Report of the Comptroller and Auditor General of India (Local Bodies) for the Year Ended March 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

National Compilation on Dynamic Ground Water Resources of India, 2017

National Compilation on Dynamic Ground Water Resources of India, 2017 Government of India Ministry of Jal Shakti Department of Water Resources, RD & GR Central Ground Water Board Faridabad July 2019 भारत सरकार K C Naik केीय भूिम जल बोड Chairman जल श मंालय जल संसाधन , नदी िवकास और गंगा संर ण िवभाग Government of India Central Ground Water Board Ministry of Jal Shakti Department of Water Resources, River Development and Ganga Rejuvenation FOREWORD Water is crucial to life on Earth, however, its availability in space and time is not uniform. The near utilization of surface water resources has made the public and Government to look towards groundwater resources to supplement the water supply. The ever- increasing demand has resulted in the greater dependence on groundwater and consequently resulting in depletion of groundwater resources in many parts of the country. In the era of climate change, groundwater may act as a buffering resource in the time of drought and it needs to be managed more intensively to enhance its sustainability. The change in groundwater extraction and rainfall pattern necessitate periodic revision of groundwater resources assessment. The report 'National Compilation on Dynamic Groundwater Resources of India, 2017' is a compilation of State-wise assessment carried out jointly by CGWB and State Groundwater Departments at periodical intervals under the supervision of State level Committee of the respective States/UTs and under overall guidance of Central Level Expert Group. The groundwater resources of India are assessed following Groundwater Estimation Methodology, 2015, which takes care of all the relevant parameters contributing to the net annual ground water recharge and extractions for various uses. -

Government of India Ministry of Housing & Urban Affairs

GOVERNMENT OF INDIA MINISTRY OF HOUSING & URBAN AFFAIRS LOK SABHA UNSTARRED QUESTION No. 2503 TO BE ANSWERED ON JANUARY 2, 2018 URBAN INFRASTRUCTURE PROJECTS No. 2503. SHRI R. GOPALAKRISHNAN: Will the Minister of HOUSING & URBAN AFFAIRS be pleased to state: (a) whether the Government has granted approval and released funds for implementing a number of urban infrastructure projects of Tamil Nadu; (b) if so, the details thereof along with the funds allocated/released for the said purpose during the last three years and the current year, city-wise including Madurai city in Tamil Nadu; and (c) the present status of those projects and the steps taken/being taken for expediting these projects? ANSWER THE MINISTER OF STATE (INDEPENDENT CHARGE) IN THE MINISTRY OF HOUSING & URBAN AFFAIRS (SHRI HARDEEP SINGH PURI) (a) to (c) Yes Madam. The Ministry of Housing & Urban Affairs has approved and released funds for implementing urban infrastructure projects in Tamil Nadu under its various schemes, viz., Atal Mission for Rejuvenation and Urban Transformation (AMRUT), Smart Cities Mission (SCM), Page 1 of 2 Heritage City Development and Augmentation Yojana (HRIDAY), Swacchh Bharat Mission – Urban [SBM (U)], Urban Infrastructure Development in Satellite Towns around Seven Mega Cities (UIDSST), Urban Transport (UT), Pradhan Mantri Awas Yojana-Urban [PMAY (U)] and Jawaharlal Nehru National Urban Renewal Mission (JnNURM). Under AMRUT, the Ministry of Housing & Urban Affairs does not approve projects for individual cities but accords approval to the State Annual Action Plans (SAAPs) only. Selection, approval and implementation of individual projects is done by State Government. Further, the Ministry of Housing & Urban Affairs does not release central share of funds city-wise, but funds are released State-wise. -

