Audited Financial Statements

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

NBS 3Rd Quarter Report

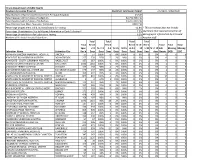

Illinois Department of Public Health Newborn Screening Program Specimen Submission Report 7/1/2018 - 9/30/2018 Total Number of Specimens Received from Perinatal Hospitals 43,345 Total Received within 3 Days of Collection 42,732 (98.6 %) Total Received within 5 Days of Collection 43,297 (99.9 %) Total Received 6 or More Days after Collection 24 (0.1%) Percentage of Specimens Valid and Satisfactory for Testing 92.8% * This percentage does not include Percentage Unsatisfactory Due to Missing Information or Early Collection* 7.0% specimens that required correction of Percentage Unsatisfactory for Laboratory Testing 0.2% demographic information by IDPH and Number of Perinatal Hospital Submitters 121 hospital staff. Total Total Total Total Total Rec'd Rec'd Rec'd % >5- Rec'd Total Total Total Spec. <=3 % <= 3 4-5 % 4-5 % 0-5 >5-14 14 >=14 % >= 14 Lab Missing Missing Submitter Name Submitter City Rec'd Days Days Days Days Days Days Days Days days Unsats DOB DOC ABRAHAM LINCOLN MEMORIAL HOSPITAL LINCOLN 57 57 100% 0 0% 100% 0 0% 0 0% 0 0 0 ADVENTIST BOLINGBROOK HOSPITAL BOLINGBROOK 257 250 97% 5 2% 99% 0 0% 0 0% 0 0 2 ADVOCATE - SOUTH SUBURBAN HOSPITAL HAZELCREST 167 167 100% 0 0% 100% 0 0% 0 0% 0 0 0 ADVOCATE CHRIST MEDICAL CENTER OAK LAWN 1592 1592 100% 0 0% 100% 0 0% 0 0% 2 0 0 ADVOCATE TRINITY HOSPITAL CHICAGO 162 158 98% 4 2% 100% 0 0% 0 0% 0 0 0 ALEXIAN BROS MEDICAL CENTER LAB ELK GROVE VILLAGE 570 557 98% 13 2% 100% 0 0% 0 0% 2 0 0 ALTON MEMORIAL HOSPITAL ALTON 199 197 99% 2 1% 100% 0 0% 0 0% 0 0 0 AMITA HEALTH ADVENTIST MEDICAL CENTER - HHINSDALE 805 801 100% 4 0% 100% 0 0% 0 0% 10 0 0 AMITA HEALTH ADVENTIST MEDICAL CENTER - LLA GRANGE 3 2 67% 1 33% 100% 0 0% 0 0% 0 0 0 AMITA HEALTH-ADVENTIST MEDICAL CENTER - GGLENDALE HEIGHTS 111 107 96% 4 4% 100% 0 0% 0 0% 1 0 0 ANDERSON HOSPITAL MARYVILLE 357 345 97% 12 3% 100% 0 0% 0 0% 0 0 0 ANN & ROBERT H. -

