Super Direction

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PCB Men's T20 Matches Playing Conditions for Domestic

PCB Men’s T20 Matches Playing Conditions For Domestic Tournaments 2020/21 (Incorporating the 2017 Code of the MCC Laws of Cricket - 2ndEdition 2019) Effective 3oth September 2020 These Playing conditions shall be read with the PCB Almanac 2019-20 and will apply to all PCB Domestic tournaments with the exclusion of HBL PSL. All matches will be played under the Laws of Cricket 2017 Code (2nd Edition – 2019) and ICC Standard Playing Conditions as adopted hereunder. These Playing Conditions will operate based on the underlying principle that the PCB organized Domestic Tournaments will take precedence over any privately organized league(s) or competition(s). Preamble - The Spirit of Cricket Cricket owes much of its appeal and enjoyment to the fact that it should be played not only according to the Laws (which are incorporated within these Playing Conditions), but also within the Spirit of Cricket. The major responsibility for ensuring fair play rests with the captains, but extends to all players, match officials and, especially in junior cricket, teachers, coaches and parents. Respect is central to the Spirit of Cricket. Respect your captain, team-mates, opponents and the authority of the umpires. Play hard and play fair. Accept the umpire‟s decision. Create a positive atmosphere by your own conduct, and encourage others to do likewise. Show self-discipline, even when things go against you. Congratulate the opposition on their successes, and enjoy those of your own team. Thank the officials and your opposition at the end of the match, whatever the result. Cricket is an exciting game that encourages leadership, friendship and teamwork, which brings together people from different nationalities, cultures and religions, especially when played within the Spirit of Cricket. -

Barbados Advocate

Established October 1895 Brace for an ashy, dusty weekend PAGE 2 Saturday April 10, 2021 $1 VAT Inclusive Barbados pledges its full support to the HERE people of St. Vincent TO HELP THE government of the situation in St. Vincent, Barbados has pledged its with the increased seismic full support to the people activity connected with the La of St. Vincent and the Soufrière volcano and at 8:41 Grenadines, as that island this morning, the volcano battles a dire disaster suffered an explosive eruption. emergency situation, given So basically,what we have been the eruption of its La fearing for quite a while has Soufrière volcano early come to pass. And I want yesterday. to start by expressing our During a swiftly convened complete sympathy as a press conference, Minister of government, as a people of Home Affairs, Information Barbados, for the government and Public Affairs, Wilfred and people of St. Vincent and Abrahams, noted that as the Grenadines, on what is a residents continue to be catastrophic event in their evacuated, Barbados will do its lives. It is almost beyond part to assist, even as the contemplation that a couple situation remains an evolving weeks ago, they were in relative one. comfort and now people are in “Over the last few weeks, From left to right: Attorney General, Dale Marshall, Commanding Officer of the Barbados Coast we’ve been closely monitoring FULL SUPPORT on Page 2 Guard, Commander Mark Peterson; Barbados Defence Force Chief of Staff, Colonel Glyne Grannum; and Press Secretary to the Prime Minister, Roy Morris, during yesterday’s ceremony. -

Weekly Update – 24 October 2009

Parnell Cricket Club Incorporated - Established 1858 Update No.174 – Black Caps Pipped Again Unbelievable – Deja Vue – Black Caps Pipped Again! Call it what you will, the Tie at Eden Park on Sunday, in the series deciding 5th T20, was the most extraordinary coincidence. Again, NZ lost fewer wickets to England, the winner of the “super over”. But who makes the rules by which these games are played? Consider these logics: CRICKET IS A GAME BETWEEN TWO TEAMS – OBJECT TO SCORE MORE RUNS/TAKE MORE WICKETS THAN THE OTHER TEAM • Why then not award the game, when tied, to the Team that loses the fewer wickets – on this basis NZ would have won the ICC CWC (lost only 8 wickets to England’s 10) and yesterday’s T20 (T11) – NZ lost 5, England 7 wickets. • But why, in the ICC CWC, was England able to contest the “super over” – it had lost all 10 wickets. Should have been end of story! • Or, if a “super over” has to be bowled, then wouldn’t it be more logical for the batsmen to be those who were not out or still to bat? Once out means OUT? And bowl only a bowler who hadn’t used his T20 quota. In the interest of fairness and logic! Having got that angst off my chest, what a remarkable game yesterday! Talk of coincidences – and quite extraordinary that the game even took place. We had waited all day Saturday for the forecast rain which, most thankfully, held off. And Sunday morning was fine – when the rain did come, around 11am, it came! The whole of Auckland was blanketed – not too heavy but steady and the wind had dropped. -

