Financial Proforma

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Marriott International Annual Report 2019

Marriott International Annual Report 2019 Form 10-K (NASDAQ:MAR) Published: March 1st, 2019 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended December 31, 2018 or o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File No. 1-13881 MARRIOTT INTERNATIONAL, INC. (Exact name of registrant as specified in its charter) Delaware 52-2055918 (State or other jurisdiction of (IRS Employer incorporation or organization) Identification No.) 10400 Fernwood Road, Bethesda, Maryland 20817 (Address of Principal Executive Offices) (Zip Code) Registrant’s Telephone Number, Including Area Code (301) 380-3000 Securities registered pursuant to Section 12(b) of the Act: Title of Each Class Name of Each Exchange on Which Registered Class A Common Stock, $0.01 par value Nasdaq Global Select Market (339,668,839 shares outstanding as of February 20, 2019) Chicago Stock Exchange Securities registered pursuant to Section 12(g) of the Act: NONE Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in rule 405 of the Securities Act. Yes ý No o Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Data Standards Manual Summary of Changes

October 2019 Visa Public gfgfghfghdfghdfghdfghfghffgfghfghdfghfg This document is a supplement of the Visa Core Rules and Visa Product and Service Rules. In the event of any conflict between any content in this document, any document referenced herein, any exhibit to this document, or any communications concerning this document, and any content in the Visa Core Rules and Visa Product and Service Rules, the Visa Core Rules and Visa Product and Service Rules shall govern and control. Merchant Data Standards Manual Summary of Changes Visa Merchant Data Standards Manual – Summary of Changes for this Edition This is a global document and should be used by members in all Visa Regions. In this edition, details have been added to the descriptions of the following MCCs in order to facilitate easier merchant designation and classification: • MCC 5541 Service Stations with or without Ancillary Services has been updated to include all engine fuel types, not just automotive • MCC 5542 Automated Fuel Dispensers has been updated to include all engine fuel types, not just automotive • MCC 5812 Eating Places, Restaurants & 5814 Fast Food Restaurants have been updated to include greater detail in order to facilitate easier segmentation • MCC 5967 Direct Marketing – Inbound Telemarketing Merchants has been updated to include adult content • MCC 6540 Non-Financial Institutions – Stored Value Card Purchase/Load has been updated to clarify that it does not apply to Staged Digital Wallet Operators (SDWO) • MCC 8398 Charitable Social Service Organizations has -

List of Tax Reform Good News

List of Tax Reform Good News 1,200 examples of pay raises, charitable donations, special bonuses, 401(k) match hikes, business expansions, benefit increases, and utility rate reductions attributed to the Tax Cuts and Jobs Act As of August 17, 2020. Please send any additions to this list to John Kartch at [email protected] This list and all 50 state lists are constantly updated – please access this national list and all 50 state lists at www.atr.org/list A 1A Auto, Inc. (Westford, Massachusetts) -- Bonuses for all full-time employees: Massachusetts based online auto parts retailer 1A Auto announced across the board cash bonuses for all full-time employees. CEO Rick Green says that the decision was based on recent changes to tax policy. In a company meeting Wednesday, Green told employees, "Ultimately the tax savings will be passed to our customers in the form of lower prices, but we want to also share some of the savings with you, our hard-working employees." Jan. 25, 2018 1A Auto, Inc. press release 2nd South Market (Twin Falls, Idaho) -- A food hall is opening because of the TCJA Opportunity Zone program, and is slated to create new jobs: One of the nation’s fastest-growing trends, food halls, is coming to Twin Falls. 2nd South Market, slated to open this summer, will be housed in the historic 1926 downtown Twin Falls building formerly occupied by the Salvation Army. 2ndSouth Market will be the first Opportunity Zone project to open in Idaho and the state’s third Opportunity Zone investment. -

