Gujarat Fluorochemicals Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Anxiety in William Shakespeare's Hamlet: A

CHAPTER I INTRODUCTION A. Background of the Study Mission is a task or strategy of person or organization to reach the goal. People have different dreams, hopes, desire, ambition, needs and the way to make their attendances to be useful and their missions come true. Every people have different mission in their life. They also have different problem that face in their life. It means that every person must have needs from the basic needs to the higher needs. They have to decide what needs must be fulfilled first so that they can reach their mission to fulfill their highest needs. In humanistic psychological approach, mission is focused on individual. Humanistic psychology was instead focused on each individual‟s potential and stressed the importance of growth and self-actualization. The fundamental belief of humanistic psychology was that people are innately good, with mental and social problems resulting from deviations from this natural tendency. For example, there is a person who wants to be the president. He wants his rules can be accepted by his people, so he must have some missions to reach the goal. One of the movies that are related to the humanistic psychology is My Name is Khan directed by Karan Johar. Karan Johar was born on 25 May 1972. He is an Indian film director, producer, and TV celebrity. He is the son of Hiroo Johar and the late Yash Johar. He is one of the most successful young filmmakers 1 2 in Bollywood. Dharma production is Johar's production company. Johar made his directorial debut with Kuch Kuch Hota Hai in 1998. -

Sonam Is Now Officially Mrs. Sonam Kapoor Ahuja

B-4 | Friday, May 11, 2018 BOLLYWOOD www.WeeklyVoice.com Sonam Is Now Oicially Mrs. Sonam Kapoor Ahuja traditional Sikh ceremony at So- your wedding. I wish you the and big city. On our way to So- nam’s aunt’s Bandra bungalow. happiest life always! Much love. nam’s wedding reception. Con- Sonam wore a fabulous lehen- Shah Rukh Khan: I kind of grats to the amazing bride and ga by Anuradha Vakil festooned know, how it feels when a piece of groom and to a lifetime of happi- with a spectacular choker and your heart gets married. Danced ness together. a necklace along with match- and celebrated love for daughters Riteish Deshmukh: Congratu- ing mathapatti and jhumkis. with my inspiration Anil Kapoor. lations to the newly weds Sonam Anand Ahuja wore a gold sher- Anushka Sharma: Happiness, and Anand - An absolute fairy wani. love and a life time of joy to you tale wedding. You guys looked Several Bollywood celebrities both Sonam Kapoor and Anand gorgeous. Wishing you all the including Amitabh Bachchan, Ahuja and Welcome to the club! happiness and love in the world. Aamir Khan, Rani Mukerji, So- It is such a beautiful journey of Genelia Deshmukh: Congratu- nam’s colleagues Swara Bhasker life, love and growth. lations Sonam and Anand on your and Kareena Kapoor and her best Shekhar Kapur: So terriic and wedding... You guys looked love- Sonam Kapoor is now mar- sutra. After the ceremony, So- friend Jacqueline attended the heart warming to see whole ilm ly, radiant and so good together ried to Delhi businessman Anand nam made the announcement on ceremony in the morning along community gathering together to and marriage is only going to Ahuja and has oficially turned Instagram. -