Rules & Regulations of Cricket Switzerland Twenty20 Competitions

Rules & Regulations of Cricket Switzerland Twenty20 Competitions Rules & Regulations of Cricket Switzerland Twenty20 Competitions Rules & Regulations of Cricket Switzerland Twenty20 Competitions Page | 1 Rules & Regulations of Cricket Switzerland Twenty20 Competitions Table of Contents 1 TWENTY20 CRICKET ................................................................................................................. 3 1.1 Application of Rules .....................................................................................................................................................................3 1.2 Form of Twenty20 Competitions..............................................................................................................................................3 1.3 Match Arrangements....................................................................................................................................................................3 2 SUPERVISION OF TWENTY20 COMPETITIONS ...................................................................... 3 2.1 Management ...................................................................................................................................................................................3 2.2 The League Committee ...............................................................................................................................................................3 2.3 Duties of the League Committee .............................................................................................................................................3 -

Match Day Hospitality Suites and Experiences Welcome to the Home of Cricket

MATCH DAY HOSPITALITY SUITES AND EXPERIENCES WELCOME TO THE HOME OF CRICKET WE’VE PUSHED THE BOUNDARIES TO WELCOME YOU BACK TO THE HOME OF CRICKET FOR 2021 Celebrate the return of watching live cricket at the most iconic ground in the world, in one of our outstanding hospitality venues. We have a varied top order of hospitality available, suitable for a range of occasions and budgets, each celebrating our unique heritage and exquisite food to ensure a perfect day at Lord’s. We’re looking forward to welcoming you back to the Home of Cricket with friends, colleagues or clients to enjoy our exceptional hospitality, as well as top-level cricket action, in luxury. SUITES Visual Concepts Ultimate Suite ULTIMATE SUITE Visual Concepts Ultimate Suite The ultimate triumph in One-Day International cricket is to win the Cricket World Cup. The ultimate achievement in the fierce England and Australia cricket rivalry is to hold up the Ashes Urn. The ultimate goal for any cricketer is to have their name added to the Lord’s Honours Boards. The Ultimate Suite at Lord’s is the pinnacle of a day at the cricket for any cricket supporter. A brand new hospitality experience for 2021 takes our guests beyond the boundary, with a bounty of extras to create a day like no other. Step onto the hallowed turf where cricket history is made for a pitch inspection before play, and mingle with cricket legends while enjoying world-class cuisine throughout the day, from a newly refurbished private luxury suite and balcony. Visual Concepts Ultimate Suite ULTIMATE SUITE WHATS -

APPENDIX “B” the Super Over (1) Super Over in All Roster and Finals

APPENDIX “B” The Super Over (1) Super Over In all roster and finals matches in which the scores are equal (ie either the number of runs scored or as a result of Duckworth Lewis Stern calculation), the result shall be determined through a tie-breaker called the ‘Super Over’. The “Super Over” involves each team facing one 6-Ball over. The following procedure will apply: (a) Subject to ground, weather or light conditions the Super Over will take place on the scheduled day of the match at a time to be determined by the umpires. In normal circumstances it shall commence 10 minutes after the conclusion of the match. (b) 30 minutes of extra time (taken from the start of the Super Over) is allocated to complete the Super Over. Should play be delayed prior to or during the Super Over, once the playing time lost exceeds the 30 minutes, the Super Over shall be abandoned. (See (2) below) (c) The Super Over will take place on the pitch allocated for the match (the designated pitch) unless otherwise determined by the umpires in consultation with the ground authority and the Match Referee. (d) The umpires shall stand at the same end as they stood during the match. (e) In both innings of the Super Over, the fielding side shall choose which end to bowl from. (f) Only nominated players in the main match may participate in the Super Over. Should any player (including the batsmen and bowler) be unable to continue to participate in the Super Over due to injury, illness or other wholly acceptable reasons, the Laws and Playing Conditions for the main match shall apply. -

Page12 Sports.Qxd (Page 1)

