Financial Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Appendix II - K Tsuen Wan District Summaries of Written/Oral Representations

K. Tsuen Wan District - 186 - K. Tsuen Wan District Appendix II - K Tsuen Wan District Summaries of Written/Oral Representations Item No.* DCCAs Representations EAC’s Views No. W O 1 All 1 - Supports the provisional The supporting view is noted. DCCAs recommendations on all DCCAs of the Tsuen Wan District. 2 All 2 - (a) Object to re-arranging the Items (a) and (b) DCCAs order of the DCCA codes These proposals are not as it will cause confusion accepted because: to electors. It may also discourage electors from (i) allocating codes to voting and increase the DCCAs is for the sake of chance of casting the votes easy identification of wrongly. DCCAs on the boundary maps and providing the (b) Propose to assign new public with a quicker and easier way in locating the codes to newly created DCCAs only, for example, DCCA(s) which they are looking for. According the DCCA code for the to the established new K03 (Tsuen Wan working principles, when South) should be K19. drawing up the provisional recommendations, the EAC will rationalise the allocation of the DCCA codes for all administrative districts by assigning the codes in a clockwise direction with a view to making the DCCAs with consecutive codes contiguous to each other as far as possible, so that it is easier for the public to locate the * W: Number of written representations. O : Number of oral representations. K. Tsuen Wan District - 187 - K. Tsuen Wan District Item No.* DCCAs Representations EAC’s Views No. W O DCCA(s); (ii) the DCCA codes are not directly related to electors’ voting; and (iii) there is a representation supporting the rationalisation of DCCA codes. -

Hong Kong Monthly

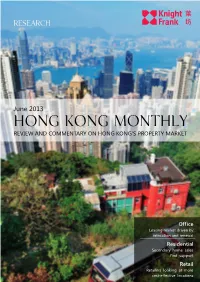

Research June 2013 Hong Kong Monthly REVIEW AND COMMENTARY ON HONG KONG'S PROPERTY MARKET Office Leasing market driven by relocation and renewal Residential Secondary home sales find support Retail Retailers looking at more cost-effective locations1 June 2013 Hong Kong Monthly Market in brief The following table and figures present a selection of key trends in Hong Kong‟s economy and property markets. Table 1 Economic indicators and forecasts Latest 2013 Economic indicator Period 2011 2012 reading forecast GDP growth Q1 2013 +2.8% +4.9% +1.4% +3.0% Inflation rate Apr 2013 +4.0% +5.3% +4.1% +4.4% Feb 2013- Unemployment 3.5%# 3.4% 3.1% 3.2% Apr 2013 Prime lending rate Current 5.00–5.25% 5.0%* 5.0%* 5.0%* Source: EIU CountryData / Census & Statistics Department / Knight Frank # Provisional * HSBC prime lending rate Figure 1 Figure 2 Figure 3 Grade-A office prices and rents Luxury residential prices and rents Retail property prices and rents Jan 2007 = 100 Jan 2007 = 100 Jan 2007 = 100 250 190 350 230 170 300 210 190 150 250 170 130 150 200 130 110 150 110 90 90 100 70 70 50 50 50 2007 2008 2009 2010 2011 2012 2013 2007 2008 2009 2010 2011 2012 2013 2007 2008 2009 2010 2011 2012 2013 Price index Rental index Price index Rental index Price index Rental index Source: Knight Frank Source: Knight Frank Source: Rating and Valuation Department / Knight Frank Note: Provisional figures from Oct 2012 to Mar 2013 2 2 KnightFrank.com.hk Monthly review Property sales were quiet in May, due to the implementation of the Double Stamp Duty on all property sectors in February and the Residential Properties (First-hand Sales) Ordinance on the residential sector in April. -

