Seaside Resorts Action Plan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Trend Report on Travel After 2020

in collaboration with GLOBETRENDER Travel Trend Report October 2020 travel after 2020 what will tourism look like in our new reality? table of contents Co-authors Damon Embling World Affairs Reporter, Euronews Damon is a seasoned journalist, specialising in travel and tourism. He regularly reports from key global industry events including ITB Berlin and WTM London and moderates high-profile debates on the future of the sectors. Most recently, these have included a special virtual series for Euronews and a debate session for Brand USA Travel Week Europe 2020. Damon has also presented several travel programmes for Euronews, from across Europe and Asia. Jenny Southan, Editor & Founder of travel trend forecasting agency Globetrender Jenny Southan is editor and founder of Globetrender, a travel trend forecasting agency and online magazine dedicated to the future of travel. Jenny is also a public speaker and freelance journalist who writes for publications including Conde Nast Traveller, The Telegraph and Mr Porter. Previously she was features editor of Business Traveller magazine for ten years. Contributor Eva zu Beck Euronews Travel Contributor Eva zu Beck is an adventure YouTuber and travel TV host with a community of 2 million fans across her social media channels. She travels to countries rarely covered by mainstream media, and tells the stories of overcoming challenges in some of the planet’s most remote places. table of contents 2 introduction Hit hard by the global Covid-19 pandemic, the travel and tourism sectors are facing a rapidly changing future. As brands and businesses look to recover losses, there’s also a need to re-think their offerings, amid changing consumer behaviour and habits. -

GRAND TOUR of PORTUGAL Beyond Return Date FEATURING the D OURO RIVER VALLEY & PORTUGUESE RIVIERA

Durgan Travel presents… VALID 11 Days / 9 Nights PASSPORT REQUIRED Must be valid for 6 mos. GRAND TOUR OF PORTUGAL beyond return date FEATURING THE D OURO RIVER VALLEY & PORTUGUESE RIVIERA Your choice of departures: April ~ Early May ~ October $ $ TBA* for payment by credit card TBA* for payment by cash/check Rates are per person, twin occupancy, and INCLUDE $TBA in air taxes, fees, and fuel surcharges (subject to change). OUR GRAND TOUR OF PORTUGAL TOUR ITINERARY: DAY 1 – BOSTON~PORTUGAL: Depart Boston’s Logan International Airport aboard our transatlantic flight to Porto, Portugal (via intermediate city) with full meal and beverage service, as well as stereo headsets, available in flight. DAY 2 – PORTO, PORTUGAL: Upon arrival at Francisco Carneiro Airport in Porto, we will meet our Tour Escort, who will help with our transfer. We’ll board our private motorcoach and enjoy a panoramic sightseeing tour en route to our 4-star hotel, which is centrally located. After check-in, the remainder of the day is at leisure. Prior to dinner this evening, we will gather for a Welcome Drink. Dinner and overnight. (D) DAY 3 – PORTO: After breakfast at our hotel, we are off for a full day of guided sightseeing in Porto, Portugal’s second largest city, situated on the right bank of the Douro River. Our tour begins in the Foz area near the mouth of the river. Next, we will visit Pol ácio da Bolsa (the stock exchange) , the Old Trade Hall, the Gold Room, the Arabian Hall, the Clerigos Tower, and Cais da Bibeira. -

