHITRADURGA CHALLAKERE- 1510001014 DEVARAMARIKUNTE ೇವರಮಕುಂ%ೆ STATE BANK Challakere SBMY0040681 64170488347 53436 -ತದುಗ ಚಳ ೆ ೆ OF MYSORE CHITRADURGA CHALLAKERE- 1510001015 DEVAREDDIHALLI ೇವ ೆಹ STATE BANK Talaku SBMY0040681 64170488358 76151 -ತದುಗ ಚಳ ೆ ೆ OF MYSORE CHITRADURGA CHALLAKERE- 1510001012 DODDACHELLUR ೊಡfi≥ೆಲೂ(ು STATE BANK Doddaullarthi SBMY0040681 64170488370 52928 -ತದುಗ ಚಳ ೆ ೆ OF MYSORE CHITRADURGA CHALLAKERE- 1510001011 DODDAULLARTHI ೊಡfi ಉ+ಾ , STATE BANK Doddaullarthi SBMY0040681 64170488381 63018 -ತದುಗ ಚಳ ೆ ೆ OF MYSORE CHITRADURGA -

Study of Small Schools in Karnataka. Final Report.Pdf

Study of Small Schools in Karnataka – Final Draft Report Study of SMALL SCHOOLS IN KARNATAKA FFiinnaall RReeppoorrtt Submitted to: O/o State Project Director, Sarva Shiksha Abhiyan, Karnataka 15th September 2010 Catalyst Management Services Pvt. Ltd. #19, 1st Main, 1st Cross, Ashwathnagar RMV 2nd Stage, Bangalore – 560 094, India SSA Mission, Karnataka CMS, Bangalore Ph.: +91 (080) 23419616 Fax: +91 (080) 23417714 Email: raghu@cms -india.org: [email protected]; Website: http://www.catalysts.org Study of Small Schools in Karnataka – Final Draft Report Acknowledgement We thank Smt. Sandhya Venugopal Sharma,IAS, State Project Director, SSA Karnataka, Mr.Kulkarni, Director (Programmes), Mr.Hanumantharayappa - Joint Director (Quality), Mr. Bailanjaneya, Programme Officer, Prof. A. S Seetharamu, Consultant and all the staff of SSA at the head quarters for their whole hearted support extended for successfully completing the study on time. We also acknowledge Mr. R. G Nadadur, IAS, Secretary (Primary& Secondary Education), Mr.Shashidhar, IAS, Commissioner of Public Instruction and Mr. Sanjeev Kumar, IAS, Secretary (Planning) for their support and encouragement provided during the presentation on the final report. We thank all the field level functionaries specifically the BEOs, BRCs and the CRCs who despite their busy schedule could able to support the field staff in getting information from the schools. We are grateful to all the teachers of the small schools visited without whose cooperation we could not have completed this study on time. We thank the SDMC members and parents who despite their daily activities were able to spend time with our field team and provide useful feedback about their schools. -

District Census Handbook, Uttara Kannada, Part XII-A, Series-11

CENSUS OF INDIA 1991 Series -11 KARNATAKA DISTRICT CENSUS HANDBOOK UTTARA KANNADA DISTRICT - PART XII-A VILLAGE ANI> TOWN DIRECTORY S08HA ,NAMBISAN Director of Census Operations, Karnataka CONTENTS Pagl: Nu. FORE\VORD \'-\'1 PREFACE' , VII-\'lll IMPORTANT STATISTICS ANAL YTI( 'AL N( )TE xv-xliv \ Section-I • Villa~t! lJirt'ctory Explanatllry Note I-tJ Alphahl:tic:tl List of Villagl:s - Ankol<J, CO,Block 13-15 Village Directory SlaLl..:men! - Ankola CD,Block 16-31 Alphahe~ical List of Villages - Bhatkal CD. Block 35-J() Village Directory Stakml:nl - Bhallal CO.Block Alphah..:tical List of Villages - Haliyal CO,Block 53-5(; VillagL~ Directory Statement - Haliyal CO.Blnck 58-7:'> Alphahdic;;1 List or Villages - Honavar CO.Blnck 79-i-H Villi1ge Oin:ctnry Statement - Honavar CO.Bllll:k 82-105 Alphabetical List or Vilhlges - Karwar CO.Blnck 109-1 LO Village Directory St,;kment - Karwar CO.Blllck 112-119 Alphahdical List or Yillagt.:s - Kumta CO.Block 123~125 Villag~ Directory Statement - Kumta CO.Block 126-149 Alphabetical List of Villages - Mundgod CD.Block 153-155 Village Din:cttlTY Statl.:mcn\ - Munlignu CD.Bluck t56-1(i<) . Alphahdical List of Villag..:s - Siddapur CO.Block 173-177 Village Directory Slatement - Siddapur CD.Block 178-205 Alphabetical List of Villages - Sirsi CO.Blllek 209-2] 4 Village OirL'l'tnry Statement - Sirsi CO.Block 2]6-251 Alphabetical List uf Village!'> - Sura C.D.Blm:k 255-25,1-; \'illagc Din:ctury Statement - Supa CD. Block 260-177 Alph;lbdical List Ill' Villages - Ycllapur C.O.Blm:k 28l-2K4 Village Oirectmy Statement - YdhlPur C.O.Block 286-303 (ii i) Pa~c No. -

