An Introduction of NABIL BANK

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

November 16, 2018 Certificates of Authorisation Issued by the Reserve Bank of India Under the Payment and Settlement Syst

Date : November 16, 2018 Certificates of Authorisation issued by the Reserve Bank of India under the Payment and Settlement Systems Act, 2007 for Setting up and Operating Payment System in India A. Certificates of Authorisation issued by the Reserve Bank of India under the Payment and Settlement Systems Act, 2007 for Setting up and Operating Payment System in India The Payment and Settlement Systems Act, 2007 along with the Board for Regulation and Supervision of Payment and Settlement Systems Regulations, 2008 and the Payment and Settlement Systems Regulations, 2008 have come into effect from 12th August, 2008. The list of 'Payment System Operators’ authorised by the Reserve Bank of India to set up and operate in India under the Payment and Settlement Systems Act, 2007 is as under: Sr. Name of the Address of the Payment System Date of issue of No. Authorised Principal Office Authorised Authorisation Entity & Validity Period (given in brackets) Financial Market Infrastructure 1. The Clearing The Managing i. Securities 11.02.2009 Corporation of Director, segment covering India Ltd. Clearing Corp. of Govt Securities; India, ii. Forex 5th, 6th & 7th floor Settlement Trade World, Segment -do- “C” Wing Kamala comprising of sub- city, SB Marg, segments Lower Parel (West) a. USD-INR Mumbai 400 013 segment, -do- b. CLS segment – Continuous Linked Settlement (Settlement of Cross Currency -do- Deals), c. Forex Forward segment; iii. Rupee Derivatives -do- Segment-Rupee denominated trades in IRS & FRA. Retail Payments Organisation 2. National The Chief Executive i. National Payments Officer, Financial Switch Corporation of National Payments (NFS) 15.10.2009 India Corporation of ii. -

Annual Report 2014/15 (English)

ANNUAL REPORT 2014/15 Machhapuchchhre Bank Ltd., registered in 1998, is a commercial bank with a network of 56 branches, including an extension counter, located at major business centres of Nepal. It has 600 plus staff; it uses Globus banking software developed by Temenos NV, Switzerland. The Bank has been named after the famous peak, Machhapuchchhre (fish-tailed), located in the Himalayan range of western Nepal. The Bank has been promoted by renowned Non-Resident Nepalese, prominent businessmen and industrialists with a clear vision and commitment to provide a full range of financial services in the most efficient and professional manner. CONTENT Board of Directors 10 Products and Services 25 Chairman’s Statement 12 Head of Department 32 CEO’s Message 14 Auditor’s Report 34 Management Team 16 Financial Statement 36 Board of Directors’ Report 19 Branch Managers 87 6 Machhapuchchhre Bank Limited / Annual Report 2014/15 BANK’S OVERVIEW The Bank, which started its operation from 2000, During FY 2014-15, despite cut-throat competition offers complete banking solutions such as varieties of and a 7.8 magnitude earthquake that hit the deposit products, inward and outward remittance and country, the Bank increased its net profits by 35%, trade finance services, retail and consumer loans as loan portfolio by 17%, deposits by 19%, number of well as loans to SME, corporate houses, and varieties customers by 15%, simplified the service delivery of infrastructure and industrial projects. processes, becoming more techno-savvy, and building a stronger balance sheet. At the end of FY 2014-151, the Bank’s total assets stood at NPR 48.75 billion and total liabilities at NPR The bank also launched various loan products specially 44.77 billion; the bank has a customer base of more meant for small scale farmers, youths involved in small than 400,000. -

English Annual Report 18-19.Pdf

ANNUAL REPORT 2018-19 TOGETHER WE RISE CONTENTS STRATEGIC REPORT An Overview (Vision, Mission, Objectives & Core Values) ................6 Bank’s Performance ..............................................................................................8 Financial Reviews ...................................................................................................9 Macroeconomic-Outlook ..................................................................................10 Customer Centric Business Model .............................................................. 13 CORPORATE GOVERNANCE REPORT OBJECTIVES Governance at A Glance ...................................................................................16 Board of Directors ............................................................................................... 18 The consolidated as well as standalone financial Profile of Directors ..............................................................................................20 statements, prepared in accordance with NFRS, remain the Chairman's Statement ...................................................................................... 23 The CEO’S Point of View ................................................................................. 25 primary source of communication with stakeholders. The Management Team .............................................................................................26 Department Heads .............................................................................................30 -

