Secluded Destinations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Каталог Îáíîâëåíèé Èþíü 2017 Исполнитель/Название Июнь 2017 А-Б

КАТАЛОГ îáíîâëåíèé èþíü 2017 ИСПОЛНИТЕЛЬ/НАЗВАНИЕ ИЮНЬ 2017 А-Б Abokir Алоэ Вера Черные глаза • Берега A-Lion, SerhioS Арбенина Диана, Ночные Снайперы Ушел в отрыв Наотмашь Artik, Asti Ария Неделимы • Отшельник Brandon Stone Артур Best, Шоуа Александр Ленка Я украду ее • Dj Kan А-Студио Sex Ты • DV Street Ахин Андрей Дороже золота Точно знаю • EMIN (Агаларов Эмин) Ты знаешь все На краю Ты или я • HOMIE Чужой Лето Я скучаю Ivan Я так тебя люблю Не стреляй Бабенко Александр Jamala (Джамала) Ворон • Иные Балакирева Саша Kristina Si Летаю • Дороги • Балашова Елена Тебе не будет больно • Без тебя в голове • Ты знаешь (Забери меня) Дым без огня • L'One Жизнь • Время Кто-то другой • Made In Ukraine Я падаю в небо • Три тополі Барских Макс Mamarika Я люблю тебя Мама ріка Баста Ніч у барі • Евпатория • MC Doni Баян Mix Бомбей Доброй ночи Полегче Би-2 MC Doni, Марвин Миша Алиса • В пути Билан Дима Oxxxymiron Girlfriend • Полигон Lady • Varsal Number One Fan • Сладкая девочка • Берега (Небеса) • Агата Кристи Бум • Опиум для никого Как Ромео • Агурбаш Анжелика Космос Четверг в твоей постели Написать тебе песню Агурбаш Анжелика, Моисеев Борис Ночь без тебя • Две тени Петербургская весна Агутин Леонид, Варум Анжелика Полная луна • Твой голос Так устроен этот мир Агутин Леонид Улетаю Бедная Марта • Шейк под снегом Александрова Марина Богомолова Мария За победу Горько • Алехно Руслан, Сумишевский Ярослав Бородин Арсений Самая милая Стань моей • Аллегрова Ирина Брежнева Вера Изменяла • Близкие люди • Изменяла Бужинская Катя Мир полон звуков Белая пантера -

1 Giant Leap Dreadlock Holiday -- 10Cc I'm Not in Love

Dumb -- 411 Chocolate -- 1975 My Culture -- 1 Giant Leap Dreadlock Holiday -- 10cc I'm Not In Love -- 10cc Simon Says -- 1910 Fruitgum Company The Sound -- 1975 Wiggle It -- 2 In A Room California Love -- 2 Pac feat. Dr Dre Ghetto Gospel -- 2 Pac feat. Elton John So Confused -- 2 Play feat. Raghav & Jucxi It Can't Be Right -- 2 Play feat. Raghav & Naila Boss Get Ready For This -- 2 Unlimited Here I Go -- 2 Unlimited Let The Beat Control Your Body -- 2 Unlimited Maximum Overdrive -- 2 Unlimited No Limit -- 2 Unlimited The Real Thing -- 2 Unlimited Tribal Dance -- 2 Unlimited Twilight Zone -- 2 Unlimited Short Short Man -- 20 Fingers feat. Gillette I Want The World -- 2Wo Third3 Baby Cakes -- 3 Of A Kind Don't Trust Me -- 3Oh!3 Starstrukk -- 3Oh!3 ft Katy Perry Take It Easy -- 3SL Touch Me, Tease Me -- 3SL feat. Est'elle 24/7 -- 3T What's Up? -- 4 Non Blondes Take Me Away Into The Night -- 4 Strings Dumb -- 411 On My Knees -- 411 feat. Ghostface Killah The 900 Number -- 45 King Don't You Love Me -- 49ers Amnesia -- 5 Seconds Of Summer Don't Stop -- 5 Seconds Of Summer She Looks So Perfect -- 5 Seconds Of Summer She's Kinda Hot -- 5 Seconds Of Summer Stay Out Of My Life -- 5 Star System Addict -- 5 Star In Da Club -- 50 Cent 21 Questions -- 50 Cent feat. Nate Dogg I'm On Fire -- 5000 Volts In Yer Face -- 808 State A Little Bit More -- 911 Don't Make Me Wait -- 911 More Than A Woman -- 911 Party People.. -

Hansard Reflect This, That the Policy of This Government, Our Government, the People‟S Partnership Government, As Stated by the Hon