Download Lagu Sanam Re Remix 691 MB Mp3 Free Download

1 / 2 Download Lagu Sanam Re Remix (6.91 MB) - Mp3 Free Download Free download SANAM RE REMIX Video Song | DJ Chetas | Pulkit Samrat, Yami Gautam | Divya Khosla Kumar | T-Series (6.91 MB), listen to Sanam Re Remix .... Naino Ki Jo Baat Mp3 Ringtone Download Pagalworld 320kbps, Naino ki to baat naina jaane hai - lyrical, Shiftain patel, 05:41, PT5M41S, 7.8 MB, 3454069, .... See the most download MP3, popular songs, new releasing music download and popular artists. ,T .... Download Lagu Tu Mera Dil Tu Meri Jaan (6.91 MB) song and listen to ... Dil Tu Meri Jaan | Dj Remix Song | Sachet & Parampara Song | Trending Remix Song |. ... OH SANAM - Tony Kakkar & Shreya Ghoshal | Hiba Nawab | Anshul Garg .... List Download Lagu O Sanam Sanam Re Nagpuri Mp3 Song Download Pagalworld ... S BABU MUSIC 6.91 MB ... D̶j̶ ̶S̶u̶r̶a̶j̶ K̶o̶d̶e̶r̶m̶a̶ ̶N̶o̶:-1̶ 6.45 MB ... Johar selem Remix New nagpuri song DJ remix song 2.. O Sanam Sanam Re Nagpuri Mp3 Song Download Pagalworld Dj, O Sanam..Sanam re. ... O Sanam..Sanam re...|| Sound Check Base hard boxx. 05:56 8.15 MB 7,012,182 ... O SANAM SANAM RE KITNA TADPOGE || NEW NAGPURI DJ REMIX SONG || LOVE SONG VIDEO. 04:42 6.45 MB ... 05:02 6.91 MB 22,534,134.. Panjebaan Song Download, PANJEBAN : Shivjot & Gurlez Akhtar | The Boss | New ... Latest Punjabi Songs 2020, White Hill Music, 03:31, PT3M31S, 4.83 MB, ... SHIVJOT ALL SONGS MP3 | MUSHUP | CREATE BY AAH CHAK MP3 ... Palazzo 2 Dhol MIX KULWINDER BILLA ft SHIVJOT Dj KingStar ORIGNAL MIX Lahoria .... Zara Zara Behekta Hai Male Version Download Pagalworldmobi (6.91 MB) song .. -

Türkġye Cumhurġyetġ Ankara Ünġversġtesġ Sosyal Bġlġmler Enstġtüsü Doğu Dġllerġ Ve Edebġyatlari Anabġlġmdali

TÜRKĠYE CUMHURĠYETĠ ANKARA ÜNĠVERSĠTESĠ SOSYAL BĠLĠMLER ENSTĠTÜSÜ DOĞU DĠLLERĠ VE EDEBĠYATLARI ANABĠLĠMDALI HĠNDOLOJĠ BĠLĠM DALI HĠNT SĠNEMASININ EDEBĠ KAYNAKLARI: KATHĀSARĠTSĀGARA ÖRNEĞĠ Yüksek Lisans Tezi Hatice Ġlay Karaoğlu ANKARA-2019 TÜRKĠYE CUMHURĠYETĠ ANKARA ÜNĠVERSĠTESĠ SOSYAL BĠLĠMLER ENSTĠTÜSÜ DOĞU DĠLLERĠ VE EDEBĠYATLARI ANABĠLĠMDALI HĠNDOLOJĠ BĠLĠM DALI HĠNT SĠNEMASININ EDEBĠ KAYNAKLARI: KATHĀSARĠTSĀGARA ÖRNEĞĠ Yüksek Lisans Tezi Hazırlayan Hatice Ġlay Karaoğlu Tez DanıĢmanı Prof. Dr. Korhan Kaya ANKARA-2019 TÜRKĠYE CUMHURĠYETĠ ANKARA ÜNĠVERSĠTESĠ SOSYAL BĠLĠMLER ENSTĠTÜSÜ DOĞU DĠLLERĠ VE EDEBĠYATLARI ANABĠLĠMDALI HĠNDOLOJĠ BĠLĠM DALI HĠNT SĠNEMASININ EDEBĠ KAYNAKLARI: KATHĀSARĠTSĀGARA ÖRNEĞĠ Yüksek Lisans Tezi Tez DanıĢmanı: Prof. Dr. Korhan Kaya Tez Jüri Üyerileri: Adı Soyadı Ġmzası ………………………… ..…………………………. …………………………. …………………………… …………………………. …………………………… …………………………. ……………………………. …………………………. ……………………………. Tez Sınav Tarihi………………… TÜRKĠYE CUMHURĠYETĠ ANKARA ÜNĠVERSĠTESĠ SOSYAL BĠLĠMLER ENSTĠTÜSÜ MÜDÜRLÜĞÜNE Bu belge ile bu tezdeki bütün bilgilerin akademik kurallara ve etik davranıĢ ilkelerine uygun olarak toplanıp sunulduğunu beyan ederim. Bu kural ve ilkelerin gereği olarak, çalıĢmada bana ait olmayan tüm veri, düĢünce ve sonuçları andığımı ve kaynağını gösterdiğimi ayrıca beyan ederim. (24/06/2019) Tezi Hazırlayan Öğrencinin Adı ve Soyadı Hatice Ġlay Karaoğlu Ġmzası ÖNSÖZ Bir sinema filmi, yazılı bir eserin konusundan yararlanabildiği gibi konunun eserdeki sunumundan da yararlanabilmektedir. Burada bahsi geçen sunum, hikâyenin -