11 Amrit Banstola

The Journal of Nepalese Business Studies Vol. IV No. 1 Dec. 2007 Prospects and Challenges of E-banking in Nepal Amrit Banstola ABSTRACT Financial Institutions are slowly moving from Brick and Mortar (Physical branches) to click and Brick (E-banking). ATM's are the most popular electronic delivery channel for banking services in Nepal. Only few customers are using internet banking facilities. Nepalese financial institutions till date have not faced any kind of electronic fraud or risk. Banks have basic security tools like firewall, lightening/power surge protection. But it is found that the some banks are in lack of having regular back up of website information and E-banking policy. Nepalese banks are using E-banking for their own convenience and for the purpose of retaining exiting customers. The cost analysis of most of the banks in Nepal is seems to be either inadequate or not applied due to their narrow space of business transaction or lack of sufficient tools. No significant correlation was found between use of E-bank- ing and gender, marital status or salary of customer. However, Use of E-banking signification asso- ciation was found with age and education. Keywords: E-banking, Tele-banking, PC Banking, Internet Banking, Mobile Banking Across the globe, but specifically in Nepal, current trend in private banking has been the consumer movement from traditional branch banking to more stand-alone banking. In other words, a move towards using e-delivery channels such as the Internet, telephone and mobile phones. Many banks are beginning to deliver credit and deposit products electroni- cally. -

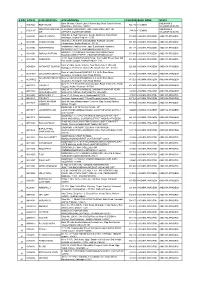

S No Atm Id Atm Location Atm Address Pincode Bank

S NO ATM ID ATM LOCATION ATM ADDRESS PINCODE BANK ZONE STATE Bank Of India, Church Lane, Phoenix Bay, Near Carmel School, ANDAMAN & ACE9022 PORT BLAIR 744 101 CHENNAI 1 Ward No.6, Port Blair - 744101 NICOBAR ISLANDS DOLYGUNJ,PORTBL ATR ROAD, PHARGOAN, DOLYGUNJ POST,OPP TO ANDAMAN & CCE8137 744103 CHENNAI 2 AIR AIRPORT, SOUTH ANDAMAN NICOBAR ISLANDS Shop No :2, Near Sai Xerox, Beside Medinova, Rajiv Road, AAX8001 ANANTHAPURA 515 001 ANDHRA PRADESH ANDHRA PRADESH 3 Anathapur, Andhra Pradesh - 5155 Shop No 2, Ammanna Setty Building, Kothavur Junction, ACV8001 CHODAVARAM 531 036 ANDHRA PRADESH ANDHRA PRADESH 4 Chodavaram, Andhra Pradesh - 53136 kiranashop 5 road junction ,opp. Sudarshana mandiram, ACV8002 NARSIPATNAM 531 116 ANDHRA PRADESH ANDHRA PRADESH 5 Narsipatnam 531116 visakhapatnam (dist)-531116 DO.NO 11-183,GOPALA PATNAM, MAIN ROAD NEAR ACV8003 GOPALA PATNAM 530 047 ANDHRA PRADESH ANDHRA PRADESH 6 NOOKALAMMA TEMPLE, VISAKHAPATNAM-530047 4-493, Near Bharat Petroliam Pump, Koti Reddy Street, Near Old ACY8001 CUDDAPPA 516 001 ANDHRA PRADESH ANDHRA PRADESH 7 Bus stand Cudappa, Andhra Pradesh- 5161 Bank of India, Guntur Branch, Door No.5-25-521, Main Rd, AGN9001 KOTHAPET GUNTUR 522 001 ANDHRA PRADESH ANDHRA PRADESH Kothapeta, P.B.No.66, Guntur (P), Dist.Guntur, AP - 522001. 8 Bank of India Branch,DOOR NO. 9-8-64,Sri Ram Nivas, AGW8001 GAJUWAKA BRANCH 530 026 ANDHRA PRADESH ANDHRA PRADESH 9 Gajuwaka, Anakapalle Main Road-530026 GAJUWAKA BRANCH Bank of India Branch,DOOR NO. 9-8-64,Sri Ram Nivas, AGW9002 530 026 ANDHRA PRADESH ANDHRA PRADESH -

Annual Report FY 2019/20 (English)

