Comment Letter

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Washington DC Marriott Wardman Park Hotel Shipping Instructions

Washington DC Marriott Wardman Park Hotel Shipping Instructions PREPARING YOUR SHIPMENT FedEx Office is committed to providing you with an outstanding experience during your stay. All guest and event packages be- ing shipped to the property must follow the address label standards (illustrated below) to prevent package routing delays. Please schedule your shipment(s) to arrive four days prior to the event start date to avoid additional storage fees. Use the name of the recipient who will be on-site to receive and sign for the package(s). Please do not address shipments using property employee names, unless the items are specifically for their use (e.g., hotel specifications, rooming lists, or signed documents); this includes arranging for deliveries to all areas on the property. If a package has not been picked up by the recipient and no contact information is provided, the package will be returned to the sender, who will be responsible for all additional shipping fees. For more information on package retention, the Return to Sender process, or to schedule package deliveries, please contact the FedEx Office Business Center at 202.986.4028. Package deliver- ies should only be scheduled after the recipient has completed the check-in process. PACKAGE LABELING STANDARDS AND FEDEX OFFICE CONTACT (Guest Name) (Guest Cell Number) FedEx Office Business Center Operating Hours c/o FedEx Office at Washington DC Marriott Wardman Washington DC Marriott Mon – Fri: 7:00am - 7:00pm Park Hotel Wardman Park Hotel Saturday: Closed 2600 Woodley Road NW 2600 Woodley Road NW Sunday: Closed Washington, DC, 20008 Washington, DC 20008 (Convention / Conference / Group / Event Name) Phone: 202.986.4028 Box ____ of ____ Fax: 202.986.4728 Email: [email protected] SHIPMENTS WITH SPECIAL REQUIREMENTS Meeting and event planners, exhibitors and attendees are encouraged to contact FedEx Office in advance of shipping their items to Washington DC Marriott Wardman Park Hotel with any specific questions. -

UNITED STATES DISTRICT COURT NORTHERN DISTRICT of INDIANA SOUTH BEND DIVISION in Re FEDEX GROUND PACKAGE SYSTEM, INC., EMPLOYMEN

USDC IN/ND case 3:05-md-00527-RLM-MGG document 3279 filed 03/22/19 page 1 of 354 UNITED STATES DISTRICT COURT NORTHERN DISTRICT OF INDIANA SOUTH BEND DIVISION ) Case No. 3:05-MD-527 RLM In re FEDEX GROUND PACKAGE ) (MDL 1700) SYSTEM, INC., EMPLOYMENT ) PRACTICES LITIGATION ) ) ) THIS DOCUMENT RELATES TO: ) ) Carlene Craig, et. al. v. FedEx Case No. 3:05-cv-530 RLM ) Ground Package Systems, Inc., ) ) PROPOSED FINAL APPROVAL ORDER This matter came before the Court for hearing on March 11, 2019, to consider final approval of the proposed ERISA Class Action Settlement reached by and between Plaintiffs Leo Rittenhouse, Jeff Bramlage, Lawrence Liable, Kent Whistler, Mike Moore, Keith Berry, Matthew Cook, Heidi Law, Sylvia O’Brien, Neal Bergkamp, and Dominic Lupo1 (collectively, “the Named Plaintiffs”), on behalf of themselves and the Certified Class, and Defendant FedEx Ground Package System, Inc. (“FXG”) (collectively, “the Parties”), the terms of which Settlement are set forth in the Class Action Settlement Agreement (the “Settlement Agreement”) attached as Exhibit A to the Joint Declaration of Co-Lead Counsel in support of Preliminary Approval of the Kansas Class Action 1 Carlene Craig withdrew as a Named Plaintiff on November 29, 2006. See MDL Doc. No. 409. Named Plaintiffs Ronald Perry and Alan Pacheco are not movants for final approval and filed an objection [MDL Doc. Nos. 3251/3261]. USDC IN/ND case 3:05-md-00527-RLM-MGG document 3279 filed 03/22/19 page 2 of 354 Settlement [MDL Doc. No. 3154-1]. Also before the Court is ERISA Plaintiffs’ Unopposed Motion for Attorney’s Fees and for Payment of Service Awards to the Named Plaintiffs, filed with the Court on October 19, 2018 [MDL Doc. -

