Evidence Log CRMF 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TOP 100 POWER PEOPLE 2016 the Movers and Shakers in Wind

2016 Top 100 Power People 1 TOP 100 POWER PEOPLE 2016 The movers and shakers in wind Featuring interviews with Samuel Leupold from Dong Energy and Ian Mays from RES Group © A Word About Wind, 2016 2016 Top 100 Power People Contents 2 CONTENTS Compiling the Top 100: Advisory panel and ranking process 4 Interview: Dong Energy’s Samuel Leupold discusses offshore 6 Top 100 breakdown: Statistics on this year’s table 11 Profiles: Numbers 100 to 41 13 Interview: A Word About Wind meets RES Group’s Ian Mays 21 Profiles: Numbers 40 to 6 26 Top five profiles:The most influential people in global wind 30 Top 100 list: The full Top 100 Power People for 2016 32 Next year: Key dates for your diary in 2017 34 21 Facing the future: Ian Mays on RES Group’s plans after his retirement © A Word About Wind, 2016 2016 Top 100 Power People Editorial 3 EDITORIAL resident Donald Trump. It is one of The company’s success in driving down the Pthe biggest shocks in US presidential costs of offshore wind over the last year history but, in 2017, Trump is set to be the owes a great debt to Leupold’s background new incumbent in the White House. working for ABB and other big firms. Turn to page 6 now if you want to read the The prospect of operating under a climate- whole interview. change-denying serial wind farm objector will not fill the US wind sector with much And second, we went to meet Ian Mays joy. -

Annual Report 2011 2011 Annu a L Repo R T

Key AnnuAl RepoRt Key milestones 2011 figuRes Financial figures 2011 2010 2009 2008 2007 2012 2011 Revenues (€mn) 3,033 2,764 3,229 3,834 3,247 MW equivalent sold 2,802 2,405 3,145 3,684 3,289 • Gamesa consolidated its leading position in energy • Gamesa maintains its leading position in the world EBIT (€mn) 131 119 177 233 250 efficiency and environmental terms with the energy business, having installed 3,308 MW in net profit (€mn) 51 50 115 320 220 certification of the world's first ecodesigned the year net debt/EBITDA 2.0x -0.6x 0.7x 0.1x 0.5x wind turbine • Gamesa signs deal to supply 356 MW of the new Share price at 31 Dec. (€) 3.21 5.71 11.78 12.74 31.98 • Ignacio Martín appointed Executive Chairman G97-2.0 MW turbine in 2011 Earnings per share (€) 0.21 0.21 0.47 1.32 0.90 Gross dividend per share (€) 0.05 0.12 0.21 0.23 0.21 • Gamesa decides to install its first offshore prototype • Supply of 200 MW in Egypt, with a 5-year in Spain, at Arinaga (Gran Canaria) maintenance contract • Entering new markets: uruguay and nicaragua • new framework agreement with Iberdrola Social indicators 2011 2010 2009 2008 2007 2011 t Workforce 8,357 7,262 6,360 7,187 6,945 • European launch of large component • Type certificate from lG for the G128-4.5 MW turbine, R refurbishment service the most powerful onshore turbine on the market % international workforce 42 36 31 32 33 % women in workforce 23.2 24.55 25.52 25.34 22.30 Repo • Agreement to sell 480 MW in the united States to • New supply contracts in China: 200 MW for Huadian % permanently employed -

