Clorox Co /De

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Savannah Morning News Smartsource 8/21

Savannah Morning News SmartSource 8/21 $1 off Act mouthwash, 16.9 oz + (exp 10/31) $1 off Brita bottle water filtration system (exp 10/31) $4 off Brita pitcher or faucet mount (exp 10/31) .50/1 Carefree product (exp 10/31) $2 off Claritin product, 4 oz or 10 ct + (exp 9/18) $4 off Claritin product, 15 ct + (exp 9/18) $6 off Claritin product, 45 ct (exp 8/28) $1 off Clear Care Cleansing and Disinfecting solution, 12 oz + (exp 9/30) $3 off Clear Care Cleaning and Disinfecting solution, twin pk (exp 9/30) .25/1 Clorox disinfecting wipes, 35 ct + (exp 10/16) .25/1 Clorox bleach, 82 oz + (exp 10/16) .75/1 Cremel liquid coffee creamer (available at Walmart) (exp 10/31) $1/2 Select Clorox, Tilex, or Pine-Sol cleaners (exp 10/16) $1 off any Coach first aid product (exp 11/30) $1/3 Dannon Oikos or Stonyfield Oikos organic yogurt, 5.3 oz (exp 9/18) .75/2 Dole fruit bowls (exp 10/31) .75/1 Excedrin product, 20 ct + (exp 10/8) $1.50 off Excedrin product, 80 ct + (exp 10/8) .50/1 Formula 409 All Purpose cleaner, 32 oz + (exp 10/16) .75/1 French’s Worcestershire Sauce (exp 10/31) .75/1 French’s honey mustard dipping sauce (exp 11/30) .55/1 Frigo Cheese Heads string cheese, 10 oz + (exp 11/30) $1/2 Glad food storage (exp 10/1) .75/2 Glade Sense & Spray refills (exp 9/24) .55/1 Glade Premium room spray, 9.7 oz (exp 9/24) .75/1 Glade Scented Oil candles holder or (2) refills (exp 9/24) .75/2 Glade jar candles, 4 oz (exp 9/24) $1 off Glade Decor Scents electric warmer (exp 10/8) $1 off Glade Decor Scents glass holder (exp 10/8) $1 off Glade Decor Scents -

Strategic Report

Strategic Report Prepared for Lead Consultant: Andrew Barnette Associate Consultants: Elizabeth Davis Travis Evans 19 April 2004 Clorox Report / 2 Report Contents Company Background 3 Financial Analysis 7 Porter’s Five-Forces Analysis 13 Evaluation of Key Issues 18 Conclusions 21 PAC Consulting, LLP Clorox Report / 3 Background History On May 3, 1913, five Oakland, California entrepreneurs invested $100 apiece to set up America's first commercial-scale liquid bleach factory on the east side of San Francisco Bay. Their ambitious plan was to convert the brine available in abundance from the nearby salt ponds of San Francisco Bay into sodium hypochlorite bleach, using a sophisticated and technologically demanding process of electrolysis. They called their new undertaking the Electro-Alkaline Company. During its outfitting, an engineer for an equipment supplier, Abel M. Hamblet, suggested a name for the new product. From the words "chlorine" and "sodium hydroxide," which in combination form the bleach's active ingredient, he proposed the amalgam “Clorox”. By 1916, Clorox bleach was in distribution throughout the San Francisco Bay Area. Sales were $14,237 for the year. In 1918, the company went public for the first time. Registered as the Clorox Chemical Company in the state of Delaware, its stock began trading on the San Francisco Exchange. By 1957 annual sales had multiplied more than tenfold, to over $40 million. Through effective advertising (the first television commercials aired in 1953) and the construction of a dozen new plants between 1938 and 1956, the Clorox Chemical Company had garnered the largest share of the US Household Bleach products by the 1950s. -

Billboard Concert Marketing and Promotion Award Goes to Clorox Barbecue Brands for Firing up the Keith Urban Escape Together World Tour