Creative Resources for Attractive Seaside Resorts: the French Turn

Journal of Investment and Management 2015; 4(1-1): 78-86 Published online February 11, 2015 (http://www.sciencepublishinggroup.com/j/jim) doi: 10.11648/j.jim.s.2015040101.20 ISSN: 2328-7713 (Print); ISSN: 2328-7721 (Online) Creative resources for attractive seaside resorts: The French turn Anne Gombault 1, Ludovic Falaix 2, Emeline Hatt 3, Jérôme Piriou 4 1Research Cluster for Creative Industries, KEDGE Business School, Bordeaux-Marseille, France 2Laboratoire ACTé EA 4281, Blaise Pascal University, Clermont-Ferrand France 3Laboratoire interdisciplinaire en urbanisme – EA 889, Aix Marseille Univeristy, Aix Marseille, France 4Tourism Management Institute, La Rochelle Business School, La Rochelle, France Email address: [email protected] (A. Gombault), [email protected] (L. Falaix), [email protected] (E. Hatt), [email protected] (J. Piriou) To cite this article: Anne Gombault, Ludovic Falaix, Emeline Hatt, Jérôme Piriou. Creative Resources for Attractive Seaside Resorts: The French Turn. Journal of Investment and Management. Special Issue: Attractiveness and Governance of Tourist Destinations. Vol. 4, No. 1-1, 2015, pp. 78-86. doi: 10.11648/j.jim.s.2015040101.20 Abstract: This article presents a qualitative analysis of the specific strategies used by coastal resorts in the South of France to valorise their creative regional resources. These strategies emerge from factors of change in the trajectories of the resorts: change in the relationship between man and nature, environmental turning point and the need for sustainability, emergence of creative tourism centred on recreation, sport and culture. The research is supported by three case studies, Biarritz, Lacanau and Martigues, and assesses the constraints that arise in terms of design and management of coastal resorts and tourist areas, against a background of numerous conflicting requirements, including attractiveness and sustainability. -

Wellbeing Tourism and Its Potential in Case Regions of the South Baltic

Wellbeing tourism and its potential in case regions of the South Baltic Lithuania - Poland - Sweden Lindell, L. (ed.), Dziadkiewicz, A., Sattari, S., Misiune, I., Pereira, P., Granbom, A., 2019. 2 EDITOR: Lindell, L.1 AUTHORS: Lindell, L.1, Dziadkiewicz, A.2, Sattari, S.1, Misiune, I.3, Pereira, P.4, and, Granbom, A.1 1 Linnaeus University, Sweden. 2 Gdansk University, Poland. 3 Vilnius University, Lithuania. 4 Mykolas Romeris University, Lithuania. Main author contribution for each theme: Introduction: Lindell, L. Wellbeing tourism concept: Lindell, L. Lithuania: Dziadkiewicz, A., Misiune, I., & Pereira, P. Poland: Dziadkiewicz, A. Sweden: Sattari, S. IMAGE Royalty-free by Bigstockphoto. PUBLISHED BY: Linnaeus University (Lnu) 391 82 Kalmar 351 95 Växjö Tel.: +46 0772-28 80 00 E-mail: [email protected] Web: www.lnu.se ISBN: 978-91-89283-05-3 (pdf) Version 1.0, 31th of October 2019. © 2019 Linnaeus University (Lnu), and authors This report was produced with financial support from the Swedish Institute, SI, that encourage projects that focus on cross border challenges that fit in to the theme: ”Save the Sea, connect the region, increase prosperity”. The contents of this publication are the sole responsibility of the authors and can in no way be taken to reflect the views of the Swedish Institute. 3 4 TABLE OF CONTENTS 1. INTRODUCTION .............................................................................................................. 7 BACKGROUND ...................................................................................................................... -

Chapter 27. Tourism and Recreation Group of Experts: Alan Simcock

Chapter 27. Tourism and Recreation Group of Experts: Alan Simcock (Lead member) and Lorna Inniss 1. Introduction Seaside holidays have a long history. They were popular for several hundred years (100 BCE – 400) among the ruling classes of the Roman Empire: these visited the coast of Campania, the Bay of Naples, Capri and Sicily for swimming, boating, recreational fishing and generally lounging about (Balsdon, 1969). But thereafter seaside holidaying largely fell out of fashion. In the mid-18th century, the leisured classes again began frequenting seaside resorts, largely as a result of the health benefits proclaimed by Dr. Richard Russell of Brighton, England, in 1755 (Russell, 1755). Seaside resorts such as Brighton and Weymouth developed in England, substantially helped by the royal patronage of Kings George III and George IV of Great Britain (Brandon, 1974). After the end of the Napoleonic wars, similar developments took place across Europe, for example at Putbus, on the island of Rügen in Germany (Lichtnau, 1996). The development of railway and steamship networks led both to the development of long-distance tourism for the wealthy, with the rich of northern Europe going to the French Riviera, and to more local mass tourism, with new seaside resorts growing up to serve the working classes of industrialised towns in all countries where industrialisation took place. In England, whole towns would close down for a “wakes week”, and a large part of the population would move to seaside resorts to take a holiday: for example, in 1860 in north-west England, 23,000 travelled from the one town of Oldham alone for a week in the seaside resort of Blackpool (Walton, 1983). -

