Field Actions Science Reports, Special Issue 15

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

An Abstract of the Thesis Of

AN ABSTRACT OF THE THESIS OF Bryan R. Cobb for the degree of Master of Science in Mechanical Engineering presented on July 8, 2011 Title: Experimental Study of Impulse Turbines and Permanent Magnet Alternators for Pico-hydropower Generation Abstract Approved: Kendra V. Sharp Increasing access to modern forms of energy in developing countries is a crucial component to eliminating extreme poverty around the world. Pico-hydro schemes (less than 5-kW range) can provide environmentally sustainable electricity and mechanical power to rural communities, generally more cost-effectively than diesel/gasoline generators, wind turbines, or solar photovoltaic systems. The use of these types of systems has in the past and will continue in the future to have a large impact on rural, typically impoverished areas, allowing them the means for extended hours of productivity, new types of commerce, improved health care, and other services vital to building an economy. For this thesis, a laboratory-scale test fixture was constructed to test the operating performance characteristics of impulse turbines and electrical generators. Tests were carried out on a Pelton turbine, two Turgo turbines, and a permanent magnet alternator (PMA). The effect on turbine efficiency was determined for a number of parameters including: variations in speed ratio, jet misalignment and jet quality. Under the best conditions, the Turgo turbine efficiency was observed to be over 80% at a speed ratio of about 0.46, which is quite good for pico-hydro-scale turbines. The Pelton turbine was found to be less efficient with a peak of just over 70% at a speed ratio of about 0.43. -

Hydro, Tidal and Wave Energy in Japan Business, Research and Technological Opportunities for European Companies

Hydro, Tidal and Wave Energy in Japan Business, Research and Technological Opportunities for European Companies by Guillaume Hennequin Tokyo, September 2016 DISCLAIMER The information contained in this publication reflects the views of the author and not necessarily the views of the EU-Japan Centre for Industrial Cooperation, the views of the Commission of the European Union or Japanese authorities. While utmost care was taken to check and confirm all information used in this study, the author and the EU-Japan Centre may not be held responsible for any errors that might appear. © EU-Japan Centre for industrial Cooperation 2016 Page 2 ACKNOWLEDGEMENTS I would like to first and foremost thank Mr. Silviu Jora, General Manager (EU Side) as well as Mr. Fabrizio Mura of the EU-Japan Centre for Industrial Cooperation to have given me the opportunity to be part of the MINERVA Fellowship Programme. I also would like to thank my fellow research fellows Ines, Manuel, Ryuichi to join me in this six-month long experience, the Centre's Sam, Kadoya-san, Stijn, Tachibana-san, Fukura-san, Luca, Sekiguchi-san and the remaining staff for their kind assistance, support and general good atmosphere that made these six months pass so quickly. Of course, I would also like to thank the other people I have met during my research fellow and who have been kind enough to answer my questions and helped guide me throughout the writing of my report. Without these people I would not have been able to finish this report. Guillaume Hennequin Tokyo, September 30, 2016 Page 3 EXECUTIVE SUMMARY In the long history of the Japanese electricity market, Japan has often reverted to concentrating on the use of one specific electricity power resource to fulfil its energy needs. -