397 Letter of Sympathy Tuesday March 15, 2011 SENATE Tuesday, March 15, 2011 The Senate met at 1.30 p.m. PRAYERS [MR. PRESIDENT in the Chair] LETTER OF SYMPATHY (JAPAN TRAGEDY) Mr. President: Hon. Senators, you will be aware of the tragedy that has occurred in Japan relative to the earthquake, the tsunami and now the question relating to their nuclear reactors. I propose, therefore, on behalf of this Senate to send a letter of sympathy to the Ambassador of Japan and the people of Japan. I propose, therefore, that in your name, such a letter be sent. Thank you. [Desk thumping] LEAVE OF ABSENCE Mr. President: Hon. Senators, I have granted leave of absence to Sen. The Hon. Vasant Bharath who is out of the country and to Sen. Helen Drayton. SENATORS’ APPOINTMENT Mr. President: Hon. Senators, I have received the following correspondence from His Excellency the President, Professor George Maxwell Richards, T.C., C.M.T., Ph.D.: “THE CONSTITUTION OF THE REPUBLIC OF TRINIDAD AND TOBAGO By His Excellency Professor GEORGE MAXWELL RICHARDS, T.C., C.M.T., Ph.D., President and Commander-in-Chief of the Republic of Trinidad and Tobago. /s/ G. Richards President. TO: MR. RABINDRA MOONAN WHEREAS Senator the Honourable Vasant Vivekanand Bharath is incapable of performing his duties as a Senator by reason of his absence from Trinidad and Tobago: 398 Senators’ Appointment Tuesday March 15, 2011 [MR. PRESIDENT] NOW, THEREFORE, I, GEORGE MAXWELL RICHARDS, President as aforesaid, in exercise of the power vested in me by section 40(2)(c) and section 44 of the Constitution of the Republic of Trinidad and Tobago, do hereby appoint you, RABINDRA MOONAN, to be temporarily a member of the Senate, with effect from 14th March, 2011 and continuing during the absence from Trinidad and Tobago of the said Senator the Honourable Vasant Vivekanand Bharath. -

Songs by Artist

Songs by Artist Karaoke Collection Title Title Title +44 18 Visions 3 Dog Night When Your Heart Stops Beating Victim 1 1 Block Radius 1910 Fruitgum Co An Old Fashioned Love Song You Got Me Simon Says Black & White 1 Fine Day 1927 Celebrate For The 1st Time Compulsory Hero Easy To Be Hard 1 Flew South If I Could Elis Comin My Kind Of Beautiful Thats When I Think Of You Joy To The World 1 Night Only 1st Class Liar Just For Tonight Beach Baby Mama Told Me Not To Come 1 Republic 2 Evisa Never Been To Spain Mercy Oh La La La Old Fashioned Love Song Say (All I Need) 2 Live Crew Out In The Country Stop & Stare Do Wah Diddy Diddy Pieces Of April 1 True Voice 2 Pac Shambala After Your Gone California Love Sure As Im Sitting Here Sacred Trust Changes The Family Of Man 1 Way Dear Mama The Show Must Go On Cutie Pie How Do You Want It 3 Doors Down 1 Way Ride So Many Tears Away From The Sun Painted Perfect Thugz Mansion Be Like That 10 000 Maniacs Until The End Of Time Behind Those Eyes Because The Night 2 Pac Ft Eminem Citizen Soldier Candy Everybody Wants 1 Day At A Time Duck & Run Like The Weather 2 Pac Ft Eric Will Here By Me More Than This Do For Love Here Without You These Are Days 2 Pac Ft Notorious Big Its Not My Time Trouble Me Runnin Kryptonite 10 Cc 2 Pistols Ft Ray J Let Me Be Myself Donna You Know Me Let Me Go Dreadlock Holiday 2 Pistols Ft T Pain & Tay Dizm Live For Today Good Morning Judge She Got It Loser Im Mandy 2 Play Ft Thomes Jules & Jucxi So I Need You Im Not In Love Careless Whisper The Better Life Rubber Bullets 2 Tons O Fun -

