Bulletin No. 2020–1 January 2, 2020 HIGHLIGHTS of THIS ISSUE

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Early Dance Division Calendar 17-18

Early Dance Division 2017-2018 Session 1 September 9 – November 3 Monday Classes Tuesday Classes September 11 Class September 12 Class September 18 Class September 19 Class September 25 Class September 26 Class October 2 Class October 3 Class October 9 Class October 10 Class October 16 Class October 17 Class October 23 Class October 24 Class October 30 Last Class October 31 Last Class Wednesday Classes Thursday Classes September 13 Class September 14 Class September 20 Class September 21* Class September 27 Class September 28 Class October 4 Class October 5 Class October 11 Class October 12 Class October 18 Class October 19 Class October 25 Class October 26 Class November 1 Last Class November 2 Last Class Saturday Classes Sunday Classes September 9 Class September 10 Class September 16 Class September 17 Class September 23 Class September 24 Class September 30* Class October 1 Class October 7 Class October 8 Class October 14 Class October 15 Class October 21 Class October 22 Class October 28 Last Class October 29 Last Class *Absences due to the holiday will be granted an additional make-up class. Early Dance Division 2017-2018 Session 2 November 4 – January 22 Monday Classes Tuesday Classes November 6 Class November 7 Class November 13 Class November 14 Class November 20 No Class November 21 No Class November 27 Class November 28 Class December 4 Class December 5 Class December 11 Class December 12 Class December 18 Class December 19 Class December 25 No Class December 26 No Class January 1 No Class January 2 No Class January 8 Class -

2021 7 Day Working Days Calendar

2021 7 Day Working Days Calendar The Working Day Calendar is used to compute the estimated completion date of a contract. To use the calendar, find the start date of the contract, add the working days to the number of the calendar date (a number from 1 to 1000), and subtract 1, find that calculated number in the calendar and that will be the completion date of the contract Date Number of the Calendar Date Friday, January 1, 2021 133 Saturday, January 2, 2021 134 Sunday, January 3, 2021 135 Monday, January 4, 2021 136 Tuesday, January 5, 2021 137 Wednesday, January 6, 2021 138 Thursday, January 7, 2021 139 Friday, January 8, 2021 140 Saturday, January 9, 2021 141 Sunday, January 10, 2021 142 Monday, January 11, 2021 143 Tuesday, January 12, 2021 144 Wednesday, January 13, 2021 145 Thursday, January 14, 2021 146 Friday, January 15, 2021 147 Saturday, January 16, 2021 148 Sunday, January 17, 2021 149 Monday, January 18, 2021 150 Tuesday, January 19, 2021 151 Wednesday, January 20, 2021 152 Thursday, January 21, 2021 153 Friday, January 22, 2021 154 Saturday, January 23, 2021 155 Sunday, January 24, 2021 156 Monday, January 25, 2021 157 Tuesday, January 26, 2021 158 Wednesday, January 27, 2021 159 Thursday, January 28, 2021 160 Friday, January 29, 2021 161 Saturday, January 30, 2021 162 Sunday, January 31, 2021 163 Monday, February 1, 2021 164 Tuesday, February 2, 2021 165 Wednesday, February 3, 2021 166 Thursday, February 4, 2021 167 Date Number of the Calendar Date Friday, February 5, 2021 168 Saturday, February 6, 2021 169 Sunday, February -

