View Original

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Infant Department 2020-21 Parent's

PARENT’S HANDBOOK INFANT DEPARTMENT 2020-21 Contents PRINCIPAL & HEAD OF INFANTS’ WELCOME ....................................................................................... 4 WHO’S WHO AT BLANCHELANDE ........................................................................................................ 5 Our management structure ..................................................................................................................... 5 The Infant team ...................................................................................................................................... 5 Access to the school building ................................................................................................................... 6 INFANT QUEST ....................................................................................................................................... 7 A DAY IN THE LIFE OF A BLANCHELANDE INFANT .............................................................................. 8 SEMPER FIDELIS – BLANCHELANDE TRADITION .................................................................................. 9 Our ethos .............................................................................................................................................. 9 History of the College .......................................................................................................................... 10 Religious life ....................................................................................................................................... -

Ommuniquécommunique the Newsletter of LA SOCIÉTÉ GUERNESIAISE the Newsletter of LA SOCIÉTÉ GUERNESIAISE Autumn 2010 Issue No.73

WINTER 2009 Issue No.68 CommuniquéCommunique The Newsletter of LA SOCIÉTÉ GUERNESIAISE The Newsletter of LA SOCIÉTÉ GUERNESIAISE Autumn 2010 Issue No.73 Guernsey’s Local Research, Natural History and Conservation Society Guernse y's Local Res ty earch, Natural History and Conservation Socie Christmas Luncheon ....................................................................................................... Collection of Annual Sunday 12 December Transactions We have arranged our Christmas lunch this year at the Hotel de Havelet, at 12.45 pm at a cost of £15.50 Saturday 4 December per person, including tip to staff, but excluding drinks. TheAnnual menu is on theGeneral enclosed sheet. Meeting TransactionsThe Annual Transactions 2007for 2009 will be available for Please send your cheque, payable to collection on or after Saturday 4 December, for those who elected to have a printed version. They can be TheLa Société AGM will Guernesiaise, be held at 7.30 along pm with on Tuesday 24 March at Every member of La Société is entitled to a copy of the Report Lathe Trelade names Hotel of those for the attending purpose and of transacting the following and collectedTransactions, from which La Société is the society’sHQ at Candie annual between journal. 10.00The business:their menu choices, 2007am Transactions and 12.30 werepm, or published from Les in Sablons November Interpretation and many to the Secretary by 1 December. membersCentre have between already 10.00 collected am and their 5.00 copies pm. from Please the a.There To hear will thebe noreport seating of the plan. President, Mrs Pat Costen. Headquartersnote that theyat Candie. will remain Some athave these also locations been delivered until to b. -

WINTER 2009 Issue No.68 Communiqué the Newsletter of LA SOCIÉTÉ GUERNESIAISE

WINTER 2009 Issue No.68 Communiqué The Newsletter of LA SOCIÉTÉ GUERNESIAISE Guernsey’s Local Research, Natural History and Conservation Society Annual General Meeting Transactions 2007 The AGM will be held at 7.30 pm on Tuesday 24 March at Every member of La Société is entitled to a copy of the Report La Trelade Hotel for the purpose of transacting the following and Transactions, which is the society’s annual journal. The business: 2007 Transactions were published in November and many members have already collected their copies from the a. To hear the report of the President, Mrs Pat Costen. Headquarters at Candie. Some have also been delivered to b. To receive the annual statement of accounts. members’ homes by volunteer members of La Société. c. To elect the officers and members of the council. Unfortunately it has not been possible to deliver all the There will be 3 vacancies for Council members as uncollected 2007 Transactions. Mrs J. Grange, L. Curtis and J. Nicolle retire after serving their term of office. Nominations for these, supported by a Therefore if you have not received your 2007 copy of the seconder, should be sent to the Secretary to reach her by Transactions it is available for collection at the headquarters Monday 9 March. at Candie when the office is open on Saturday, Tuesday and e. To appoint auditors. Thursday mornings. f. To award Honorary Membership. g. To approve raising the corporate subscription rate to £200. The journal contains the reports of the various study sections. h. To consider any other matters or propositions affecting For example, the Ornithology Section report contains five La Société. -