Terms and Conditions of Ground Service

Terms and Conditions of Ground Service Terms and Conditions of Ground Service The following paragraphs contain the general rules and regulations under which United Parcel Service ('UPS') is engaged in the transportation of small packages in its own territory and jointly through interchange with an affiliated United Parcel Service company. Commodities Handled and Restrictions on Service UPS holds itself out to transport general commodities, as usually defined, subject to the following restrictions: a. No service shall be rendered in the transportation of articles of unusual value. Articles having a value or declared value of more than $50,000 (U.S.) - $500 (U.S.) for packages containing jewelry - will not be accepted for transportation. The maximum liability assumed by UPS shall not exceed $100 (U.S.) regardless of the declaration of value in excess of $100 (U.S), provided that the shipper complies with the terms and conditions of the services hereby established. The maximum liability per package assumed by the applicable insurance company shall not exceed $50,000 (U.S.) - $500 (U.S.) for packages containing jewelry - regardless of the value in excess of the maximum, except for packages containing jewelry, in which case the maximum value or declared value per package is $500 (U.S.) per package and the maximum carrier liability per package is $500 (U.S.). b. No service shall be rendered in the transportation of any package or article weighing more than 150 pounds, or exceeding 108 inches in length, or exceeding a total of 130 inches in length and girth combined. Each package or article shall be considered as a separate and distinct shipment. -

MEMORANDUM OPINION and ORDER on MOTIONS Granting

Sanchez et al v. Lasership, Inc. Doc. 163 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF VIRGINIA ALEXANDRIA DIVISION MILTON MANUEL SANCHEZ, CARMELO MEDINA, GERARD EDMOND, individually and on behalf ofa group ofindividuals similarly situated, Plaintiffs, Case No. l:12-cv-246 (GBL/TRJ) v. LASERSHIP, INC., Defendant. MEMORANDUM OPINION AND ORDER THIS MATTER is before the Court on Defendant's Motion for Summary Judgment (Dkt. No. 114), Defendant's Motion to Strike Portions of Plaintiffs' Evidence in Opposition to Summary Judgment (Dkt. No. 131), Defendant's Motion to Strike Portions of Plaintiffs' Declarations Submitted in Support of Their Motion for Class Certification (Dkt. No. 106), Plaintiffs' Motion to Certify Class (Dkt. No. 79), Plaintiffs' Motion for Partial Summary Judgment (Dkt. No. 118), Defendant's Motion to Strike Plaintiffs' Notice of Supplemental Authority (Dkt. No. 138), and Defendant's Motion for Leave to File Surreply in Opposition to Plaintiffs' Motion for Partial Summary Judgment (Dkt. No. 157). This case concerns an action brought by a purported class of delivery truck drivers, seeking declaratory relief that they are misclassified under the Massachusetts Independent Contractor ("IC") Statute, M.G.L. 149 § 148B ("Section 148B"). The issue before the Court is whether the Court should grant Defendant Lasership's Motion for Summary Judgment, which seeks a determination that Section 148B, which would 1 Dockets.Justia.com compel Lasership to classify its independent contractors as employees, is preempted by the Federal Aviation Administration Authorization Act of 1994 ("FAAAA"). The Court grants summary judgment because enforcement ofSection 148B against motor carriers is preempted by the FAAAA. -

April 4–5 2019 Pennsylvania Convention Center, Philadelphia

6th Annual April 4–5 2019 Pennsylvania Convention Center, Philadelphia CO-LOCATED WITH FREE EXHIBITION TITLE SPONSORS OPENING TIMES THURSDAY APRIL 4 8:00 AM – 5:00 PM FRIDAY APRIL 5 8:00 AM – 2:00 PM ORGANISED BY REGISTER FREE www.terrapinn.com/homedelivery WELCOME 2 3 CONTENTS All-access vs Free Expo ......................... Page 4 Featured speakers .................................... Page 8 Home Delivery World 2019 All 325+ speakers ..................................... Page 10 Agenda highlights ................................... Page 18 Home Delivery World will gather 2,500 attendees representing retailers, grocers, distributors, manufacturers, city executives, supply chain professionals and carriers. Conference Agenda .................................. Page 32 Pre-conference Workshop ........................ Page 42 Our expo floor features seminar theaters covering 260+ topic areas including last mile Free Expo .................................................... Page 44 & returns, grocery eCommerce, cannabis eCommerce, city mobility, urban logistics, driver safety, freight planning, real estate site selection, transportation and more. Free Expo Highlights ................................. Page 46 Featured Seminar speakers ...................... Page 48 In partnership with Plug & Play Tech Center, we are bringing exciting new startups into Last Mile & Returns the spotlight. Frayt Technologies, Veho, 5 String Logistics, Ladingo, BoxLock, Nauto, Seminar Theater ........................................ Page 50 Truckblox and more, -