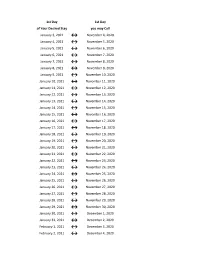

Flex Dates.Xlsx

1st Day 1st Day of Your Desired Stay you may Call January 2, 2022 ↔ November 3, 2021 January 3, 2022 ↔ November 4, 2021 January 4, 2022 ↔ November 5, 2021 January 5, 2022 ↔ November 6, 2021 January 6, 2022 ↔ November 7, 2021 January 7, 2022 ↔ November 8, 2021 January 8, 2022 ↔ November 9, 2021 January 9, 2022 ↔ November 10, 2021 January 10, 2022 ↔ November 11, 2021 January 11, 2022 ↔ November 12, 2021 January 12, 2022 ↔ November 13, 2021 January 13, 2022 ↔ November 14, 2021 January 14, 2022 ↔ November 15, 2021 January 15, 2022 ↔ November 16, 2021 January 16, 2022 ↔ November 17, 2021 January 17, 2022 ↔ November 18, 2021 January 18, 2022 ↔ November 19, 2021 January 19, 2022 ↔ November 20, 2021 January 20, 2022 ↔ November 21, 2021 January 21, 2022 ↔ November 22, 2021 January 22, 2022 ↔ November 23, 2021 January 23, 2022 ↔ November 24, 2021 January 24, 2022 ↔ November 25, 2021 January 25, 2022 ↔ November 26, 2021 January 26, 2022 ↔ November 27, 2021 January 27, 2022 ↔ November 28, 2021 January 28, 2022 ↔ November 29, 2021 January 29, 2022 ↔ November 30, 2021 January 30, 2022 ↔ December 1, 2021 January 31, 2022 ↔ December 2, 2021 February 1, 2022 ↔ December 3, 2021 1st Day 1st Day of Your Desired Stay you may Call February 2, 2022 ↔ December 4, 2021 February 3, 2022 ↔ December 5, 2021 February 4, 2022 ↔ December 6, 2021 February 5, 2022 ↔ December 7, 2021 February 6, 2022 ↔ December 8, 2021 February 7, 2022 ↔ December 9, 2021 February 8, 2022 ↔ December 10, 2021 February 9, 2022 ↔ December 11, 2021 February 10, 2022 ↔ December 12, 2021 February -

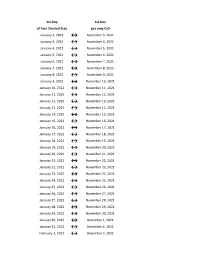

Flex Dates.Xlsx

1st Day 1st Day of Your Desired Stay you may Call January 3, 2021 ↔ November 4, 2020 January 4, 2021 ↔ November 5, 2020 January 5, 2021 ↔ November 6, 2020 January 6, 2021 ↔ November 7, 2020 January 7, 2021 ↔ November 8, 2020 January 8, 2021 ↔ November 9, 2020 January 9, 2021 ↔ November 10, 2020 January 10, 2021 ↔ November 11, 2020 January 11, 2021 ↔ November 12, 2020 January 12, 2021 ↔ November 13, 2020 January 13, 2021 ↔ November 14, 2020 January 14, 2021 ↔ November 15, 2020 January 15, 2021 ↔ November 16, 2020 January 16, 2021 ↔ November 17, 2020 January 17, 2021 ↔ November 18, 2020 January 18, 2021 ↔ November 19, 2020 January 19, 2021 ↔ November 20, 2020 January 20, 2021 ↔ November 21, 2020 January 21, 2021 ↔ November 22, 2020 January 22, 2021 ↔ November 23, 2020 January 23, 2021 ↔ November 24, 2020 January 24, 2021 ↔ November 25, 2020 January 25, 2021 ↔ November 26, 2020 January 26, 2021 ↔ November 27, 2020 January 27, 2021 ↔ November 28, 2020 January 28, 2021 ↔ November 29, 2020 January 29, 2021 ↔ November 30, 2020 January 30, 2021 ↔ December 1, 2020 January 31, 2021 ↔ December 2, 2020 February 1, 2021 ↔ December 3, 2020 February 2, 2021 ↔ December 4, 2020 1st Day 1st Day of Your Desired Stay you may Call February 3, 2021 ↔ December 5, 2020 February 4, 2021 ↔ December 6, 2020 February 5, 2021 ↔ December 7, 2020 February 6, 2021 ↔ December 8, 2020 February 7, 2021 ↔ December 9, 2020 February 8, 2021 ↔ December 10, 2020 February 9, 2021 ↔ December 11, 2020 February 10, 2021 ↔ December 12, 2020 February 11, 2021 ↔ December 13, 2020 -

