Microfinance and Women's Empowerment in Uganda

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Food Security in Albertine Region

ENVIRONMENTAL FOOD DEFENDERS, CHAN BER KU FUR SECURITY IN Dei-Panyimur, Pakwach district, West Nile, Uganda, Albertine Region ALBERTINE REGION A MODEL FOR SUBSISTENCE FARMERS RESILIENCE RIGHT TO FOOD is defined by General Comment No. 12 of the United Nations Committee on Economic, Social and Cultural Rights (the body in charge of monitoring the implementation of the International Covenant on Economic, Social and Cultural Rights - ICESCR in those states which are party to it). FOOD SECURITY All people, at all times, have physical and economic access to sufficient, safe, and nutritious food to meet their dietary needs and food preferences for an active and healthy life (Food and Agriculture Organization - FAO, 1996) CONTEXT 74% of households in northern Uganda suffered drought/irregular rains and longtime insurgence which led to a decline in food production by about 94% and income by 81% forcing two fifths of them to change their dietary patterns. Uganda Bureau of Statistics - UBOS, Government of Uganda - GoU, World Food Programme - WFP, 2013 ← Source: Ian Davison, Tectonics and sedimentation in extensional rifts: Implications for petroleum systems, 2012 ← ACUTE FOOD INSECURITY: NEAR TERM JULY-SEPTEMBER 2020 Famine Early Warning Systems Network - FEWS SEASONAL CALENDAR FOR A TYPICAL YEAR IN UGANDA KEY MESSAGES FROM FEWS ● At the household level, number of people that are Stressed (IPC Phase 2) is higher than average due to reduced income from crop sales and agricultural labor, resulting from below-normal demand for agricultural products; ● The reduced demand for agricultural products is linked to the COVID-19 pandemic. Regionally, the mandatory testing of truck drivers at border crossing points, business uncertainty in destination markets, and the business risks associated with the variations in preventive measures between countries led to higher transportation costs and a decline in exports. -

Founding Voices of Women's and Gender Studies in Uganda

Journal of International Women's Studies Volume 21 Issue 2 Articles from the 5th World Conference Article 2 on Women’s Studies, Bangkok, Thailand April 2020 A Room, A Chair, and A Desk: Founding Voices of Women’s and Gender Studies in Uganda Adrianna L. Ernstberger Marian University Follow this and additional works at: https://vc.bridgew.edu/jiws Part of the Women's Studies Commons Recommended Citation Ernstberger, Adrianna L. (2020). A Room, A Chair, and A Desk: Founding Voices of Women’s and Gender Studies in Uganda. Journal of International Women's Studies, 21(2), 4-16. Available at: https://vc.bridgew.edu/jiws/vol21/iss2/2 This item is available as part of Virtual Commons, the open-access institutional repository of Bridgewater State University, Bridgewater, Massachusetts. This journal and its contents may be used for research, teaching and private study purposes. Any substantial or systematic reproduction, re-distribution, re-selling, loan or sub-licensing, systematic supply or distribution in any form to anyone is expressly forbidden. ©2020 Journal of International Women’s Studies. A Room, A Chair, and A Desk: Founding Voices of Women’s and Gender Studies in Uganda By Adrianna L. Ernstberger1 Abstract This paper studies the birth and development of women’s and gender studies in Uganda. I conducted this research as part of a doctoral thesis on the history of women’s and gender studies in the Global South. Using feminist and standpoint theories, much of the research includes oral histories gathered over the course of three years of field work in Uganda. -

Female Educators in Uganda

Female Educators in Uganda UNDERSTANDING PROFESSIONAL WELFARE IN GOVERNMENT PRIMARY SCHOOLS WITH REFUGEE STUDENTS Johns Hopkins School of Advanced International Studies & Creative Associates International SPRING 2019 | SAIS WOMEN LEAD PRACTICUM PROGRAM Table of Contents TABLE OF FIGURES ............................................................................................................... III ABOUT THE AUTHORS ......................................................................................................... IV ACKNOWLEDGEMENTS ....................................................................................................... V ACRONYMS ....................................................................................................................... VI MAP OF UGANDA............................................................................................................. VII EXECUTIVE SUMMARY ..................................................................................................... VIII 1. INTRODUCTION .............................................................................................................. 10 2. BACKGROUND AND LITERATURE REVIEW...................................................................... 13 3. METHODOLOGY & RESULTS ........................................................................................... 18 METHODOLOGY .......................................................................................................................... 18 ANALYSIS ................................................................................................................................... -