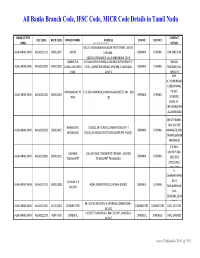

Banks Branch Code, IFSC Code, MICR Code Details in Tamil Nadu

All Banks Branch Code, IFSC Code, MICR Code Details in Tamil Nadu NAME OF THE CONTACT IFSC CODE MICR CODE BRANCH NAME ADDRESS CENTRE DISTRICT BANK www.Padasalai.Net DETAILS NO.19, PADMANABHA NAGAR FIRST STREET, ADYAR, ALLAHABAD BANK ALLA0211103 600010007 ADYAR CHENNAI - CHENNAI CHENNAI 044 24917036 600020,[email protected] AMBATTUR VIJAYALAKSHMIPURAM, 4A MURUGAPPA READY ST. BALRAJ, ALLAHABAD BANK ALLA0211909 600010012 VIJAYALAKSHMIPU EXTN., AMBATTUR VENKATAPURAM, TAMILNADU CHENNAI CHENNAI SHANKAR,044- RAM 600053 28546272 SHRI. N.CHANDRAMO ULEESWARAN, ANNANAGAR,CHE E-4, 3RD MAIN ROAD,ANNANAGAR (WEST),PIN - 600 PH NO : ALLAHABAD BANK ALLA0211042 600010004 CHENNAI CHENNAI NNAI 102 26263882, EMAIL ID : CHEANNA@CHE .ALLAHABADBA NK.CO.IN MR.ATHIRAMIL AKU K (CHIEF BANGALORE 1540/22,39 E-CROSS,22 MAIN ROAD,4TH T ALLAHABAD BANK ALLA0211819 560010005 CHENNAI CHENNAI MANAGER), MR. JAYANAGAR BLOCK,JAYANAGAR DIST-BANGLAORE,PIN- 560041 SWAINE(SENIOR MANAGER) C N RAVI, CHENNAI 144 GA ROAD,TONDIARPET CHENNAI - 600 081 MURTHY,044- ALLAHABAD BANK ALLA0211881 600010011 CHENNAI CHENNAI TONDIARPET TONDIARPET TAMILNADU 28522093 /28513081 / 28411083 S. SWAMINATHAN CHENNAI V P ,DR. K. ALLAHABAD BANK ALLA0211291 600010008 40/41,MOUNT ROAD,CHENNAI-600002 CHENNAI CHENNAI COLONY TAMINARASAN, 044- 28585641,2854 9262 98, MECRICAR ROAD, R.S.PURAM, COIMBATORE - ALLAHABAD BANK ALLA0210384 641010002 COIIMBATORE COIMBATORE COIMBOTORE 0422 2472333 641002 H1/H2 57 MAIN ROAD, RM COLONY , DINDIGUL- ALLAHABAD BANK ALLA0212319 NON MICR DINDIGUL DINDIGUL DINDIGUL -

![Kqøokj] Twu 7] 2019@T;S"B 17] 1941 No](https://docslib.b-cdn.net/cover/7978/kq%C3%B8okj-twu-7-2019-t-s-b-17-1941-no-527978.webp)