Government of Karnataka Directorate of Economics and Statistics

Government of Karnataka Directorate of Economics and Statistics Modified National Agricultural Insurance Scheme - GP-wise Average Yield data for 2012-13 Experiments Average District Taluk Gram Panchayath Planned Analysed Yield Crop : RICE Irrigated Season KHARIF 1 Tumkur 1 Gubbi 1 Marasettyhalli 4 4 2114 2 Mukanahallipatna 4 4 2188 3 Adagoor 4 4 1751 4 Kadaba 4 4 2740 5 Idagoor 4 4 1894 2 Koratagere 6 Thovinakere 4 4 2531 7 Boodagavi 4 4 3613 8 Kuramkote 4 4 3393 9 Bukkapatna 4 4 2622 10 Agrahara 4 4 3371 11 Tumbadi 4 4 2389 12 Hulikunte 4 4 3743 13 Hanchihalli 4 4 3371 Page 1 of 5 Experiments Average District Taluk Gram Panchayath Planned Analysed Yield 3 Kunigal 14 Nademavinapura 4 4 3640 15 Kithanamangala 4 4 3180 16 Baktharahalli 4 4 2760 17 Taredakuppe 4 4 3751 18 Bagenahalli 4 4 3236 19 Kothagere 4 4 2505 20 Madikehalli 4 4 2791 21 Belidevalaya 4 4 2946 22 Herur 4 4 2796 23 Begur 4 4 2489 24 Hosahalli (D) 4 4 1725 25 Huthridurga 4 4 1207 26 Huliyurdurga 4 4 3110 27 Kodavathi 4 4 2999 28 Nidasale 4 4 2508 29 Yadavanne 4 4 2278 30 Jinnagara 4 4 2109 31 Padavagere 4 4 2542 32 Amruthur 4 4 2486 33 Markonahalli 4 4 2141 34 Kodagihalli 4 4 3352 35 Yadiyur 4 4 3196 36 Kaggere 4 4 2994 37 Nagasandra 4 4 3130 4 Madhugiri 38 Hosakere 4 4 2073 39 Kavanadala 4 4 1701 5 Pavagada 40 Dommathamari 4 4 1980 41 Nagalamadike 4 4 3118 42 Ryapate 4 4 3203 43 Palavalli 4 4 2100 44 Kamanadurga 4 4 2632 45 Chikkahalli 4 4 1873 46 Mangalavada 4 4 2910 47 Arasikere 4 4 2012 48 Y N Hosakote 4 2 5810 * 49 Roppa 4 4 2123 Page 2 of 5 Experiments Average District -