SUNDAY, APRIL 30, 2017 (PAGE 14) DAILY EXCELSIOR, JAMMU RCB all but out of contention for IPL playoffs 5th Jammu Tawi Premier T20 Tournament RCC’s Karmanya wins hearts, PUNE, Apr 29: out below 100 runs twice in the take first strike, with left-arm spin- Paras, Surya guide JCC to big win Indian Premier League. ner Pawan Negi returning with Formidable Royal Challengers RCB were shot out for 49 by impressive figures of 1/18 from his Excelsior Sports Correspondent stipulated 20 overs, losing 3 Bangalore led by India captain Virat wickets in the process. Both but KCCC wins match KKR in an earlier game in the tour- 4 overs. JAMMU, Apr 29: Brilliant Kohli became first team to be the batsmen hit the ball with and 24 runs to the total. Snoop also bagged 3 wickets, while Snoop and nament. Stuart Binny (1/17) and Samuel batting display by Surya Excelsior Sports Correspondent thrown out of contention for play- fluidity and grace and sent the chipped in with 12 runs. Mokshin took 2 wickets each. Chasing a modest 158, Badree (1/31) chipped in with wick- Mahotra (81) and Paras offs after a humiliating 61 -run rival bowlers on a leather JAMMU, Apr 29: Young and In reply, RCC Srinagar scored Nityam and Raghav Sharma Bangalore just kept losing wickets et apiece. Sharma (71) powered Jammu defeat against Rising Pune hunt. For Strikers XI, Lablu promising leg-spinner Karmanya 178 runs in 33.2 overs, thus lost the claimed one wicket each. For his 7- Cricket Club (JCC) to big win Supergiant in an Indian Premier TODAY’S FIXTURE took all 3 wickets to fall. -

List of Office Bearers 2004

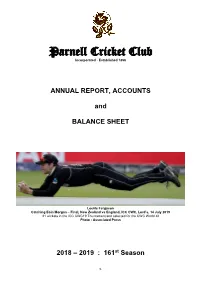

Parnell Cricket Club Incorporated - Established 1858 ANNUAL REPORT, ACCOUNTS and BALANCE SHEET Lockie Ferguson Catching Eoin Morgan – Final, New Zealand vs England, ICC CWC, Lord’s, 14 July 2019 21 wickets in the ICC CWC19 Tournament and selected for the CWC World XI Photo - Associated Press 2018 – 2019 : 161st Season 1. NEW ZEALAND – BLACK CAPS – 2018/19 & ICC CRICKET WORLD CUP 2019 The Club was honoured to have two members selected to represent New Zealand in the past 12 months. WER (WILL) SOMERVILLE and LH (LOCKIE) FERGUSON Will and Lockie – both bowling for Parnell Will, a dream Test debut 7/127 (4/75 & 3/52) and Test won Lockie, 21 wickets at 19.47 in the ICC CWC And Lockie selected for the WORLD XI, ICC CWC 2019 WILL SOMERVILLE Born in 1984, Will, an off spinner, made his 1st Class debut for Otago in 2004/05 for whom he represented till 2007/08. Then, whilst in Sydney, for NSW from 2014 to 2018. Will returned to NZ later last year, accepted a contract with ACA and joined Parnell. Selected for the Black Caps’ series vs Pakistan in the UAE in December, he took, in the 3rd Test on debut, 7/127 (4/75 and 3/52). This enabled NZ to win the Test by 123 runs and so take out the series. Will’s apparences for Parnell were limited but he did well for Auckland and was awarded Cricketer of the Year – the John Bentham Morris Memorial Trophy, the first Parnell player to be so honoured since Ross Morgan in 1978/79. -

Delhi Capsize

TheHitavada JABALPUR Sunday November 1 2020 SPORTS 7 POINTS TABLE DUBAI, Oct 31 (PTI) less cricket. Boult was brilliant upfront removing openers RR look to winning TEAM M W L PTS NRR MUMBAI Indians ensured a top- Shikhar Dhawan (0) and Prithvi MI (Q) 13 9 4 18 +1.296 two finish in the IPL league table DELHI CAPSIZE Shaw (10 off 11 balls) in the pow- RCB 12 7 5 14 +0.048 with a clinical nine-wicket dec- erplay which pegged the Delhi imation of an already battered Capitals back. against Kolkata DC 13 7 6 14 -0.159 Mumbai thrash Delhi by 9 wickets, Delhi Capitals, who wilted under Captain Shreyas Iyer (25 off 29 KXIP 13 6 7 12 -0.133 relentless pressure from Trent ensure Top-2 finish in league stage balls) and Rishabh Pant (21 off DUBAI, Oct 31 (PTI) RR 13 6 7 12 -0.377 Boult and Jasprit Bumrah. 24 balls) then compounded their KKR 13 6 7 12 -0.467 While Boult (3-21 in 4 overs) team’s worries as they failed to THEY have just given their SRH 12 5 7 10 +0.396 dealt telling opening blows, regain the lost momentum. play-offs qualification hopes a CSK 13 5 8 10 -0.532 Jasprit Bumrah (3-17 in 4 overs) The duo, for the umpteenth lift and Rajasthan Royals will look (Updated before RCB vs SRH match) broke the backbone of the Delhi time, looked like playing for to sustaining the momentum Capitals middle-order, choking themselves and the intent was against Kolkata Knight Riders in them to 110 for 9. -