Mark J. Kelly, MD Radiology Subspecialists of Northern Illinois

Mark J. Kelly, MD Radiology Subspecialists of Northern Illinois Primary Specialty Diiagnostiic Radiiollogy Does Not Schedule or Accept New Patients Locatiions Radiology Subspecialists of Northern Illinois 885 Roosevelt Rd Ste 101 Glen Ellyn, IL 60137-6141 22.19 mi 630.384.6200 Radiology Subspecialists of Northern Radiology Subspecialists of Northern Illinois Illinois 7 Blanchard Cir Ste 102 231 S Gary Ave Wheaton, IL 60189-2038 Bloomingdale, IL 60108-2234 630.682.0500 630.286.6573 25.16 mi 25.83 mi Radiology Subspecialists of Northern Radiology Subspecialists of Northern Illinois Illinois 235 S Gary Ave 25 N Winfield Rd Bloomingdale, IL 60108-2213 Winfield, IL 60190-1295 630.893.9600 630.933.4240 25.85 mi 27.61 mi Radiology Subspecialists of Northern Radiology Subspecialists of Northern Illinois Illinois 636 Raymond Dr Ste 106 820 S IL Rte 59 Naperville, IL 60563-9790 Bartlett, IL 60103-1694 630.416.2300 630.213.9600 29.91 mi 30.75 mi Radiology Subspecialists of Northern Radiology Subspecialists of Northern Illinois Illinois 2900 Foxfield Rd 2635 Church Rd Ste 101 St Charles, IL 60174-5799 Aurora, IL 60502-8943 630.377.6500 630.315.6900 33.83 mi 34.61 mi Radiology Subspecialists of Northern Radiology Subspecialists of Northern Illinois Illinois 300 N Randall Rd 2425 Fargo Blvd Geneva, IL 60134-4200 Geneva, IL 60134-3588 630.208.4142 630.232.2200 37 mi 37.16 mi Radiology Subspecialists of Northern Radiology Subspecialists of Northern Illinois Illinois 351 Delnor Dr Ste 201B 905 N 1st St Ste A Geneva, IL 60134-4222 Elburn, IL 60119-9150 630.933.5000 630.232.2200 37.19 mi 43.64 mi Radiology Subspecialists of Northern Radiology Subspecialists of Northern Illinois Illinois 1310 N Main St 2111 Midlands Ct Ste 100 Sandwich, IL 60548-1394 Sycamore, IL 60178-3125 815.758.0000 815.758.0000 54.07 mi 56.49 mi Insurance Accepted Insurance plans are subject to change. -

FY 2020 Proposed Rule Impact File.Xlsx

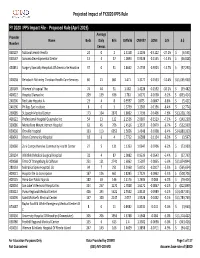

Projected Impact of FY2020 IPPS Rule FY 2020 IPPS Impact File ‐ Proposed Rule (April 2019) Average Provider Name Beds Daily Bills CMIV36 CMIV37 ∆CMI ∆ % ∆ $ Number Census 060107 National Jewish Health 24 0 2 1.5158 1.1036 ‐0.4122 ‐27.2%$ (6,595) 050547 Sonoma Developmental Center 13 4 37 1.0893 0.9338 ‐0.1555 ‐14.3% $ (46,028) 450831 Surgery Specialty Hospitals Of America Se Houston 37 0 31 2.8662 2.4739 ‐0.3923 ‐13.7%$ (97,290) 320038 Rehoboth Mckinley Christian Health Care Services 60 21 861 1.471 1.3177 ‐0.1533 ‐10.4%$ (1,055,930) 150149 Women's Hospital The 74 44 31 1.582 1.4228 ‐0.1592 ‐10.1%$ (39,482) 400022 Hospital Damas Inc 209 139 636 1.781 1.6172 ‐0.1638 ‐9.2%$ (833,414) 240206 Red Lake Hospital A 23 4 8 0.9597 0.875 ‐0.0847 ‐8.8%$ (5,421) 240196 Phillips Eye Institute 8 0 3 1.3739 1.2583 ‐0.1156 ‐8.4%$ (2,774) 260085 St Joseph Medical Center 173 104 2870 1.8602 1.7196 ‐0.1406 ‐7.6%$ (3,228,176) 400122 Professional Hospital Guaynabo Inc 54 13 122 2.1536 2.0007 ‐0.1529 ‐7.1%$ (149,230) 330086 Montefiore Mount Vernon Hospital 63 45 706 1.4516 1.3537 ‐0.0979 ‐6.7%$ (552,939) 050030 Oroville Hospital 133 113 6052 1.5656 1.4648 ‐0.1008 ‐6.4%$ (4,880,333) 460043 Orem Community Hospital 18 6 4 1.7712 1.6588 ‐0.1124 ‐6.3%$ (3,597) 320060 Zuni Comprehensive Community Health Center 27 5 131 1.1353 1.0647 ‐0.0706 ‐6.2%$ (73,989) 250134 Whitfield Medical Surgical Hospital 32 4 87 1.0082 0.9539 ‐0.0543 ‐5.4%$ (37,793) 420068 Trmc Of Orangeburg & Calhoun 251 121 2741 1.6062 1.5207 ‐0.0855 ‐5.3%$ (1,874,844) 280133 Nebraska Spine Hospital, -