Legend Halevuru Kenchanahalli J.I

Village Map of Tumakuru District, Karnataka µ Jalodu Gowdathimmanahalli Nagalapura Kyathaganacharlu Dalavayihalli Bheemanakunte Siddapura Thimmammanahalli Kunihalli Valluru Marammanahalli Chikkahalli Y.N.Hosakote Pothaganahalli Rayacharlu Bettadha Kelaginahalli Vaddarevu Balasamudra Y N HOSAKOTE Hosadurga K.G.Achhammanahalli Hanumanabetta Dalavayihalli Dalavayihalli Thirumani Thippaganahalli Kamanadurga Polenahalli Sasalakunte Soolanayakanahalli Annadanapura Thippaiahanadurga Yarrmmanahalli Kyathaganakere Hosahalli ThimmammanahalliKambalahalli NAGALAMADIKE Meenakuntehalli Hanumanthanahalli K.Sevalapura Kenchammanahalli Sarvatapura Buddareddyhalli Katthikyathanahalli Pennammanahalli Etthinahalli Ryapete Vadanakallu S.I.Rangasamudra Hosahalli Maridasanahalli Budhibetta Kenchiganahalli Dasarammanahalli Bugaduru Honnasamudra Nagalamadike Jadenahalli Rachamaranahalli Upparahalli Obalapura Doddenahalli Shingareddyhalli Gangasagara Pendlijeevi Husenapura Kashipura Thopaganadoddi Shylapura Talemaradahalli Hottebommanahalli Komarlahalli Palavalli Kyathaganahalli Thimmalapura Kanikalabande Kotagudda Srirangapura Madalerahalli Kyadhigunte Nidagallu Bellibatlu Kadapalakere KodigenahalliNyayadhakunte Muddaganahalli Bommanagathihalli AcchammanahalliVeerammanahalli Mummadisagara Siddappanakatte Thimlapura Rangappanahalli Devalakere NIDAGAL HOBALI Bommathanahalli Kadamalakunte Gollanakunte Mugadalabetta Gundlahalli Kondethimmanahalli Aralikunte Budasanahalli HosahalliJangamarahalli Devarabetta Naliganahalli Pavagada Pavagada Dandenahalli Maruru Uddaghatta -

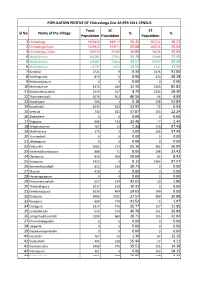

Sl No Name of the Village Total Population SC Population % ST

POPULATION PROFILE OF Chitradurga Dist AS PER 2011 CENSUS Total SC ST Sl No Name of the Village % % Population Population Population 1 Chitradurga 1659456 389117 23.45 302554 18.23 2 Chitradurga-Rural 1329923 333571 25.08 266526 20.04 3 Chitradurga-Urban 329533 55546 16.86 36028 10.93 4 Molakalmuru 141284 27951 19.78 52908 37.45 5 Molakalmuru 125487 25810 20.57 50797 40.48 6 Molakalmuru 15797 2141 13.55 2111 13.36 7 Bandravi 2721 9 0.33 2476 91.00 8 Santhegudda 870 0 0.00 420 48.28 9 Krishnarajapura 0 0 0.00 0 0.00 10 Melinakanive 1474 182 12.35 1265 85.82 11 Bommadevarahalli 2235 107 4.79 1303 58.30 12 Thammenahalli 1076 501 46.56 44 4.09 13 Kanakuppe 564 1 0.18 298 52.84 14 Karadihalli 1039 332 31.95 72 6.93 15 Sirekola 742 281 37.87 165 22.24 16 Swamikere 0 0 0.00 0 0.00 17 Rajapura 696 233 33.48 17 2.44 18 Kelaginakanive 467 11 2.36 455 97.43 19 Malleharavu 275 3 1.09 268 97.45 20 Yerrenahalli 0 0 0.00 0 0.00 21 Jilladagundi 0 0 0.00 0 0.00 22 Pokkurthi 1081 272 25.16 282 26.09 23 Nallareddikondapura 888 71 8.00 208 23.42 24 Obalapura 930 266 28.60 83 8.92 25 Konapura 2423 3 0.12 2364 97.57 26 Bommakkanahalli 832 239 28.73 0 0.00 27 Murudi 478 0 0.00 0 0.00 28 Hosanagalapura 0 0 0.00 0 0.00 29 Pennammanahalli 557 234 42.01 10 1.80 30 Thimmalapura 2017 210 10.41 0 0.00 31 Kerekondapura 1639 404 24.65 149 9.09 32 Rampura 9086 2505 27.57 989 10.88 33 Basapura 660 274 41.52 13 1.97 34 Dadaguru 1314 470 35.77 157 11.95 35 Jambalamalki 525 214 40.76 141 26.86 36 Jahagirbuddenahalli 2299 660 28.71 755 32.84 37 Chinivaladagudda 0 0 0.00 0 -