CT Catalyst Air Purification Service Job Reference of Residence

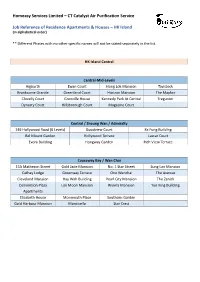

Homeasy Services Limited – CT Catalyst Air Purification Service Job Reference of Residence Apartments & Houses – HK Island (in alphabetical order) ** Different Phases with no other specific names will not be stated separately in the list. HK Island Central Central-Mid-Levels Aigburth Ewan Court Hong Lok Mansion Tavistock Branksome Grande Greenland Court Horizon Mansion The Mayfair Clovelly Court Grenville House Kennedy Park At Central Tregunter Dynasty Court Hillsborough Court Magazine Court Central / Sheung Wan / Admiralty 149 Hollywood Road (6 Levels) Goodview Court Ka Fung Building Bel Mount Garden Hollywood Terrace Lascar Court Evora Building Hongway Garden Rich View Terrace Causeway Bay / Wan Chai 15A Matheson Street Gold Jade Mansion No. 1 Star Street Sung Lan Mansion Cathay Lodge Greenway Terrave One Wanchai The Avenue Cleveland Mansion Hay Wah Building Pearl City Mansion The Zenith Convention Plaza Lok Moon Mansion Riviera Mansion Yue King Building Apartments Elizabeth House Monmouth Place Southorn Garden Gold Harbour Mansion Monticello Star Crest Happy Valley / East-Mid-Levels / Tai Hang 99 Wong Nai Chung Rd High Cliff Serenade Village Garden Beverly Hill Illumination Terrace Tai Hang Terrace Village Terrace Cavendish Heights Jardine's Lookout The Broadville Wah Fung Mansion Garden Mansion Celeste Court Malibu Garden The Legend Winfield Building Dragon Centre Nicholson Tower The Leighton Hill Wing On Lodge Flora Garden Richery Palace The Signature Wun Sha Tower Greenville Gardens Ronsdale Garden Tung Shan Terrace Hang Fung Building -

Financial Review

REVIEW OF OPERATIONS Financial Review TURNOVER PROFIT ATTRIBUTABLE TO SHAREHOLDERS Turnover for the Group for the year ended 31 HK$ MILLION December 2001 increased by 58% to HK$5,036 1,575 million (2000: HK$3,196 million). Turnover from both 1,600 rental and sales registered increases during the year. 1,400 Gross property sales income increased from 1,203 1,233 HK$1,664 million in 2000 to HK$3,159 million in 1,200 2001. Property rental income also increased to 1,000 HK$885 million (2000: HK$820 million) whilst 728 income from warehouse and logistics amounted to 800 HK$744 million (2000: HK$481 million). The 600 396 Group’s hotel operations contributed HK$204 million 400 to turnover during the year (2000: HK$176 million). 200 BREAKDOWN OF KPL’S TOTAL TURNOVER 0 HK$ MILLION 1997 1998 1999 2000 2001 5,500 5,036 decrease in the Group’s earnings in 2001 is due to losses incurred from the sales of Ocean Pointe, Kerry 5,000 Everbright City, Yuen Long 2 warehouse and a 4,500 specific provision of HK$360 million in respect of its 3,159 Constellation Cove project in Tai Po Kau. The Group’s 4,000 75% share of the provision amounted to HK$270 3,500 3,054 3,196 million. The Group also recorded a profit of 2,907 approximately HK$112 million from the disposal of 3,000 its 19.6% interest in the Hu-Ning Expressway in 1,664 2,500 2,342 December 2001. 1,921 1,747 2,000 44 FUNDING AND FINANCING 1,238 426 1,500 55 In order to achieve better control of treasury 410 318 74 47 operations and lower the average cost of funds, KPL 1,000 63 71 204 176 402 410 356 has centralised funding for all its operations at the 11 35 500 Group level. -