Kqøokj] Twu 7] 2019@T;S"B 17] 1941 No

jftLVªh laö Mhö ,yö&33004@99 REGD. NO. D. L.-33004/99 vlk/kj.k EXTRAORDINARY Hkkx II—[k.M 3—mi -[k.M (ii) PART II—Section 3—Sub-section (ii) izkf/dkj ls izdkf'kr PUBLISHED BY AUTHORITY la- 1725] ubZ fnYyh] 'kqØokj] twu 7] 2019@T;s"B 17] 1941 No. 1725] NEW DELHI, FRIDAY, JUNE 7, 2019/JYAISTHA 17, 1941 पयाϕवरण ,,, वन और जलवायु पƗरवतϕन मंJालय अिधसूचना नई Ƙदली, 7 जून , 2019 काकाका.का ...आआआआ.. 19301930((((अअअअ))))....————Oाďप अिधसूचना भारत सरकार के पयाϕवरण, वन और जलवायु पƗरवतϕन मंJालय कƙ अिधसूचना सं. का.आ. 294 9 (अ), तारीख 18 जून, 2018 ůारा भारत के राजपJ, असाधारण मĞ Oकािशत कƙ गई थी िजसमĞ उन सभी ƆिŎयĪ से, िजनको उससे Oभािवत होने कƙ संभावना थी, उस तारीख से, िजसको उŎ अिधसूचना कƙ राजपJ कƙ Oितयां जनता को उपल ध करा दी गई थी, साठ Ƙदन कƙ अविध के भीतर, आपिē और सुझाव आमंिJत Ƙकए गए थे; और, उŎ OाĐप अिधसूचना कƙ रा जपJ कƙ Oितयां जनता को 19 जून, 2018 को उपल ध करा दी गई थĕ ; और, उŎ Oाďप अिधसूचना के Oयुēर मĞ ƆिŎयĪ और पणधाƗरयĪ से OाƁ आϓेपĪ और सुझावĪ पर मंJालय मĞ िवचार Ƙकया गया था ; और, कुथांकुलम पϓी अभयारय तिमलनाडु मĞ ितďनेलवेली िजले के नंगुनेरी तालुक के अंतगϕत 1.2933 वगϕ Ƙकलोमीटर के ϓेJ मĞ फैला ćआ है और इसमĞ ताजे जल कƙ दो आLϕभूिम , अथाϕत् कुथांकुलम और कदंकुलम हġ और यह नंगुनेरी से लगभग 15 Ƙकलोमीटर पिƇम और ितďनेलवेली शहर से 35 Ƙकलोमीटर दूर कुथांकुलम =ाम मĞ िथ त है और ितďनेलवेली से स पकϕ मागϕ मूलकाƞयपŝी से होते ćए जाता है, जो अभयारय से 6 Ƙकलोमीटर दूर है; औरऔरऔर,और ,,, कुथांकुलम पϓी अभयारय उ 08° 29’ से उ 08° 30’ 15” अϓांश और पू 77 0 45’ से पू 77 0 51’ 30” देशांतर के बीच िथत है और यह Oवासी और थानी य जल पिϓयĪ के समूह के िलए जाना जाने वाला एक महवपूणϕ संरिϓत ϓेJ है और इसे 1994 मĞ अभयारय घोिषत Ƙकया गया था और अभयारय मĞ दो ƚसचाई टġक 2804 GI/2019 (1) 2 THE GAZETTE OF INDIA : EXTRAORDINARY [P ART II—SEC . -

Home Tamilnadu Map Tirunelveli District Profile Print TIRUNELVELI

3/6/2017 Home TamilNadu Map Tirunelveli District Profile Print TIRUNELVELI DISTRICT PROFILE • Tirunelveli district is bounded by Virudhunagar district in the north, Thoothukudi district in the east, in the south by Gulf of Mannar and by Kerala State in the west and Kanniyakumari in the southwest. • The District lies between 08º08'09’’N to 09º24'30’’N Latitude, 77º08'30’’E to 77º58'30’’E Longitude and has an areal extent of 6810 sq.km. • There are 19 Blocks, 425 Villages and 2579 Habitations in the District. Physiography and Drainage: • Tirunelveli district falls in Tamiraparani river basin, which is the main river of the district. • The river has a large network of tributaries which includes the Peyar, Ullar, Karaiyar, Servalar, Pampar, Manimuthar, Varahanathi, Ramanathi, Jambunathi, Gadana nathi, Kallar, Karunaiyar, Pachaiyar, Chittar, Gundar, Aintharuviar, Hanumanathi, Karuppanathi and Aluthakanniar draining the district. • The river Tamiraparani originates from the hills in the west and enters Thoothukudi District and finally confluences in Bay of Bengal. • The other two rivers draining the district are river Nambiar and Hanumanathi of Nanguneri taluk in the south that are not part of the Tamiraparani river basin. • The small part of the district in the northern part falls in river Vaippar basin. Rainfall: The average annual rainfall and the 5 years rainfall collected from IMD, Chennai is as follows: Acutal Rainfall in mm Normal Rainfall in mm 2011 2012 2013 2014 2015 896.90 724.00 918.20 1348.50 1546.80 845.10 Geology: Rock Type Geological -