Renewable Energy Cost Analysis: Hydropower

IRENA International Renewable Energy Agency ER P A G P IN K R RENEWABLE ENERGY TECHNOLOGIES: COST ANALYSIS SERIES O IRENA W Volume 1: Power Sector Issue 3/5 Hydropower June 2012 Copyright © IRENA 2012 Unless otherwise indicated, material in this publication may be used freely, shared or reprinted, but acknowledgement is requested. About IRENA The International Renewable Energy Agency (IRENA) is an intergovernmental organisation dedi- cated to renewable energy. In accordance with its Statute, IRENA’s objective is to “promote the widespread and increased adoption and the sustainable use of all forms of renewable energy”. This concerns all forms of energy produced from renewable sources in a sustainable manner and includes bioenergy, geothermal energy, hydropower, ocean, solar and wind energy. As of May 2012, the membership of IRENA comprised 158 States and the European Union (EU), out of which 94 States and the EU have ratified the Statute. Acknowledgement This paper was prepared by the IRENA Secretariat. The paper benefitted from an internal IRENA review, as well as valuable comments and guidance from Ken Adams (Hydro Manitoba), Eman- uel Branche (EDF), Professor LIU Heng (International Center on Small Hydropower), Truls Holtedahl (Norconsult AS), Frederic Louis (World Bank), Margaret Mann (NREL), Judith Plummer (Cam- bridge University), Richard Taylor (IHA) and Manuel Welsch (KTH). For further information or to provide feedback, please contact Michael Taylor, IRENA Innovation and Technology Centre, Robert-Schuman-Platz 3, 53175 Bonn, Germany; [email protected]. This working paper is available for download from www.irena.org/Publications Disclaimer The designations employed and the presentation of materials herein do not imply the expression of any opinion whatsoever on the part of the Secretariat of the International Renewable Energy Agency concerning the legal status of any country, territory, city or area or of its authorities, or con- cerning the delimitation of its frontiers or boundaries. -

Analysis and Testing of the IPB Pico-Hydro Emulation Platform with Grid Connection

Analysis and Testing of the IPB Pico-hydro Emulation Platform with Grid Connection Gabriela Moreira Ribeiro Dissertation presented to the School of Technology and Management of Polytechnic Institute of Bragança to the fulfillment of the requirements for the Master of Science Degree in Industrial Engineering (Electrical Engineering branch), in the scope of double degree with Federal Center of Technological Education Celso Suckow da Fonseca - Rio de Janeiro Supervised by: Professor Ph.D. Américo Vicente Teixeira Leite Professor Ph.D. Aline Gesualdi Manhães Professor Ph.D. Ângela Paula Barbosa de Silva Ferreira Bragança 2019 ii Analysis and Testing of the IPB Pico-hydro Emulation Platform with Grid Connection Gabriela Moreira Ribeiro Dissertation presented to the School of Technology and Management of Polytechnic Institute of Bragança to the fulfillment of the requirements for the Master of Science Degree in Industrial Engineering (Electrical Engineering branch), in the scope of double degree with Federal Center of Technological Education Celso Suckow da Fonseca - Rio de Janeiro Supervised by: Professor Ph.D. Américo Vicente Teixeira Leite Professor Ph.D. Aline Gesualdi Manhães Professor Ph.D. Ângela Paula Barbosa de Silva Ferreira Bragança 2019 iv Dedication I dedicate this piece of dissertation to the Brazilian education system, in particular the Federal Center of Technological Education where I studied for many years of my life and which currently suffers severe attacks and attempts to dismantle it. v vi Acknowledgments I would like to thank my parents Carla Ribeiro and Marco Ribeiro, who concern about my physical and mental health. Also, for their daily efforts to provide all that they could not have during their childhood and youth. -

A Study on Developing Pico Propeller Turbine for Low Head Micro Hydropower Plants in Nepal

Journal of the Institute of Engineering, Vol. 9, No. 1, pp. 36–53 © TUTA/IOE/PCU TUTA/IOE/PCU All rights reserved. Printed in Nepal Fax: 977-1-5525830 A Study on Developing Pico Propeller Turbine for Low Head Micro Hydropower Plants in Nepal Pradhumna Adhikari, Umesh Budhathoki, Shiva Raj Timilsina, Saurav Manandhar, Tri Ratna Bajracharya Energy Systems Planning and Analysis Unit, Centre for Energy Studies, Institute of Engineering, Tribhuvan University, Nepal Corresponding Email: [email protected] Abstract: Most of the turbines used in Nepal are medium or high head turbines. These types of turbines are efficient but limited for rivers and streams in the mountain and hilly region which have considerably high head. Low head turbines should be used in the plain region if energy is to be extracted from the water sources there. This helps in the rural electrification and decentralized units in community, reducing the cost of construction of national grid and also to its dependency, in already aggravated crisis situation. There are good turbine designs for medium to high heads but traditional designs for heads under about 5m (i.e. cross flow turbine and waterwheel) are slow running, requiring substantial speed increase to drive an AC generator. Propeller turbines have a higher running speed but the airfoil blades are normally too complicated for micro hydro installations. Therefore, the open volute propeller turbine with constant thickness blades was ventured as possible solution. Such type of propeller turbine is designed to operate at low inlet head and high suction head. This enables the exclusion of closed spiral casing. -