The Clorox Company News Release Billboard Concert Marketing and Promotion Award Goes to Clorox Barbecue Brands for Firing Up the Keith Urban Escape Together World Tour Billboard’s Tour of the Year Award Acknowledges KC Masterpiece® and Kingsford® for Re-Inventing the Entertainment Marketing Model with the Integration of Live, Online and Mobile Experiences New York, NY (November 6, 2009) – Last night, Billboard magazine bestowed KC Masterpiece® barbecue sauce and Kingsford® charcoal with the music industry’s premier marketing honor – Billboard magazine’s annual Concert Marketing and Promotion Award – for firing up the Keith Urban Escape Together World Tour. In sponsoring the tour, the barbecue brands encouraged friends and families to get together and grill in their own backyard, something Urban and his band identify with during their hectic tour schedules. The award recognized the brand’s willingness to change the rules of traditional sponsorship and make a powerful business impact. Announced last night at the Billboard Touring Awards at the Roosevelt Hotel in New York City, the Award confirmed that the traditional sponsorship model is rapidly evolving, with increasing emphasis being placed on the natural fit between artist and brand as well as the role of online community and mobile technology in reaching and engaging fans and consumers. The Concert Marketing & Promotion Award recognizes a sponsorship or promotion that benefited the concert industry at large by stimulating attendance to live events, providing value to fans, and promoting the artist and brands involved. This year’s program received hundreds of submissions crossing every genre, narrowed down to seven finalists by Billboard’s editorial team and then voted on by the public to ultimately select the winner. -

Earn DOUBLE POINTS Foryourschool on Brandsyou

TFS_2012_broch 6/26/12 4:08 PM Page 1 Start Earning Your Share of Over $500,000 JULY 29, 2012 THRU MARCH 30, 2013 For Your Child’s School Today! Your Child’s School Can Share in “Great program… Brings the school and “Price Chopper is so generous. $500,000 for Educational Equipment! community together working for our goal. We earn points on groceries and are Thank you Price Chopper!!!!” rewarded with wonderful equipment!” West Rutland School, Owego Elementary School, West Rutland, VT Owego, NY “It was easy to use. Very quick for someone who is very busy. As your school earns Thank you for the donation and supporting local schools.” Anna Reynolds Elementary School, Newington, CT points for Tools, HOW TOOLS FOR SCHOOLS WORKS: Register your The program All purchases Every dollar spent at you earn discounts 1 AdvantEdge Card and 2 begins on Sunday, 3 using your 4 Price Chopper earns designate a school at the July 29, 2012 AdvantEdge you one point. Purchase on Fuel with Guest Services desk at and runs Card will be brands in this brochure your Price Chopper, at until Saturday, automatically and receive double points. your school, or online at March 30, 2013. credited to your www.pricechopper.com selected school. 4easystepstohelp yourchild’sschool! CHECK YOUR TOOLS FOR SCHOOLS POINT BALANCE FREQUENTLY ASKED QUESTIONS ABOUT TOOLS FOR SCHOOLS: ON YOUR RECEIPT! Do I have to sign up again if I Where do I find my school code? Can I check how many points signed up in previous years? The Guest Service Desk at Price Chopper has I have earned? Yes. -