Institute for Medical Education at Northwestern Medicine the Institutes at Northwestern Medicine

THE INSTITUTES AT NORTHWESTERN MEDICINE INSTITUTE FOR MEDICAL EDUCATION AT NORTHWESTERN MEDICINE THE INSTITUTES AT NORTHWESTERN MEDICINE INSTITUTE FOR MEDICAL EDUCATION AT NORTHWESTERN MEDICINE The central mission of a medical school is to educate apply for acceptance having shown profound commit- doctors and scientists and prepare them well for roles to ment, perseverance, and unwavering passion, as well provide exceptional care, advance breakthrough science, as the desire to be called a Northwestern University and propel medicine forward for the benefit of people graduate. everywhere. To match that dedication, Northwestern must have the At Northwestern, we are setting the gold standard by resources to provide sufficient financial assistance to ensuring we have the financial means to: ensure access to a Northwestern education. Imagine if • matriculate top candidates to our degree programs; Northwestern could become a Tuition-Free Medical School—if we could select from the very best talent. • attract and recognize faculty dedicated to state-of-the- These students would join the ranks of our alumni, art teaching; and regardless of financial need. Scholarships for medical • advance programs that foster core competencies such students, physical therapists, and others enable us to as patient-centered care, community engagement, compete with other top-tier medical schools. Stipends, effective communication, professional behavior, and a such as support available through the Driskill Integrated desire for continuous learning. Graduate Program, benefit MD-PhD and PhD candidates. And, for physicians seeking clinical or research training Our 16,000+ graduates represent us with distinction through a Fellowship, we must provide stipends for the across the globe. The impact our graduates have on the best trainees to sustain our reputation as a top-tier health and well-being of society is one of Northwestern’s training center. -

Dizziness and Balance Program

Dizziness and Balance Program Rehabilitation Services Dizziness and Balance Program The Dizziness and Balance Program at Northwestern Medicine Central DuPage Hospital and Northwestern Medicine Delnor Hospital is a collaborative program between physicians*, healthcare providers and licensed physical therapists to help patients with balance disorders, dizziness, a history of falling or walking problems. They are dedicated to the treatment and management of dizziness and related balance safety concerns so patients can return to an independent lifestyle. Dizziness symptoms There are many things that can cause dizziness. The important thing is to recognize the symptoms and talk with your physician about getting the cause identified and the disorder treated. The following are some of the more common dizziness symptoms: Unsteadiness or imbalance when walking Vertigo/dizziness Nausea Inability to concentrate * In the spirit of keeping you well-informed, some of the physician(s) and/or individual(s) identified, are neither agents nor employees of Northwestern Memorial HealthCare or any of its affiliates. They have selected our facilities as places where they want to treat and care for their private patients. 1 Rehabilitation Services Common dizziness symptoms (continued): Difficulty reading Sensitivity to noise and bright lights Muscular aches in the neck and back Fatigue Loss of stamina Commonly treated dizziness and balance diagnoses The sensation of dizziness can be debilitating for individuals if left undiagnosed or untreated. Too often, people dismiss the symptoms or are afraid to get a diagnosis when, in fact, most are treatable. For example, one very common cause of dizziness is benign positional paroxysmal vertigo (BPPV). People with BPPV feel like they are spinning when they move or turn their head. -