ANNUAL REPORT 2019-20 1 #GoDigital Annual Report 2019/20 ENABLING SMART FUTURE Machhapuchchhre Bank Limited is committed to become one of the most preferred bank in Nepal. In today’s financial market when most of the products and services offered by financial institution are same, the only difference you create is “how you deliver”. MBL does not only focus for what product we offer but also how we deliver them utilizing different means of Customer Service Excellence. Machhapuchchhre Bank Limited was registered in 1998 as the first regional commercial bank from the western region of Nepal and started its banking operations from Pokhara since year 2000. contents Bank’s Overview 06 Board of Director 10 Profile of Director 12 Chairman’s Statement 15 CEO’s Message 19 Management Team 22 Financial Highlights 25 Country’s Economic Conditions 27 Bank’s Performance 28 Human Resources 34 Corporate Governance 38 Director’s Report 47 Risk Management 62 Corporate Social Responsibility 78 Technologies 82 Products and Services 86 Remittance 91 Financial Statement 92 Branch Network 203 6 MACHHAPUCHCHHRE BANK LIMITED BANK’S OVERVIEW The Bank facilitates it’s customers’ The Bank has been promoted by need by delivering the best of highly renowned Non-Residential services in combination with the latest Nepalese, prominent businessman state of the art technologies and and industrialists with a vision and prudent international practices. The dedication to provide the best 36% Bank is the pioneer in introducing the financial products and services in PROFIT GROWTH latest technologies in the banking the most efficient and professional industry in the country. -

State Bank of Travancore

DRAFT LETTER OF OFFER May 28, 2011 For circulation to the Equity Shareholders of our Bank only STATE BANK OF TRAVANCORE (Subsidiary of the State Bank of India) Our Bank was constituted under the State Bank of India (Subsidiary Banks) Act, 1959 as a subsidiary of State Bank of India. (For further details please refer to the chapter titled “History of our Bank and Other Corporate Matters” on page 51 of this Draft Letter of Offer.) Head Offi ce: Poojapura, Thiruvananthapuram-695 012 Tel: + 91 0471 2359975/2351903 Fax: +91 0471 2351861 Contact Person: Mr. V.Viswanathan, Compliance Offi cer E-mail: [email protected] Website: www.statebankoftravancore.com FOR PRIVATE CIRCULATION TO THE EQUITY SHAREHOLDERS OF OUR BANK ONLY DRAFT LETTER OF OFFER ISSUE OF [●] EQUITY SHARES WITH A FACE VALUE OF `10/– EACH (“RIGHTS EQUITY SHARES”) FOR CASH AT A PRICE OF `[●]/– INCLUDING A PREMIUM OF `[●]/– AGGREGATING UPTO `500 CRORES TO THE EXISTING EQUITY SHAREHOLDERS OF OUR BANK ON RIGHTS BASIS IN THE RATIO OF [●] RIGHTS EQUITY SHARES FOR EVERY [●] EQUITY SHARES HELD ON THE RECORD DATE I.E. [●] (“RIGHTS ISSUE/ ISSUE”). THE ISSUE PRICE FOR THE RIGHTS EQUITY SHARES IS [●] TIMES THE FACE VALUE OF THE EQUITY SHARES. GENERAL RISKS Investments in equity and equity related securities involve a degree of risk and Investors should not invest any funds in this Issue unless they can afford to take the risk of losing their investment. Investors are advised to read the Risk Factors carefully before taking an investment decision in this Issue. For taking an investment decision, Investors must rely on their own examination of the Issuer and the Issue including the risks involved. -

DIGITAL PAYMENTS BOOK Part1

DIGITAL PAYMENTS Trends, Issues And Opportunities July 2018 FOREWORD A Committee on Digital Payments was growth figures for both volume and value. constituted by Department of Economic Notwithstanding this the analysis finds that Affairs, Ministry of Finance in August 2016 both the data are relevant and equally under my Chairmanship to inter-alia important. They are complementary. In recommend medium term measures of addition to this the underlying growth trends promotion of Digital Payments Ecosystem in Digital Payments over the last seven in the country. The Committee submitted its years are also covered in this booklet. final report to Hon’ble Finance Minister in December 2016. One of the key This booklet has some new chapters which recommendations of the Committee related cover the areas of policy developments, to development of a metric for Digital global trends and opportunities in Digital Payments. As a follow-up on this a group of Payments. In the policy space the important Stakeholders from Different Departments of developments with respect to the Government of India and RBI was amendment of the Payment and Settlement constituted in NITI Aayog under my Act 2007 are covered. chairmanship to facilitate the work relating I am grateful to Governor, RBI, Secretary to development of the metric. This group MeitY and CEO, NPCI for their support in prepared a document on the measurement preparing this booklet. Shri. B.N. Satpathy, issues of Digital Payments. Accordingly, a Senior Consultant, EAC-PM and Shri. booklet titled “Digital Payments: Trends, Suneet Mohan, Young Professional, NITI Issues and Challenges” was prepared in Aayog have played a key role in compiling May 2017 and was released by me in July this booklet. -

Political Economy in Transition Docking Nepal's Economic Analysis

NEPAL ECONOMIC FORUM ISSUE 44 | MARCH 2021 POLITICAL ECONOMY IN TRANSITION DOCKING NEPAL'S ECONOMIC ANALYSIS DOCKING NEPAL’S ECONOMIC ANALYSIS ISSUE 44 | MARCH 2021 FACTSHEETNEPAL FACTSHEET KEY ECONOMIC INDICATORS GDP (2021) *** USD 30.6 billion GDP growth rate (%)*** 0.2% GNI (PPP, 2021) *** USD 3610 Inflation (y-o-y) **** 4.05% Gross Capital Formation as of 2021, preliminary 50.2% Agriculture sector (% share of GDP)** 27.65% estimate (% of GDP) *** HDI * 0.602 Industry sector (% share of GDP)** 14.27% Rank 142 Service sector (% share of GDP)** 58.08% *HDI figure from Human Development Report of the UNDP-2020 ** Based on Nepal Rastra Bank's 12 months data of 2019/20 *** Based on World Bank Data ****Based on 4 months' Data (2020/21) CONTENTS MARCH 2021 | ISSUE 44 CONTENTS NEPAL FACTSHEET 1 EDITORIAL 4 1 GENERAL OVERVIEW 5 Political Overview 6 International Economy 8 2 MACROECONOMIC OVERVIEW 10 3 SECTORAL REVIEW 13 Agriculture 14 Energy 16 Infrastructure 17 Telecommunications 20 Real Estate 23 Education 24 Health 27 Tourism 29 Trade and Debt 31 Foreign Aid 34 Remittance 36 Environment 39 4 MARKET REVIEW 40 Financial Market 41 Capital Market 45 5 SPECIAL SECTION: POLITICAL ECONOMY IN TRANSITION 48 ENDNOTES 57 NEF Profile 61 Issue 44: March 2021 Executive Board Members: Publisher: Nepal Economic Forum Alpa B. Shakya Website: www.nepaleconomicforum.org Chandni Singh Shayasta Tuladhar P.O Box 7025, Krishna Galli, Lalitpur — Sudip Bhaju 3, Nepal Sujeev Shakya Phone: +977 1 554-8400 Email: [email protected] Advisory Board: Arnico Panday Contributors: Kul Chandra Gautam Nasala Maharjan Mahendra Krishna Shrestha Raju Dhan Tuladhar Prativa Pandey Sugam Nanda Bajracharya Shankar Sharma Sambriddhi Acharya Shraddha Gautam Sampada Shah Sneh Rajbhandari Sarik Koirala Tanushree Agrawal Senior Distinguished Fellows: Bibhakar Shakya Design & Layout: Giuseppe Savino Thuprai Solutions Suman Basnet [email protected] Senior Fellows: This issue of nefport takes into account Apekshya Shah news updates from November 16 2020 Ashraya Dixit to February 16 2021. -

Siblink March 16.Pmd

Personnel Department is awarded ISO 9001:2008 Certification: MD & CEO Mr. V G Mathew receiving the ISO 9001:2008 Certificate from Mr. Shashi Nath Mishra, Global Head, IRQS in the presence of Mr. Paul V L, General Manager (Admin). Objectives: To instil in the bank staff a sense of belonging and involvement in the bank’s affairs To appreciate and applaud the individual achievements of our members of staff Corporate Family Magazine of To act as a communication medium between management and the staff South Indian Bank To increase the professional competence of our bank staff Advisory Board: INSIDE Mr. Sivakumar G. Executive Vice President (Credit) Messages Mr. Paul V.L. General Manager (Admin) Articles Mr. John Thomas General Manager (Business Development) Profitability – A leisure time Thought! Sreekumar Chengath BANKING PROFITABILITY An Indian Story Edition Anoop Abraham George Members: Customer Service is the Best Marketing Strategy Linto Abraham Mr. Sibi P.M. Sustainable Profit Planning Strategies Biju E. Punnachalil Dy. General Manager (IRMD) SIB FY 2015- The Era of Digital Innovation Begins Seethalakshmi H. Mr. Krishnadas P.B. The Great Indian Stress Test Bino George Dy. General Manager (Credit) PRADHAN MANTRI YOJANA’s – A WIN – WIN GAME Charan Deep Singh Mr. Roy Dominic P. 69 and still counting..... Christo Paul Asst. General Manager (Personnel) Media Buzz Corporate Communication Team Mr. Bino George Regular Features Manager P&D Layout, Typeset & Printing: Publisher: Editor: Lumiere Printing Works, Thrissur Mr. Thomas Joseph K., Executive Vice President (Admin) Mr. Francy Jos E. 2 VISION To be the most preferred bank in the areas of customer service, stakeholder value and corporate governance. -