The Pico Hydro Market in Vietnam

The Pico Hydro Market in Vietnam Oliver Paish, Dr John Green IT Power, The Manor House, Chineham Court, Lutyens Close Chineham, Hampshire RG24 8AG, UK Tel: +44 (0)1256 392700 Fax: +44 (0)1256 392701 Background The term ‘Pico’ hydro covers hydropower systems normally less than 2kW and certainly less than 5kW. The most common size range is 200-1000 Watts for domestic lighting and/or battery-charging. The units are small and cheap enough to be owned, installed and utilised by a single family, hence are also known as ‘family hydro’ units. Pico-hydro covers a range of turbine technologies, applicable to different heads. For example: • Tiny pelton wheels (‘Peltric’ sets) are being promoted in Nepal for sites with 20-50m head – only a hose-pipe is required for a penstock. • In the Philippines, tiny crossflow turbines (‘Fireflies’) are being trialled (5-20m head). • In the USA, Canada and Australia, a few companies offer a variation on the Turgo-turbine for medium and high head sites, principally to serve remote off-grid dwellings. • China and Vietnam have had the greatest success with low-head propeller turbines, suitable for only 1-2m head, and tiny turgo turbines for 5-20m head. Low-head sites (<5m) are by far the most widespread, available on irrigation canals as well as streams, and both in hilly and plain areas. These sites often avoid the political difficulties of crossing land outside the ownership of the family seeking to develop a scheme. Vietnam (>100,000 units) and China (>30,000 units per year) are the only countries to date where ‘family hydro’ technology has become widely available at affordable cost. -

Promoting Small-Scale Innovations to Meet the Energy Needs of the Poor Focusing on Developing Countries in South East Asia

IDRC Innovation, Technology and Society (ITS) Commissioned Paper, December 2010 Promoting Small-Scale Innovations to Meet the Energy Needs of the Poor Focusing on Developing Countries in South East Asia by Jacqueline Loh December 2010 Note: The opinions and recommendations expressed in this paper are solely those of the author and do not reflect the views of the International Development Research Centre (IDRC). 1 IDRC Innovation, Technology and Society (ITS) Commissioned Paper, December 2010 Table of Contents 1. Executive Summary ........................................................................................................................... 3 2. Introduction .......................................................................................................................................... 6 3. Background ......................................................................................................................................... 8 4. Energy use at the household level ................................................................................................ 12 5. Overview of rural energy options ................................................................................................... 14 6. Specific Technologies and Regional Case Studies: ................................................................... 18 Biogas .................................................................................................................................................... 18 Biomass Power Generation ............................................................................................................... -