Guident Ltd Acquires Additional IP for Remote Control of Autonomous Vehicles and Drones to Enhance Safety

Guident Ltd Acquires Additional IP for Remote Control of Autonomous Vehicles and Drones to Enhance Safety For Immediate Release Silicon Valley, CA and London, U.K. / June 27th, 2019 / Guident Ltd, the developer of software apps for autonomous vehicles and drones announces it has acquired the exclusive intellectual property (IP) license to U.S. Patent No. 9,964,948 B2 entitled “Remote Control and Concierge Service for an Autonomous Transit Vehicle Fleet,” from Florida International University. This important patent describes methods for assisting Autonomous Vehicles (AV’s) by using their sensor inputs in coordination with a remote control center with the ability to operate a vehicle or drone from anywhere in the world. The Autonomous Vehicle (AV) can send its sensory input information to the control center in real-time and the control center operator can take over operation of the vehicle, enabling it to navigate in a variety of difficult situations such as heavy weather, crowded and dangerous traffic scenarios, accident prevention and remediation, and off-grid and last mile package delivery. “We are pleased to announce that Guident has acquired the exclusive license to U.S. Patent 9,964,948 B2. This patent deals with the operation and control of autonomous vehicles and drones and describes methods and systems for assisting these vehicles remotely, to increase safety and help to bridge the gap towards Level 5 autonomy,” said Harald Braun, Chairman of Guident. Remote-control AV simulation. Source: Guident Ltd, Vira Mylyan-Monastyrska and Ibnu Alias / Shutterstock.com Media News Press Release Exclusively for Client Guident ltd. Page 1 of 3 The autonomous vehicle market is expected to reach US $65 billion by 2027 and the drone logistics and transportation market is projected to reach US $29 billion by 2027, at a compound annual growth rate (CAGR) of 21% from 2022 to 2027. -

Hybrid Distribution Trucks: Costs and Benefits 6

Technical Report Documentation Page 1. Report No. 2. Government Accession No. 3. Recipient's Catalog No. SWUTC/11/476660-00080-1 4. Title and Subtitle 5. Report Date June 2011 Hybrid Distribution Trucks: Costs and Benefits 6. Performing Organization Code 7. Author(s) 8. Performing Organization Report No. Garrett Anderson and Rob Harrison Report 476660-00080-1 9. Performing Organization Name and Address 10. Work Unit No. (TRAIS) Center for Transportation Research University of Texas at Austin 11. Contract or Grant No. 1616 Guadalupe Street DTRS99-G-0006 Austin, TX 78701 12. Sponsoring Agency Name and Address 13. Type of Report and Period Covered Southwest Region University Transportation Center September 2010-June 2011 Texas Transportation Institute Texas A&M University System 14. Sponsoring Agency Code College Station, Texas 77843-3135 15. Supplementary Notes Supported by a grant from the U.S. Department of Transportation, University Transportation Centers Program. 16. Abstract The respective populations of the United States and Texas are expected to significantly increase over to the next several decades, primarily in urban and metropolitan areas. Economists have also predicted that oil prices will rise in real terms during the same period. Air quality is getting worse in a number of metropolitan areas, triggering non-attainment penalties and spurring an interest in cleaner transportation. Incentives and new policies must be adopted to increase the efficiency of the transportation system and thus move freight with a reduced impact on society and the environment. Hybrids can potentially help solve this issue through their increased fuel economy and reduced emissions. This project evaluated a package delivery truck, beverage delivery truck, and a refuse truck. -