Julian Date Cheat Sheet for Regular Years

Date Code Cheat Sheet For Regular Years Day of Year Calendar Date 1 January 1 2 January 2 3 January 3 4 January 4 5 January 5 6 January 6 7 January 7 8 January 8 9 January 9 10 January 10 11 January 11 12 January 12 13 January 13 14 January 14 15 January 15 16 January 16 17 January 17 18 January 18 19 January 19 20 January 20 21 January 21 22 January 22 23 January 23 24 January 24 25 January 25 26 January 26 27 January 27 28 January 28 29 January 29 30 January 30 31 January 31 32 February 1 33 February 2 34 February 3 35 February 4 36 February 5 37 February 6 38 February 7 39 February 8 40 February 9 41 February 10 42 February 11 43 February 12 44 February 13 45 February 14 46 February 15 47 February 16 48 February 17 49 February 18 50 February 19 51 February 20 52 February 21 53 February 22 54 February 23 55 February 24 56 February 25 57 February 26 58 February 27 59 February 28 60 March 1 61 March 2 62 March 3 63 March 4 64 March 5 65 March 6 66 March 7 67 March 8 68 March 9 69 March 10 70 March 11 71 March 12 72 March 13 73 March 14 74 March 15 75 March 16 76 March 17 77 March 18 78 March 19 79 March 20 80 March 21 81 March 22 82 March 23 83 March 24 84 March 25 85 March 26 86 March 27 87 March 28 88 March 29 89 March 30 90 March 31 91 April 1 92 April 2 93 April 3 94 April 4 95 April 5 96 April 6 97 April 7 98 April 8 99 April 9 100 April 10 101 April 11 102 April 12 103 April 13 104 April 14 105 April 15 106 April 16 107 April 17 108 April 18 109 April 19 110 April 20 111 April 21 112 April 22 113 April 23 114 April 24 115 April -

Pay Date Calendar

Pay Date Information Select the pay period start date that coincides with your first day of employment. Pay Period Pay Period Begins (Sunday) Pay Period Ends (Saturday) Official Pay Date (Thursday)* 1 January 10, 2016 January 23, 2016 February 4, 2016 2 January 24, 2016 February 6, 2016 February 18, 2016 3 February 7, 2016 February 20, 2016 March 3, 2016 4 February 21, 2016 March 5, 2016 March 17, 2016 5 March 6, 2016 March 19, 2016 March 31, 2016 6 March 20, 2016 April 2, 2016 April 14, 2016 7 April 3, 2016 April 16, 2016 April 28, 2016 8 April 17, 2016 April 30, 2016 May 12, 2016 9 May 1, 2016 May 14, 2016 May 26, 2016 10 May 15, 2016 May 28, 2016 June 9, 2016 11 May 29, 2016 June 11, 2016 June 23, 2016 12 June 12, 2016 June 25, 2016 July 7, 2016 13 June 26, 2016 July 9, 2016 July 21, 2016 14 July 10, 2016 July 23, 2016 August 4, 2016 15 July 24, 2016 August 6, 2016 August 18, 2016 16 August 7, 2016 August 20, 2016 September 1, 2016 17 August 21, 2016 September 3, 2016 September 15, 2016 18 September 4, 2016 September 17, 2016 September 29, 2016 19 September 18, 2016 October 1, 2016 October 13, 2016 20 October 2, 2016 October 15, 2016 October 27, 2016 21 October 16, 2016 October 29, 2016 November 10, 2016 22 October 30, 2016 November 12, 2016 November 24, 2016 23 November 13, 2016 November 26, 2016 December 8, 2016 24 November 27, 2016 December 10, 2016 December 22, 2016 25 December 11, 2016 December 24, 2016 January 5, 2017 26 December 25, 2016 January 7, 2017 January 19, 2017 1 January 8, 2017 January 21, 2017 February 2, 2017 2 January -