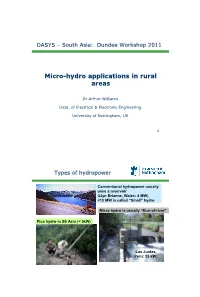

Micro-Hydro Applications in Rural Areas

OASYS – South Asia: Dundee Workshop 2011 Micro-hydro applications in rural areas Dr Arthur Williams Dept. of Electrical & Electronic Engineering University of Nottingham, UK 1 Types of hydropower Conventional hydropower usually uses a reservoir (Llyn Brianne, Wales: 4 MW) <10 MW is called “Small” hydro Micro hydro is usually “Run-of-river” Pico hydro in SE Asia (< 5kW) (Las Juntas, Peru: 25 kW) 2 Where are the potential sites? Hydropower usually uses the potential energy of water: mass flow × head × gravity Good sites either have high head Or high flow AKRSP, Pakistan Many good sites in remote rural areas 3 Rural Electrification Options Grid Connection • too expensive • unreliable, especially in mountainous areas Stand-alone options • rechargeable batteries • Solar Home Systems Mini-grid options Kushadevi - Nepal • diesel generators - site of a 3 kW Pico Hydro project • Pico Hydro 4 Rural Electrification Options Minimum 2006 World 300-1000 W Lower Range Bank study: hydroPico Probable Range Off-grid 300 W Costs. Wind Higher Range 300 W hybrid 2002 study in PV-Wind Kenya: Generator of Type PH: 15 ¢ 50 - 300 W Solar PV PV: >$1 300-1000 W Diesel Petrol or 0 10 20 30 40 50 60 70 80 Predicted Cost in 2010 (UScent/kWh) 5 Civil works for pico hydro Simple intake structures Kenya Kathamba, Storage only for evening use in dry season Minimal use of cement For higher head schemes, Polyethylene or PVC pipe is easily available and light to transport. Magdalena, Peru Magdalena, 6 Pico hydro turbine types • For higher heads: locally manufactured Pelton -

A Bizarre Design and Engineering Physics of Small/Micro and Pico/Family Hydro-Electric Power Plants/Farms

Available online www.jsaer.com Journal of Scientific and Engineering Research, 2016, 3(3):519-526 ISSN: 2394-2630 Research Article CODEN(USA): JSERBR A Bizarre Design and Engineering physics of small/micro and Pico/family hydro-electric power plants/farms Amajama Joseph Electronics & Computer Technology unit, Physics Department, University of Calabar, Nigeria Abstract The bizarre design and engineering physics of two kinds of small/medium/pico/family hydro-electric power generating plants/farms have been analysed. One utilizes a stream/river with a dam constructed so that the water falls from a height and turn a turbine while, the other maximizes the energy of a falling mass of water from a reservior at a particular height to also turn a turbine. The latter, in addition uses a solar pump to raise the water from a receptacle at the ground level back to the elevated reservior and it can also make use of a public water supply, running at high pressure to raise water to the reservior. Also, employing the relevant engineering physics, a mini power plant/farm has been designed with calculations on how to generate about then thousand watt (10000W) of electricity. Keywords Design, Engineering physics, Small/medium, Pico/family, hydro-electric power plant/farm. Introduction There are many sources of energy that are renewable and considered to be environmentally friendly and harness natural processes. These sources of energy provide an alternative cleaner source of energy that is not hazardous or harmful to the ecosystem. These power generation techniques are described as renewable since they are not depleting any resource to create their energy. -

Challenges Facing the Implementation of Pico-Hydropower Technologies

Williamson, S. J., Lubitz, W. D., Williams, A. A., Booker, J. D., & Butchers, J. P. (2019). Challenges Facing the Implementation of Pico- Hydropower Technologies. Journal of Sustainability Research, 2(1). https://doi.org/10.20900/jsr20200003 Publisher's PDF, also known as Version of record License (if available): CC BY Link to published version (if available): 10.20900/jsr20200003 Link to publication record in Explore Bristol Research PDF-document This is the final published version of the article (version of record). It first appeared online via Hapres at https://www.hapres.com/htmls/JSR_1137_Detail.html . Please refer to any applicable terms of use of the publisher. University of Bristol - Explore Bristol Research General rights This document is made available in accordance with publisher policies. Please cite only the published version using the reference above. Full terms of use are available: http://www.bristol.ac.uk/red/research-policy/pure/user-guides/ebr-terms/ sustainability.hapres.com Review Challenges Facing the Implementation of Pico-Hydropower Technologies Samuel J. Williamson 1,*, W. David Lubitz 2, Arthur A. Williams 3, Julian D. Booker 1, Joseph P. Butchers 1 1 Faculty of Engineering, University of Bristol, University Walk, Bristol, BS8 1TR, UK 2 School of Engineering, University of Guelph, 50 Stone. Rd. E., Guelph, ON, N1G 2W1, Canada 3 Department of Electrical and Electronic Engineering, University of Nottingham, University Park, Nottingham, NG7 2RD, UK * Correspondence: Samuel J. Williamson, Email: [email protected]; Tel.: +44-117-954-5177. ABSTRACT 840 million people living in rural areas across the world lack access to electricity, creating a large imbalance in the development potential between urban and rural areas. -