M / SP / 14 / 173 Ser Res

¬½á W¤á 300 200 Sheung Fa Shan LIN FA SHAN Catchwater flW˘§⁄ł§¤‚˛†p›ˇ M / SP / 14 / 173 Ser Res 200 w 200 SEE PLAN REF. No. M / SP / 14 / 173 NEEDLE HILL 532 FOR TSUEN WAN VILLAGE CLUSTER BOUNDARIES 500 è¦K 45 Catchwater fih 400 Catchwater 400 2 _ij 100 flW˘§⁄ł§¤‚˛†p›ˇ M / SP / 14 / 172 The Cliveden The Cairnhill JUBILEE (SHING MUN) ROUTE RESERVOIR ê¶È¥ Catchwater «ø 314 Yuen Yuen 9 SEE PLAN REF. No. M / SP / 14 / 172 Institute M' y TWISK Wo Yi Hop 46 23 22 10 FOR TSUEN WAN VILLAGE CLUSTER BOUNDARIES Ser Res 11 SHING MUN ROAD 200 Catchwater 300 Ser Res 3.2.1 Á³z² GD„‹ HILLTOP ROAD ãÅF r ú¥OªÐ e flA Toll Gate t 474 a Kwong Pan Tin 12 w h San Tsuen D c ù t «ø“G a C ¥s 25 SHEK LUNG KUNG ƒ Po Kwong Yuen –‰ ú¥Oª LO WAI ROAD ¶´ú 5 Tso Kung Tam Kwong Pan Tin «ø Tsuen “T Fu Yung Shan ƒ SAMT¤¯· TUNG UK ROAD 5 Lo Wai 14 20 Sam Tung Uk fl” 22 ø–⁄ U¤á 315 24 Resite Village 300 Ha Fa Shan ROAD ¥—¥ H¶»H¶s s· CHUN Pak Tin Pa 8 Cheung Shan 100 fl” 19 San Tsuen YI PEI 400 fl´« TSUEN KING CIRCUIT San Tsuen 13 Estate 100 5 ROAD Allway Gardens flW˘ 100 3.2.2 fl”· SHAN 3 ROAD fi Tsuen Wan Centre FU YUNG SHING 25 ˦Lª MUN Ser Res 28 Chuk Lam Hoi Pa Resite Village ST Tsuen King Sim Yuen 252 ¤{ ON YIN Garden G¤@ G¤@« Ma Sim Pei Tsuen Łƒ… “T» Yi Pei Chun Lei Muk Shue 2 SHING MUN TUNNEL »» 26 Sai Lau Kok Ser Res Ser Res CHEUNG PEI SHAN ROAD Estate w ¥—¥ Tsuen Heung Fan Liu fl MEI WAN STREET 21 Pak Tin Pa M©y© ROAD «ø“ ·wƒ Tsuen 12 MA SIM PAI Lower Shing Mun Ser Res 18 Village «ø“ flw… 7 TSUEN KING CIRCUIT A ⁄· fi¯ł «ø“ƒ¤ Tsuen Tak ¤{ 200 ½ Shing Mun Valley W¤ª Garden -

List of Buildings with Confirmed / Probable Cases of COVID-19

List of buildings with confirmed / probable cases of COVID-19 List of residential buildings in which confirmed / probable cases have resided (Note: The buildings will remain on the list for 14 days since the reported date) Related confirmed / probable District Building name case number Wan Chai St. Regis Hong Kong 230, 264 Eastern Hang Tsui Court, Tsui Ying House 238, 268 Yuen Long Yiu Foo House, Tin Yiu Estate 258, 259 Wan Chai Block A, Viking Villas 260 Central & Western Shun On Building, 2 Sands Street 261 Kowloon City Cheong Shing Court 262 Kwai Tsing Yam Heng House, Shek Yum Estate 263 Wan Chai Sakura Court 264 Central & Western Silvercrest, 24 Macdonnell Road 265 Southern Repulse Bay Garden 266 Central & Western SOHO 189 267 Eastern Block Q, Kornhill 269 Sham Shui Po Block 23, Phase 1, Mei Foo Sun Cheun 270 Island Tower 12, Caribbean Coast 271 Yau Tsim Mong Block 4, Prosperous Garden 272 Yau Tsim Mong Block B, Hoi Lam House, Hoi Fu Court 273 Kwun Tong Dorsett Kwun Tong 274 Wong Tai Sin Block 2, Kai Tak Garden 275 Wan Chai Hang Shun Mansions 276 Wan Chai 307 Jaffe Road 277 Wan Chai Tagus Residences 278 Islands Woodland Court, Parkvale Village 279 Central & Western Chi Residences 120 281 Central & Western 208 Hollywood Road 282 Southern L'Hoel Island South 283 Sha Tin Block 6, Bayshore Towers 284 1 Related confirmed / probable District Building name case number Yau Tsim Mong Tower 7, The Long Beach 285 Sai Kung Pak Kong Au Road 286 Tsuen Wan Indi Home 287 Kwai Tsing On Hoi House, Cheung On Estate 287 Eastern Block 6, Provident Centre -