2021 Calendar Campaign

One Tail at a Time 2021 Calendar Pets Date Status Date Status Date Status Date Status Date Status Date Status Date Status Date Status Friday, January 1 Not Available Saturday, February 20 Not Available Sunday, April 11 Available Monday, May 31 Not Available Tuesday, July 20 Available Wednesday, September 8 Not Available Thursday, October 28 Available Thursday, December 16 Available Saturday, January 2 Available Sunday, February 21 Available Monday, April 12 Not Available Tuesday, June 1 Available Wednesday, July 21 Not Available Thursday, September 9 Available Friday, October 29 Available Friday, December 17 Available Sunday, January 3 Available Monday, February 22 Available Tuesday, April 13 Available Wednesday, June 2 Available Thursday, July 22 Not Available Friday, September 10 Available Saturday, October 30 Available Saturday, December 18 Not Available Monday, January 4 Available Tuesday, February 23 Available Wednesday, April 14 Available Thursday, June 3 Available Friday, July 23 Available Saturday, September 11 Available Sunday, October 31 Not Available Sunday, December 19 Available Tuesday, January 5 Available Wednesday, February 24 Available Thursday, April 15 Not Available Friday, June 4 Available Saturday, July 24 Available Sunday, September 12 Available Monday, November 1 Available Monday, December 20 Available Wednesday, January 6 Available Thursday, February 25 Available Friday, April 16 Not Available Saturday, June 5 Available Sunday, July 25 Available Monday, September 13 Available Tuesday, November 2 Available Tuesday, -

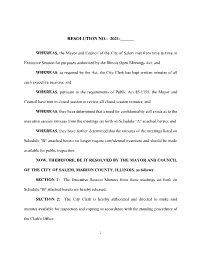

Resolution No.: 2021-______

RESOLUTION NO.: 2021-______ WHEREAS, the Mayor and Council of the City of Salem met from time to time in Executive Session for purposes authorized by the Illinois Open Meetings Act; and WHEREAS, as required by the Act, the City Clerk has kept written minutes of all such executive sessions; and WHEREAS, pursuant to the requirements of Public Act 85-1355, the Mayor and Council have met in closed session to review all closed session minutes; and WHEREAS, they have determined that a need for confidentiality still exists as to the executive session minutes from the meetings set forth on Schedule "A" attached hereto; and WHEREAS, they have further determined that the minutes of the meetings listed on Schedule "B" attached hereto no longer require confidential treatment and should be made available for public inspection; NOW, THEREFORE, BE IT RESOLVED BY THE MAYOR AND COUNCIL OF THE CITY OF SALEM, MARION COUNTY, ILLINOIS, as follows: SECTION 1: The Executive Session Minutes from those meetings set forth on Schedule "B" attached hereto are hereby released. SECTION 2: The City Clerk is hereby authorized and directed to make said minutes available for inspection and copying in accordance with the standing procedures of the Clerk's Office. 1 SECTION 3: This Resolution shall be in full force and effect from and after its passage. IN WITNESS WHEREOF, I have hereunto set my hand and caused the seal of the City of Salem, Illinois, to be affixed this 6th day of July, 2021. CITY OF SALEM, ILLINOIS MAYOR ATTEST: CITY CLERK 2 SCHEDULE A EXECUTIVE SESSION -