Spotlight on Northern Ireland Regional Focus

COMMUNICATION HUB FOR THE WIND ENERGY INDUSTRY ‘TITANIC’ SPOTLIGHT ON NORTHERN IRELAND REGIONAL FOCUS GLOBAL WIND ALLIANCE COMPETEncY BasED TRaininG FEBRUARY/MARCH 2012 | £5.25 www.windenergynetwork.co.uk INTRODUCTION COMMUNICATING YOUR THOUGHTS AND OPINIONS WIND ENERGY NETWORK TV CHANNEL AND ONLINE LIBRARY These invaluable industry resources continue to build and we are very YOU WILL FIND WITHIN THIS We hope you enjoy the content and pleased with the interest and support EDITION CONTRIBUTIONS WHICH please feel free to contact us to make of our proposed sponsors. Please give COULD BE DESCRIBED AS OPINION your feelings known – it’s good to talk. the team a call and find out how to get PIECES. THEY ARE THERE TO FOCUS involved in both. ATTENTION ON VERY IMPORTANT ‘SpoTLIGHT ON’ regIONAL FOCUS SUBJECT AREAS WITH A VIEW Our regional focus in this edition features Remember they are free to TO GALVANISING OPINION AND Northern Ireland. Your editor visited contribute and free to access. BRINGING THE INDUSTRY TOGETHER the area in late November 2011 when TO ENSURE EFFECTIVE PROGRESS reporting on the Quo Vadis conference Please also feel free to contact us AND THEREFORE SUCCESS. and spent a very enjoyable week soaking if you wish to highlight any specific up the atmosphere, local beverages as area within the industry and we will Ray Sams from Spencer Coatings well the Irish hospitality (the craic). endeavour to encourage debate and features corrosion in marine steel feature the issue within our publication. structures, Warren Fothergill from As you will see it is a very substantial Group Safety Services on safety feature and the overall theme is one of passports and Michael Wilder from excitement and forward thinking which Petans on competency based training will ensure Northern Ireland is at the standardisation. -

Annual-Report-Summary-2014.Pdf

gamesa 2014-01-1 INGLES (resumen)_Maquetación 1 27/04/15 09:52 Página 1 gamesa 2014-01-1 INGLES_Maquetación 1 24/04/15 14:40 Página 2 Gamesa in 2014 MW installed 18,831 MW MW installed 3,572 MW MW under O M 961 MW MW under O &M 14,498 MW & Proprietary capacity 3,971 MW Proprietary capacity 602 MW Europe & RoW 16% United States China 15% MW installed 4,151 MW 9% MW under O &M 1,348 MW Proprietary capacity 838 MW % India 26% Latin America MW installed 1,713 MW 34% MW under O &M 1,444 MW Proprietary capacity 1,041 MW MW installed 2,970 MW MW under O &M 2,519 MW Proprietary capacity 314 MW % MW sold in 2014. 31,237 MW 6,766 MW 20,770 MW installed proprietary capacity under O &M 2 gamesa 2014-01-1 INGLES_Maquetación 1 24/04/15 14:40 Página 3 Economic indicators Recurring E bit Net profit and E bit margin Sales MW sold MM € MM € MM € 2,623 92 191 2,846 129 2,336 1,953 45 5.5% 6.7% 2013 2014 2013 2014 2013 2014 2013 2014 Social and environmental indicators Employees Health & Safety CO 2 prevented MM t Workforce Frequency index 6,431 47 6,079 1.74 1.72 43 2013 2014 2013 2014 2013 2014 Gender Severity index 0.055 0.054 22% 78% 2013 2014 Gamesa in 2014 3 gamesa 2014-01-1 INGLES_Maquetación 1 28/04/15 11:36 Página 4 Index Message from the Chairman Message from the Business CEO Corporate Governance 4 gamesa 2014-01-1 INGLES (resumen)_Maquetación 1 27/04/15 10:39 Página 5 1 2 Business model 2014 Results 18 Geographic 52 Market environment diversification and outlook 21 Vertical integration 55 Financial performance 24 Innovation 28 Financial strength 32 Commitments: employees, customers, shareholders, suppliers, environment and communities Index 5 gamesa 2014-01-1 INGLES_Maquetación 1 24/04/15 14:41 Página 6 Message from the Chairman Dear shareholders, For the past couple of years Gamesa has been focused on executing its 2013-2015 business Plan, designed with the aim of making the company profitable again and adapting it to the new sector paradigm without sacrificing the flexibility needed to tap potential market opportunities. -

Forecast from 2016-17 to 2019-20

Tariff Information Paper Forecast TNUoS tariffs from 2016/17 to 2019/20 This information paper provides a forecast of Transmission Network Use of System (TNUoS) tariffs from 2016/17 to 2019/20. These tariffs apply to generators and suppliers. This annual publication is intended to show how tariffs may evolve over the next five years. The forecast tariffs for 2016/17 will be refined throughout the year. 28 January 2015 Version 1.0 1 Contents 1. Executive Summary....................................................................................4 2. Five Year Tariff Forecast Tables ...............................................................5 2.1 Generation Tariffs ................................................................................. 5 2.2 Onshore Local Circuit Tariffs ..............................................................10 2.3 Onshore Local Substation Tariffs .......................................................12 Any Questions? 2.4 Offshore Local Tariffs .........................................................................12 2.5 Demand Tariffs ...................................................................................13 Contact: 3. Key Drivers for Tariff Changes................................................................14 Mary Owen 3.1 CMP213 (Project TransmiT)...............................................................14 Stuart Boyle 3.2 HVDC Circuits.....................................................................................14 3.3 Contracted Generation .......................................................................15 -