G.I. Journal - 47 1 30/10/2012

G.I. JOURNAL - 47 1 30/10/2012 GOVERNMENT OF INDIA GEOGRAPHICAL INDICATIONS JOURNAL NO. 47 October 30, 2012/ KARTIKA 08, SAKA 1934 G.I. JOURNAL - 47 2 30/10/2012 INDEX S.No. Particulars Page No. 1. Official Notices 4 2. New G.I Application Details 5 3. Public Notice 6 4. GI Applications Pattamadai Pai (‘Pattamadai Mats’) – GI Application No. 195 Nachiarkoil Kuthvilakku (‘Nachiarkoil Lamp’) – GI Application No. 196 Chettinad Kottan – GI Application No. 200 Narayanpet Handloom Sarees – GI Application No. 214 5. General Information 6. Registration Process G.I. JOURNAL - 47 3 30/10/2012 OFFICIAL NOTICES Sub: Notice is given under Rule 41(1) of Geographical Indications of Goods (Registration & Protection) Rules, 2002. 1. As per the requirement of Rule 41(1) it is informed that the issue of Journal 47 of the Geographical Indications Journal dated 30th October 2012 / Kartika 08th, Saka 1934 has been made available to the public from 30th October 2012. G.I. JOURNAL - 47 4 30/10/2012 NEW G.I APPLICATION DETAILS 371 Shaphee Lanphee 25 Manufactured 372 Wangkhei Phee 25 Manufactured 373 Moirang Pheejin 25 Manufactured 374 Naga Tree Tomato 31 Agricultural 375 Arunachal Orange 31 Agricultural 376 Sikkim Large Cardamom 30 Agricultural 377 Mizo Chilli 30 Agricultural 378 Jhabua Kadaknath Black Chicken Meat 29 Manufactured 379 Devgad Alphonso Mango 31 Agricultural 380 RajKot Patola 24 Handicraft 381 Kangra Paintings 16 Handicraft 382 Joynagarer Moa 30 Food Stuff 383 Kullu Shawl (Logo) 24 Textile 23, 24, 384 Muga Silk of Assam (Logo) 25, 27 & Handicraft 31 385 Nagpur Orange 31 Agricultural 386 Orissa Pattachitra (Logo) 24 & 16 Handicraft G.I. -

Tirunelveli Sl.No

TIRUNELVELI SL.NO. APPLICATION NO NAME AND ADDRESS MUTHUKUMAR P, S/O.PETCHIMUTHU K, PLOT 66 KARPAGAM, 1 3250 NAGAR 7TH ST, KTC NAGAR, PALAYAMKOTTAI THIRUNELVELI-627011 VIJAYALAKSHMI.N, D/O NADARAJAN, 2 3251 24, RAJENDRANAGAR, PALAYAMCOTTAI, THIRUNELVELI-627002 THANGAMANI. C D/O.M CHINNAPPA, ARIYANAYAKIPURAM, 3 3252 VEERASIGAMANI, SANKARANKOIL TK- THIRUNELVELI GOVINDARAJ.S, S/O.P.S UDALAIMANI,, 9/32,A.EAST STREET,, 4 3253 VAIKKALPATTY,, METTUR,AMBAI TK THIRUNELVELI-627436 NAGESWARI.N, W/O.MANIKANDAN, DOOR NO. 13/106, AMBALAVANAPURAM 5 3254 PERIA THERU, VICKRAMASINGA - PURAM, AMBASAMUDRAM PO, THIRUNELVELI-627425 SAKILA.S, D/O.SENTHILVEL, 157/2, WEST STREET,, 6 3255 KUVALAIKANNI, SANKARANKOVIL TK., THIRUNELVELI KANAGARAJ.S, S/O.A.SUDALAIMUTHU, 16/A, AMMANKOVIL ST, 7 3256 MEENATCHIPURAM, PANPOZHI, TENKASI TK., THIRUNELVELI-627807 RAVINDRAN.N, S/O NALLA PERUMAL.K, CHIDAMBARAPURAM, 8 3257 KURUVIKULAM VIA, SANKARANKOIL TK. THIRUNELVELIPage 1 RAMESH AMARNATH.B, S/O.S.BALASUBRA- MANIAN, NO:9, 5TH STREET, 9 3258 STATE BANK COLONY, MELAGARAM, TENKASI TK, TIRUNELVELI-627818. JAIKUMAR.G.S S/O.M.G.G.SEKAR, 18, PUTHANERI WEST, 10 3259 SINGANERI PO, NANGUNERI TK., THIRUNELVELI-627108 VELMURUGESWARI.R, W/O AYYAPPAN, NO.10/1037.E SELVA VINAYAGAR PURAM, 11 3260 PAVOOR CHATRAM, TENKASI THIRUNELVELI- 0 JANITA MANO C, W/O AMARAN S, MAIN ROAD, KUVALAI KANNI, 12 3261 KARIVALAM VANDANALLUR THIRUNELVELI 627753 GANAGAMMAL., 14,RASIPURAM, 13 3262 TIRUNELVELI TOWN, THIRUNELVELI 0 RAJESWARI.V D/O.P.VELUCHAMY, AMBEDKAR STREET, 14 3263 MEENATCHIPOURAM, PANPOZHI THIRUNELVELI 0 KUMAR.K, S./O.K.KARUPPIAH,, 13A, KARUPPASAMY 15 3264 KOVIL STREET, KRISHNAPURAM THIRUNELVELI-627811 Page 2 RAJESWARAN.P, S/O.M.PAULRAJ,, 5/76A, AMMAN KOVIL ST, 16 3265 ALAGAPPAPURAM,, SAMBANKULAM, AMBAI THIRUNELVELI-627412 ANBU RAJ. -