January 2015 Newsletter

First Illinois HFMA’s First Illinois Chapter Newsletter January 2015 Highlights and Recap First Illinois Chapter Events begin on page 21 News, Events & Updates In This Issue A Message from Joseph J. 1 A Message from Joseph J. Fifer, FHFMA, CPA Fifer, FHFMA, CPA HEALTHCARE FINANCIAL MANAGEMENT ASSOCIATION PRESIDENT AND CEO President’s Message 3 New Year’s Resolutions– 4 I’ve had a song stuck in my head for the past several effort, we established four new Affinity Groups, From HFMA Members to You days. And, as annoying as it can be to have Andy including payer health economics executives, Utilization of Healthcare 6 Williams on a continuous loop, I have to agree with academic medical center CFOs, physician practice Services Special Report him—this really is the most wonderful time of the administrators and value chief strategy officers. Medicare Physician Fee 10 year. From the festivities to the food to the family I am pleased to report that we continue to provide Schedule Announcement: gatherings, there are many reasons to love the holiday An Annual Tug of War? our members with much-needed best practices for season. It’s also a perfect time to take stock of the the ever-changing healthcare industry. This year, we Expanding the Provider Mix; 11 past year and to recognize those who’ve taken this added two new Value Project reports to encompass Transitioning the Use of APRNs journey with us. and Other Physician Extenders value-focused acquisitions and affiliations as well as Three Ways Healthcare 13 Looking back over the past 12 months, it’s clear that physician engagement and alignment. -

Northwestern Memorial Healthcare and Subsidiaries Years Ended August 31, 2017 and 2016 with Reports of Independent Auditors

C ONS OLIDA TED F INANC IA L S TA TE M E NTS Northwestern Memorial HealthCare and Subsidiaries Years Ended August 31, 2017 and 2016 With Reports of Independent Auditors Ernst & Young LLP Northwestern Memorial HealthCare and Subsidiaries Consolidated Financial Statements Years Ended August 31, 2017 and 2016 Contents Report of Independent Auditors.......................................................................................................1 Consolidated Financial Statements Consolidated Balance Sheets ...........................................................................................................3 Consolidated Statements of Operations and Changes in Net Assets ...............................................5 Consolidated Statements of Cash Flows ..........................................................................................7 Notes to Consolidated Financial Statements ....................................................................................8 1710-2430046 Ernst & Young LLP Tel: +1 312 879 2000 155 North Wacker Drive Fax: +1 312 879 4000 Chicago, IL 60606-1787 ey.com Report of Independent Auditors The Board of Directors Northwestern Memorial HealthCare We have audited the accompanying consolidated financial statements of Northwestern Memorial HealthCare and Subsidiaries which comprise the consolidated balance sheets as of August 31, 2017 and 2016, and the related consolidated statements of operations and changes in net assets and cash flows for the years then ended, and the related notes to the consolidated -

The World's Most Active Hospital & Healthcare

The USA's Most Active Hospital & Healthcare Professionals on Social - August 2021 Industry at a glance: Why should you care? So, where does your company rank? Position Company Name LinkedIn URL Location Employees on LinkedIn No. Employees Shared (Last 30 Days) % Shared (Last 30 Days) 1 symplr https://www.linkedin.com/company/symplr/United States 1,101 204 18.53% 2 Covenant Care https://www.linkedin.com/company/covenant-care-corp/United States 509 88 17.29% 3 Johnson & Johnson Consumer Health https://www.linkedin.com/company/johnson-johnson-consumer-health/United States 727 112 15.41% 4 Phreesia https://www.linkedin.com/company/phreesia/United States 1,201 185 15.40% 5 Labcorp Drug Development https://www.linkedin.com/company/labcorpdrugdev/United States 4,362 661 15.15% 6 BrightSpring Health Services https://www.linkedin.com/company/brightspringhealth/United States 17,110 2,500 14.61% 7 Teladoc Health https://www.linkedin.com/company/teladoc-health/United States 3,932 572 14.55% 8 Alto Pharmacy https://www.linkedin.com/company/altopharmacy/United States 749 104 13.89% 9 Quantum Health https://www.linkedin.com/company/quantum-health/United States 899 119 13.24% 10 Imprivata https://www.linkedin.com/company/imprivata/United States 612 78 12.75% 11 American College of Cardiology https://www.linkedin.com/company/american-college-of-cardiology/United States 771 97 12.58% 12 VillageMD https://www.linkedin.com/company/villagemd/United States 862 108 12.53% 13 Oak Street Health https://www.linkedin.com/company/oak-street-health/United States 1,692 211 12.47% 14 ECRI https://www.linkedin.com/company/ecri-org/United States 539 64 11.87% 15 Shields Health Solutions https://www.linkedin.com/company/shields-health-solutions/United States 603 70 11.61% 16 Amwell https://www.linkedin.com/company/amwellcorp/United States 1,104 125 11.32% 17 St. -