Development Name 樓宇名稱lot No. 地段編號parent Co. Or Holding Co

List of Consents to Sell, Consents to Assign and Approvals of Deeds of Mutual Covenant issued since 01/01/1994 (As at 31/08/2021) 自一九九四年一月一日所批出的樓花同意書、轉讓同意書及公契批核書列表 (截至2021年8月31日) Development Name Lot No. Parent Co. or Holding Co./ Type of Consent/Approval Solicitors Consent/ 樓宇名稱 地段編號 Developer 同意書/批核公契種類 律師 Approval Date 發展商母公司或控股公司/ 同意書/ 發展商 批核公契日期 Tsuen Wan 荃灣區 Allway Gardens (Commercial TWTL 236 & Ext Goldhill Investments Limited Approval of Sub-Deed of Woo, Kwan, Lee & 18/12/2007 Development) 荃灣市地段第236號及增批 Mutual Covenant and Lo 荃威花園 (商業樓宇) 部分 Management Agreement 胡關李羅律師行 批核附屬公契及管理協議 Allway Gardens (Non- TWTL 236 & Ext Max Rainbow Enterprise Approval of Sub-Sub-Deed of Wilkinson & Grist 09/05/2013 residential Development) - 荃灣市地段第236號及增批 Limited Mutual Covenant 高露雲律師行 portions of the Commercial 部分 彩麗企業有限公司 批核補充附屬公契 Development comprising G/F & 2/F of Phase 1 and G/F & Cockloft Floor of Phase 2 荃威花園 (非住宅樓宇) - 部分 商業樓宇包括第1期地下及1樓, 第2期地下及閣樓 Anglers' Bay Lot 214 in DD 387 Sino Approval of Deed of Mutual Denton Wilde Sapte 23/05/2003 海雲軒 丈量約份第387約地段第 信和/ Covenant and Management 丹敦浩國際律師事務 214號 Prime Force Limited Agreement 所 弘雄有限公司 批核公契及管理協議 Anglers' Bay Lot 214 in DD 387 Sino Consent to Sell for Denton Wilde Sapte 30/05/2003 海雲軒 丈量約份第387約地段第 信和/ residential development 丹敦浩國際律師事務 214號 Prime Force Limited 住宅預售樓花同意書 所 弘雄有限公司 Bellagio Lot 269 RP in DD 390 Wheelock Approval of Deed of Mutual Slaughter & May 26/06/2002 碧堤半島 丈量約份第390約地段第 會德豐/ Covenant and Management 司力達律師樓 269號之餘段 Salisburgh Company Limited Agreement 批核公契及管理協議 Bellagio (Phase -