Davanagere & Chitradurga District

Details of Respective area engineers of BESCOM (Row 2 - District name) (Column 10 - Alphabetical order of Areas) District: Davanagere & Chitradurga Sl Zone Circle Division Sub Division O&M Unit Areas No 1 2 3 4 5 6 7 8 9 10 11 12 Superintending Assistant Executive Assistant Engineer / Junior Name Chief Engineer Name Name Executive Engineer Name Name Engineer Engineer Engineer H I R (EE) I Kulmiye Mohemad Y Guyilalu Rama Jogi Halli Maradi Halli Gollarahatti Kc Koppa Baramapura Post Maradihally Aralikatte Basappana Malige Thondekere Kodi Sri. B.K Subhash Chandra 9448279015 Pura M.K Kote Ramjogi Halli Manbbanakunte Waddy Kere Katappana Hatty Gollahalli Erehalli Myklurahalli Dasanamalige Palavanahalli Sri. B Gurumurthy U (AEE) 94482 79094 08193 229533 Karobana Hatti Burujanaroppa Salahunse Gollarahatti Kovaratti Siddavanahalli Hosanayakanahatti Hopi Boraiahana Badavane Mallappana 9448461466 R G.Thimmarayappa 1 CTAZ DAVANAGERE 08192-2263616 ([email protected]) HY1 Aimangala Oblesh JE 9844552666 Halli Village Imangala Thalavatti Marulayyanamalige T.C.Halli Hale Gollarahatti Guyilalu Giddobanahalli Hosuru Meti Kurke 08194-231466 U ([email protected]) [email protected] Maradidevigere S.G. Halli Thavandi Aladamaradahatti Kenchappanahatti Huluthotlu Devarahatti Adaraalu C.N.Malige D.S.Malige [email protected] 9448279041 .in AAO-Manjappa Bharampura Kc Roppa Mallarasanahatti Kallahatti Gannayakanahalli Mallappanahalli Kariobayyanahalli Salabommanahatti Gulagondayyana DIVISION 9164266042 Halli Mudiyappana Kottige Nagajjana Hatti Harthi Kote Channammana Halli Kapile Hatti Kalavibaagi Alappanahalli Parampara 08193-265536 ZSS No (08193) 220007 (EE) Neerathadi Grama Anagodu Grama Panchaythi Kokkanur , Ganada Katte Load Restriction 10:00Am To 12:00Pm Ulthinakatte Anagodu Sri. B.K Subhash Chandra Revanasiddappa (AEE) Bullapura Narasi Pura Shivapura Nelargi Grama Panchaythi Nerlige Icha Gatta Dodda Rangavvanahalli Ganganakatte Sulthani Pura Chinna Sri. -

Bedkar Veedhi S.O Bengaluru KARNATAKA

pincode officename districtname statename 560001 Dr. Ambedkar Veedhi S.O Bengaluru KARNATAKA 560001 HighCourt S.O Bengaluru KARNATAKA 560001 Legislators Home S.O Bengaluru KARNATAKA 560001 Mahatma Gandhi Road S.O Bengaluru KARNATAKA 560001 Rajbhavan S.O (Bangalore) Bengaluru KARNATAKA 560001 Vidhana Soudha S.O Bengaluru KARNATAKA 560001 CMM Court Complex S.O Bengaluru KARNATAKA 560001 Vasanthanagar S.O Bengaluru KARNATAKA 560001 Bangalore G.P.O. Bengaluru KARNATAKA 560002 Bangalore Corporation Building S.O Bengaluru KARNATAKA 560002 Bangalore City S.O Bengaluru KARNATAKA 560003 Malleswaram S.O Bengaluru KARNATAKA 560003 Palace Guttahalli S.O Bengaluru KARNATAKA 560003 Swimming Pool Extn S.O Bengaluru KARNATAKA 560003 Vyalikaval Extn S.O Bengaluru KARNATAKA 560004 Gavipuram Extension S.O Bengaluru KARNATAKA 560004 Mavalli S.O Bengaluru KARNATAKA 560004 Pampamahakavi Road S.O Bengaluru KARNATAKA 560004 Basavanagudi H.O Bengaluru KARNATAKA 560004 Thyagarajnagar S.O Bengaluru KARNATAKA 560005 Fraser Town S.O Bengaluru KARNATAKA 560006 Training Command IAF S.O Bengaluru KARNATAKA 560006 J.C.Nagar S.O Bengaluru KARNATAKA 560007 Air Force Hospital S.O Bengaluru KARNATAKA 560007 Agram S.O Bengaluru KARNATAKA 560008 Hulsur Bazaar S.O Bengaluru KARNATAKA 560008 H.A.L II Stage H.O Bengaluru KARNATAKA 560009 Bangalore Dist Offices Bldg S.O Bengaluru KARNATAKA 560009 K. G. Road S.O Bengaluru KARNATAKA 560010 Industrial Estate S.O (Bangalore) Bengaluru KARNATAKA 560010 Rajajinagar IVth Block S.O Bengaluru KARNATAKA 560010 Rajajinagar H.O Bengaluru KARNATAKA -