Fourteenth Annual Report 2003-2004

Fourteenth Annual Report 2003-2004 M.S. Swaminathan Research Foundation Centre for Research on Sustainable Agricultural and Rural Development Chennai, India M.S. Swaminathan Research Foundation Centre for Research on Sustainable Agricultural and Rural Development Third Cross Road, Institutional Area Taramani, Chennai 600 113 India Telephone : +91 (44) 22541229 +91 (44) 22541698 Fax : +91 (44) 22541319 Email : [email protected]; [email protected] Visit us on the World Wide Web at http://www.mssrf.org Cover Design : The Frontline, Chennai Printed at : AMM Screens Citation : Fourteenth Annual Report: 2003-2004 M S Swaminathan Research Foundation, Chennai 600 113 Contents Chairman’s Introduction ................................................................. 004 Programme Area 100 Coastal Systems Research ............................................................. 013 Programme Area 200 Biodiversity and Biotechnology ..................................................... 034 Programme Area 300 Ecotechnology ................................................................................. 069 Programme Area 400 Reaching the Unreached ................................................................. 092 Programme Area 500 Education, Communication, Training and Capacity Building ........ 109 Programme Area 600 Special Projects .............................................................................. 129 Publications..................................................................................... 132 About the Foundation -

Tirunelveli Sl.No

TIRUNELVELI SL.NO. APPLICATION NO. NAME AND ADDRESS MARUTHAMMAL.C D/O CHINNAPOOCHAN 1 3138 54 MANGAMMA SALAI, TENKASI, THIRUNELVELI 627811 MADASAMY alias RAVICHANDARAN.S 2 3139 S/O K.SUBRAMANIAN 15/91,KAILASAPURAM, ST, THIRUNELVELI 627001 RAMANIAMMAL.R D/O RAJADURAI 3 3140 12/6,TYPE I,CAMP II, HARBOUR ESTATE, TUTICORIN 628004 HEMARANI.J D/O B.JEYARAJ 4 3141 306,S.SIVANTHAKULAM RD, DAMODHAR NAGAR, TUTICORIN ALAGUSELVI.A D/O ALAGARSAMY 5 3142 U 86,MADASAMY KOVIL STREET, ABINAYAMAHAL NEAR, TUTICORIN 628002 KARTHIKA.M D/O K.MANAVALAN 9/A BRYANTNAGAR , 6 3143 10TH STREET, THOOTHUKUDI , TUTICORIN 628008 SARAVANAKUMAR.T S/O THIRUSENTHILNAYAGAM 2/ 95, SUBBAMMAL PURAM, 7 3144 SILANGULAM, OTTAPIDARAM TK, THOOTHUKUDI DIST, TUTICORIN 628718 MANTHIRAMOORTHY.G S/O GOPAL.M 6 SOUTH STREET, 8 3145 EAST URUDAIYARPURAM, THACHANALLUR, THIRUNELVELI 627358 JEGANATH.S OLD NO.2/22 NEW NO.2/6, NORTH STREET, 9 3146 V.KOVIL PATHU, SRIVAIKUNDAM TALUK, THIRUNELVELI 628809 ARUN KUMAR.N S/O C.NATARAJAN 321B/3 VIJAYAPURI RD, 10 3147 SOUTH THITTANKULAM, KOVILPATTI TK, TUTICORIN SUBASH.M 11 3148 1/194 VMS NAGAR, TUTICORIN 628002 NAGARAJ.K S/O T.KARUPPASAMY 23B/1,PAGALAMUDAI YAN ST, 12 3149 T.N.PUTHUKUDI, PULIYANGUDI, THIRUNELVELI SURESH.M S/O K.MURUGAN 13 3150 93C-5 VAKIL ST, KOVILPATTI, TUTICORIN 628501 KUMAR.M S/O U.MANI 14 3151 A.39 HEAVY WATER, COLONY, TOOTHUKUD I 7 VELRAJ.M 5/54 POST OFFICE THERU, 15 3152 KAMBANERI, TENKASI TK, THIRUNELVELI 627857 SADEESH KUMAR.S S/O P.SIVAPERUMAL 16 3153 2/121 VOC STREET, OTTAPIDARAM, TUTICORIN 628401 PREMKUMAR .S S/O.SUDALAIMANI -