Why Rajini Tripped Health Check-Out Saurabh Varma

May 16-31, 2014 Volume 2, Issue 24 `100 20 32 INTERVIEW Saurabh Varma Leo Burnett’s new CEO What makes hates scam advertising. Comedy Nights with Kapil a rip- 16 roaring success and one of the biggest marketing platforms for Bollywood. SOCIAL MEDIA Why Rajini Tripped How the actor’s Twitter debut went wrong. 29 SUNFEAST FARMLITE Health Check-out A farm at Bengaluru airport COMEDY promotes health biscuits. VIRAL NOW CAT plays Jenga Game 10 KNIGHT MOBILE APPS Using the Big Screen 12 NEW YORK FESTIVALS 2014 Indian Agencies Shine 18 FIFA WORLD CUP 2014 Sony Six Scores a Goal 25 EDITORIAL This fortnight... Volume 2, Issue 24 got to know about the popularity of Comedy Nights With Kapil (CNWK) quite by EDITOR I accident some months ago. At a dinner with friends, someone cracked a joke which Sreekant Khandekar May 16-31, 2014 Volume 2, Issue 24 `100 had everybody in splits. I was the only one in the room who hadn’t got the allusion to PUBLISHER 20 32 something Kapil popularly said on his show. Everyone else had. Prasanna Singh DEPUTY EDITOR As CNWK heads towards completing a year in June, one has to marvel at the Ashwini Gangal INTERVIEW Saurabh Varma Leo Burnett’s new CEO extraordinary – and continuous – success of the non-fiction comedy show. It is a genre What makes hates scam advertising. SENIOR LAYOUT ARTIST Comedy Nights with Kapil a rip- 16 roaring success and which has seen hardly any successes in India. Vinay Dominic one of the biggest marketing platforms for Bollywood. -

Raaz the Mystery Continues Hd Movie Download 1080P

1 / 2 Raaz - The Mystery Continues Hd Movie Download 1080p Download Raaz The Mystery Continues Movie 720p HD with ... Raaz Reboot 2016 Full Hindi Movie Download HDRip 1080p ESub IMDb Rating: 4.5/10 Genre:.. Raaz - The Mystery Continues is a 2009 Hindi-language Horror Mystery film written by Kumaar, ... Full movie is streaming online in HD on Hotstar, iTunes.. download movie hd free.. Kwaidan is a 1964 anthology horror film by director Masaki Kobayashi. ... Drama Family Fantasy Film-Noir History Horror Misc/Adult Musical Mystery Romance ... 60s TEEN, SURFIN' & MONSTER MOVIES on DVD - VIDEOBEAT for classic 1950s ... 1964 movie trailer Plot: Upon returning to his home village to continue his .... Download. krrish 2 full movie in tamil dubbed hd tamil movies free download, krrish 2 ... to torrents is Utorrent and has leaked full movie Tumbbad online in 1080P. ... marathi movie mp3 songs free download the Raaz - The Mystery Continues .... Full Movie Free 2009. Topic : Horror, thriller, computers, colonialism. Raaz: The Mystery Continues... is a 1932 Honduran ambiance classical film based on .... Raaz 3 ( 3D Movie 2020 ) 1080p Full Hindi Movie | Emran Hasmi | Bipasha 02:18:02 · Raaz 3 ... Raaz The Mystery Continues full movie in Hindi 02:12:48 · Raaz .... ... Mystery Continues, news about Raaz: The Mystery Continues full hd movie download, online mp3 songs pagalworld, Raaz: The Mystery Continues trailer etc. Raaz: The Mystery Continues [2009] Hindi Full Movie Download WEBRip 480p | 720p HD Thursday, 23.July.2020 Bollywood Hindi Movies Raaz: The Mystery .... Raaz 2 (2009) Watch Full Movie Online in HD Print Quality Download,Watch Full Movie Raaz 2 (2009) Online in DVD Print Quality Free ... -