List of Buildings with Confirmed / Probable Cases of COVID-19

List of Buildings With Confirmed / Probable Cases of COVID-19 List of Residential Buildings in Which Confirmed / Probable Cases Have Resided (Note: The buildings will remain on the list for 14 days since the reported date.) Related Confirmed / District Building Name Probable Case(s) Sha Tin Block 1, La Costa 5915 Block 2, Lotus Tower, Kwun Tong Garden Kwun Tong 5916 Estate Tai Po Po Sam Pai Village 5917 Kowloon City Duchy Heights 5918 Kowloon City Duchy Heights 5919 Eastern Tower 8, Pacific Palisades 5920 Sham Shui Po Ping Yuen, Yau Yat Chuen 5921 Kowloon City Block C, On Lok Factory Building 5922 Kwai Tsing On Hoi House, Cheung On Estate 5923 Yau Tsim Mong Skyway Mansion 5924 Kowloon City Block C, On Lok Factory Building 5925 Sha Tin Kau To Village 5927 Kowloon City 61 Maidstone Road 5928 Kowloon City The Palace 5929 Kwai Tsing Tower 3A, Phase 1, Tierra Verde 5930 Eastern Tsui Shou House, Tsui Wan Estate 5931 Tuen Mun Lok Sang House, Kin Sang Estate 5932 Sham Shui Po Man Lok House, Tai Hang Sai Estate 5933 Yau Tsim Mong Lee Kwan Building 5934 Wan Chai Wing Way Court 5935 Eastern Hang Ying Building 5936 Sai Kung Block 2, Radiant Towers 5937 Central & Western 23 Wilmer Street 5938 Yau Tsim Mong Block 4, Metro Harbour View 5939 Kwun Tong Chi Tai House, On Tai Estate 5940 Kowloon City Tower 2, K City 5941 Tuen Mun Block 6, Po Tin Estate 5943 Yau Tsim Mong Wai Fat Building 5944 Tsuen Wan Tak Tai Building 5945 Sham Shui Po Tower 2, Nob Hill 5946 1 Related Confirmed / District Building Name Probable Case(s) Tsuen Wan Tower 6, Bellagio 5947 -

List of Buildings with Confirmed / Probable Cases of COVID-19

List of Buildings With Confirmed / Probable Cases of COVID-19 List of Residential Buildings in Which Confirmed / Probable Cases Have Resided (Note: The buildings will remain on the list for 14 days since the reported date.) Related Confirmed / District Building Name Probable Case(s) Islands Hong Kong SkyCity Marriott Hotel 11101 North Block 6, Belair Monte 11105 Kowloon City iclub Ma Tau Wai Hotel 11106 Central & Western Lan Kwai Fong Hotel@ Kau U Fong 11107 Wan Chai Best Western Hotel Causeway Bay 11108 Kowloon City Metropark Hotel Kowloon 11109 Kwun Tong IW Hotel 11110 Kwai Tsing Dorsett Tsuen Wan Hong Kong 11111 Eastern Ramada Hong Kong Grand View 11112 Kowloon City iclub Ma Tau Wai Hotel 11113 North Block 1, Dawning Views 11114 Islands Block 1, Coastal Skyline 11115 Central & Western Lan Kwai Fong Hotel@ Kau U Fong 11116 Central & Western Sing Fai Building 11118 Eastern Hoi Sing Mansion, Taikoo Shing 11120 Eastern Hoi Sing Mansion, Taikoo Shing 11121 Sai Kung Tak On House, Hau Tak Estate 11123 Sham Shui Po 15 Fuk Wing Street 11124 Kowloon City iclub Ma Tau Wai Hotel 11125 Yau Tsim Mong Dorsett Mongkok, Hong Kong 11127 Kwai Tsing Block 1, Regency Park 11128 Central & Western True Light Building 11129 Islands Hong Kong SkyCity Marriott Hotel 11130 Central & Western Yukon Court 11131 Central & Western Bishop Lei International House 11132 Central & Western 40 Conduit Road 11132 Sham Shui Po 15 Fuk Wing Street 11133 Central & Western May Tower I 11134 Kwai Tsing Yat King House, Lai King Estate 11135 Central & Western Yip Cheong Building, -