Uganda: Violence Against Women and Information and Communication Technologies

Uganda: Violence against Women and Information and Communication Technologies Aramanzan Madanda, Berna Ngolobe and Goretti Zavuga Amuriat1 Association for Progressive Communications (APC) September 2009 Attribution-Noncommercial-No Derivative Works 3.0 Unported creativecommons.org/licenses/by-nc-nd/3.0/ 1Goretti Zavuga Amuriat is a Senior Gender and ICT Policy Program Officer at Women of Uganda Network (WOUGNET). She spearheadsa campaign for integrating gender into ICT policy processes in Uganda. She is also project coordinator of the Enhancing Income Growth among Small and Micro Women Entrepreneurs through Use of ICTs initiative in Uganda. URL: www.wougnet.org Berna Twanza Ngolobe is an Advocacy Officer of the Gender and ICT Policy Advocacy Program, Women of Uganda Network (WOUGNET) URL: www.wougnet.org Aramanzan Madanda is currently finalising a PhD researching adoption of ICT and changing gender relations using the example of computing and mobile telephony in Uganda. He is also ICT Programme Coordinator in the Department of Women and Gender Studies, Makerere University Uganda. Email: [email protected], URL www.womenstudies.mak.ac.ug. Table of Contents Preface.........................................................................................................................3 Executive summary........................................................................................................4 1. Overview.............................................................................................................................6 -

Uganda and Rwanda

Women, Peace and Security: Practical Guidance on Using Law to Empower Women in Post-Conflict Systems Best Practices and Recommendations from the Great Lakes Region of Africa CASE STUDIES UGANDA AND RWANDA Julie L. Arostegui Veronica Eragu Bichetero © 2014 Julie L. Arostegui and WIIS. All rights reserved. Women in International Security (WIIS) 1111 19th Street, NW 12th Floor Washington, DC 20036 Email: [email protected] Website: http://wiisglobal.org UGANDA HISTORY OF THE CONFLICT Uganda has had a history of civil conflict since its independence from the United Kingdom in 1962 - triggered by political instability and a series of military coups between groups of different ethnic and ideological composition that resulted in a series of dictatorships. In 1966, just four years after independence, the central government attacked the Buganda Kingdom, which had dominated during British rule, forced the King to flee, abolished traditional kingdoms and declared Uganda a republic. In 1971 Army Commander Idi Amin Dada overthrew the elected government of Milton Obote, and for eight years led the country through a regime of terror under which many people lost their lives. Amin was overthrown in 1979 by rebel Ugandan soldiers in exile supported by the army of TanZania. Obote returned to power through the 1980 general elections, ruling with army support. In 1981 a five-year civil war broke out led by the current president, Yoweri Kaguta Museveni and the National Resistance Army (NRA), protesting the fraudulent elections. Known as the Ugandan Bush War, the conflict took place mainly in an area of fourteen districts north of Kampala that was known as the Luwero Triangle. -

Funding Going To

% Funding going to Funding Country Name KP‐led Timeline Partner Name Sub‐awardees SNU1 PSNU MER Structural Interventions Allocated Organizations HTS_TST Quarterly stigma & discrimination HTS_TST_NEG meetings; free mental services to HTS_TST_POS KP clients; access to legal services PrEP_CURR for KP PLHIV PrEP_ELIGIBLE Centro de Orientacion e PrEP_NEW Dominican Republic $ 1,000,000.00 88.4% MOSCTHA, Esperanza y Caridad, MODEMU Region 0 Distrito Nacional Investigacion Integral (COIN) PrEP_SCREEN TX_CURR TX_NEW TX_PVLS (D) TX_PVLS (N) TX_RTT Gonaives HTS_TST KP sensitization focusing on Artibonite Saint‐Marc HTS_TST_NEG stigma & discrimination, Nord Cap‐Haitien HTS_TST_POS understanding sexual orientation Croix‐des‐Bouquets KP_PREV & gender identity, and building Leogane PrEP_CURR clinical providers' competency to PrEP_CURR_VERIFY serve KP FY19Q4‐ KOURAJ, ACESH, AJCCDS, ANAPFEH, APLCH, CHAAPES, PrEP_ELIGIBLE Haiti $ 1,000,000.00 83.2% FOSREF FY21Q2 HERITAGE, ORAH, UPLCDS PrEP_NEW Ouest PrEP_NEW_VERIFY Port‐au‐Prince PrEP_SCREEN TX_CURR TX_CURR_VERIFY TX_NEW TX_NEW_VERIFY Bomu Hospital Affiliated Sites Mombasa County Mombasa County not specified HTS_TST Kitui County Kitui County HTS_TST_NEG CHS Naishi Machakos County Machakos County HTS_TST_POS Makueni County Makueni County KP_PREV CHS Tegemeza Plus Muranga County Muranga County PrEP_CURR EGPAF Timiza Homa Bay County Homa Bay County PrEP_CURR_VERIFY Embu County Embu County PrEP_ELIGIBLE Kirinyaga County Kirinyaga County HWWK Nairobi Eastern PrEP_NEW Tharaka Nithi County Tharaka Nithi County -