Elizabeth College Junior School Guernsey

APPLICATION PACK FOR THE POST OF HEAD Elizabeth College Junior School Guernsey IAPS Pre School, Pre-Prep and Prep School for pupils from 2 to 11 years Required for January, April or September 2018 elizabethcollege.gg/ APPLICATION PACK FOR THE POST OF HEAD Elizabeth College Junior School, Guernsey Jenny Palmer, The Principal of on developing the whole child. It Year 6 whilst girls move on to one Elizabeth College wishes to enjoys success in all academic, of two independent girls’ schools appoint an inspiring primary musical, sporting and artistic on the island: The Ladies’ College or activities and plays an important Blanchelande College. or preparatory school leader role in the lives of its community to succeed Jim Walton on his members, from whom it gains appointment as Head of Clifton much support. The School has The Role College Prep School. seen significant investment and development over the years and its This post provides an outstanding facilities are excellent. opportunity for an inspirational and experienced professional to lead Background The children are motivated, the Junior School into a new phase enthusiastic and co-operative, and of its development, building on the Elizabeth College Junior School is by the time they leave at the end significant successes of the recent an independent Pre-School, Pre- of Year 6 are independent in their past. Preparatory and Preparatory School learning. There is a happy, purposeful for boys and girls aged 2 to 11 years. atmosphere in all parts of this The Headteacher chairs the Senior The Junior School is located on two colourful and inclusive school. -

Combined Candidate Manifestos

How to vote Timeline Voting by Post Where to vote 20 September Your postal vote pack will be posted to you You can vote in person at either your parish during the week beginning 21 September polling station or at a super-polling station. Meet the Candidates and must be returned by 7 October at Parish polling stations will be open only Sunday 20 September 8pm. Completed postal votes may also be to residents of that parish who are on the dropped off to any polling station, or put Electoral Roll. 10:00am – 4:00pm at Beau Sejour in the Sir Charles Frossard House post box If you have opted for a postal vote you before 8pm on 7 October. will not be issued with a ballot paper in Week beginning 21 September Please note it is your responsibility to a polling station, you must use your check postal collection times to ensure postal vote. Postal Vote pack arrives through your letterbox, your pack will arrive before the deadline. For any questions relating to the Election delivered by Guernsey Post please email: [email protected] or call 01481 747579. For all polling station locations and opening 3 – 4 October times go to: Advance Polling www.election2020.gg/voting/where-to-vote/ St Sampson’s High School Saturday 3 October 8am to 8pm The Princess Royal Performing Arts Centre • St Sampson’s High School • The Princess Royal Performing Arts Centre 6 October Sunday 4 October 8am to 8pm Advance Polling • St Sampson’s High School • The Princess Royal Performing Arts Centre Your parish polling station The Princess Royal Performing Arts Centre Tuesday 6 October 8am to 8pm • Your parish polling station • The Princess Royal Performing Arts Centre 7 October Wednesday 7 October 8am to 8pm Election Day • Your parish polling station Your parish polling station • The Princess Royal Performing Arts Centre The Princess Royal Performing Arts Centre Postal Votes must be received by 8:00pm 8 October Vote Count at Beau Sejour Find more information at Correct at time of going to print. -

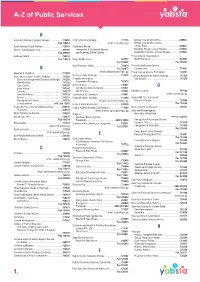

A-Z of Public Services 1

A-Z of Public Services A ActionAid (Guernsey Support Group).............................. 713230 Criminal Justice Strategy ..........................................717105 Artificial Insemination Office ................................235740 Fax 700951 email: [email protected] Artificial Insemination Centre, Adult Services Social Workers ..................................725241 Customs & Excise, Home Farm..........................................................256692 Airport - Administration only ......................................237766 Immigration & Nationality Service Slaughter House, Longue Hougue ......................213090 Fax 239595 see Guernsey Border Agency Livestock Incinerator, Longue Hougue................213090 Archives, Island ..........................................................724512 Finance Sector Development, Fax 715814 Dairy, Bailiffs Cross, ..................................................237777 North Plantation ....................................................234567 Fax 239297 Fax 235015 Data Protection Office ................................................742074 Financial Intelligence Service, B Fax 742077 Ozanne Hall............................................................714081 email: [email protected] Fire & Rescue Service, Fire Station ........................724491 Beaches & Coastline ..................................................717200 Delancey Park, Bookings ..........................................747216 Beau Sejour Leisure Centre, Amherst ....................747200 Footes Lane/Garenne -

Guernsey Community Foundation Voluntary Sector and Social Policy Newsletter October 2016