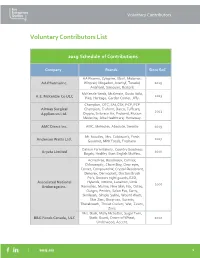

Voluntary Contributors List

Voluntary Contributors Voluntary Contributors List 2019 Schedule of Contributions Company Brands Since SoC AA Pharma, Zyloprim, Elavil, Midamor, AA Pharma Inc. Winpred, Mogadon, Aventyl, Toradol, 2019 Anafranil, Sinequan, Restoril. McKenzie Seeds, McKenzie, Gusto Italia, 2013 A.E. McKenzie Co ULC Pike, Heritage, Garden Corner, Jiffy. Champion, OTC, SAI, CSX, PCP, PCP Airway Surgical Champion, Truform, Darco, Tuffcare, 2013 Appliances Ltd. Drypro, Embrace Air, Proband, Motion Medecine, Alba Healthcare, Hemaway. AMC Direct Inc. AMC, Mehadrin, Absolute, Sweetie 2019 Mr. Noodles, Mrs. Cubbison’s, Fresh 2017 Anderson Watts Ltd. Gourmet, MPK Foods, Freshana. Oakrun Farm Bakery, Country Goodness 2010 Aryzta Limited Bagels, Healthy Start English Muffins. Acme Free, Boudreaux, Carmex, Chloraseptic, Chore Boy, Clear eyes, Comet, Compound W, Crystal Deodorant, Denorex, Dermoplast, Doctors Brush Pic's, Doctors night guards, EZO, Associated National Hylands, Inttimo, Lansinon, Little 2007 Brokerage Inc. Remedies, Murine, New Skin, Nix, Osteo, Outgro, Peridex, Salon Pas, Samy, Similasan, Simply Saline, Wound Wash, Skin Zinc, Sleep-eze, Sucrets, Therabreath, Throat Coolers, Wet, Zicam, Zims. Mrs. Dash, Molly Mcbutter, Sugar Twin, B&G Foods Canada, ULC Static Guard, Cream of Wheat, 2012 Underwood, Accent. 1 Voluntary Contributors Company Brands Since SoC Bellisio Food Canada Joy of Cooking, Michelina's. 2010 Bissell Canada Bissel. 2005 Corporation Blistex Inc. Blistex. 2015 Boshart Industries Inc. Iron Out, Plumbeeze Line. 2005 Bulk Barn Foods Ltd. Bulk Barn Foods. 2009 PediFix, Xenna, Silk Feet, Magni Life, Support Plus, Thera Sock, Thera Glove, Nova, No Rince, ArmRx, Hartmobility, Sea Band, Trion Z, Vital ID, Aquatabs, Card Health Care Inc. 2019 Sabona, Sleep Pretty in Pink, Hearos, Ear Band-it, 4 Eyes, First Medic, Vita Medic, Kids Medic, Citrus Magic, Clearly Natural, Worlds Best. -

Clorox AI Case Study

CASE STUDY How a leading global manufacturer and marketer of consumer and professional products used RevTrax AI to increase audience engagement, units moved and gross sales. 27% 660% $196,353.65 INCREASE IN AUDIENCE INCREASE IN WEIGHTED INCREASE IN ESTIMATED ENGAGEMENT UNITS MOVED GROSS SALES THE CLOROX THE CHALLENGE COMPANY PROFILE The Clorox Company (formerly Clorox In September 2019, the Clorox Company, a leading global Chemical Company), based in Oakland, manufacturer and marketer of consumer and professional products, California, is an American global approached RevTrax with the desire to increase promotional manufacturer and marketer of consumer and marketing efficiency. professional products, with approximately 8,700 employees worldwide, as of June 30, The main objective was to increase the number of units moved for 2018. Net sales in the company's 2019 fiscal year were US$6.2 billion. Clorox ranked three specific products: Toilet Wand Starter Kit, Clorox Disinfecting #468 on Fortune's 2018 Fortune 500 list. Wipes, and 55oz Bleach. In addition, the Clorox Company required the acquisition of consumer behavioral insights to further optimize Clorox products are sold primarily through future promotional marketing campaigns. mass merchandisers, retail outlets, e-commerce channels, distributors and medical supply providers. Clorox brands include its namesake bleach and cleaning products, as well as Burt's Bees, Formula THE SOLUTION: REVTRAX AI 409, Glad, Hidden Valley, Kingsford, Kitchen Bouquet, KC Masterpiece, Liquid-Plumr, Brita Clorox deployed the RevTrax AI solution. (in the Americas), Mistolin, Pine-Sol, Poett, Green Works Cleaning Products, Soy Vay, By analyzing billions of consumer engagement data points over a decade of consumer RenewLife, Rainbow Light, Natural Vitality, Neocell, Tilex, S.O.S., and Fresh Step, Scoop purchase insights and state of the art machine learning algorithms, our AI assigns Away and Ever Clean pet products. -