Annexure-District Survey Report

10/17/2018 Home TamilNadu Map Tirunelveli District Profile Print TIRUNELVELI DISTRICT PROFILE • Tirunelveli district is bounded by Virudhunagar district in the north, Thoothukudi district in the east, in the south by Gulf of Mannar and by Kerala State in the west and Kanniyakumari in the southwest. • The District lies between 08º08'09’’N to 09º24'30’’N Latitude, 77º08'30’’E to 77º58'30’’E Longitude and has an areal extent of 6810 sq.km. • There are 19 Blocks, 425 Villages and 2579 Habitations in the District. Physiography and Drainage: • Tirunelveli district falls in Tamiraparani river basin, which is the main river of the district. • The river has a large network of tributaries which includes the Peyar, Ullar, Karaiyar, Servalar, Pampar, Manimuthar, Varahanathi, Ramanathi, Jambunathi, Gadana nathi, Kallar, Karunaiyar, Pachaiyar, Chittar, Gundar, Aintharuviar, Hanumanathi, Karuppanathi and Aluthakanniar draining the district. • The river Tamiraparani originates from the hills in the west and enters Thoothukudi District and finally confluences in Bay of Bengal. • The other two rivers draining the district are river Nambiar and Hanumanathi of Nanguneri taluk in the south that are not part of the Tamiraparani river basin. • The small part of the district in the northern part falls in river Vaippar basin. Rainfall: The average annual rainfall and the 5 years rainfall collected from IMD, Chennai is as follows: Acutal Rainfall in mm Normal Rainfall in mm 2013 2014 2015 2016 2017 918.20 1348.50 1546.80 411.90 1127 844.3 Geology: Rock Type Geological -