Name and Address of the Blos

Name and Address of the BLOs Name of Assembly Constituency: 97.Molakalmuru Total No. of Parts in the AC: 221 Total No. of BLOs in the AC:221 Part No. Name of the BLO Complete Address of the BLO Contact No. 1 2 3 4 1 B.hanamapura Thejamurthi H.M. GHPS B.Hanumapur 2 Bhandravi Bhadravappa G.P BILL collecter Santhegudda 9449790929 3 Hanumagudda Kumaraswamy G.P Secretry Santhegudda 4 santhegudda R,Devaraj H.M. GHPS Santhegudda 9448149352 5 Melinakanive C.S, Dillipsen V.A. Santhegudda 6 kelaginaknive T,Laksmana H.M. GHPS Kelaginaknive 7 Bommadevarahalli Hulikuntappa A.M GHPS Bommadevarahally 9379126199 8 .Thammenahalli Anjinappa G.P BILL collecter 9343070649 9 Rajapura Anjinappa G.P BILL collecter 9343070649 10 Konapura Vedavasalu G.P Secretry Thammenahally Nallareddikondapura 11 Sridhara S,T V.A.J.B.hally 9482010159 12 Obalapura Sridhara S,T V.A. J.B.hally 9482010159 13 Pakurthi M,Hanumanthappa H.M.GHPS Pakkurthi 14 J.B halli-1 Abdul Azeez G.P,Secretry J,B,hally 15 J.B halli-2 Abdul Azeez G.P,Secretry J,B,hally 16 janbalamalki Vasantha H.M. Jambalamalki 9449271178 17 Vaderahalli Phathimakhan A.M GHPS Voderahally 18 Hasadadaguru Gurushankarappa A.M GHPS Dadaguru 9341825708 19 Basaoura Rudramuniyappa H.M. GHPS Basapura 9449537120 20 Bommakkanahalli M, Renukashwamy H,M,GHPS Bommakkanahally 9449743609 21 muradi Nagarathnamma A.M GHPS Murudi 22 Karadihalli B.D. Srinivas G,P BILL collecte Thammenahally 9019470111 23 Kanakuppe B.D. Srinivas G,P BILL collecte Thammenahally 9019470111 24 Thimmalapura Sridhara chari A.M GHPS Thimlapura 9343070666 25 -

Sl.No. Name and Location of the Nursery Taluk District /Div

DETAILS OF THE LOCATIONS OF PERMANENT FOREST NURSERIES IN THE STATE: Sl.No. Name and Location of the Nursery Taluk District /Division 1 Nagarenahally Hosakote Bangalore (R) - SF 2 Jadigenahally Hosakote Bangalore (R) - SF 3 Guduvanahally Devanahally Bangalore (R) - SF 4 D-Cross Doddaballapura Bangalore (R) - SF 5 Aarsinakunte Nelamangala Bangalore (R) - SF 6 Hulimuthige (Kengal) Ramanagara Bangalore (R) - SF 7 Gubbi Kanakapura Bangalore (R) - SF 8 Marur old Nursery Magadi Bangalore (R) - SF 9 Marur new Nursery Magadi Bangalore (R) - SF 10 RFO Campus Magadi Bangalore (R) - SF 11 Kadugodi (White Field) Bangalore South Bangalore (U) 12 Pattandur (White Field) Bangalore South Bangalore (U) 13 HAL Kempapura Bangalore South Bangalore (U) 14 Somanalli Bangalore South Bangalore (U) 15 BUC Nursery (University Campus) Bangalore South Bangalore (U) 16 Sulikere Nursery, South Bangalore South Bangalore (U) 17 Chandapura Bangalore South Bangalore(U) 18 Gowrenahalli Bangalore South Bangalore(U) 19 Sankey tank bed Bangalore North Bangalore (U) 20 Dollar's colony nursery BDA park Bangalore North Bangalore (U) 21 N.P.K. Nursery Bangalore North Bangalore (U) 22 Nagrur, Dasanapura Bangalore North Bangalore (U) 23 Hebbal tank, Hebbal Bangalore North Bangalore (U) 24 BEL Nursery Bangalore North Bangalore (U) 25 Puttenahalli Bangalore North Bangalore (U) 26 Thalak Challkere Chitradurga -SF 27 Katral Chitradurga Chitradurga -SF 28 Chandravalli Chitradurga Chitradurga -SF 29 Metikurke Hiriyur Chitradurga -SF 30 K.R. Halli Hiriyur Chitradurga -SF 31 Kariyala Hiriyur -