Guernsey Community Foundation Voluntary Sector and Social Policy Newsletter October 2016 Welcome to the latest edition of the Guernsey Community Foundation’s Voluntary Sector and Social Policy newsletter. My name is Niki Cleal and I have taken over from Emilie Yerby as the Guernsey Community Foundation’s Policy Director and I lead the Foundation’s work on social policy and research. I also support an umbrella organisation of charities and organisations working for, or with, older people, called Ageing Well in the Bailiwick. As many of you will know Emilie was elected as a People’s Deputy in this year’s General Election. You can read more about Emilie’s current work as a Deputy in the States of Deliberation in her blog http://emilieyerby.com/blog/ About Niki Cleal Immediately before joining the Foundation I was commissioned by the States of Guernsey to assist in the development of the Social Security Department’s proposals for a Secondary Pensions System which were agreed by the States Assembly and will lead to the introduction of automatic enrolment in private pension saving. This project gave me a really helpful insight into the States’ policy making process. From 2006-2013, I was the Director of the Pensions Policy Institute, an educational research charity based in London, with overall responsibility for leading and managing the charity where I oversaw a large number of research projects on pension reforms in the UK and was involved in a number of UK Government reviews. Prior to this I spent ten years working as a Civil Servant in the UK Government, at HM Treasury and at the NHS Executive in Leeds, including three years working on health policy. -

Safeguarding Policy

SAFEGUARDING AND CHILD PROTECTION POLICY & PROCEDURES Author/reviewer responsible: LE Last amended: December 2020 Reviewed by: SLT Date of authorisation: February 2021 Authorisation by resolution of: Governors Date of next review: February 2022 Contents GLOSSARY OF TERMS ................................................................................................................ 6 INTRODUCTION ........................................................................................................................ 7 Exceptional circumstances ......................................................................................................... 9 1. CONCERNS ABOUT A CHILD .......................................................................................... 10 The School’s Local Safeguarding Children Board ........................................................................ 10 The Designated Safeguarding Lead (DSL) .................................................................................. 10 Governor for safeguarding ....................................................................................................... 10 The School and MASH ............................................................................................................. 11 Understanding the signs and forms of abuse and taking action ...................................................... 12 Specific safeguarding issues and statutory framework and guidance .............................................. 14 Sexual violence and sexual harassment -

2018 Contents | Editorial

Elizabeth College provides a rich, diverse and exciting experience for pupils of all backgrounds, enabling them to flourish and make the very most of themselves. 2018 CONTENTS | EDITORIAL Editorial FOREWORDS & 2-5 DIRECTORS & STAFF 6-7 FOUNDATION Elizabeth College Junior School FOREWORD 9 SPORTS 32-34 NEWS 10-14 ARTS 35-43 ACTIVITIES 15-27 MUSIC 44-45 ACTIVITIES WEEK 28-31 Elizabeth College ACTIVITIES 49-73 SCOUT CAMP 67 FOOTBALL 91-93 CCF 49-53 CHARITY ACTIVITIES 68 GOLF 94 DUKE OF EDINBURGH AWARDS 54-55 YEAR 11 PROM 69 HOCKEY 95 CCF ADVENTURE TRAINING 56 SIXTH FORM LEAVERS’ DINNER 70 SAILING 96 YOUNG ENTERPRISE 58 INVESTIGATION AND SHOOTING 98-99 72 YOUTH SPEAKS 58 DISCOVERY WEEK SWIMMING 100 SENIOR DEBATING 59 ECO TEAM 73 RACQUET SPORTS 101 DE PUTRON CHALLENGE 59 ARTS 74-84 TRIPS 102-108 IOD MANAGEMENT SHADOWING 60 A YEAR IN ART 74-76 YEAR 12 – 102 CAREERS AND GEOGRAPHY FIELD TRIP 61 DESIGN AND TECHNOLOGY 77 WORK EXPERIENCE POTTERY 78 ART TRIP TO LONDON 103 IOD DIRECTORS OF 61 GUERNSEY LITERARY FESTIVAL 78 HISTORY TRIP TO LONDON 104 TOMORROW CREATIVE WRITING 79-80 CHOIR ST MALO 104-105 HISTORY – CROSS CURRICULAR DAY 62 A REVIEW OF THE KENYA TRIP 106 DESIGN AND TECHNOLOGY 80 62 MUSICAL YEAR SKI TRIP 107 – CASTLES DAY Where are solutions MATHS ROADSHOW 64 THE ELIZABETHAN CONCERT 82 FRENCH EXCHANGE 108 DRAMA – GERMAN EXCHANGE 108 MATHS CHALLENGE 64 82-83 before they’re found? OH WHAT A LOVELY WAR THE RIEMANN SOCIETY 65 EDITORIAL 110-115 DRAMA TRIP TO LONDON 84 LOWER SIXTH FORM PRIZE WINNERS 110-111 65 Welcome to the home of the curious. -