2018 Hotel Brand Reputation Rankings: USA & Canada

REPORT 2018 Hotel Brand Reputation Rankings: USA & Canada October 2018 INDEX Introduction 4 Methodology 6 The Importance of Brand Reputation 7 Key Data Points: All Chain Scales 8 Key Findings 9 Summary of Top Performers 10 ECONOMY BRANDS Overview 13 Top 25 Branded Economy Hotels 14 Economy Brand Ranking 15 Economy Brand Ranking by Improvement 16 Economy Brand Ranking by Service 17 Economy Brand Ranking by Value 18 Economy Brand Ranking by Rooms 19 Economy Brand Ranking by Cleanliness 20 Review Sources: Economy Brands 21 Country Indexes: Economy Brands 22 Response Rates: Economy Brands 22 Semantic Mentions: Economy Brands 23 MIDSCALE BRANDS Overview 24 Top 25 Branded Midscale Hotels 25 Midscale Brand Ranking 26 Midscale Brand Ranking by Improvement 27 Midscale Brand Ranking by Service 28 Midscale Brand Ranking by Value 29 Midscale Brand Ranking by Rooms 30 Midscale Brand Ranking by Cleanliness 31 Review Sources: Midscale Brands 32 Country Indexes: Midscale Brands 33 Response Rates: Midscale Brands 33 Semantic Mentions: Midscale Brands 34 UPPER MIDSCALE BRANDS Overview 35 Top 25 Branded Upper Midscale Hotels 36 Upper Midscale Brand Ranking 37 Upper Midscale Brand Ranking by Improvement 38 Upper Midscale Brand Ranking by Service 39 Upper Midscale Brand Ranking by Value 40 Upper Midscale Brand Ranking by Rooms 41 Upper Midscale Brand Ranking by Cleanliness 42 Review Sources: Upper Midscale Brands 43 Country Indexes: Upper Midscale Brands 44 Response Rates: Upper Midscale Brands 44 Semantic Mentions: Upper Midscale Brands 45 Index www.reviewpro.com -

Proposed Downtown Berryville Hotel

Proposed Downtown Berryville Hotel Berryville, Virginia 22611-1315 NKF Job No.: 19-0004412 Feasibility Study Prepared For: Mr. Nathan Stalvey President Berryville Main Street 23 East Main Street Berryville, VA 22611-1315 Prepared By: Newmark Knight Frank Hospitality, Gaming & Leisure Group Valuation & Advisory 1350 Euclid Avenue, Suite 300 Cleveland, OH 44115 1350 Euclid Avenue, Suite 300 Cleveland, OH 44115 July 19, 2019 Mr. Nathan Stalvey President Berryville Main Street 23 East Main Street Berryville, VA 22611-1315 RE: Feasibility Study of a Proposed Downtown Berryville Hotel Downtown Berryville , Berryville, Virginia NKF Job No.: 19-0004412 Newmark Knight Frank Valuation & Advisory, LLC has prepared a feasibility study of the referenced property in the following report. Summary of the Proposed Subject Property The feasibility study considers development of a proposed hotel in Downtown Berryville on or proximate to Main Street. The subject site has average access to major roadway (State Route 7) because of its proposed location in downtown Berryville's Main Street district, limiting its visibility and ease of ingress and egress from a major roadway. While the proposed site is proximate to some demand generators, the low density of commercial developments in the area is projected to be a weakness. Leisure attractions in Berryville and Clarke County including vineyards, historic manors and event venues, and Barns of Rose Hill will help mitigate this weakness. Visibility is considered to be average, relative to other historic downtown locations, due to its proposed multi- level configuration, assumed signage, and on or proximate to Main Street. State Route 7, which connects Berryville to neighboring Winchester and Leesburg, is less than a mile north from central downtown. -

Back INN Style?