Smartsource 8/21

SmartSource 8/21 $1 off Act mouthwash, 16.9 oz + (exp 10/31) .40/1 Bob Evans refrigerated side (exp 10/16) $1/2 Bob Evans refrigerated side (exp 10/16) .75/1 Bob Evans Sausage patty or link (exp 10/16) $1 off Brita bottle water filtration system (exp 10/31) $4 off Brita pitcher or faucet mount (exp 10/31) .50/1 Carefree product (exp 10/31) $3 off wyb Rio Blu-ray or DVD and (2) Chiquita bites singles, (1) Family, (1) Muti-pack, or (2) Duos (exp 9/30) $1/2 Chiquita Bites singles or (2) Duos (exp 10/15) $2 off Claritin product, 4 oz or 10 ct + (exp 9/18) $4 off Claritin product, 15 ct + (exp 9/18) $6 off Claritin product, 45 ct (exp 8/28) $1 off Clear Care Cleansing and Disinfecting solution, 12 oz + (exp 9/30) $3 off Clear Care Cleaning and Disinfecting solution, twin pk (exp 9/30) .25/1 Clorox disinfecting wipes, 35 ct + (exp 10/16) .25/1 Clorox bleach, 82 oz + (exp 10/16) $1/2 Select Clorox, Tilex, or Pine-Sol cleaners (exp 10/16) $1 off Coach Brand Product (exp 11/30) $1/3 Dannon Oikos or Stonyfield Oikos organic yogurt, 5.3 oz (exp 9/18) .50/2.75/2 Dole fruit bowls (exp 10/31) $1 Dole Fruit Bites (exp 11/20) .75/1 Excedrin product, 20 ct + (exp 10/8) $1.50 off Excedrin product, 80 ct + (exp 10/8) .50/1 Formula 409 All Purpose cleaner, 32 oz + (exp 10/16) .75/1 French’s honey mustard dipping sauce (exp 11/30) .75/1 French’s Worchestershire Sauce (exp 10/31) .55/1 Frigo Cheese Heads string cheese, 10 oz + (exp 11/30) $1/2 Glad food storage (exp 10/1) $1/2 Glade Sense & Spray refills (exp 9/24) .75/2 Glade Sense & Spray refills (exp 9/24) -

Over a 100-Year Span, the Clorox Company Has Evolved from a Single-Product Manufacturer Into a Multinational Powerhouse with Leading Household Brands

Over a 100-year span, The Clorox Company has evolved from a single-product manufacturer into a multinational powerhouse with leading household brands. Here’s a quick blast from the past with fun facts about our company and product lines : How It All Began: On May 3, 1913, five California entrepreneurs invested $100 each to create America's first commercial liquid bleach factory, the Electro Alkaline Company. Using brine from the salt ponds of San Francisco Bay and an electrical current, our famous bleach product was born in Oakland, Calif., where the company remains headquartered to this day. Early Adopters: The first gallon size of Clorox ® regular bleach was sold to businesses like breweries, walnut bleachers and municipal water systems. Spouses Save Company: The early company was near collapse when investors Bill and Annie Murray came to the rescue. Bill became the company’s first general manager, streamlining operations and arranging financing. Annie, who ran the couple's thriving Oakland grocery store, had the brilliant idea to market Clorox liquid bleach to homemakers. She gave away free samples in 15-ounce amber glass “pint” bottles and talked up the product's benefits as a "bleacher, germicide, cleanser and disinfectant." Giving Back: We made our first-recorded charitable donation to a national youth organization in 1921. In 1980 we formalized our efforts, establishing The Clorox Company Foundation. We’ve since awarded $87 million in grants to nonprofits and in fiscal year 2012 alone, donated $15 million in products used primarily for disaster relief. Taking Stock: We went public for the first time in 1928 as the Clorox Chemical Company, issuing 200,000 shares of common stock traded on the San Francisco Stock Exchange. -