Small-Package Delivery Services in Indonesia

OECD COMPETITION NEUTRALITY REVIEWS Small-package Delivery Services in Indonesia Highlights Competitive neutrality (state-owned and private businesses competing on a level playing field) ensures that all enterprises, public or private, domestic or foreign, face the same sets of rules. Ensuring a level playing field between public and private market participants leads therefore to more choice, higher quality and lower prices for consumers and ultimately benefits economic growth and development. This is why it is useful to assess the impact of SOEs on competition. The OECD was tasked by the ASEAN Secretariat and the ASEAN Expert Group on Competition, with funding from the ASEAN Economic Reform Programme under the UK Foreign, Commonwealth & Development Office (UK Government), to carry out an independent assessment of the impact of state-owned enterprises (SOEs) on competition in the small-package delivery services sector in ASEAN. The results of the assessment can help to promote a level playing field between SOEs and private entities in ASEAN and help detect special rights and privileges granted to SOEs that affect long-term growth and competitiveness. This document presents the highlights and main finding from the assessment and the full review is available at oe.cd/comp-asean. The review is the result of an assessment by the OECD based on an analysis of selected (prioritised) Indonesian legislation, interviews with stakeholders and desk research. The review took place in stages. Stage 1 served to determine the exact scope of the study. PT Pos Indonesia (Pos Indonesia) was identified as the relevant SOE, and the main laws and regulations and other SOE-related information were analysed. -

NEW YORK CITY LAW DEPARTMENT OFFICE of the CORPORATION COUNSEL Press Release

NEW YORK CITY LAW DEPARTMENT OFFICE OF THE CORPORATION COUNSEL Press Release Zachary W. Carter, Corporation Counsel nyc.gov/law For Immediate Release CITY REACHES $5 MILLION SETTLEMENT WITH LASERSHIP, INC., IN BOOTLEG CIGARETTE DELIVERY CASE CITY’S LAWSUIT CHARGED LASERSHIP, INC., WITH DELIVERING MORE THAN 45 TONS OF CONTRABAND CIGARETTES TO RESIDENTS OF THE FIVE BOROUGHS IN VIOLATION OF FEDERAL AND STATE LAW Contact: Media Office, New York City Law Department, [email protected] or (212) 356-4000 New York, N.Y., Sept. 24, 2014 – The New York City Law Department today announced the settlement of a lawsuit filed by the City against LaserShip, Inc., a Virginia-based package delivery service covering much of the East Coast, over residential deliveries of “untaxed” (e.g., contraband) cigarettes in New York City. LaserShip agreed to a payment of $5 million to resolve the City’s civil charges, brought under a variety of federal and state laws, including those prohibiting the distribution of untaxed cigarettes and residential cigarette deliveries. LaserShip also agreed to end all cigarette shipments and has strengthened its compliance practices. Corporation Counsel Zachary W. Carter said: “It should be clear by now that the City will vigorously pursue illegal cigarette deliveries by shipping companies that attempt to avoid City tax laws and circumvent laws designed to protect public health.” In July 2010, Congress enacted the Prevent All Cigarette Trafficking (PACT) Act, which, in addition to requiring cigarette sellers to ensure that all taxes had been paid on cigarettes shipped to consumers, prohibited the U.S. Postal Service from allowing cigarettes in the mails. -

1 United Parcel Service (UPS) Is Using Modern Technology to Revolutionize Supply Chain Management. the Shipping Company Is Expa

1 United Parcel Service (UPS) is using modern technology to revolutionize supply chain management. The shipping company is expanding its business to involve a symbiotic relationship between itself and any outside company that will integrate their technologies into their processes. UPS is growing its wireless, billing, freight and international technologies to truly offer a well rounded solution for any small to large company’s shipping and supply chain management requirements. Largely web-based the technology solutions simplify and increase cost efficiencies of any company. One of the best parts of the UPS software and product offerings is that companies can mix and match and add on any element that will benefit them. Supply chain management is an increasingly complex issue within companies, especially in today’s day and age. As companies increasingly need to compete on an international landscape UPS technologies are leveling the playing field. Wireless Technologies The United Parcel Service of America, Inc is constantly improving and implementing wireless technology around the world. These wireless technologies are strengthening the company’s value chain. UPS is the world’s largest package delivery company. The two related wireless technology topics that will be emphasized in this section are: wireless logistics and wireless solutions for customers. The pros and cons of deploying these technologies will be discussed, as well as the current competitive forces and corporate strategy. 2 UPS has already started its global roll-out of wireless technologies including: Bluetooth, Wi-Fi, and various cellular systems. Their plan for wireless logistical deployment started in Europe. These technologies are used in package sorting centers. -