HYLodging2002.qxd 1/16/02 12:54 PM Page 3 High Yield Lodging Research January 2002 High Yield Lodging Outlook 2002 Back INN Style? Jason N. Ader (212) 272-4257 Jason M. Kroll CFA (212) 272-9621 Trip McCoy (212) 272-8821 High Yield Lodging Outlook 2002 January 18, 2002 Table of Contents Investment Thesis .............................................................................................. 4 Is the Lodging Industry Poised for a Turnaround?.................................................... 5 What is the Credit Outlook?................................................................................ 10 How Are Current Trends? ................................................................................... 13 Relative Value Analysis...................................................................................... 15 Company Updates Boca Resorts, Inc.............................................................................................. 17 Extended Stay America, Inc................................................................................. 24 FelCor Lodging Trust .......................................................................................... 34 Host Marriott, LP .............................................................................................. 45 MeriStar Hospitality Corp. ................................................................................... 56 Prime Hospitality Corp........................................................................................ 66 Starwood Hotels & Resorts -

City of Sydney 2018

Tourist Accommodation Register TA category Historic Property Establishment name & location Key type & No Original Building & other Pre-TA uses AR Dates & Ages Prior history TARC : Current : City of Sydney 2018 & type Records Street TA TA TAC VAM LAB Sands LC ANU Key HT PB SA BP Original Use AR TAC Pre-AR AR Establishment Name Main Street Name Other Street frontages Suburb PC V Built Pre-TA uses Building(s) demolishd Other TA idenitities No Cat Type Type 2016 1986 1933 Plans T&C type Rooms Rooms Units Beds sector Type Date Date Age Age 2019 ARB : Adaptive Reuse Backpacker hostels 790 on George St 790-798 George St Rawson St (1-9) & Rawson Lane Haymarket 2000 2 AR BP 69 x Beds 281 1914 Commercial Office Building (Station House ) 2007 93 12 Asylum Sydney 201-203 Brougham St Woolloomooloo 2011 8 AR BP 159 x Beds 92 1848 Residential 2 terrace houses 1988 140 31 1990 Backpacker to Boarding House Base Backpackers 477-481 Kent St Sydney 2000 1 AR BP 9 x Beds 492 1917 Industrial Warehouse & offices (Civic House) 2001 84 18 Wanderers on Kent Big Hostel 212-214 Elizabeth St Blackburn St Surry Hills 2010 3 AR BP 115 x Beds 137 1918 Commercial Offices (Anker House) 2002 84 17 Residence ( Craigholme ), Boarding House Blue Parrot Backpackers 87 Macleay St Potts Point 2011 8 AR BP 173 x Beds 50 1891 Residential 2001 110 18 (queried by some locals), Shops & Restaurant Film exchange ( MGM); dental school. Part of Bounce Sydney 20-28 Chalmers St Randle Lane Surry Hills 2010 3 AR BP 113 x Beds 163 1933 Miscellaneous 2010 77 9 dental hospital Casa Central -

Hotel Destinations Asia Pacific 1 Hotel Destinations – Asia Pacific

Hotels & Hospitality Group | May 2017 Hotel Destinations Asia Pacific 1 Hotel Destinations – Asia Pacific Auckland Quick Facts OCC ADR RevPAR International Visitor Arrivals (NZ 2016) Number of New Rooms (2017) 86.6% NZD 191 NZD 166 3.5 million 663 rooms Tourism Demand New notable hotels Auckland International Airport, which is the Auckland reported an average occupancy ‘gateway’ for Auckland and New Zealand level of 86.6% for the period year ending Jet Inn Extension, overseas visitors, has experienced strong March 2017, the highest occupancy level on Auckland International Airport growth. For the period YTD December record in over 20 years. Auckland’s market 60 rooms 2016, total passenger movements have occupancy has risen every year since 2010, increased 12% with an increase recorded in after reaching a post-GFC low of 69.5% in Swiss-Belsuites Victoria Park domestic passenger movements, up 12.5% 2009. FIT and Corporate business dominate 40 rooms and international passengers increasing the business mix of Auckland hotels by 11.5%. International visitor arrivals to contributing 47.5% and 20.5% of hotel guest New Zealand reached 3.5 million for the nights respectively, y-o-y to March 2017. period year ending February 2017, a 10.7% International sourced guests accounted for Upcoming hotels improvement over the corresponding prior 45% of guest nights sold, while domestic year period. guests accounted for 55%. SKYCITY Hobson Street Hotel Four Points by Sheraton Park Hyatt Auckland M Social Auckland (former Copthorne Hotel Auckland Harbourcity) The Sebel Auckland Manukau Supply Outlook Seven projects (comprising a total of 1,291 We anticipate that Auckland’s rooms) are currently under construction accommodation market will continue to Notable hotel deals and are forecast to enter the market over perform strongly in the short term and is the next two years, with five of the hotel poised for further rate growth and to solidify Ibis Christchurch projects (818 rooms) comprising 5-star recent gains in occupancy levels given the product. -