UPC Description Size 0003700050838 Always Infinity Heavy Flow with Sample Liners Multi Pack 36 Ct

UPC Description Size 0003700050838 Always Infinity Heavy Flow with Sample Liners Multi Pack 36 Ct. 0003700011715 Always Infinity Overnight Pantiliners w/Wings 14 Ct. 0003700011718 Always Infinity Overnight Pantiliners w/Wings 28 Ct. 0003700050840 Always Infinity Overnight w/Sample Liners Multi Pack 28 Ct. 0003700011713 Always Infinity Regular Pantiliners w/Wings 18 Ct. 0003700011716 Always Infinity Regular Pantiliners w/Wings 36 Ct. 0003700011714 Always Infinity Super Pantiliners w/Wings 16 Ct. 0003700011717 Always Infinity Super Pantiliners w/Wings 32 Ct. 0001780014197 Beneful Healthy Fiesta 15.5 Lb. 0001780014195 Beneful Healthy Fiesta 7 Lb. 0001780014188 Beneful Healthy Fiesta 3.5 Lb. 0001780013639 Beneful Incredibites 15.5 Lb. 0001780013640 Beneful Incredibites 3.5 Lb. 0003700028727 Bounty Extra Soft Select‐A‐Size White Paper Towel 6‐Roll ‐ 283.2 Sq. Ft. 0003700021410 Bounty Prints Big Roll Paper Towels 6‐Roll ‐ 322.6 Sq. Ft. 0003700028844 Bounty Prints Big Roll Paper Towels 6‐Roll ‐ 305 Sq. Ft. 0003700028848 Bounty Select‐a‐Size Big Roll Paper Towels 6‐Roll ‐ 308 Sq. Ft. 0003700021407 Bounty White Big Roll Paper Towels 6‐Roll ‐ 352.9 Sq. Ft. 0003700028857 Bounty White Big Roll Paper Towels 6‐Roll ‐ 333.6 Sq. Ft. 0003700049260 Bounty White Napkins 50 Ct. 0003700006356 Bounty White Napkins 400 Ct. 0003940001880 Bush's Best Black Beans 15 Oz. 0003940001690 Bush's Best Chili Beans 16 Oz. 0003940001734 Bush's Best Dark Red Kidney Beans 16 Oz. 0003940001700 Bush's Best Garbanzo Beans 16 Oz. 0003940001782 Bush's Best Great Northern Beans 15.8 Oz. 0003940001673 Bush's Best Large Butter Beans 16 Oz. 0003940001747 Bush's Best Light Red Kidney Beans 16 Oz. -

LCLD Posting

The Clorox Company 1L LCLD Scholar Legal Internship Summer 2015 Oakland, California or Buenos Aires, Argentina The Clorox Company is a leading multinational manufacturer and marketer of consumer and professional products with about 7,700 employees worldwide and fiscal year 2014 sales of $5.5 billion. Clorox markets some of the most trusted and recognized consumer brand names, including its namesake bleach and cleaning products; Pine-Sol® cleaners; Liquid Plumr® clog removers; Poett® home care products; Fresh Step® cat litter; Glad® bags, wraps and containers; Kingsford® charcoal; Hidden Valley® and KC Masterpiece® dressings and sauces; Brita® water- filtration products and Burt's Bees® natural personal care products. The company also markets brands for professional services, including Clorox Healthcare®, HealthLink®, Aplicare® and Dispatch® infection control products for the healthcare industry. More than 80 percent of the company's brands hold the No. 1 or No. 2 market share positions in their categories. Clorox's commitment to corporate responsibility includes making a positive difference in its communities. In fiscal year 2014, The Clorox Company and The Clorox Company Foundation contributed more than $16 million in combined cash grants, product donations, cause marketing and employee volunteerism. For more information, visit TheCloroxCompany.com. We are proud to be a member of the Leadership Council on Legal Diversity (“LCLD”). LCLD was formed in 2009 to advance diversity and inclusion in the legal profession. The organization comprises more than 200 corporate chief legal officers and law firm managing partners dedicated to a truly diverse and inclusive legal profession. The leaders who make up the LCLD share the belief that for the profession of the law to prosper, it is necessary to hire, engage, retain, and promote the best talent. -