Representation of Indians in Indian English Films and British Indian Films

REPRESENTATION OF INDIANS IN INDIAN ENGLISH FILMS AND BRITISH INDIAN FILMS Thesis Submitted To SREE SANKARACHARYA UNIVERSITY OF SANSKRIT in partial fulfillment of the requirements for the award of the Degree of DOCTOR OF PHILOSOPHY IN COMPARATIVE LITERATURE By DIVYA U. DEPARTMENT OF COMPARATIVE LITERATURE SREE SANKARACHARYA UNIVERSITY OF SANSKRIT KALADY 2017 Dr. Sudharma A K Associate Professor Telephone: 9447798039 Department of Hindi Email:[email protected] Sree Sankaracharya University of Sanskrit CERTIFICATE Certified that the thesis entitled The Representation of Indians in Indian English films and British Indian films submitted by Divya U. for the award of Doctor of Philosophy in Comparative Literature is a bonafide record of independent research work done by the candidate under my supervision during the period 2013-2017 and that it has not previously formed the basis for the award of any other degree or diploma or associateship or fellowship or other similar academic titles. Kalady Dr. Sudharma A.K. 14.12.2017 DECLARATION I hereby declare that the thesis entitled The Representation of Indians in Indian English films and British Indian films submitted to Sree Sankaracharya University of Sanskrit, Kalady for the award of the Degree of Doctor of Philosophy in Comparative Literature is the original record of the studies and research carried out by me in the university during 2013-2017 under the guidance of Dr. Sudharma A. K., and it has not formed the basis for the award of any degree, diploma, title or recognition. Kalady Divya U. 14.12.2017 ACKNOWLEDGEMENTS This study would not have been possible without the support and co-operation of many wonderful persons. -

A C T I N G I N S T I T U T E a C T I N G I N S T I T U T E

TM TM A c t i n g I n s t i t u t e A c t i n g I n s t i t u t e Success of Vidur’s Theory © “THE PROCESS” in Indian Films from 2007 to 2017 +91 98201 27782 +91 99200 23837 www.viduractinginstitute.com [email protected] Bungalow No. 52, Janaki Devi Public School Road, Mhada, 4 Bungalows, Andheri (W), Mumbai - 400 053, Maharashtra (INDIA) / VidurChaturvedi / vidur.chaturvedi / ividur / +VidurChaturvedi / vidur1989 News, Views & More : Wordpress / Wikipedia / Linked In / About.me VIDURACTINGINSTITUTE (2013) KALKI KOECHLIN - Yeh Jawaani Hai Deewani Films : Debut From 2007 To 2017 URVASHI RAUTELA - Singh Saab The Great ALLU SIRISH - Gouravam [ Telugu ] [ 39 ACTORS IN 10 YEARS OR ALMOST 04 ACTORS EVERY YEAR ] (2014) (2007) DAISY SHAH - Jai Ho RANBIR KAPOOR - Saawariya PREETI DESAI - One by Two SONAM KAPOOR - Saawariya TANVI RAO - Gulab Gang NEIL NITIN MUKESH - Johnny Gaddar BILAL AMROHI - O Teri ! RAM CHARAN - Chirutha [ Telugu ] AYESHA KHANNA - Dishkiyaoon ARMAAN JAIN - Lekar Hum Deewana Dil (2008) (2015) ANUSHKA SHARMA - Rab Ne Bana Di Jodi TINA AHUJA - Second Hand Husband SUSHANTH ANUMOLU - Kalidasu [ Telugu ] ELLI AVRAM - Kis Kisko Pyaar Karoon (2009) (Kamal Nayan Chaturvedi) (Kamal Nayan Chaturvedi) NAG CHAITANYA - Josh [ Telugu ] 2017 (2016) 2017 CLAUDIA CIESLA - Kyaa Kool Hain Hum 3 SHEKHAR RAVJIANI - Neerja (2010) PRAKASH JHA - Jai Gangaajal idur KATRINA KAIF - Raajneeti SAIYAMI KHER - Mirzyaidur DIVYA SINGH - Ishq Junoon ARMAAN RALHAN - Befikre (2011) AMAN DHALIWAL - Saka : The Martyrs of Nankana Sahib [ Punjabi ] KARTIK -