Date of Close Contact Exposure

Date of Close Contact Exposure 7 days 10 days 14 days Monday, November 16, 2020 Tuesday, November 24, 2020 Friday, November 27, 2020 Tuesday, December 1, 2020 Tuesday, November 17, 2020 Wednesday, November 25, 2020 Saturday, November 28, 2020 Wednesday, December 2, 2020 Wednesday, November 18, 2020 Thursday, November 26, 2020 Sunday, November 29, 2020 Thursday, December 3, 2020 Thursday, November 19, 2020 Friday, November 27, 2020 Monday, November 30, 2020 Friday, December 4, 2020 Friday, November 20, 2020 Saturday, November 28, 2020 Tuesday, December 1, 2020 Saturday, December 5, 2020 Saturday, November 21, 2020 Sunday, November 29, 2020 Wednesday, December 2, 2020 Sunday, December 6, 2020 Sunday, November 22, 2020 Monday, November 30, 2020 Thursday, December 3, 2020 Monday, December 7, 2020 Monday, November 23, 2020 Tuesday, December 1, 2020 Friday, December 4, 2020 Tuesday, December 8, 2020 Tuesday, November 24, 2020 Wednesday, December 2, 2020 Saturday, December 5, 2020 Wednesday, December 9, 2020 Wednesday, November 25, 2020 Thursday, December 3, 2020 Sunday, December 6, 2020 Thursday, December 10, 2020 Thursday, November 26, 2020 Friday, December 4, 2020 Monday, December 7, 2020 Friday, December 11, 2020 Friday, November 27, 2020 Saturday, December 5, 2020 Tuesday, December 8, 2020 Saturday, December 12, 2020 Saturday, November 28, 2020 Sunday, December 6, 2020 Wednesday, December 9, 2020 Sunday, December 13, 2020 Sunday, November 29, 2020 Monday, December 7, 2020 Thursday, December 10, 2020 Monday, December 14, 2020 Monday, November -

2 3 2 2 2 2 2 2 2 2 2 2 2 3 2 3 2 2 2 2 3 2 2 2 2 3 2 2 2 2 2015

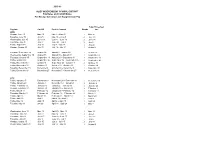

2015-16 ALIEF INDEPENDENT SCHOOL DISTRICT Pay Dates and Cut-Off Dates For Hourly, Substitute and Supplemental Pay Supp/Timesheet Paydate Cut Off Period Covered Weeks due 2015 Monday, June 15 May 15 May 2 – May 15 2 May 20 Tuesday, June 30 June 5 May 16 – June 5 3 June 10 Wednesday, July 15 June 19 June 6 – June 19 2 June 24 Thursday, July 30 July 3 June 20 – July 3 2 July 8 Friday, August 14 July 17 July 4 - July 17 2 July 22 Monday, August 31 July 31 July 18 - July 31 2 August 5 Tuesday, September 15 August 14 August 1 – August 14 2 August 19 Wednesday, September 30 August 28 August 15 – August 28 2 September 2 Thursday, October 15 September 11 August 29 – September 11 2 September 16 Friday, October 30 September 25 September 12 – September 25 2 September 30 Friday, November 13 October 9 September 26 – October 9 2 October 14 Friday, November 20 October 23 October 10 – October 23 2 October 28 Tuesday, December 15 November 6 October 24 – November 6 2 November 11 Friday, December 18 November 27 November 7 – November 27 3 December 2 2016 Friday, January 15 December 11 November 28 – December 11 2 December 16 Friday, January 29 January 1 December 12 – January 1 3 January 6 Friday, February 12 January 15 January 2 – January 15 2 January 20 Monday, February 29 January 29 January 16 – January 29 2 February 3 Friday, March 11 February 12 January 30 – February 12 2 February 17 Thursday, March 31 February 26 February 13 – February 26 2 March 2 Friday, April 15 March 18 February 27 – March 18 3 March 23 Friday, April 29 April 1 March 19 – April 1 2 April 6 Friday, May 13 April 15 April 2 – April 15 2 April 20 Tuesday, May 31 29-Apr April 16 – April 29 2 May 4 Wednesday, June 15 May 13 April 30 – May 13 2 May 18 Thursday, June 30 June 3 May 14 – June 3 3 June 8 Thursday, July 14 June 17 June 4 – June 17 2 June 22 Thursday, July 28 July 1 June 18 – July 1 2 July 6 Monday, August 15 July 15 July 2 - July 15 2 July 20 Wednesday, August 31 July 29 July 16 - July 29 2 August 3 . -