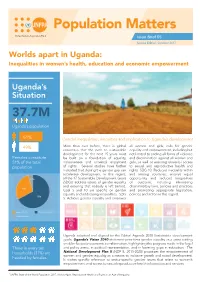

Uganda's Situation

United Nations Population Fund Issue Brief 05 Worlds apart in Uganda: Inequalities in women’s health, education and economic empowerment Uganda’s Situation 37.7M Uganda’s population 51% Gender inequalities, inequities and implication to Uganda’s development 49% More than ever before, there is global all women and girls, calls for gender consensus that the path to sustainable equality and empowerment, including but development for the next 15 years must not limited to ending all forms of violence Females constitute be built on a foundation of equality, and discrimination against all women and 51% of the total inclusiveness and universal enjoyment girls, as well as ensuring universal access population of rights. Several studies have further to sexual and reproductive health and indicated that closing the gender gap can rights. SDG 10: Reduced inequality within accelerate development. In this regard, and among countries; ensures equal 3.7% all the 17 Sustainable Development Goals opportunity and reduced inequalities (SDGs) address issues of gender equality of outcome, including eliminating and ensuring that nobody is left behind. discriminatory laws, policies and practices 23% Goal 5 and 10 are specific on gender and promoting appropriate legislation, equality and addressing inequalities. SDG policies and action in this regard. 55% 5: Achieve gender equality and empower Youth (18-30) Children below 18 Older persons Uganda adopted and aligned to the Global Agenda 2030 Sustainable development goals. Uganda’s Vision 2040 statement prioritizes gender equality as a cross-cutting enabler for socio-economic transformation, highlighting the progress made in the legal Three in every ten and policy arena, in political representation, and in lowering gaps in education. -

Women and the Web Bridging the Internet Gap and Creating New Global Opportunities in Low and Middle-Income Countries

Women and the Web Bridging the Internet gap and creating new global opportunities in low and middle-income countries Women and the Web 1 For over 40 years Intel has been creating technologies that advance the way people live, work, and learn. To foster innovation and drive economic growth, everyone, especially girls and women, needs to be empowered with education, employment and entrepreneurial skills. Through our long-standing commitment to helping drive quality education, we have learned first-hand how investing in girls and women improves not only their own lives, but also their families, their communities and the global economy. With this understanding, Intel is committed to helping give girls and women the opportunities to achieve their individual potential and be a power for change. www.intel.com/shewill For questions or comments about this study, please contact Renee Wittemyer ([email protected]). Dalberg Global Development Advisors is a strategy and policy advisory firm dedicated to global development. Dalberg’s mission is to mobilize effective responses to the world’s most pressing issues. We work with corporations, foundations, NGOs and governments to design policies, programs and partnerships to serve needs and capture opportunities in frontier and emerging markets. www.dalberg.com For twenty-five years, GlobeScan has helped clients measure and build value-generating relationships with their stakeholders, and to work collaboratively in delivering a sustainable and equitable future. Uniquely placed at the nexus of reputation, brand and sustainability, GlobeScan partners with clients to build trust, drive engagement and inspire innovation within, around and beyond their organizations. www.globescan.com Women and the Web 3 FOREWORD BY SHELLY ESQUE Over just two decades, the Internet has worked a thorough revolution. -

In Uganda, but Full Equality with Men Remains a Distant Reality

For more information about the OECD Development Centre’s gender programme: [email protected] UGANDA www.genderindex.org SIGI COUNTRY REPORT Social Institutions & Gender Index UGANDA SIGI COUNTRY REPORT UGANDA SIGI COUNTRY Uganda SIGI Country Report The opinions expressed and arguments employed in this document are the sole property of the authors and do not necessarily reflect those of the OECD, its Development Centre or of their member countries. This document and any map included herein are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area. © OECD 2015 UGANDA SIGI COUNTRY REPORT © OECD 2015 FOREWORD – 3 Foreword Uganda’s economic and political stability over the past two decades has brought unprecedented opportunities to address social inequalities and improve the well-being of citizens. Investments in key human development areas have reaped benefits in poverty reduction, and seen some improvements on a range of socio-economic indicators: but is everyone benefiting? Ugandan women and girls have partially benefited from these trends. New laws and measures to protect and promote women’s economic, political and human rights have been accompanied by impressive reductions in gender gaps in primary and secondary education and greater female political participation. Yet, wide gender gaps and inequalities remain, including in control of assets, employment and health. Economic development may have improved the status quo of women in Uganda, but full equality with men remains a distant reality. Tackling the discriminatory social norms that drive such gender inequalities and ensuring that women can equally benefit from Uganda’s development were twin objectives of this first in-depth country study of the OECD Social Institutions and Gender Index (SIGI). -