Sex Tourism: Do Women Do It Too?

Leisure Studies ISSN: 0261-4367 (Print) 1466-4496 (Online) Journal homepage: https://www.tandfonline.com/loi/rlst20 Sex tourism: do women do it too? Sheila Jeffreys To cite this article: Sheila Jeffreys (2003) Sex tourism: do women do it too?, Leisure Studies, 22:3, 223-238, DOI: 10.1080/026143603200075452 To link to this article: https://doi.org/10.1080/026143603200075452 Published online: 01 Dec 2010. Submit your article to this journal Article views: 3869 View related articles Citing articles: 60 View citing articles Full Terms & Conditions of access and use can be found at https://www.tandfonline.com/action/journalInformation?journalCode=rlst20 Leisure Studies 22 (July 2003) 223–238 Sex tourism: do women do it too? SHEILA JEFFREYS Department of Political Science, The University of Melbourne, Victoria 3010, Australia This article examines a recent tendency amongst researchers of sex tourism to include women within the ranks of sex tourists in destinations such as the Caribbean and Indonesia. It argues that a careful attention to the power relations, context, meanings and effects of the behaviours of male and female tourists who engage in sexual relations with local people, makes it clear that the differences are profound. The similarities and differences are analysed here with the conclusion that it is the different positions of men and women in the sex class hierarchy that create such differences. The political ideas that influence the major protagonists in this debate to include or exclude women will be examined. The article ends with a consideration of the problematic implications of arguing that women do it too. -

Rental Guidelines

Rental Guidelines The guest, including all members of the guest’s party understands and agrees: Upon confirming a reservation, a contractual agreement is made between Resort Vacation Properties of St. George Island, Inc. and the guest, including all members of the guest’s party. The guest and the rest of their party agree to abide by the following Rental Guidelines: Maximum Occupancy: At all times, both inside and outside the home, the maximum occupancy is the number of persons allowed on the premises, including infants. We cater to family groups and cannot accept reservations for vacationing students or house parties. We do not rent to students even if one or more parents or legally responsible adults accompany them, or to groups under the age of 25. This policy is strictly enforced. Special events such as weddings, reunions, and church retreats are only allowed in select homes and require a separate contract. Special pricing and security deposits may be required. Please contact our office for details. Pets: Guests may bring up to 2 pets to our pet-friendly homes unless otherwise noted in an individual property description. Guests must obtain special permission, and a fee of $100 will be charged, for each pet that exceeds the amount allowed as outlined above or as specified in an individual property description. Guests are required to clean up after their pets, and there may be additional charges if pet waste is left on the property. Franklin County law prohibits leaving pet waste on the beach or dunes. Pets in non-pet-friendly homes are strictly prohibited and will result in immediate eviction with no refund of rent. -

Twixt Ocean and Pines : the Seaside Resort at Virginia Beach, 1880-1930 Jonathan Mark Souther