Start up of Manufacturing of Pico- and Micro Hydro Generators and Small

Project Name: Start up of Manufacturing of Pico- and Micro Hydro Generators and Small Wind Turbines Using a Patented Direct Driven Radial Flux, Permanent Magnet Generator, Republic of Panama. a) Organization leader data: Organization: Autoridad Nacional Address: Albrook, Edificio 804, del Ambiente (ANAM) Panama City, Republic of Panama Contact Person: Ing. Eduardo Reyes position: Sub-Administrador General de la Anam Phone 500-0800 E-mail: [email protected] Fax 500-0820 [email protected] b) Others Group member data: Organization: Luz Buena, SA Address: Antigua Estación del Contact Person: Ing. Heine Aven Ferrocarril, local no. 3 position: Gerente General Ancon, Panama City Phone: 232-7690 E-mail: [email protected] Fax: 232-7437 Organization: Phaesun, SA Address: Antigua Estación del Contact Person: Ing. Heine Aven Ferrocarril, local no. 2 position: Gerente General Ancon, Panama City Phone: 232-7927 E-mail: [email protected] Fax: 232-7437 Organization: Ing. Antonio Clement Address: Villa Las Cumbres, A-4 Alcalde Díaz, Ciudad Bolívar Contact Person: Ing. Antonio Clement position: Gerente General Telefax: 268-4819 E-mail: [email protected] Page 1 of 24 Table Of Contents 1.0 Executive Summary 3 1.1 Objectives 3 1.2 Activities 3 1.3 Results 4 2.0 Company Summary 5 2.2 Start-up Summary 6 3.0 Products 7 4.0 Market Analysis Summary 9 4.1 Market Segmentation 12 4.2 Target Market Segment Strategy 13 4.3 Industry Analysis 14 4.3.1 Competition and Buying Patterns 14 5.0 Strategy and Implementation Summary 15 5.1 Competitive Edge -

Suitability of Pico-Hydropower Technology for Addressing the Nigerian Energy Crisis – a Review

International Journal of Engineering Inventions e-ISSN: 2278-7461, p-ISSN: 2319-6491 Volume 4, Issue 9 [May 2015] PP: 17-40 Suitability of Pico-Hydropower Technology For Addressing The Nigerian Energy Crisis – A Review Alex Edeoja, Sunday Ibrahim, and Emmanuel Kucha Department of Mechanical Engineering, University of Agriculture, PMB 2373, Makurdi, Nigeria Abstract: - The energy crisis is global with various approaches being adopted by various regions of the world to tackle their peculiar situations. In Nigeria, several proposals and/or projections including rural electrification programmes have been made but they have largely remained in the pipeline like they say. The ragged energy mix in the country is literally at the mercy of saboteurs and the inexistent capacity to enforce environmental laws despite all the perceived and realistic global warming effects. The summary of all the approaches to the energy crisis is the development of smaller, smarter, decentralised systems and more efficient utilization of existing ones. These are less expensive, more environmentally benign and concede the control to the end user thereby reducing the exposure to influence of outsiders with whatever motivation. Among these category of energy systems is pico hydro technology. Most of the projections and hydropower activities do not directly consider this technology thereby excluding the majority of Nigerians living in the rural areas. However, an aggressive attention to the technology can contribute to the enhancement of the MDGs as well as Nigeria‘s vision 20 – 20 – 20 objectives. Farms and small and medium scale enterprises could be offered an ultimately cheaper and cleaner energy option over which they have more control.