The Norms Factor: Recent Research on Gender, Social Norms, and Women's

The norms factor Recent research on gender, social norms, and women’s economic empowerment Rachel Marcus Photo: Scott Wallace / World Bank THE NORMS FACTOR: RECENT RESEARCH ON GENDER, SOCIAL NORMS, AND WOMEN’S ECONOMIC EMPOWERMENT Rachel Marcus, Overseas Development Institute © 2018 International Development Research Centre This paper was commissioned by IDRC through the GrOW program to review and put in context recently-supported research on social norms and the interaction with women’s economic empowerment. Opinions stated in this paper are those of the author and do not necessarily reflect the views of IDRC or the GrOW funders. AUTHOR’S ACKNOWLEDGEMENTS Many thanks to Gillian Dowie, Arjan de Haan, Caroline Harper, and Maria Stavropoulou for comments on previous versions, and to Georgia Plank and Ciara Remerscheid for research assistance. ABOUT THE AUTHOR Rachel Marcus is Senior Research Fellow at the Overseas Development Institute. She specialises in evidence reviews on gender, social norms, youth and adolescence, and in recent years has focused on formal and informal education and women’s and girls’ empowerment. She is a lead advisor on the Advancing Learning and Innovation in Gender Norms (ALIGN) project. ABOUT THE GROW PROGRAM The Growth and Economic Opportunities for Women (GrOW) program is a multi-funder partnership between the United Kingdom’s Department for International Development, the Hewlett Foundation, and the International Development Research Centre. www.idrc.ca/grow ABOUT IDRC CONTACT Part of Canada’s foreign affairs and development International Development Research Centre efforts, IDRC invests in knowledge, innovation, and PO Box 8500, Ottawa, ON solutions to improve lives and livelihoods in the Canada K1G 3H9 developing world. -

Annual Report 2017

ANNUAL REPORT 2017 “BUILDING INCLUSIVE AND RESILIENT LIVELIHOODS” AFARD Annual Report | 2017 1 About AFARD Our Vision: A prosperous, healthy and informed people of West Nile region, Uganda Mission: To contribute to the molding of a region in which the local people (men and women), including those who are marginalized (children, youths, women, the elderly, and Persons Living with disabilities and HIV/AIDS), are able to participate effectively and sustainably and take a lead in the development of the West Nile region. Where we work Headquarters: Nebbi Municipality Satellite offices: Maracha, and Yumbe Outreach districts: Pakwach, Nebbi, Zombo, Arua, Maracha, Yumbe, Moyo and Adjumani. Strategic Direction Our 5-year Strategic Plan 2015- 19 aims to contribute to the socio- economic transformation of 150,000 vulnerable and marginalized people for inclusive and resilient livelihoods. The plan’s strategic pillars are: 1 Climate – smart and nutrition–sensitive agriculture to secure food and nutrition security. Economic empowerment and asset building to lift targeted 2 households out of extreme [asset] poverty. Human capital building to reduce disease burden and 3 increase in literacy rates. 4 Community-led advocacy for responsive and accountable local governance. Community group strengthening to ensure strong sustainable 5 member-owned and –managed groups. Organizational growth and Sustainability to strengthen 6 AFARD’s operational and financial capacity. 2 AFARD Annual Report | 2017 Acronyms AFARD = Agency for Accelerated Regional Development -

Impacts of AIDS on Women Uganda

Impacts of Abstract AIDS on This paper discusses the broad impacts of AIDS on women in Uganda. An extensive literature review and analysis demonstrate that not only is Women. the risk ofHIV-infection and AIDS higher for women than for men in lD Uganda, individual and social impacts of the disease on Ugandan society disproportionately affect women. Both afflicted and non Uganda afflicted women are greatly affected by the AIDS scourge through their multiple roles as individuals, caregivers, and mothers. Research by demonstrates that AIDS in Uganda presents severe socioeconomic implications for women as well as a higher risk for infection due to cultural expectations, subordinate status, and patriarchy in the society. Valerie Durrant About the Author Utah State Valerie L. Durrant recently completed her M.S. in Sociology at Utah University State University. Her thesis was entitled "AIDS Prevention: Applying the Theory of Reasoned Action to Sexual Abstinence and Condom Use." She spent a year in Kampala, Uganda, working with AIDS orphans in 1991-1992. She is currently a doctoral student of Sociology at the University of Maryland at College Park. Working Paper #249 October 1994 Women and International Development Michigan State University 202 lntemational Center, East Lansing, Ml 48824-1035 Phone: 517/353-5040, Fax: 517/432-4845 Email: [email protected], Web: http.//www.isp.msu.edulwid See back page for ordering information and call for papers Copyright 1994 MSU Board of Trustees Impacts of AIDS on Women in Uganda Introduction Illness and death caused by AIDS are taking a big toll on Ugandan society. The World Health Organization estimates that 20 to 30 percent of the adults in Kampala, the capital city of Uganda, are mv infected (Van De Walle 1990).