District Irrigation Plan (Dip)

DISTRICT IRRIGATION PLAN (DIP) UTTARAKANNADA DISTRICT KARNATAKA STATE 1 | D I P U K Index Sl no Contents Page NO 1 Introduction 6-7 Components and responsible Ministries /Departments 8-9 District Irrigation Plans (DIPs ) 10 Background 11 Vision and Objective 12 Strategy /Approach 13 Methodology 14 Rationale/Justification statement 15-16 2 CHAPTER -1 General Information district 1.1 District Profile 17 1.2 Brief History of the district 20-24 1.3 Present administrative Profile 24 1.4 Demography 25 1.5 Biomass and Livestock 27 1.6 Agro, Ecology, Climate, Hydrdogy, and topography 28-29 1.7 Land use pattern in uttarakannda 31 1.8 Soil Profile 35 1.9 Soil Erosion and Run off status 41 1.10 Rail Fall 42 1.11 Ground water 43 2 | D I P U K 3 CHAPTER -2 District water Profile 2.1 Area wise, Crop wise irrigation status 50 2.2 Production and productivity of major crops 53 2.3 Irrigation based classification 54 4 CHAPTER -3 3.1 Status of water availability 55 3.2 Status of ground water Availability 56 3.3 Existing type of irrigation 58 5 CHAPTER -4 Water Requirement demand 4.1 Domestic water 59 4.2 Crop water requirement 60 4.3 Livestock water demand 65 4.4 Industrials water demand 66 4.5 Water demand of power generation 67 4.6 Total water demand (Present) of district for various sectors 68 4.6 a Total water Demand of the District for various sectors 69 4.7 Water Budget 70 3 | D I P U K Index Sl no Contents (Table) Page No 1 1.1 District Profile 18 2 1.5 Biomass and Live stock 27 3 1.6 Agro, Ecology, Climate, Hydrology and topography 30 4 1.7 -

Chitradurga Dist.Xlsx

All India Veerashaiva Mahasabha (R.) Bangalore Chitradurga Dist Voters List S.No Reg No/MEM No Name & Address 11Smt Sowmya Angadi Jain Temple Backside,Doddapet Chitradurga Taluk:Chitradurga District:Chitradurga State:Karnataka-577501 Mobile: 24Shri K.B.Ramesh Jain Temple Backside, Doddapet Chitradurga Taluk:Chitradurga District:Chitradurga State:Karnataka-577501 Mobile: 37NagaveniT Jain Temple Backside, Doddapet Chitradurga Taluk:Chitradurga District:Chitradurga State:Karnataka-577501 Mobile: 49VeerannaKN Jain Temple Backside, Doddapet Chitradurga Taluk:Chitradurga District:Chitradurga State:Karnataka-577501 Mobile: 512B M Veena Gumasta Colony, 1st Colony, APMC Road Chitradurga Taluk:Chitradurga District:Chitradurga State:Karnataka-577501 Mobile: 614Shri J.S Tippeswamy Siddeshwara, J.C.R Layout Chitradurga Taluk:Chitradurga District:Chitradurga State:Karnataka-577501 Mobile: 715BasavakumarBM J.M.I.T.Backside, Main Road, 1st Stage, Taralabalu Nagar, Chitradurga Taluk:Chitradurga District:Chitradurga State:Karnataka-577502 Mobile: 817K N Vijaya A.C.S. Complex, Opp: Krishna Nursing Home, Lakshmi Bazzar Chitradurga Taluk:Chitradurga District:Chitradurga State:Karnataka-577501 Mobile: 919 Dr E.C. Thipperudrappa "Guru Basava Krupa" Gumasthara Colony, 2nd Cross, 1st Floor, Near APMC Yard, Lakshmi Bazzar Chitradurga Taluk:Chitradurga District:Chitradurga State:Karnataka-577501 Mobile: 10 21 Leelabasavakumar J.M.I.T.Backside, Main Road, 1st Stage, Taralabalu Nagar Chitradurga Taluk:Chitradurga District:Chitradurga State:Karnataka-577502 Mobile: