State Bank of Travancore

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

State Bank of Travancore

State Bank of Travancore Instruments Amount Rating Action (Rs. Crore)1 (October 2016) Lower Tier-II Bond Programme 250.00 [ICRA]AAA (stable); reaffirmed Lower Tier-II Bond Programme 375.00 [ICRA]AAA (stable); withdrawn Tier-II Bonds Programme-Basel III 691.00 [ICRA]AAA (hyb) (stable); withdrawn ICRA has reaffirmed the [ICRA]AAA (pronounced ICRA triple A) rating with stable outlook for the Rs. 250.00 crore lower tier-II bond programme of State Bank of Travancore (SBT). ICRA has withdrawn the [ICRA]AAA rating assigned to the bank’s Rs. 375.00 crore lower tier-II bond programme as requested by the bank, as the rated instrument has been fully redeemed and there is no amount outstanding. ICRA has also withdrawn the [ICRA]AAA (hyb) (pronounced ICRA triple A hybrid) rating assigned to the bank’s Rs. 691.00 crore Basel III compliant tier-II bonds, as no funds were raised against this rated instrument and there is no amount outstanding. The letters “hyb” in parenthesis suffixed to a rating symbol stand for “hybrid”, indicating that the rated instrument is a hybrid subordinated instrument with equity-like loss-absorption features; such features may translate into higher levels of rating transition and loss-severity vis-à-vis conventional debt instruments. The highest credit quality rating for SBT factors in its strong parentage (79% stake held by State Bank of India (SBI); rated [ICRA]AAA(stable)/[ICRA]A1+), the operational and management synergies with its parent and its well-established franchise in its area of operations (primarily Kerala) supported by the State Bank brand. -

November 16, 2018 Certificates of Authorisation Issued by the Reserve Bank of India Under the Payment and Settlement Syst

Date : November 16, 2018 Certificates of Authorisation issued by the Reserve Bank of India under the Payment and Settlement Systems Act, 2007 for Setting up and Operating Payment System in India A. Certificates of Authorisation issued by the Reserve Bank of India under the Payment and Settlement Systems Act, 2007 for Setting up and Operating Payment System in India The Payment and Settlement Systems Act, 2007 along with the Board for Regulation and Supervision of Payment and Settlement Systems Regulations, 2008 and the Payment and Settlement Systems Regulations, 2008 have come into effect from 12th August, 2008. The list of 'Payment System Operators’ authorised by the Reserve Bank of India to set up and operate in India under the Payment and Settlement Systems Act, 2007 is as under: Sr. Name of the Address of the Payment System Date of issue of No. Authorised Principal Office Authorised Authorisation Entity & Validity Period (given in brackets) Financial Market Infrastructure 1. The Clearing The Managing i. Securities 11.02.2009 Corporation of Director, segment covering India Ltd. Clearing Corp. of Govt Securities; India, ii. Forex 5th, 6th & 7th floor Settlement Trade World, Segment -do- “C” Wing Kamala comprising of sub- city, SB Marg, segments Lower Parel (West) a. USD-INR Mumbai 400 013 segment, -do- b. CLS segment – Continuous Linked Settlement (Settlement of Cross Currency -do- Deals), c. Forex Forward segment; iii. Rupee Derivatives -do- Segment-Rupee denominated trades in IRS & FRA. Retail Payments Organisation 2. National The Chief Executive i. National Payments Officer, Financial Switch Corporation of National Payments (NFS) 15.10.2009 India Corporation of ii. -

State Bank of India

State Bank of India State Bank of India Type Public Traded as NSE: SBIN BSE: 500112 LSE: SBID BSE SENSEX Constituent Industry Banking, financial services Founded 1 July 1955 Headquarters Mumbai, Maharashtra, India Area served Worldwide Key people Pratip Chaudhuri (Chairman) Products Credit cards, consumer banking, corporate banking,finance and insurance,investment banking, mortgage loans, private banking, wealth management Revenue US$ 36.950 billion (2011) Profit US$ 3.202 billion (2011) Total assets US$ 359.237 billion (2011 Total equity US$ 20.854 billion (2011) Owner(s) Government of India Employees 292,215 (2012)[1] Website www.sbi.co.in State Bank of India (SBI) is a multinational banking and financial services company based in India. It is a government-owned corporation with its headquarters in Mumbai, Maharashtra. As of December 2012, it had assets of US$501 billion and 15,003 branches, including 157 foreign offices, making it the largest banking and financial services company in India by assets.[2] The bank traces its ancestry to British India, through the Imperial Bank of India, to the founding in 1806 of the Bank of Calcutta, making it the oldest commercial bank in the Indian Subcontinent. Bank of Madras merged into the other two presidency banks—Bank of Calcutta and Bank of Bombay—to form the Imperial Bank of India, which in turn became the State Bank of India. Government of Indianationalised the Imperial Bank of India in 1955, with Reserve Bank of India taking a 60% stake, and renamed it the State Bank of India. In 2008, the government took over the stake held by the Reserve Bank of India. -

Resolution Plan Section 1: Public Section December 31, 2015

STATE BANK OF INDIA Resolution Plan Section 1: Public Section December 31, 2015 TABLE OF CONTENTS Section 1: Public Section Introduction Overview of the Bank I. Summary of the Resolution Plan A. Overview of the U.S. Resolution Plan B. Names of Material Entities C. Description of Core Business Lines D. Summary of Financial Information Regarding Assets, Liabilities, Capital and Major Funding Sources E. Description of Derivative and Hedging Activities F. Memberships in Material Payment, Clearing, and Settlement systems G. Description of Non-U.S. Operations H. Material Supervisory Authorities I. Principal Officers J. Resolution Planning Corporate Governance Structure and Processes K. Material Management Information Systems L. High-Level Description of Resolution Strategy Section 1: Public Section Introduction State Bank of India (the “Bank”) is a foreign banking organization duly organized and existing under the laws of India. In the United States, the Bank maintains (a) a New York state-licensed, insured branch (the “New York Branch”), (b) an Illinois state- licensed, insured branch (the “Chicago Branch,” and together with the New York Branch, the “Branches”), (c) a California state-licensed agency (the “Los Angeles Agency”), (d) a representative office in Washington, D.C. licensed by the Federal Reserve (the “Washington D.C. Representative Office”), and (e) a wholly-owned bank subsidiary that is chartered in California, State Bank of India (California) Ltd. (“SBIC”). The Bank has developed a U.S. resolution plan (“U.S. Resolution Plan”) -

Introduction Banking in India

Introduction Banking in India Banking in India originated in the last decades of the 18th century. The first banks were The General Bank of India which started in 1786, and the Bank of Hindustan, both of which are now defunct. The oldest bank in existence in India is the State Bank of India, which originated in the Bank of Calcutta in June 1806, which almost immediately became the Bank of Bengal. This was one of the three presidency banks, the other two being the Bank of Bombay and the Bank of Madras, all three of which were established under charters from the British East India Company. For many years the Presidency banks acted as quasi-central banks, as did their successors. The three banks merged in 1921 to form the Imperial Bank of India, which, upon India’s Independence became the State Bank of India. Origin of Banking in India Indian merchants in Calcutta established the Union Bank in 1839, but it failed in 1848 as a consequence of the economic crisis of 1848-49. The Allahabad Bank, established in 1865 and still functioning today, is the oldest Joint Stock bank in India. (Joint Stock Bank: A company that issues stock and requires shareholders to be held liable for the company’s debt) It was not the first though. That honor belongs to the Bank of Upper India, which was established in 1863, and which survived until 1913, when it failed, with some of its assets and liabilities being transferred to the Alliance Bank of Simla. When the American Civil War stopped the supply of cotton to Lancashire from the Confederate States, promoters opened banks to finance trading in Indian cotton. -

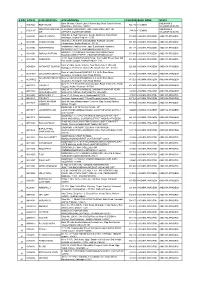

S No Atm Id Atm Location Atm Address Pincode Bank

S NO ATM ID ATM LOCATION ATM ADDRESS PINCODE BANK ZONE STATE Bank Of India, Church Lane, Phoenix Bay, Near Carmel School, ANDAMAN & ACE9022 PORT BLAIR 744 101 CHENNAI 1 Ward No.6, Port Blair - 744101 NICOBAR ISLANDS DOLYGUNJ,PORTBL ATR ROAD, PHARGOAN, DOLYGUNJ POST,OPP TO ANDAMAN & CCE8137 744103 CHENNAI 2 AIR AIRPORT, SOUTH ANDAMAN NICOBAR ISLANDS Shop No :2, Near Sai Xerox, Beside Medinova, Rajiv Road, AAX8001 ANANTHAPURA 515 001 ANDHRA PRADESH ANDHRA PRADESH 3 Anathapur, Andhra Pradesh - 5155 Shop No 2, Ammanna Setty Building, Kothavur Junction, ACV8001 CHODAVARAM 531 036 ANDHRA PRADESH ANDHRA PRADESH 4 Chodavaram, Andhra Pradesh - 53136 kiranashop 5 road junction ,opp. Sudarshana mandiram, ACV8002 NARSIPATNAM 531 116 ANDHRA PRADESH ANDHRA PRADESH 5 Narsipatnam 531116 visakhapatnam (dist)-531116 DO.NO 11-183,GOPALA PATNAM, MAIN ROAD NEAR ACV8003 GOPALA PATNAM 530 047 ANDHRA PRADESH ANDHRA PRADESH 6 NOOKALAMMA TEMPLE, VISAKHAPATNAM-530047 4-493, Near Bharat Petroliam Pump, Koti Reddy Street, Near Old ACY8001 CUDDAPPA 516 001 ANDHRA PRADESH ANDHRA PRADESH 7 Bus stand Cudappa, Andhra Pradesh- 5161 Bank of India, Guntur Branch, Door No.5-25-521, Main Rd, AGN9001 KOTHAPET GUNTUR 522 001 ANDHRA PRADESH ANDHRA PRADESH Kothapeta, P.B.No.66, Guntur (P), Dist.Guntur, AP - 522001. 8 Bank of India Branch,DOOR NO. 9-8-64,Sri Ram Nivas, AGW8001 GAJUWAKA BRANCH 530 026 ANDHRA PRADESH ANDHRA PRADESH 9 Gajuwaka, Anakapalle Main Road-530026 GAJUWAKA BRANCH Bank of India Branch,DOOR NO. 9-8-64,Sri Ram Nivas, AGW9002 530 026 ANDHRA PRADESH ANDHRA PRADESH -

List of Bank Names

List of Banks for e-BRC Registration and Uploading S No. Name of Bank User Id (7 characters) Remarks 1 Abhyudaya Co-op Bank Ltd ABHY001 First four characters are IFSC code +001 2 Abu Dhabi Commercial Bank Ltd ADCB001 First four characters are IFSC code +001 3 National Bank of Abu Dhabi PJSC NBAD001 First four characters are IFSC code +001 4 AB Bank Ltd. ABBL001 First four characters are IFSC code +001 5 Ahmedabad Mercantile Co-op Bank First four characters are IFSC code +001 AMCB001 6 Allahabad Bank ALLA001 First four characters are IFSC code +001 7 Andhra Bank ANDB001 First four characters are IFSC code +001 8 Antwerp Diamond Bank Mumbai ADIA001 First four characters are IFSC code +001 9 Australia and New Zealand Banking ANZB001 First four characters are IFSC code +001 Group Limited 10 Axis Bank UTIB001 First four characters are IFSC code +001 11 Bank Of America BOFA001 First four characters are IFSC code +001 12 Bank Of Bahrain And Kuwait BBKM001 First four characters are IFSC code +001 13 Bank of Baroda BARB001 First four characters are IFSC code +001 14 Bank Of Ceylon BCEY001 First four characters are IFSC code +001 15 Bank of India BKID001 First four characters are IFSC code +001 16 Bank Of Maharashtra MAHB001 First four characters are IFSC code +001 17 Bank Of Nova Scotia NOSC001 First four characters are IFSC code +001 18 Bank Of Tokyo-Mitsubishi Ufj Ltd BOTM001 First four characters are IFSC code +001 19 Bank Internasional Indonesia IBBK001 First four characters are IFSC code +001 20 Barclays Bank Plc BARC001 First four characters -

5390310316.Pdf

Dear Investor, The year gone by was an exceptional one for many reasons. Our country has been the beacon of all that is good – growth potential of our economy and markets, positivity in our future as a country with a host of measures taken by our elected representatives to ease and enable businesses and individuals; and general positivity with conviction as more people, young and experienced, taking the plunge to start-up on their own thus helping create employment and consumption for people and the community around them. The Indian economy and the equity markets were in the thick of the action and the year was a momentous one. A lot of crucial bills were passed which will ease the way we do business and deliver services including bills like The Real Estate (Regulation and Development) Bill and The Aadhaar (targeted delivery of financial and other subsidies, benefits and services) Bill. This was backed with a strong fiscal show from the Government by sticking to its fiscal deficit targets while pursuing its growth agenda. The equity markets touched all-time highs on the back of retail investors, betting on the potential of the country, investing in record numbers which was an encouraging sign in recent times. The Mutual Fund industry gained significantly buoyed by record inflows into equity-based funds with growth of 14% in the financial year ended March 2016, with average assets under management touching `13.53 lakh crore and taking the total number of folios to a record 4.7 crore (Source: SEBI and AMFI). More importantly, asset management companies were net-investors in the markets last year providing the counter-balance to FIIs which is heartening. -

Retirement Planning Products Offered by the State Bank of India and Its Affiliates

© 2021 JETIR January 2021, Volume 8, Issue 1 www.jetir.org (ISSN-2349-5162) Retirement Planning Products Offered by the State Bank of India and Its Affiliates Sharvee Shrotriya, Research Scholar, Department of Commerce and Management, Banasthali Vidyapith, Niwai- 304022, India. ABSTRACT An integral aspect of financial planning is retirement planning. The need for retirement planning is intensified by a rise in overall life expectancy. In addition to providing an extra source of revenue, retirement planning also allows one to cope with medical emergencies, meet life goals, and remain financially independent. The State Bank of India and other commercial banks and financial institutions have brought out many products and schemes to facilitate retirement planning procedures. However, the plans are not organized enough to be accessible to the public. The degree of effectiveness of these plans and their execution are some of the things that raise concern. The retirement planning among women and the ways of delivering services by the bank is yet to be researched. The study is based on secondary data. The research shows that apart from measures taken by the SBI for the betterment of retirement planning, the products launched are not ample. It is essential to ensure that retirement planning is started by youngsters at an early age and the banks lubricate the process with their innovative, accessible, and customer-friendly products. Key Words- Financial Planning, SBI and Retirement Planning. 1. INTRODUCTION Famously known as the SBI, the State Bank of India, with its headquarters in Mumbai, Maharashtra, is the largest commercial bank of India. It is not some public sector banking and financial services company but it is also classified as an Indian Multinational. -

Annual Report 2017-18

Annual Report 2017-18 Persistence is the Cornerstone of Success NEVER UNDERESTIMATE THE POWER OF PERSISTENCE here is an inherent strength in persistence. It can whittle down obstacles and Tchallenges like the way a river cuts through a rock, not because of its power but because of its persistence. Guided by a definite purpose, backed by a burning desire of achievement, steered by a clear-cut plan, persistence can open up any door closed by the resistance of problems. Results are simply inevitable. The ability to never give up, never lose faith and the loyalty towards being a part of the solution rather than the problem have been the providers of our success and progress over the past three decades. As one of India's leading Investment Banks and project advisers, we find ways not excuses to deliver cutting-edge solutions for our clients which, in turn has helped shape the Indian infrastructure story and contributed to nation building. While achieving this, the compelling reason for our victory over all odds has been our habit of persistence. We staunchly believe as long as we persist, we will be successful. ANNUAL REPORT 2017 - 2018 1 VISION To be the best India based Investment Bank. MISSION To provide credible, professional and customer focused world-class investment banking services. Persistent intent and determined action are an unbeatable combination for success. INDEX Board of Directors ..................................................................................................... 05 Awards & Rankings .................................................................................................. -

I. State Bank of India

COMPANY PROFILE I. STATE BANK OF INDIA OVERVIEW INTERNATIONAL PRESENCE HISTORY ASSOCIATE BANKS BRANCHES State Bank of India (SBI) (BSE: 500112, LSE: SBID) is the largest state- owned banking and financial services company in India, by almost every parameter - revenues, profits, assets, market capitalization, etc. The bank traces its ancestry to British India, through the Imperial Bank of India, to the founding in 1806 of the Bank of Calcutta, making it the oldest commercial bank in the Indian Subcontinent. Bank of Madras merged into the other two presidency banks, Bank of Calcutta and Bank of Bombay to form Imperial Bank of India, which in turn became State Bank of India. The Government of India nationalized the Imperial Bank of India in 1955, with the Reserve Bank of India taking a 60% stake, and renamed it the State Bank of India. In 2008, the Government took over the stake held by the Reserve Bank of India. SBI provides a range of banking products through its vast network of branches in India and overseas, including products aimed at NRIs. The State Bank Group, with over 16,000 branches, has the largest banking branch network in India. With an asset base of $352 billion and $285 billion in deposits, it is a regional banking behemoth. It has a market share among Indian commercial banks of about 20% in deposits and advances, and SBI accounts for almost one- fifth of the nation's loans. SBI has tried to reduce over-staffing by computerizing operations and "golden handshake" schemes that led to a flight of its best and brightest managers. -

Download a Mobile Wallet App on Our Phone NFC Contactless Payments

1 ACKNOWLEDGMENT The incredible activity of Team All India Legal Forum is to give a stage to the scholars from all through the country to get their unique work distributed in type of diaries is outstanding. This volume has been capably arranged by the group and has advanced vital and most most important aspects comes under Banking Law in India, Evolution of Banking Law, Structure of RBI, DRAT, Lok Adalats under legal services authority act, Securitization, Dishonour of cheques, Banking Regulation Act Amendment Bill 2020 and many more. At the very end of our publication it inludes the Multiple Choice Questions to quickly learn and revise along with some fun corners to not to get bored. We praise all the understudy benefactors for their superb piece of work and our all the best for all your future undertakings. We guarantee all the perusers that this will add a ton to the information subsequent to perusing this ideal assemblage of examination on the most recent consuming of the country. Truth be told its for the lawful clique as well as for any individual who has an interest in field of law and to know Banking System in India. With Best Wishes Ms Mahimashree Kaur ALL INDIA LEGAL FORUM 2 FOREWORD More has been aforesaid regarding the writing of lawyers and judges than of the other cluster, except, of course, poets and novelists. The distinction is that whereas the latter has sometimes been loved for their writing, the general public has nearly always damned lawyers and judges for theirs. If this state of affairs has modified in recent times, it's solely therein several lawyers and judges have currently joined the rest of the globe is repining regarding the standard of legal prose.