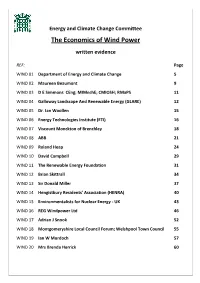

Memorandum Submitted by the Department of Energy and Climate Change (WIND 01)

Energy and Climate Change Committee The Economics of Wind Power written evidence REF: Page WIND 01 Department of Energy and Climate Change 5 WIND 02 Maureen Beaumont 9 WIND 03 D E Simmons CEng; MIMechE; CMIOSH; RMaPS 11 WIND 04 Galloway Landscape And Renewable Energy (GLARE) 12 WIND 05 Dr. Ian Woollen 15 WIND 06 Energy Technologies Institute (ETI) 16 WIND 07 Viscount Monckton of Brenchley 18 WIND 08 ABB 21 WIND 09 Roland Heap 24 WIND 10 David Campbell 29 WIND 11 The Renewable Energy Foundation 31 WIND 12 Brian Skittrall 34 WIND 13 Sir Donald Miller 37 WIND 14 Hengistbury Residents' Association (HENRA) 40 WIND 15 Environmentalists for Nuclear Energy ‐ UK 43 WIND 16 REG Windpower Ltd 46 WIND 17 Adrian J Snook 52 WIND 18 Montgomeryshire Local Council Forum; Welshpool Town Council 55 WIND 19 Ian W Murdoch 57 WIND 20 Mrs Brenda Herrick 60 WIND 21 Mr N W Woolmington 62 WIND 22 Professor Jack W Ponton FREng 63 WIND 23 Mrs Anne Rogers 65 WIND 24 Global Warming Policy Foundation (GWPF) 67 WIND 25 Derek Partington 70 WIND 26 Professor Michael Jefferson 76 WIND 27 Robert Beith CEng FIMechE, FIMarE, FEI and Michael Knowles CEng 78 WIND 28 Barry Smith FCCA 81 WIND 29 The Wildlife Trusts (TWT) 83 WIND 30 Wyck Gerson Lohman 87 WIND 31 Brett Kibble 90 WIND 32 W P Rees BSc. CEng MIET 92 WIND 33 Chartered Institution of Water and Environmental Management 95 WIND 34 Councillor Ann Cowan 98 WIND 35 Ian M Thompson 99 WIND 36 E.ON UK plc 102 WIND 37 Brian D Crosby 105 WIND 38 Peter Ashcroft 106 WIND 39 Campaign to Protect Rural England (CPRE) 109 WIND 40 Scottish Renewables 110 WIND 41 Greenpeace UK; World Wildlife Fund; Friends of the Earth 114 WIND 42 Wales and Borders Alliance 119 WIND 43 National Opposition to Windfarms 121 WIND 44 David Milborrow 124 WIND 45 SSE 126 WIND 46 Dr Howard Ferguson 129 WIND 47 Grantham Research Institute 132 WIND 48 George F Wood 135 WIND 49 Greenersky. -

Sathyajith Mathew Wind Energy Fundamentals, Resource Analysis and Economics

Sathyajith Mathew Wind Energy Fundamentals, Resource Analysis and Economics Sathyajith Mathew Wind Energy Fundamentals, Resource Analysis and Economics with 137 Figures and 31 Tables Dr. Sathyajith Mathew Assistant Professor & Wind Energy Consultant Faculty of Engineering, KCAET Tavanur Malapuram, Kerala India E-mail : [email protected] Library of Congress Control Number: 2005937064 ISBN-10 3-540-30905-5 Springer Berlin Heidelberg New York ISBN-13 978-3-540-30905-5 Springer Berlin Heidelberg New York This work is subject to copyright. All rights are reserved, whether the whole or part of the material is concerned, specifically the rights of translation, reprinting, reuse of illustrations, recitation, broadcasting, reproduction on microfilm or in any other way, and storage in data banks. Duplication of this publication or parts thereof is permitted only under the provisions of the German Copyright Law of September 9, 1965, in its current version, and permission for use must always be obtained from Springer-Verlag. Violations are liable to prosecution under the German Copyright Law. Springer is a part of Springer Science+Business Media springeronline.com © Springer-Verlag Berlin Heidelberg 2006 Printed in The Netherlands The use of general descriptive names, registered names, trademarks, etc. in this publication does not imply, even in the absence of a specific statement, that such names are exempt from the relevant protective laws and regulations and therefore free for general use. Cover design: E. Kirchner, Heidelberg Production: Almas Schimmel Typesetting: camera-ready by Author Printing: Krips bv, Meppel Binding: Stürtz AG, Würzburg Printed on acid-free paper 30/3141/as 5 4 3 2 1 0 Who has gathered the wind in his fists? ……………………………………………...................Proverbs 30:4 Dedicated to my parents, wife Geeta Susan and kids Manuel & Ann Preface Growing energy demand and environmental consciousness have re-evoked human interest in wind energy. -