Certificates of Authorisation Issued by the Reserve Bank of India Under the Payment and Settlement Systems Act, 2007 For

Certificates of Authorisation issued by the Reserve Bank of India under the Payment and Settlement Systems Act, 2007 for Setting up and Operating Payment System in India A. Certificates of Authorisation issued by the Reserve Bank of India under the Payment and Settlement Systems Act, 2007 for Setting up and Operating Payment System in India The Payment and Settlement Systems Act, 2007 along with the Board for Regulation and Supervision of Payment and Settlement Systems Regulations, 2008 and the Payment and Settlement Systems Regulations, 2008 have come into effect from 12th August, 2008. The list of 'Payment System Operators’ authorised by the Reserve Bank of India to set up and operate in India under the Payment and Settlement Systems Act, 2007 is as under: Sr. Name of the Address of the Payment System Date of issue of No. Authorised Entity Principal Office Authorised Authorisation & Validity Period (given in brackets) Financial Market Infrastructure 1. The Clearing The Managing i. Securities Corporation of India Director, segment covering 11.02.2009 Ltd. Clearing Corp. Govt Securities; of India, ii. Forex 5th, 6th & 7th Settlement floor Trade Segment -do- World, comprising of “C” Wing sub-segments Kamala City, SB a. USD-INR Marg, segment, -do- Lower Parel b. CLS segment – (West) Mumbai Continuous 400 013 Linked Settlement -do- (Settlement of Cross Currency Deals), c. Forex Forward -do- segment; iii. Rupee Derivatives Segment-Rupee denominated trades in IRS & FRA. Retail Payments Organisation 2. National Payments The Chief i. National Corporation of India Executive Financial Switch Officer, (NFS) 15.10.2009 National ii. Immediate Payments Payment System 12.10.2010 Corporation of (IMPS) India, iii. -

Most Admired Bank by All Stakeholders OUR MISSION Devote Balanced Attention to the Interests and Expectations of Stakeholders, and in Particular

Safe Harbour This document contains certain forward-looking statements based on current expectations of The Federal Bank Limited management. Actual results may vary significantly from the forward–looking statements contained in this document due to various risks and political conditions in India and outside India, volatility in interest rates and in the securities market, new regulations and Government policies that may impact the businesses for The Federal Bank Limited as well as its ability to implement the strategy. The Federal Bank Limited does not undertake to update these statements. This documents does not constitute an offer or recommendation to buy or sell any securities of The Federal Bank Limited or any of its subsidiaries and associate companies. This document also does not constitute an offer or recommendation to buy or sell any financial products offered by The Federal Bank Limited. Figures for the previous year have been regrouped wherever necessary to conform to current year’s presentation. Content About our Bank 04 Performance Dashboard 05 Message from Chairman 08 Message from MD & CEO 10 Board of Directors & Management Team 12 Directors' Report 15 Management Discussion and 49 Analysis Corporate Governance 67 Financial Statement of Federal Bank 88 Basel III Disclosures 155 Consolidated Financial Statement 179 From AOC - I 219 Glimpses of events 221 2 THE DELECTABLE FEDERAL PIE The Federal Pie is a metaphor for the diverse strengths and attributes of Federal Bank. It captures the solidity as well as the agility of an organization that has withstood the vicissitudes of time with aplomb. The bank’s Home Market Dominance, robust Capital Structure, evergrowing NR business, State-of-the Art Digital Capabilities, high quality Liability Fran- chise and adaptive Credit Processes are the ingredients that make this pie delectable for investors and customers alike.