Match Day Hospitality Vitality Blast Welcome to the Home of Cricket

MATCH DAY HOSPITALITY VITALITY BLAST WELCOME TO THE HOME OF CRICKET WE’VE PUSHED THE BOUNDARIES TO WELCOME YOU BACK TO THE HOME OF CRICKET FOR 2021 Celebrate the return of watching live cricket at the most iconic ground in the world, in one of our outstanding hospitality venues. We have a varied top order of hospitality available, suitable for a range of occasions and budgets, each celebrating our unique heritage and exquisite food to ensure a perfect day at Lord’s. We’re looking forward to welcoming you back to the Home of Cricket with friends, colleagues or clients to enjoy our exceptional hospitality, as well as top-level cricket action, in luxury. SUITES Visual Concepts Ultimate Suite ULTIMATE SUITE Visual Concepts Ultimate Suite The ultimate triumph in One-Day International cricket is to win the Cricket World Cup. The ultimate achievement in the fierce England and Australia cricket rivalry is to hold up the Ashes Urn. The ultimate goal for any cricketer is to have their name added to the Lord’s Honours Boards. The Ultimate Suite at Lord’s is the pinnacle of a day at the cricket for any cricket supporter. Visual Concepts Ultimate Suite ULTIMATE SUITE WHATS INCLUDED? NEW-STATE OF THE ART PITCH-FACING PRIVATE SUITE WITH BALCONY SEATING, FOR UP TO 15 GUESTS • DEDICATED HOSPITALITY ENTRANCE FOR FAST-TRACKED LORD’S DINING PRICES ENTRY • • Enhanced premium buffet menu PERSONAL SUITE HOST • Full complimentary bar, including MIDDLESEX v ESSEX Thursday 24 June POA • VISITS FROM THE GREATS OF THE GA• PERSONAL SUITE Veuve Clicquot Champagne, fine wines, HOST craft beers, premium spirits and soft drinks MIDDLESEX v SUSSEX Thursday 1 July POA MIDDLESEX v KENT Friday 16 July POA VITALITY BLAST VITALITY VEUVE CLICQUOT SUITE There have been countless champagne moments at Lord’s over the past two centuries. -

20/20 Competitions Rules

Playing Rules - Readers 20/20 Competition 6. Clothing Players in all matches in the Competition may wear white or coloured clothing. 1. Match Rules 7. Umpires This version of the rules is effective in all matches in the 20-20 Competition 7.1. Umpires will be appointed by the League from the Umpires Panel for all matches (“The Competition”). Except as varied hereunder the Laws of Cricket (2017 Code 2nd Edition 2019) shall apply. 7.2. All clubs must submit a report on the umpires for each match they play in the Competition 2. Management 7.3. Umpires appointed by the Panel shall be entitled to receive a fee of £25 and 2.1. The Competition shall be under the control of the League and all decisions each side shall pay one umpire. For the avoidance of doubt a sole umpire relating to these rules or to matches played in the Competition shall be final shall not be entitled to receive more than £25. On Finals Day the umpires will and binding. be paid by the League. 2.2. Clubs must play their home matches on the main square of their home ground unless prior permission has been obtained from the League to move the 8. Scorers fixture to an alternative ground, if such permission is not given the League Each team shall provide their own competent, non-playing scorer in all will order the match to be re-played on the opponent’s ground. Should the matches. If a team fails to provide a scorer a player has to be nominated from umpires report a pitch as being unfit, the League shall have the option of the team to take up the duty for the entire duration of the match. -

New Zealand Beat India in World Test Final

Friday 35 Sports Friday, June 25, 2021 New Zealand beat India in World Test final SOUTHAMPTON: New Zealand enjoyed the at the presentation ceremony as he paid trib- greatest triumph in their cricket history as ute to a “formidable” India side. “It was just they beat India by eight wickets in the inau- great the heart that our team showed to get gural World Test Championship final at across the line in what was a brilliant Test. We Southampton on Wednesday. Two years after know we don’t always have the stars — we their agonizing Super Over loss to England in rely on a few other bits and pieces to try and the 50-over World Cup final at Lord’s, the stay in games and be competitive and I think Blackcaps claimed their first major global we saw that in this match.” title. In a match in which bowlers held sway, Set a modest target of 139 in 53 overs, New Zealand’s all-pace attack did most dam- New Zealand finished on 140-2 with time to age Wednesday by dismissing India for just spare in a match extended into a reserve sixth 170 in their second innings as blue skies pro- day following two days lost to rain. Off-spin- vided the best batting conditions of the game. ner Ravichandran Ashwin reduced New Tim Southee took 4-48 in 19 overs, with Zealand to 44-2 by removing openers Tom longtime new-ball partner Trent Boult strik- Latham and Devon Conway to the delight of ing twice in an over during his 3-39.