SPRING 2010 CALENDAR • January 19 – May 25

SPRING 2010 CALENDAR • January 19 – May 25 August 2009 August 3 - 19 Spring 2010 Intersession Registration via CSU X-press November 2009 November 11 – December 2 Advance Spring 2010 Registration via CSU X-press December 2009 December 1 - 2 Advance Spring 2010 Registration via CSU X-press continues December 16 – January 15 Intersession Course Period December 16 – January 13 Spring 2010 Registration / Change of Program – (See Quick View for payment information.) December 17 Fall 2009 Commencement Ceremony (6p.m.) Emil & Patricia A. Jones Convocation Center December 24 – 25 (R-F) HOLIDAY – Christmas – No Intersession classes December 31 (R) HOLIDAY – New Year’s Day – No Intersession classes January 2010 January 1 (F) HOLIDAY – New Year’s Day – No Intersession classes January 2 – 15 Intersession Course Period continues January 1 – 13 Spring 2010 Registration / Change of Program continues – (See Quick View for payment information.) January 14-15 (R-F) NO REGISTRATION January 16-18 (S-M) Spring 2010 registration resumes January 18 (M) HOLIDAY – Martin Luther King Jr.’s Birthday – No classes January 19 (T) All day/evening on-campus, extension, and online classes begin January 19–20(T-W) Late registration period ($100.00 late fee charged); late change of program - (via CSU X-press) January 23 (S) Saturday on-campus classes begin February 2010 February 2 (T) Deadline for 100% refund of refundable fees upon complete withdrawal from all courses February 2 (T) Deadline for partial refund of refundable fees for formally reducing credit hour load below 12 semester hours for all courses February 5 (F) Deadline for requesting cancellation of student health insurance coverage for Spring 2010 February 15 (M) HOLIDAY – President’s Day – No classes February 16 (T) Deadline for 50% refund of refundable fees upon withdrawal from ALL courses. -

07 Fulkerson 2022-WECC Preschedule Calendar Version

2022 WECC Scheduling Calendar Approved Scheduling Days New Year’s Day (Observed) Friday December 31, 2021 Martin Luther King Day Monday January 17, 2022 President’s Day Monday February 21, 2022 Good Friday Friday April 15, 2022 Memorial Day Monday May 30, 2022 Independence Day Monday July 4, 2022 New Month - August Monday August 1, 2022 Labor Day Monday September 5, 2022 New Month- October Saturday October 1, 2022 Veteran’s Day Friday November 11, 2022 Thanksgiving Thursday November 24, 2022 Day after Thanksgiving Friday November 25, 2022 Christmas Eve (Observed) Friday December 23, 2022 Christmas Day (Observed) Monday December 26, 2022 New Year’s Day (Observed) Monday January 2, 2023 New Year’s Day (Observed)—Friday, December 31, 2021 Wednesday, December 29—Preschedule Thursday-Friday, December 30-31 (2) Thursday, December 30—Preschedule Saturday-Monday, January 1-3, 2022 (3) Martin Luther King’s Birthday—Monday, January 17, 2022 Wednesday, January 12—Preschedule for Thursday-Friday January 13-14 (2) Thursday, January 13—Preschedule for Saturday-Sunday January 15-16 (2) Friday, January 14—Preschedule for Monday-Tuesday, January 17-18 (2) President’s Day—Monday, February 21, 2022 Wednesday, February 16—Preschedule for Thursday-Friday, February 17-18 (2) Thursday, February 17—Preschedule for Saturday-Sunday, February 19-20 (2) Friday, February 18—Preschedule for Monday-Tuesday, February 21-22 (2) Good Friday—Friday, April 15, 2022 Tuesday, April 12—Preschedule for Wednesday-Thursday, April 13-14 (2) Wednesday, April 13—Preschedule for