University of Richmond UR Scholarship Repository Master's Theses Student Research 5-1996 Twixt ocean and pines : the seaside resort at Virginia Beach, 1880-1930 Jonathan Mark Souther Follow this and additional works at: http://scholarship.richmond.edu/masters-theses Part of the History Commons Recommended Citation Souther, Jonathan Mark, "Twixt ocean and pines : the seaside resort at Virginia Beach, 1880-1930" (1996). Master's Theses. Paper 1037. This Thesis is brought to you for free and open access by the Student Research at UR Scholarship Repository. It has been accepted for inclusion in Master's Theses by an authorized administrator of UR Scholarship Repository. For more information, please contact [email protected]. TWIXT OCEAN AND PINES: THE SEASIDE RESORT AT VIRGINIA BEACH, 1880-1930 Jonathan Mark Souther Master of Arts University of Richmond, 1996 Robert C. Kenzer, Thesis Director This thesis descnbes the first fifty years of the creation of Virginia Beach as a seaside resort. It demonstrates the importance of railroads in promoting the resort and suggests that Virginia Beach followed a similar developmental pattern to that of other ocean resorts, particularly those ofthe famous New Jersey shore. Virginia Beach, plagued by infrastructure deficiencies and overshadowed by nearby Ocean View, did not stabilize until its promoters shifted their attention from wealthy northerners to Tidewater area residents. After experiencing difficulties exacerbated by the Panic of 1893, the burning of its premier hotel in 1907, and the hesitation bred by the Spanish American War and World War I, Virginia Beach enjoyed robust growth during the 1920s. While Virginia Beach is often perceived as a post- World War II community, this thesis argues that its prewar foundation was critical to its subsequent rise to become the largest city in Virginia. -

The History of British Spa Resorts: an Exceptional Case in Europe? John K

1-Teresita_G mez:dossier1 09/12/2008 16:53 PÆgina 28 [138] TST, junio 2011, nº 20, pp. 138-157 The history of British spa resorts: an exceptional case in Europe? John K. Walton Universidad del País Vasco Resumen ste artículo propone que desde el siglo XVIII los balnearios termales del Reino Unido E han seguido una trayectoria única dentro del más amplio contexto europeo, que se concreta en la estructura de la red de balnearios, la falta de dinamismo desde principios del siglo XIX y la ausencia del papel innovador británico que se ha notado en otros aspectos de la historia del turismo. Trata también de explicar el temprano declive de los balnearios ter- males británicos y la ausencia de una respuesta efectiva frente a la competencia europea. Palabras clave: Turismo, Balnearios, Salud. Códigos JEL: N3, N5, N7. Abstract his article argues that the British experience of spa resort development since the T eighteenth century has been unique in Europe, in terms of the nature of the resort net- work, the lack of sustained dynamism, and the failure of the British role in spa tourism to match the dynamic and innovatory influence displayed in other aspects of tourism develop- ment. It also discusses the reasons for the early decline of British spas and their failure to respond effectively to European competition. Keywords: Tourism, Spa resorts, Health. JEL Codes: N3, N5, N7. 05 dossier 20 (J.K. Walton).indd 138 28/7/11 01:14:27 1-Teresita_G mez:dossier1 09/12/2008 16:53 PÆgina 28 [139] TST, junio 2011, nº 20, pp. -

Global Trends in Coastal Tourism

CESD: Global Trends in Coastal Tourism Global Trends in Coastal Tourism Prepared by: Martha Honey, Ph.D. and David Krantz, M.A. Center on Ecotourism and Sustainable Development A Nonprofit Research Organization Stanford University and Washington, DC Prepared for: Marine Program World Wildlife Fund Washington, DC December 2007 1 CESD: Global Trends in Coastal Tourism TABLE OF CONTENTS Acronyms.......................................................................................... 5 1.0 Executive Summary: Key Findings........................................... 8 2.0 WWF Working Hypothesis...................................................... 15 3.0 CESD Research ........................................................................ 15 4.0 Global Tourism Trends ............................................................ 16 4.1 Importance of Tourism............................................................................16 4.2 Environmental Impacts...........................................................................17 4.3 Market Trends in the New Millennium: 2000-2020 ................................24 5.0 Types of Tourism and Definitions........................................... 28 5.1 Beach Resort, Cruise, Ecotourism, Sustainable Tourism ...................28 5.2 History and Importance of Ecotourism and Sustainable Tourism......29 5.3 Consumer Demand for Ecotourism and Sustainable Tourism............33 6.0 Structure of the Tourism Industry .......................................... 35 6.1 Airlines .....................................................................................................38 -