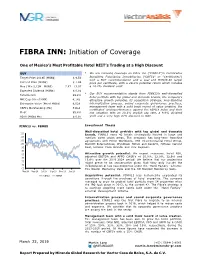

Fibra Inn – Initiation of Coverage

FIBRA INN: Initiation of Coverage One of Mexico’s Most Profitable Hotel REIT’s Trading at a High Discount BUY • We are initiating coverage on Fibra Inn ("FINN13")'s Certificados Target Price 2019E (MXN$) $ 9.50 Bursátiles Fiduciarios Inmobiliarios ("CBFI's" or "Certificates") with a BUY recommendation and a year-end MXN$9.50 target Current Price (MXN$) $ 7.98 price per certificate, with a 29.2% potential return which includes Max / Min (L12M - MXN$) 7.87 - 13.07 a 10.2% dividend yield. Expected Dividend (MXN$) $ 0.81 Our BUY recommendation stands from FINN13's well-diversified Total Return 29.2% • hotel portfolio with top global and domestic brands, the company's Mkt Cap (Mn of MXN) 4,145 attractive growth potential, its acquisition strategy, long-standing Enterprise Value (Mn of MXN$) 6,528 internalization process, sound corporate governance practices, management team with a solid track record of value creation, the CBFI's Outstanding (Mn) 519.4 certificates' underperformance against the FBMEX index and their Float 85.4% low valuation with an 10.1% implicit cap rate, a 9.0% dividend ADTV (MXN$ Mn) $ 0.97 yield and a very high 47% discount to NAV. FINN13 vs. FBMEX Investment Thesis Well-diversified hotel portfolio with top global and domestic 115 brands. FINN13 owns 42 hotels strategically located in large and 110 medium sized urban areas. The company has long-term franchise 105 agreements with Hilton Worldwide, IHG Intercontinental Hotel Group, 100 Marriott International, Wyndham Hotels and Resorts, Hoteles Camino 95 Real, Hoteles Casa Grande and City Express. 90 85 Attractive growth potential. -