HTS Systems Order Form

ORDER FORM 5 West Olive Plaza • Scranton, PA 18508 (1-866) 388-2102 • Phone or Fax: (570) 347-3878 HAND TRUCK TRANSPORT SOLUTIONS www.handtrucksystems.com • www.handtruckcarrier.com Shipping Method Shipping Address (Please Print Clearly) Attention:____________________________________________________Title:______________ ❑ UPS Next Day Air Company:_____________________________________________________________________ ❑ UPS 2nd Day Air Address:___________________________________________________M/S:_____________ ❑ UPS Ground City:_____________________________________Street:___________________________ ❑ FedEx Zip:_____________________________________Country:_________________________ ❑ DHL Phone: ( )________________________________Fax: ( )_________________________ ❑ Common Carrier E-Mail: _______________________________________________________________________ ❑ Other____________________________ Purchase Order Number:_________________________________________________________ Please provide the year, make and model of vehicle and truck body manufacturer. Special Instructions Vehicle: Year:__________________ Make:__________________ Model: _________________ ___________________________________ Body/Van: Year:__________________ Make:__________________ Model: ________________ ❑ ❑ ❑ ___________________________________ Vehicle Fuse Block ATO Standard ATM Mini Fuse Inline Fuse / M2 ___________________________________ Billing Address (If Different than Shipping Address) ___________________________________ Company:_____________________________________________________________________ -

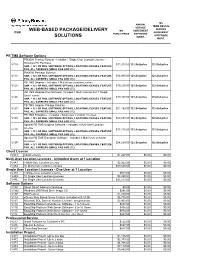

Finalrevised Pricebookdavidscopy

MS ANNUAL TERM RENTAL SERVICE SERVICE WEB-BASED PACKAGE/DELIVERY MS AGREEMENT ITEM AGREEMENT PURCH PRICE SOFTWARE SOFTWARE SOLUTIONS MAINT. MAINT. PB TMS Software Options PM3000 Turnkey System - Includes 1 Single User Location License - Requires PC Purchase V115 $11,013.00 12%list price 12%list price SMA = 12% OF PKG, SOFTWARE OPTIONS, LOCATION LICENSES, FEATURE PKG, ALL CARRIERS (SMALL PKG AND LTL) PM3000 Package Solution V118 SMA = 12% OF PKG, SOFTWARE OPTIONS, LOCATION LICENSES, FEATURE $16,945.00 12%list price 12%list price PKG, ALL CARRIERS (SMALL PKG AND LTL) PB TMS Uniprise - Includes 1 Multi-User Location License V125 SMA = 12% OF PKG, SOFTWARE OPTIONS, LOCATION LICENSES, FEATURE $15,250.00 12%list price 12%list price PKG, ALL CARRIERS (SMALL PKG AND LTL) PB TMS Uniprise Plus Software Includes 1 Multi-License and 1 Single User License V126 $19,407.00 12%list price 12%list price SMA = 12% OF PKG, SOFTWARE OPTIONS, LOCATION LICENSES, FEATURE PKG, ALL CARRIERS (SMALL PKG AND LTL) PB TMS Uniprise Pakage Solution V127 SMA = 12% OF PKG, SOFTWARE OPTIONS, LOCATION LICENSES, FEATURE $21,183.00 12%list price 12%list price PKG, ALL CARRIERS (SMALL PKG AND LTL) PB TMS Enterprise - Includes 2 Multi-User Location Licenses V135 SMA = 15% OF PKG, SOFTWARE OPTIONS, LOCATION LICENSES, FEATURE $29,658.00 12%list price 12%list price PKG, ALL CARRIERS (SMALL PKG AND LTL) Special PB TMS Uniprise Software - Includes 1 Multi-User Location License V12P $13,216.00 12%list price 12%list price SMA = 12% OF PKG, SOFTWARE OPTIONS, LOCATION LICENSES, FEATURE