Breeze Production Wind Farm Management System

Breeze Production Wind Farm Management System PRODUCT OVERVIEW Software for wind farm owners and operators. Contents Contents 2 Monitor 15 Operator’s Dashboard 16 Company Overview 4 Map Overview 17 Wind Turbine 18 Increase Profitability 5 Alarms & Notifications 19 Error Categorization 20 Customers 6 Analyze 21 Wallenstam 7 YARD ENERGY Group 8 Performance 22 Rabbalshede Kraft 9 Stop 23 Vindin 10 Loss 24 Weather 25 Product Overview 11 Custom Data 26 Breeze User Types 12 Manage 27 Breeze Highlights 13 Breeze Components 14 Budget & KPI’s 28 Scheduled Maintenance 29 2 Contractual Availability 30 Support 44 Flexible User Permissions 31 Release Management 45 Reports 32 Breeze vs. the Competition 46 Secure 33 Network Architecture 34 Word from the CEO 47 Wind Farm Architecture 35 Data Security 36 Data Collection 37 Extend 38 Breeze API 39 Park PC Data Buffer 40 Wind Farm Monitoring for Your Mobile Device 41 Installation & Support 42 Installation 43 3 Company Overview Greenbyte, the company behind Breeze, was founded in 2010 based on the firm belief that the inherent variability in the “fuels”, for renewable electricity production make the industry highly dependent on quality data to create value. During the company’s four year life time this belief has proven to be true and to become increasingly important. Value creation in the renewable energy industry is dependent on high quality data from production assets. With so many actors in the value chain dependent on data to create value there is a need for products leveraging modern software to make the data available. During the past four years Greenbyte has developed two products - Breeze Development – for wind energy project developers and Breeze Production – for wind turbine owners. -

Triton Knoll Offshore Wind Farm Limited Triton Knoll Electrical System …………………………………………………

Triton Knoll Offshore Wind Farm Limited Triton Knoll Electrical System ………………………………………………… Appendix 6: Credentials Outline - Triton Knoll Team Date: 30th November 2015 Appendix 6 of the Applicant’s response to Deadline 3 Triton Knoll Offshore Wind Farm Limited Triton Knoll Electrical System Triton Knoll Offshore Wind Farm Limited Triton Knoll Offshore Wind Farm Limited 4th Floor One Kingdom Street Triton Knoll Electrical System Paddington Central London W2 6BD Appendix 6: Credentials Outline - Triton Knoll T: 0845 026 0562 Team Email: [email protected] www.rweinnogy.com/tritonknoll Appendix 6 of the Applicant’s response to Deadline 3 Date: 30th November 2015 Drafted By: Burgess Salmon Approved By: Kim Gauld-Clark Date of Approval: 30/11/15 Revision: 1.0 Triton Knoll Offshore Wind Farm Limited Copyright © 2015 RWE Innogy UK Ltd All pre-existing rights reserved 2 Triton Knoll Offshore Wind Farm Limited Triton Knoll Electrical System TABLE OF CONTENTS 1. CREDENTIALS OUTLINE - TRITON KNOLL TEAM 4 Sub-Heading 4 TABLE OF TABLES Table 1: Triton Knoll Team 4 3 Triton Knoll Offshore Wind Farm Limited Triton Knoll Electrical System Name Kristen Read Position Solicitor Company Burges Salmon Qualifications BSc. Biochemistry, LLB, Dip. Legal Practice Relevant Experience Has particular expertise advising on major planning applications, appeals and public inquiries in both Scotland and England. Recent experience includes: advising on the s36 application for the Dorenell wind farm, including drafting and advising on conditions agreements; advising on the Tom Nan Clach wind farm and appeal, including the conjoined inquiry with the s36 Glenkirk wind farm and advising on the Harbour Revision Order inquiry for the Rosyth International Container Terminal. -