Community Health Needs Assessment

Community Health Needs Assessment Northwestern Medicine Huntley Hospital Northwestern Medicine McHenry Hospital Northwestern Medicine Woodstock Hospital Northwestern Medicine Community Health Needs Assessment Northwestern Medicine’s northwest region consists of the following hospitals: Northwestern Medicine Northwestern Medicine Northwestern Medicine Huntley Hospital McHenry Hospital Woodstock Hospital Northwestern Medicine Huntley Hospital, Northwestern Medicine McHenry Hospital, Northwestern Medicine Woodstock Hospital 2 2019 Community Health Needs Assessment Northwestern Medicine Table of contents Introduction . 4 Cancer About Northwestern Memorial HealthCare Respiratory Disease About Northwestern Medicine Huntley Hospital, Diabetes McHenry Hospital and Woodstock Hospital Reproductive Health Acknowledgements Risk Factors Impacting Health Outcomes The Community Health Needs Assessment . 9 Diet & Nutrition Background Physical Activity Goals Overweight and Obesity NM Medicine Huntley Hospital, McHenry Hospital Sexual Health and Woodstock Hospital Community Service Area Sexually Transmitted Diseases Methodology Access to Health Services & Primary Care Providers Primary Data Collection Oral Health Secondary Data Collection Interpreting and Prioritizing Health Needs . 36 Information Gaps Public Dissemination Additional Resources Available to Address Significant Health Needs . 38 Public Comment Prioritization Process of Health Needs . 39 Key Findings . 13 Community Description & Demographics Community Health Needs Assessment Social Determinants -

Authorization to Obtain Confidential Information

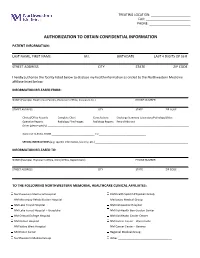

TREATING LOCATION: ______________________ FAX: _________________________ PHONE: _______________________ AUTHORIZATION TO OBTAIN CONFIDENTIAL INFORMATION PATIENT INFORMATION: LAST NAME, FIRST NAME M.I. BIRTHDATE LAST 4 DIGITS OF SS # STREET ADDRESS CITY STATE ZIP CODE I hereby authorize the facility listed below to disclose my health information as circled to the Northwestern Medicine affiliate listed below: INFORMATION RELEASED FROM: NAME (Example: Health Care Facility, Physician’s Office, Insurance Co.) PHONE NUMBER STREET ADDRESS CITY STATE ZIP CODE Clinical/Office Records Complete Chart Consultations Discharge Summary Laboratory/Pathology/Slides Operative Reports Radiology Film/Images Radiology Reports Record Abstract Other (please specify) ______________________________________________________________________________________________________ DATES OF SERVICE FROM _______________________________ TO __________________________________ SPECIAL INSTRUCTIONS (e.g. specific information, lab only, etc.) ___________________________________________________________________ INFORMATION RELEASED TO: NAME (Example: Physician’s Office, Clinic/Office, Department) PHONE NUMBER STREET ADDRESS CITY STATE ZIP CODE TO THE FOLLOWING NORTHWESTERN MEMORIAL HEALTHCARE CLINICAL AFFILIATES: Northwestern Memorial Hospital KishHealth System Physician Group NM Marianjoy Rehabilitation Hospital Marianjoy Medical Group NM Lake Forest Hospital NM Kishwaukee Hospital NM Lake Forest Hospital – Grayslake NM KishHealth Ben Gordon Center NM Central DuPage Hospital NM KishHealth -