Enjoying Your Vacation Options

Enjoying Your Vacation Options Marriott Vacation Club® has created the most flexible and exciting vacation ownership program available—the Marriott Vacation Club Destinations™ program. This guide will help you understand and maximize your options. As a Marriott Vacation Club Destinations Owner and through the Marriott Vacation Club Destinations Exchange Program, you can use Vacation Club Points for a variety of experiences within four flexible collections of vacation options: Marriott Vacation Club® Resorts – Enjoy a vacation at any of more than 50 Marriott Vacation Club resorts in the U.S., the Caribbean, Europe and Asia. Marriott Rewards® – Redeem your Vacation Club Points for Marriott Rewards points and stay at more than 3,800 Marriott® hotels worldwide. Explorer Collection – Discover unique travel opportunities and adventures, including cruises, safaris, rafting, mountain biking and guided tours. Exchange Partner Resorts – Vacation at hundreds of resorts in dozens of locations through our external exchange partner, Interval International®. With all this flexibility, you have virtually limitless possibilities! OPTION 1: MARRIOTT VACATION CLUB RESORTS Choose a spacious vacation villa for your next getaway. When you plan a vacation within Marriott Vacation Club Resorts, you will have access to more than 50 magnificent resorts offering spacious accommodations, from deluxe studios to 1- and 2-bedroom villas and even 3-bedroom villas and townhouses, depending on the location. Stretch out and enjoy all the comforts of home with amenities such as a fully equipped kitchen, washer and dryer, a balcony or patio, and separate living and dining areas.1 Vacationing at a Marriott Vacation Club resort is perfect for extended vacations or family reunions. -

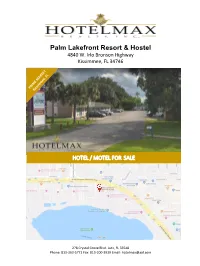

Palm Lakefront Resort & Hostel

Palm Lakefront Resort & Hostel 4840 W. Irlo Bronson Highway Kissimmee, FL 34746 HOTEL / MOTEL FOR SALE 278 Crystal Grove Blvd. Lutz, FL 33548 Phone: 813-363-5771 Fax: 813-200-3939 Email: [email protected] 4840 W. Irlo Bronson Highway Kissimmee, FL 34746 EXECUTIVE SUMMARY 4840 W. Irlo Bronson Highway Kissimmee, FL 34746 County: Osceola Property Type: Hotel/Motel No. of Buildings: 4 No. of Stories: 1 m No. of Units/Rooms: 50 .co Building Area Size: 7,372 Sq. Ft. Lot Size/Acres: 4.24 Acres Year Built: 1978 Pool: Yes Zoned: Commercial CONTACT LISTING BROKER- Price: Signed NDA Required HotelMaxRealty CONFIDENTIAL LISTING – DO NOT CONTACT OWNER OR EMPLOYEES CONFIDENTIAL SALE Property is centrally located near Orlando Theme Parks Must schedule appointment with listing agent to visit www.hostelinorlando.com www. property – Terry Hatfield – 813-363-5771 2 Property Description 3 The Palm Lakefront Resort and Hostel is a 50 Unit, inn-style relaxed hostel that is beautifully landscaped with lush gardens, tropical trees and old Florida character. The lakefront walking pier is a reflection of the picturesque sitting along Lake Cecile and offers all of nature’s delight. A beautiful swimming pool overlooks the lake and tropical grounds surrounded by large, Florida ancient oaks and statue-oriented fountains. The hostel offers free Wi-Fi, exercise area, swimming pool, outdoor fire pit, picnic areas, BBQ facilities, canoeing, game room with Karaoke, ping pong, pool tables and foosball tables, badminton equipment, board games, a commercial laundry. The hostel has a kitchen where guests may cook their own food. Location Description Off Interstate 4 and US-192, this hostel is 14 miles from the Universal Orlando Theme Park, 8 miles from SeaWorld Orlando and 5 miles from the Walt Disney World Resort.