Current Top 40.Doc

02/2012 Page 1 of 10 2000 + Top 40 A Thousand Years Christina Perri Love Generation Bob Sinclar American Boy Estelle Low Flo Rida Baby Justin Bieber Memories David Guetta Bad Romance Lady Gaga More Usher Bangarang Skrillex Moves Like Jagger Maroon 5 ft C Aguilera Beautiful People Chris Brown Nothing On You Bruno Mars Born This Way Lady Gaga OMG Usher ft Will.I.Am California Gurls Katy Perry On The Floor Jennifer Lopez California King Bed Rihanna Only Girl In The World Rhianna Candyman Christina Aguilera Own This Club Marvin Priest Club Can't Handle Me Flo-Rida Paradise Coldplay Coming Home Diddy Party Rock Anthem LMFAO Cooler Than Me Mike Posner Poker Face Lady Gaga Count On Me Bruno Mars Price Tag Jessie J ft B.O.B Dance In The Dark Lady Gaga Pumped Up Kicks Foster The People Dedication To My Ex Lloyd ft Andre 3000 Read All About It Professor Green Disturbia Rhianna Riding Solo Jason Derulo DJ Got Us Falling In Love Usher ft Pitbull Right Round Flo Rida Do You Remember? Jay Sean Rock DJ Robbie Williams Don't Stop The Party Black Eyed Peas Rolling In The Deep Adele Don't Wanna Go Home Jason Derulo Rude Boy Rhianna Down Jay Z ft Lil Wayne Run The World Beyonce Dynamite Taio Cruz S&M Rhianna Electric Feel MGMT Set It Off Timomatic Empire State Of Mind Jay Z ft Alicia Keys Sex On Fire Kings Of Leon Evacuate The Dancefloor Cascada Sexy & I Know It LMFAO Feel So Close Calvin Harris Sexy Back Justin Timberlake Fireflies Owl City Shots LMFAO ft Lil Jon Forever Chris Brown Single Ladies Beyonce From The Music Potbelleez Somebody That I Used To -

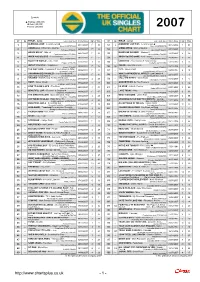

Chartsplus Year-End 2007

Symbols: p Platinum (600,000) ä Gold (400,000) è Silver (200,000) 2007 07 06 TITLE - Artist Label (Cat. No.) Entry Date High Wks 07 06 TITLE - Artist Label (Cat. No.) Entry Date High Wks ä 7 p 4 1 -- BLEEDING LOVE - Leona Lewis 03/11/2007 1 10 51 2 A MOMENT LIKE THIS - Leona Lewis 30/12/2006 1 31 Syco (88697175622) Syco (88697050872) è 10 2 -- UMBRELLA - Rihanna ft. Jay-Z 26/05/2007 1 33 52 -- GIMME MORE - Britney Spears 27/10/2007 3 11 Def Jam (1735491) Jive (88697186802) è 5 3 -- GRACE KELLY - Mika 20/01/2007 1 51 53 -- MAKES ME WONDER - Maroon 5 19/05/2007 2 20 Casablanca/Island (1721083) Octone/A&M (1734956) 4 -- WHEN YOU BELIEVE - Leon Jackson 29/12/2007 12 2 54 -- WHEN YOU'RE GONE - Avril Lavigne 28/04/2007 3 31 Syco (88697220162) RCA (88697119262) 5 -- RULE THE WORLD - Take That 27/10/2007 2 11 55 -- UNINVITED - Freemasons ft. Bailey Tzuke 13/10/2007 8 13 Polydor (1746285) Loaded (LOAD118CD) 6 -- ABOUT YOU NOW - Sugababes 29/09/2007 14 15 56 85 REHAB - Amy Winehouse 28/10/2006 7 63 Island (1748657) Island (1709535) 7 -- THE WAY I ARE - Timbaland ft. Keri Hilson [& DOE] 30/06/2007 12 28 57 -- 1973 - James Blunt 08/09/2007 4 18 Interscope (1742316) Custard/Atlantic (AT0285CDX) 8 -- (I'M GONNA BE) 500 MILES - The Proclaimers ft. 24/03/2007 13 14 58 -- WHAT A WONDERFUL WORLD - Eva Cassidy & 22/12/2007 1 3 Brian Potter & Andy Pipkin è EMI (COMICCD01) Katie Melua Blix Street/Dramatico (TD001) 9 -- VALERIE - Mark Ronson ft. -