The Clorox Company

THE CLOROX COMPANY Technology Business Management (TBM) TBM AWARDS CASE STUDY is a methodology, ©2015 Technology Business Management Council. All Rights Reserved community and category of software for data- driven management of the business of IT. Clorox TBM Summary Clorox uses TBM methodologies and their TBM system to integrate and automate their previously fragmented IT planning processes. By almost doubling the accuracy and increasing the detail of its IT spending forecasts they saved 7% on a major outsourcing contract, free up 80 man-hours each quarter, and quickly identify unspent funds so they could be redirected to innovation projects. Program Owner • IT Finance Related Initiatives • Outsourcing TBM Solutions • Budgeting & Forecasting / IT Planning • Cost Transparency Focus of Analysis • Plan vs. Actuals Variance • Cost Centers • Projects Insight • Found $3M error in project budget that helped meet top-down budget cut Outcomes • Improved forecast accuracy from 50% range to 97% for the past 8 quarters • Funded more innovation projects by identifying unspent funds sooner and creating a single, pooled contingency account to benefit all cost centers • 7% savings on new outsourcing contract using line-item budget detail • Avoided 6% IT budget cut with facts to defend spend, showing what projects would actually get cut if target lowered • 80 man-hours removed from forecast each quarter by eliminating spreadsheets • Reduced number of IT cost centers in the financial accounting system Corporate Overview Leading multinational manufacturer and marketer of consumer and professional products with heavily outsourced IT. Brands include Clorox, Formula 409, Pine-Sol, Poett, Liquid-Plumr, Glad, Hidden Valley, K.C. Masterpiece, Kingsford, Brita, Fresh Step, and Burt's Bees. -

The Makers of KC Masterpiece® Announce $5K Donation to Bu Alo

The Makers of KC Masterpiece® Announce $5K Donation to Bualo and Kansas City Food Banks and Challenge Football Fans to Join In 1/21/2021 Kansas City barbecue sauce spreads good will amid football rivalry BUFFALO, N.Y., Jan. 21, 2021 /PRNewswire/ -- All's fair in love and football, and as Bualo and Kansas City's teams rapidly approach the big game this Sunday, the competition is ercer than ever before. In the spirit of healthy competition, a Bualo radio station has nudged a handful of local supermarkets to remove KC Masterpiece® Sauces from their shelves until after gameday, leaving the perfect opening for KC Masterpiece to make the next move. Kill 'em with kindness! "When we heard the hilarious news of our sauces being removed from store shelves in Bualo, albeit temporarily, we saw a great opportunity to serve both communities while encouraging football fans to do the same," said Peddy Khatami, Director of Sales Planning for KC Masterpiece. "We're excited that our sauce is a strong symbol of its namesake city during the lead up to the big game, and even more excited to rally fans from both cities to join us in paying it forward." In response, KC Masterpiece is taking the high road and tapping into Bualo fans' well-documented penchant for doing good and going all-in to support their local communities to help uplift those who may need a bit of extra support this season. While KC Masterpiece may not be on shelves in the Bualo area for now, the brand will make their presence known, donating a total of $5,000 and 5,000 bottles of KC Masterpiece to local food banks FeedMore WNY in Bualo, and Harvesters—The Community Food Network in Kansas City, in the hopes that the team's local superfans will match this good-natured gesture and contribute as well.