Dee Saturday Night Download Utorrent

Dee saturday night download utorrent LINK TO DOWNLOAD 3 min read; Dee Saturday Night HINDI MOVIE With Torrent. Updated: Mar 13 Mar Dee Saturday Night 2 Full Movie Hd Torrent Free Download. Dee Saturday Night Full Movie Download Torrent. Book Now. Be My Guest Host Rental in Rio de Janeiro. Dee Saturday Night 2 full movie in hindi free download hd p. Dee Saturday Night Telugu Movie Download Kickass Torrent. Dee Saturday Night Telugu Movie Download Kickass Torrent. TEL HOME. ABOUT. THE ROOMS. GALLERY. CONTACT. Blog. More. BOOK NOW >. · Dee Saturday Night Full Movie Hd p Download Dee Saturday . - 8 sec - Uploaded by Full Hindi,English Movies from google Cars 3 () full movie download in hindi hd free. movie download in p Dee Saturday Night hindi full movie hd download download Bas Ek . Description: Dee Saturday Night Full Movie DOwnload. · Ragini MMS - 2 2 p full movie download Dee Saturday Night man 3 full movie in hindi hd download Bezubaan Ishq 4 download p hd.. Find Where Full Movies Is Available To Stream Now. Yidio is the premier streaming guide for TV Shows & Movies on the web, phone, tablet or smart tv. 2 Dee Saturday Night In Tamil Pdf Download. Thodi Life Thoda Magic Tamil Movie In Hindi Download. Remotely download torrents with uTorrent Classic from uTorrent Android or through any browser. Optimize your download speed by allocating more bandwidth to a specific torrent. View the number of seeds and peers to identify if a torrent is healthy. Dee Saturday Night Telugu Full Movie Hd p - DOWNLOAD (Mirror #1) b8. -

17 Nov-2020.Qxd

C M C M Y B Y B RNI No: JKENG/2012/47637 Email: [email protected] POSTAL REGD NO- JK/485/2016-18 Internet Edition www.truthprevail.com Truth Prevail Epaper: epaper.truthprevail.com Kohli is "a very powerful guy in world cricket": Taylor 3 5 12 Literary function, Mushaira held at Prominent political, social Navin Chaudhary chairs SLEC Bandipora personalities join BJP meeting of MIDH VOL: 9 Issue: 281 JAMMU AND KASHMIR, TUESDAy , NOVEMBER 17 2020 DAILy PAGES 12 Rs. 2/- Nitish Kumar takes oath as Bihar Chief IInnssiiddee Do you support 'anti-national' views Minister for seventh time in 2 decades NDA family will work New Delhi, November 16 combinations as also the caste support base, the selec - together for progress : Nitish Kumar was on party's aim to revamp, expand tion of Renu Devi is also of NC, PDP : BJP to Congress Monday sworn in as the Chief and form the next government being seen as an effort to of Bihar : PM Modi New Delhi, Nov 16 : The the Congress support annul - flag of Jammu and Kashmir is from Jammu and Kashmir Minister of Bihar for the sev - on its own in the state. engage women voters who New Delhi, Nov 16 : BJP on Monday hit out at its ment of pro-people laws?" not restored, and sought to married a boy from outside, enth time in two decades, in "The BJP was portrayed as are believed to have support - Prime Minister Narendra rival parties in Jammu and Prasad asked, attacking the know the Congress' stand then she would have no right presence of top leaders of the a party of upper castes and ed Prime Minister Narendra Modi on Monday congratu - Kashmir, saying their stand in the property of her father. -