Mint Building S.O Chennai TAMIL NADU

pincode officename districtname statename 600001 Flower Bazaar S.O Chennai TAMIL NADU 600001 Chennai G.P.O. Chennai TAMIL NADU 600001 Govt Stanley Hospital S.O Chennai TAMIL NADU 600001 Mannady S.O (Chennai) Chennai TAMIL NADU 600001 Mint Building S.O Chennai TAMIL NADU 600001 Sowcarpet S.O Chennai TAMIL NADU 600002 Anna Road H.O Chennai TAMIL NADU 600002 Chintadripet S.O Chennai TAMIL NADU 600002 Madras Electricity System S.O Chennai TAMIL NADU 600003 Park Town H.O Chennai TAMIL NADU 600003 Edapalayam S.O Chennai TAMIL NADU 600003 Madras Medical College S.O Chennai TAMIL NADU 600003 Ripon Buildings S.O Chennai TAMIL NADU 600004 Mandaveli S.O Chennai TAMIL NADU 600004 Vivekananda College Madras S.O Chennai TAMIL NADU 600004 Mylapore H.O Chennai TAMIL NADU 600005 Tiruvallikkeni S.O Chennai TAMIL NADU 600005 Chepauk S.O Chennai TAMIL NADU 600005 Madras University S.O Chennai TAMIL NADU 600005 Parthasarathy Koil S.O Chennai TAMIL NADU 600006 Greams Road S.O Chennai TAMIL NADU 600006 DPI S.O Chennai TAMIL NADU 600006 Shastri Bhavan S.O Chennai TAMIL NADU 600006 Teynampet West S.O Chennai TAMIL NADU 600007 Vepery S.O Chennai TAMIL NADU 600008 Ethiraj Salai S.O Chennai TAMIL NADU 600008 Egmore S.O Chennai TAMIL NADU 600008 Egmore ND S.O Chennai TAMIL NADU 600009 Fort St George S.O Chennai TAMIL NADU 600010 Kilpauk S.O Chennai TAMIL NADU 600010 Kilpauk Medical College S.O Chennai TAMIL NADU 600011 Perambur S.O Chennai TAMIL NADU 600011 Perambur North S.O Chennai TAMIL NADU 600011 Sembiam S.O Chennai TAMIL NADU 600012 Perambur Barracks S.O Chennai -

AND IT's CONTACT NUMBER Tirunelveli 0462

IMPORTANT PHONE NUMBERS AND EMERGENCY OPERATION CENTRE (EOC) AND IT’S CONTACT NUMBER Name of the Office Office No. Collector’s Office Control Room 0462-2501032-35 Collector’s Office Toll Free No. 1077 Revenue Divisional Officer, Tirunelveli 0462-2501333 Revenue Divisional Officer, Cheranmahadevi 04634-260124 Tirunelveli 0462 – 2333169 Manur 0462 - 2485100 Palayamkottai 0462 - 2500086 Cheranmahadevi 04634 - 260007 Ambasamudram 04634- 250348 Nanguneri 04635 - 250123 Radhapuram 04637 – 254122 Tisaiyanvilai 04637 – 271001 1 TALUK TAHSILDAR Taluk Tahsildars Office No. Residence No. Mobile No. Tirunelveli 0462-2333169 9047623095 9445000671 Manoor 0462-2485100 - 9865667952 Palayamkottai 0462-2500086 - 9445000669 Ambasamudram 04634-250348 04634-250313 9445000672 Cheranmahadevi 04634-260007 - 9486428089 Nanguneri 04635-250123 04635-250132 9445000673 Radhapuram 04637-254122 04637-254140 9445000674 Tisaiyanvilai 04637-271001 - 9442949407 2 jpUney;Ntyp khtl;lj;jpy; cs;s midj;J tl;lhl;rpah; mYtyfq;fspd; rpwg;G nray;ghl;L ikaq;fspd; njhiyNgrp vz;fs; kw;Wk; ,izatop njhiyNgrp vz;fs; tpguk; fPo;f;fz;lthW ngwg;gl;Ls;sJ. Sl. Mobile No. with Details Land Line No No. Whatsapp facility 0462 - 2501070 6374001902 District EOC 0462 – 2501012 6374013254 Toll Free No 1077 1 Tirunelveli 0462 – 2333169 9944871001 2 Manur 0462 - 2485100 9442329061 3 Palayamkottai 0462 - 2501469 6381527044 4 Cheranmahadevi 04634 - 260007 9597840056 5 Ambasamudram 04634- 250348 9442907935 6 Nanguneri 04635 - 250123 8248774300 7 Radhapuram 04637 – 254122 9444042534 8 Tisaiyanvilai 04637 – 271001 9940226725 3 K¡»a Jiw¤ jiyt®fë‹ bršngh‹ v§fŸ mYtyf vz; 1. kht£l M£Á¤ jiyt®, ÂUbešntè 9444185000 2. kht£l tUthŒ mYty®, ÂUbešntè 9445000928 3. khefu fhtš Miza®, ÂUbešntè 9498199499 0462-2970160 4. kht£l fhtš f§fhâ¥ghs®, ÂUbešntè 9445914411 0462-2568025 5.