Le Fainel 2, Choisi Fort Saumarez Apartment 7

Summer Property Guernsey Estate Agents Guernsey Open Market Cover Also Featured Le Fainel 2, Choisi Fort Saumarez Apartment 7, FLIP TO BACK FOR Vue Du Godfrey LIFESTYLE FEATURES The Best of the Rest LTS Tax Limited A local fi rm of Chartered Tax Advisers focused on providing a pro-active, high quality service with a personal and fl exible approach. Guernsey and UK tax advice Preparation of tax returns UK residence and domicile planning Inheritance tax planning Emigration and immigration planning Trust tax advice and compliance Fund taxation and reporting obligations Estate planning and executorship services Advising on real estate holding structures ATED and tax on UK residential property Private client services Pensions including: RATS / QROPS / IPPs / EBTs / EFRBS PO Box 20, Les Echelons Court, Les Echelons, St Peter Port, Guernsey, GY1 4AN T: +44 (0)1481 755862 E: [email protected] www.lts-tax.com 2971-LTS TAX SWOFFERS MAGAZINE MAY 2019.indd 1 17/05/2019 16:39 Design/Production GIO Creative Works and 02 2, Choisi 30 £6m - £3m Spike Productions St Peter Port Printed by 44 £3m - £1m Colour Monster 10 Fort Saumarez St Peter's Some Images courtesy of 76 Up to £1m VisitGuernsey 16 Le Fainel 84 St Martin's Rentals 24 Apartment 7, Vue Du Godfrey Contents St Peter Port 2, Choisi For full details of 2, Choisi please contact our Open Market team on 01481 711766 SUMMER 2019 | OPEN MARKET PROPERTIES | SWOFFERS - p3 For full details of 2, Choisi please contact our Open Market team on 01481 711766 Perrys Ref: 17 E5 2, Choisi | St Peter Port | £5,750,000 This impressive Regency home offers elegantly proportioned beautifully presented accommodation. -

Student Handbook 2019 / 2020

STUDENT HANDBOOK 2019 / 2020 CONTENTS Principal’s welcome 2 History of the College 4 Term dates 6 Your attendance 7 Your day 8 Your teachers 8 Your form and form teacher 8 Your voice: the School Council 9 Your House 9 Representing the College 10 Your clubs 10 Your uniform 11 Your spiritual life 11 Your well-being 12 Your peer mentor / your mentee 13 Your behaviour – and what to expect of others 13 Your health: if you’re not feeling well 15 Your stuff: lost property and insurance 16 Your homework 17 1 PRINCIPAL’S WELCOME Dear Pupils, Whether you are a current Blanchelande pupil or just joining, thank you for taking a look at this School Handbook. Hopefully you will find some useful information here. It won’t answer every question that you have, and if you can think of something that’s missing, please tell me. By being educated at Blanchelande you are part of a long and important tradition. A tradition is something that’s bigger than us as individuals. It is a chain that goes before us, and it will continue after us. While we are here, we have the task to enrich, preserve and pass on that tradition to the pupils who we work alongside and who will come after us. So, what is this tradition? At its heart, Blanchelande’s tradition is about joyfulness, kindness and service. No matter what we do – in our academic work, sport or artistic performance – these three things should always be present. If we are doing things without joy, without kindness, and without service to others, we’re getting things wrong. -

SPRING 2008 Communiqué Issue No.66 the Newsletter of LA SOCIÉTÉ GUERNESIAISE

SPRING 2008 Communiqué Issue No.66 The Newsletter of LA SOCIÉTÉ GUERNESIAISE Guernsey’s Local Research, Natural History and Conservation Society Annual Sale Jethou Trips Sunday 18 May at 2.00pm at Blanchelande College, Once again we have arranged with Sir Peter Ogden, the tenant Les Vauxbelets, by kind permission of the Principal of Jethou, to run two trips there. The dates are 17 May, Mrs L Le Page. departing at 1.00pm, returning at 4.00pm, and 14 June, departing at 9.30am and returning at 12 noon. The cost is £13 Please support this enjoyable fund-raising event by attending, per person by prior booking via the Secretary at Candie HQ, helping and contributing items. The following are the stalls to whom you should send £13 pp along with the names of and the organisers who will arrange to collect or to receive those wishing to go. Travel will be on Buz White’s Access goods from you. Any goods may be brought to Challenger, leaving from the Sark boat quay. This is a Les Vauxbelets on the morning of the Sale from 10 o’clock wonderful opportunity to visit a very special place. Charles onwards. David will accompany the 17 May trip for a natural history tour if you wish. Plants - This stall is being organised by the Botany Section Please contact: Jennie Grange tel. 713403 Rhiannon Cook tel. 253705 Orchid Field Walks Cakes - Please contact: The following walks have been arranged and all will start at Julia Peet tel. 238620 10.30am at the car park with the bus shelter at L'Erée.