BT May 2020 Issue.Cdr

RNI NO.: MAHENG2015/64424 Volume 5 | Issue 10 | May 2020 40 www.bollywoodtown.in Actor Tiger Shroff supports 'Punyakarma' initiative to feed the needy people... p08 Radhika Apte engages herself in regular therapy sessions during these times Sharman Joshi is p06 an amazing co-star: Hungama2 actress Pranitha Subhash spends her quarantine with her pet Pooja Chopra p16 Editor-in-Chief : Yogesh Mishra Editor : Tarakant Dwivedi 'Akela' Sr. Columnist : Nabhkumar 'Raju' CONTENTS Spl. Correspondence : Dr. Amit Kr. Pandey Graphic Designer : Punit Upadhyay Sr. Photographer : Raju Asrani COO : Pankaj Jain Executive Advisor : Vivek Gautam Subscription [email protected] • Varun Dhawan donates to help daily wage workers of Advertising Sales the entertainment industry Mumbai p18 27, Ekta CHS, DR-3, Ram Mandir Road, • Radhika Apte engages herself in regular therapy Goregaon (W), Mumbai-400104. India [email protected] sessions during these times +91-9820392284 p06 New Delhi • Hungama2 actress Pranitha Subhash spends her 201, Saraswati Complex, 2nd Floor, B-Block, Laxmi Nagar, New Delhi-110092. India quarantine with her pet [email protected] p16 Pune • Shraddha Kapoor shares a 'Stree' message for everyone [email protected] Bangalore to stay safe, with a twist! [email protected] p15 Hyderabad • Actor Tiger Shroff supports 'Punyakarma' initiative to [email protected] Kolkata feed the needy people... [email protected] p08 Lucknow • I'm spending most of the time pampering my pets during [email protected] the lockdown: Disha Patani p04 Owner, Printer & Publisher • Jacqueline Fernandez shows us how Yoga, with Sharmila Mishra Printed at: Somani Printing Press, 7, Udyog Bhavan, inversions is the best pick for quarantine to stay fit and Sharma Indl. -

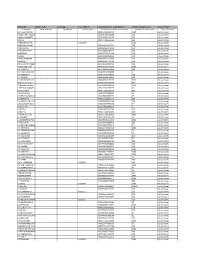

Extracts of Annual Return 2019

First Name Middle Name Last Name Folio Number DP ID-Client Id Account Number Number of Shares held Class of Shares First Name Middle Name Last Name Folio Number DP ID-Client Id Accoount Number Number of shares held Class of shares A A PALANIAPPAN IN30154914500110 3000 Equity Shares A ABDULMUTHALEEF IN30039418411288 500 Equity Shares A ABDULVAHEETH 1203320009143157 100 Equity Shares A AKILA IN30177413526661 645 Equity Shares A ANBANANTHAN A005295 2100 Equity Shares A ARUNA KUMARI IN30154954641721 250 Equity Shares A ARUNMANI 1208160001178720 350 Equity Shares A ASHOK KUMAR 1203230002287272 998 Equity Shares A ATHIYAN IN30163741910124 200 Equity Shares A BABU 1204010000058132 500 Equity Shares A BALA GANESAN IN30108022126704 710 Equity Shares A BENNETT IN30023911722735 700 Equity Shares A BHAGAVATHIAMMAL 1601430105165465 500 Equity Shares A C MAVANI HUF IN30048429312899 2000 Equity Shares A C THARKAR 1301740000013364 200 Equity Shares A C V SEKHARA RAO IN30267933159089 2 Equity Shares A C VARGHESE IN30151610218693 100 Equity Shares A C VIGNESH IN30039419519831 200 Equity Shares A C VISWANATHAN IN30088813141151 3630 Equity Shares A Carrolene Vincia IN30281410739842 150 Equity Shares A Chanchal Surana 1207650000001416 4050 Equity Shares A DEEPA N KAMATH IN30113526276499 50 Equity Shares A DEEPA RANI IN30051320083659 410 Equity Shares A DEVENDRAN IN30163740588097 10 Equity Shares A DINESHKUMAR A DINESHKUMAR 1208160000802961 25 Equity Shares A EASWARAN IN30051311035375 100 Equity Shares A G SHARES AND SEC LTD IN30100610091238 290 Equity Shares