MCC Description

MCC Description 0742 VETERINARY SERVICES 0743 WINE PRODUCERS 0744 CHAMPAGNE PRODUCERS 0763 AGRICULTURAL COOPERATIVES 0780 HORTICULTURAL AND LANDSCAPING SERVICES 1520 GENERAL CONTRACTORS‐RESIDENTIAL AND COMMERCIAL 1711 AIR CONDITIONING, HEATING, AND PLUMBING CONTRACTORS 1731 ELECTRICAL CONTRACTORS 1740 INSULATION, MASONRY, PLASTERING, STONEWORK, AND TILE SETTING CONTRACTORS 1750 CARPENTRY CONTRACTORS 1761 ROOFING AND SIDING, SHEET METAL WORK CONTRACTORS 1771 CONCRETE WORK CONTRACTORS 1799 CONTRACTORS, SPECIAL TRADE CONTRACTORS‐NOT ELSEWHERE CLASSIFIED 2741 MISCELLANEOUS PUBLISHING AND PRINTING 2791 TYPESETTING, PLATE MAKING, AND RELATED SERVICES 2842 SANITATION, POLISHING, AND SPECIALTY CLEANING PREPARATIONS 3000 UNITED AIRLINES 3001 AMERICAN AIRLINES 3002 PAN AMERICAN 3003 EUROFLY 3004 DRAGON AIRLINES 3005 BRITISH AIRWAYS 3006 JAPAN AIR LINES 3007 AIR FRANCE 3008 LUFTHANSA GERMAN AIRLINES 3009 AIR CANADA 3010 ROYAL DUTCH AIRLINES (KLM AIRLINES) 3011 AEROFLOT 3012 QANTAS 3013 ALITALIA 3014 SAUDI ARABIAN AIRLINES 3015 SWISS INTERNATIONAL AIR LINES 3016 SCANDINAVIAN AIRLINE SYSTEM (SAS) 3017 SOUTH AFRICAN AIRWAYS 3018 VARIG 3019 GERMANWINGS 3020 AIR INDIA 3021 AIR ALGERIE 3022 PHILIPPINE AIRLINES 3023 MEXICANA 3024 PAKISTAN INTERNATIONAL MCC Description 3025 AIR NEW ZEALAND LTD. INTERNATIONAL 3026 EMIRATES AIRLINES 3027 UNION DE TRANSPORTS AERIENS (UTA/INTERAIR) 3028 AIR MALTA 3029 SN BRUSSELS AIRLINES 3030 AEROLINEAS ARGENTINAS 3031 OLYMPIC AIRWAYS 3032 EL AL 3033 ANSETT AIRLINES 3034 ETIHADAIR 3035 TAP AIR PORTUGAL (TAP) 3036 VIACAO AEREA -

Surrey Hotel Futures

SURREY HOTEL FUTURES FINAL REPORT Prepared for: Surrey County Council August 2015 Surrey Hotel Futures Study 2015 __________________________________________________________________________________________ CONTENTS EXECUTIVE SUMMARY .................................................................................................................................. i 1. INTRODUCTION ................................................................................................................................... 1 1.1. Study Background and Brief................................................................................................... 1 1.2. Scope of the Study ................................................................................................................... 2 1.3. Methodology ............................................................................................................................. 4 2. NATIONAL HOTEL TRENDS ................................................................................................................ 6 2.1. National Hotel Performance Trends ...................................................................................... 6 2.2. National Hotel Development Trends .................................................................................... 8 3. SURREY HOTEL SUPPLY ..................................................................................................................... 19 3.1. Current Surrey Hotel Supply ................................................................................................. -

Letter to Shareholders

Letter to Shareholders Arne M. Sorenson J.W. Marriott, Jr. President and Chief Executive Officer Executive Chairman and Chairman of the Board Dear Shareholders, This year our company celebrates its 90th anniversary, and we are pleased to say that Marriott International has never been better positioned for the future after one of the most exciting and dynamic years in our company’s history. Last year, we successfully completed our historic 2016 Highlights acquisition of Starwood Hotels & Resorts Worldwide, The Starwood acquisition, completed on September 23, and immediately started to capitalize on the benefits 2016, expands our presence around the world, broad- of this merger. We saw strong growth here and ens our appeal to younger travelers, and provides a wide abroad, and continued to delight our guests with new range of choices for our guests. With our tremendous innovations. The integration of Starwood is opening scale, we see significant financial benefit for our own- new doors of opportunity for Marriott, as it strength- ers, franchisees, and shareholders and exciting, new ens our competitive position for the future. opportunities for our associates and the communities where we live and work. WWW.MARRIOTT.COM While the merger dominated the news last year, there n Marriott repurchased 8.0 million shares of the were many other highlights, starting with our 2016 company’s common stock for $573 million. We financial performance: remain committed to our asset-light management and franchise strategy, which should continue to n Diluted earnings per share totaled $2.64, a yield significant cash returns to stockholders decrease of 16 percent over the prior year.