Regulatory Committee 6

Page 1 – Navitus Bay Wind Park Local Impact Report Agenda I tem: Regulatory 6 Committee Date of Meeting Regulatory Committee - 5 September 2014 Officer Head of Planning Subject of Report Navitus Bay Wind Park Local Impact Report Executive Summary Through the National Infrastructure Planning process, Dorset County Council, as a local authority is invited to submit a Local Impact Report on the proposed Navitus Bay Wind Park development. This committee report presents a draft Local Impact Report which is based on the ‘relevant representation’ previously approved by Dorset County Council Planning Committee and Cabinet and sent to the Planning Inspectorate in June. Officers have examined the application and have provided views on the technical aspects of the project. The key issues are described in detail in this draft Local Impact Report, which is to be submitted to the Examining Authority by October 6 th for consideration during the six month examination of the Navitus Bay application. Impact Assessment: Equalities Impact Assessment: This report concerns the submission of a Local Impact Report to the Examining Authority who have been selected to assess the Navitus Bay Wind Park application by the Secretary of State. The submission of a Local Impact Report is invited through Section 60 (2) of the Planning Act 2008 and has no implications in terms of changes to any new or existing policy with equalities implications. Use of Evidence: The recommendation has been made after consideration of government and local policy and guidance and local evidence in specific topic areas. Budget: The response to this consultation does not give rise to any budget implications for the Committee. -

Wind Energy La Rocca Srl Pagina 1 Di 7 Via Caravaggio, 125 – 65125 Pescara

Wind Energy La Rocca Srl Pagina 1 di 7 Via Caravaggio, 125 – 65125 Pescara Progetto di un impianto eolico composto da n.10 aerogeneratori nel Comune di Foggia in località “La Stella - Duanera”. INDICE A. PARTE GENERALE .................................................................................................................................. 2 A.1 Componenti dell’impianto....................................................................................................................... 2 A.2 Schede Tecniche dei Componenti dell’impianto ..................................................................................... 2 A.3 Schemi di Funzionamento dell’impianto ................................................................................................. 5 B. SISTEMA DI MANUTENZIONE DELL’IMPIANTO ........................................................................................ 5 C. MANUALE D’USO DI TUTTI I COMPONENTI DELL’IMPIANTO ................................................................... 6 D. PROGRAMMA DI MANUTENZIONE ........................................................................................................ 7 E. ALLEGATI ............................................................................................................................................... 7 INDICE FIGURE Figura 1 - Navicella SG 4.3-145 ............................................................................................................................. 3 Protocollo: U5U1VR6 Data emissione: 2020 Committente: Wind -

Opportunities and Challenges for a Floating Offshore Wind Market in California

Opportunities and challenges for a floating offshore wind market in California PIETER-JAN VANDENBRANDE Master of Science Thesis Stockholm, Sweden 2017 Opportunities and challenges for a floating offshore wind market in California Pieter-Jan Vandenbrande Master of Science Thesis INDEK 2017:71 KTH Industrial Engineering and Management Industrial Management SE-100 44 STOCKHOLM Master of Science Thesis INDEK 2017:71 Opportunities and challenges for a floating offshore wind market in California Pieter-Jan Vandenbrande Approved Examiner Supervisor 2017-05-30 Terrence Brown Serdar Temiz Commissioner Contact person n.a. n.a. Abstract The offshore wind energy industry is a rapidly growing industry as solutions are becoming cost-competitive and there is an increasing need to limit greenhouse gas emissions. New floating offshore wind turbine designs now enable the access to previously inaccessible offshore wind resources. In this research, a comprehensive analysis is made of the different factors influencing the macro environment for a potential floating offshore wind energy market in California. The analysis assesses the relevant political, economic, social, technological, environmental, and legal aspects in California. The outcome of this research shows the opportunities and challenges for a floating wind turbine market in California. It is found that there are many opportunities present due to California's political and economic climate. There is considerable support for offshore wind projects on the state level, demonstrated by the active engagement of the governor and the creation of the California Task Force. The large economy and high electricity prices are promising for future projects. Furthermore, wind resources are vast and the technical infrastructure is present, especially Southern California is well suited.