Mqii Stakeholders and Collaborators

MQii Stakeholders and Collaborators The Malnutrition Quality Improvement Initiative (MQii) is a project of the Academy of Nutrition and Dietetics, Avalere Health, and other stakeholders who provided guidance and expertise through a collaborative partnership. Support for the MQii is provided by Abbott. Special thanks to the members of the MQii Advisory Committee for their guidance in designing and informing the content of the Toolkit; to the members of the Technical Expert Panel for their guidance in specifying and testing the malnutrition electronic clinical quality measures (eCQMs); and to the members of the MQii Learning Collaborative for their work to implement the MQii Toolkit and eCQMs, and provide feedback to inform revisions and future iterations to MQii tools. MQii Advisory Committee Members Al Barrocas, MD, FACS, FASPEN Bob Blancato, MPA Owner of Alma, LLC President Fellow and Co-Chair of ASPEN’s Value Project Matz, Blancato and Associates (Former Chief Medical Officer of WellStar Atlanta (Former Chair of American Society on Aging, Director of Medical Center, Clinical Professor in the Surgery National Association of Nutrition and Aging Services Departments of LSU and Tulane Schools of Medicine) Programs, and board member for AARP) Member: 2020–Present Member: 2020–Present Charley John, PharmD Leslie Kelly-Hall Director of U.S. Public Policy Founder of Engaging Patient Strategy, Senior Vice Walgreens President of Policy Member of Government Affairs Committee at National Healthwise Association of Specialty Pharmacy Member: 2014–Present -

L. Michael Lee, DO Northwestern Medical Group

L. Michael Lee, DO Northwestern Medical Group Primary Specialty Emergency Mediiciine Secondary Specialties Immediate Care Does Not Schedule or Accept New Patients Locatiions Northwestern Medicine Immediate Care Center - Streeterville 635 N Fairbanks Ct Chicago, IL 60611 0.09 mi 312.472.3173 f 312.472.3176 Northwestern Memorial Hospital Northwestern Medicine Immediate Care Emergency Department Center - River North 211 E Ontario St Ste 200 635 N Dearborn St Ste 100 Chicago, IL 60611 Chicago, IL 60654 312.694.7000 312.694.CARE (2273) 0.12 mi 0.43 mi Northwestern Medicine Immediate Care Northwestern Medicine Immediate Care Center - West Loop Center - South Loop 171 N Aberdeen St Ste 100 1135 S Delano Ct Ste B201 Chicago, IL 60607 Chicago, IL 60605 312.926.4150 312.694.2500 1.83 mi 1.91 mi 1.83 mi 1.91 mi Northwestern Medicine Immediate Care Northwestern Medicine Immediate Care Center - Lakeview Center - Evanston 1333 W Belmont Ave Ste 100 1704 Maple Ave Ste 100 Chicago, IL 60657 Evanston, IL 60201-3134 312.694.CARE (2273) 312.694.CARE (2273) 3.77 mi 11.17 mi Northwestern Medicine Immediate Care Northwestern Medicine Immediate Care Center - Glenview Center - Deerfield 2701 Patriot Blvd Ste 110 350 S Waukegan Rd Ste 150 Glenview, IL 60026 Deerfield, IL 60015 847.475.CARE (2273) 847.475.CARE (2273) 17.83 mi 20.52 mi Northwestern Medicine Immediate Care Northwestern Medicine Immediate Care Center – Glen Ellyn Center - Wheaton 885 E Roosevelt Rd Ste 100 7 Blanchard Cir Ste 102 Glen Ellyn, IL 60137-6141 Wheaton, IL 60189 630.384.6200 630.682.0500