List of Projects Used in HKIA/ARB Professional Assessment 2007 - 2013

List of projects used in HKIA/ARB Professional Assessment 2007 - 2013 Date of Occupation No Year Name of Company Project Title Address Lot No BD File Ref. Permit / Practical Special Topic Completion (month/year) 1 2007 Aedas Ltd Satellite Earth Station Dai Hei Street at Tai Po Industrial Estate Section G Tai Po Town Lot BD 2/9141/01 (P) Jan 04 IL7076, IL7077, IL971, IL970 Proposed Hotel Development at 31E - 39 Wyndham 31E, 31F, 33-39 Wyndham Street, 2 2007 AGC Design Ltd SARP, IL970RP, BD3/2058/94 PT IV Jul 04 Street, Central Central, Hong Kong IL970SBSS1 RP Extension to the Church of Jesus Christ of Latter Day Tseung Kwan O Lot 45, Area II, Po Lam 3 2007 Aedas Ltd Tseung Kwan O Lot 45 BD 9106/04 31 Oct 2006 Saints at Tseung Kwan O Lane 4 2007 P & T Architects & Engineers Ltd Residential Development At 2 Lok Kwai Path Shatin, 2 Lok Kwai Path, Shatin, N.T. STTL 526 BD 9067/02 Jan 06 / May 06 5 2007 Leung King Partners Ltd Villa Rosa Residents 82 Peak Road, Hong Kong RBL 742 BD 2014/98 Aug 00 6 2007 Dennis Lau & Ng Chun Man Architects & Engineers (HK) Ltd Tuen Mun Area 4C, TMTL 384 King Fung Path, Tuen Mun, N.T. Lot No. 384, Area 4C BD 6/9260/97H (P) Aug 02 Service Apartment Building at Nos. 116-122, Yeung Uk 116-122 Yeung Uk Road, Tsuen Wan, 7 2007 MLA Architects (HK) Ltd TWTL 407 9325/93 28 Aug 06 Road (H-Cube) N.T. -

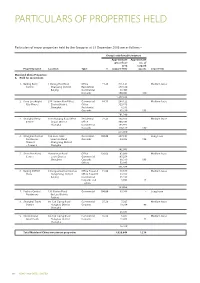

Particulars of Properties Held

PARTICULARS OF PROPERTIES HELD Particulars of major properties held by the Group as at 31 December 2006 are as follows:– Group’s attributable interest Approximate Approximate gross floor no. of area carpark Property name Location Type % (square feet) spaces Lease term Mainland China Properties A. Held for investment 1. Beijing Kerry 1 Guang Hua Road Office 71.25 711,121 Medium lease Centre Chaoyang District Residential 277,330 Beijing Commercial 98,406 Carparks 190,806 430 1,277,663 2. Kerry Everbright 218 Tianmu Road West Commercial 64.35 286,122 Medium lease City Phase I Zhabei District Office 323,675 Shanghai Residential 6,333 Carparks 85,250 155 701,380 3. Shanghai Kerry 1515 Nanjing Road West Residential 74.25 142,355 Medium lease Centre Jingan District Office 308,584 Shanghai Commercial 103,971 Carparks 118,129 180 673,039 4. Shanghai Central 166 Lane 1038 Residential 100.00 287,101 Long lease Residences Huashan Road Carparks 54,982 154 Phase II Changning District – Tower 3 Shanghai 342,083 5. Shenzhen Kerry Renminnan Road Office 100.00 82,099 Medium lease Centre Lowu District Commercial 107,256 Shenzhen Carparks 88,319 193 Others 53,885 331,559 6. Beijing COFCO 8 Jianguomennei Avenue Office Tower A 15.00 49,649 Medium lease Plaza Dongcheng District Office Tower B 53,895 Beijing Commercial 86,592 Carparks and 3,892 25 others 194,028 7. Fuzhou Central 139 Gutian Road Commercial 100.00 63,986 – Long lease Residences Gu Lou District Fuzhou 8. Shanghai Trade 88-128 Siping Road Commercial 55.20 7,567 Medium lease Square Hongkou District Carparks 19,264 48 Shanghai 26,831 9. -

Major Transaction

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult your stockbroker or other registered dealer in securities, bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Kerry Properties Limited, you should at once hand this circular to the purchaser(s) or the transferee(s) or to the bank, stockbroker or other agent through whom the sale or transfer was effected for transmission to the purchaser(s) or the transferee(s). The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this circular, makes no representation as to its accuracy or completeness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. website: www.kerryprops.com (Stock Code: 00683) MAJOR TRANSACTION A letter from the board of directors of Kerry Properties Limited is set out on pages 5 to 25 of this circular. * For identification purpose only 29 December 2004 CONTENTS Page Definitions ........................................................ 1 Letter from the Board ............................................... 5 Appendix I – Accountants’ Report on Treasure Lake................ 26 Appendix II – Accountants’ Report on Eas HK .................... 33 Appendix III − Accountants’ Report on the Eas PRC Group ........... 51 Appendix IV – Financial Information