Borghesia Corvus Corax

edition January - March 2015 free of charge, not for sale 16 quarterly published music magazine BORGHESIA CORVUS CORAX SEX GANG CHILDREN ELUVEITIE + RASTABAN SHE PAST AWAY + COCKSURE EMPUSAE + SAIGON BLUE RAIN CUÉLEBRE + 2ND CIVILIZATION - 1 - WOOL-E-TOP 10 WOOL-E-TOP 10 Best Selling Releases Best Selling Releases (Oct/Nov/Dec 2014) (January – December 2014) 1. MAN WITHOUT WORLD 1. THE KLINIK And Then It Ends (MC) Box (8CD) 2. VARIOUS ARTISTS 2. TRANSFIGURE The 15th (MC) Transfigure (MC) 3. FACTICE FACTORY 3. LUMINANCE The White Days (MC/CD/LP) Icons And Dead Fears (MC) 4. TRUE ZEBRA 4. UNIDENTIFIED MAN Adoremotion (CD) Remedy For Melancholy (MC) 5. SONAR 5. MAN WITHOUT WORLD Shadow Dancers (CD) And Then It Ends (MC) 6. SEBASTIEN CRUSENER 6. LUMINANCE / ACAPULCO CITY Dwaalspoor (MC) HUNTERS 7. WOODBENDER, CINEMA The Cold Rush (MC) PERDU, THE [LAW-RAH] 7. L’AVENIR COLLECTIVE The Wait (LP/CD) Blue Ruins Under Yellow Skies (MC) 8. PAS DE DEUX 8. NINE CIRCLES Cardiocleptomanie (LP) Alice (CD/LP) 9. SIMI NAH 9. NEUTRAL Be My Guest (CD) Grå Våg Gamlestaden (LP/MC) 10. VARIOUS ARTISTS 10. KIRLIAN CAMERA The 15th (MC) One (LP+7”) The Wool-E Shop - Emiel Lossystraat 17 - 9040 Ghent - Belgium VAT BE 0642.425.654 - [email protected] - 32(0)476.81.87.64 www.peek-a-boo-magazine.be - 2 - contents 04 CD reviews 22 Interview CUÉLEBRE 06 Interview SAIGON BLUE RAIN 24 MOVIE reviews 08 Interview RASTABAN 26 Interview SEX GANG CHILDREN 10 Interview EMPUSAE 28 CD reviews 12 CD reviews 30 Interview COCKSURE 14 Interview CORVUS CORAX 34 CD reviews 16 Interview -

ACRONYM 11 - Round 1

ACRONYM 11 - Round 1 1. Players' health slowly deteriorates if this object is stolen from them by Swipin' Stu, a denizen of Pinna Park. Before joining Rosalina at the Comet Observatory, Luma steals this thing at the end of a 2010 platformer. An impossibly frustrating monkey named Ukiki tries to steal this object on (*) Tall, Tall Mountain, a level from a certain Nintendo 64 game; that game features Metal, Vanish, and Wing variations of this object. For 10 points, name this red garment that unusually has eyes and a name in Super Mario Odyssey. ANSWER: Mario's hat (or Mario's cap; accept Cappy after "eyes and a name"; prompt on answers that don't identify Mario) <Vopava> 2. An old woman in this series uses a pendant to allegedly determine that another character was having twins, and claims to know that because of "gypsy blood." On this series, the terms "thicker than blood" and "more precious than oil" are used to describe the maple (*) syrup produced by the Blossom family. In a season finale of this series, a father played by Luke Perry is shot in an armed robbery and Cheryl is stopped from drowning herself in a certain body of water. Cole Sprouse plays Jughead Jones in, for 10 points, what CW series based on Archie Comics characters? ANSWER: Riverdale <Nelson> 3. One of these occurrences starts "from my bed" in Oasis's "Don't Look Back in Anger." A track from Green Day's album ¡Tré! calls for 99 of these events, which named Green Day’s 2013 tour. -

Calvin Harris I Created Disco Tpb

Calvin harris i created disco tpb Download I Created Disco - Calvin Harris torrent or any other torrent from the Audio Music. Direct download via magnet link. Download Calvin Harris - I Created Disco (iTunes Version) torrent or any other torrent from the Audio Other. Direct download via magnet link. Download Calvin Harris - I Created Disco torrent or any other torrent from Other Music category. See also MusicBrainz (release) [MusicBrainz (release)] ; Calvin Harris - I داﻧﻠﻮد آﻟﺒﻮم · Calvin Harris - I Created Disco داﻧﻠﻮد آﻟﺒﻮم .MusicBrainz (artist) [MusicBrainz (artist)] ; Amazon [Amazon]. Identifier Calvin Harris - I Created Disco Album Free download. Watch the video, get the download or listen to Calvin Harris · ﺑﺎ ﻟﯿﻨﮏ ﻣﺴﺘﻘﯿﻢ Created Disco – I Created Disco for free. I Created Disco appears on the album I Created Disco. Discover more. Come and download disco calvin harris absolutely for free, Fast and Direct Downloads also [tbox] Calvin Harris i Created Disco(www Widgetzone Co Uk). I Created Disco mp3 album by CALVIN HARRIS. Merrymaking At My Place, CALVIN HARRIS, , Download at iTunes. Play Song, 2. Colours, CALVIN. I Created Disco | Calvin Harris to stream in hi-fi, or to download in True CD Quality on Find album reviews, stream songs, credits and award information for I Created Disco - Calvin Harris on AllMusic - - Scottish remixer, songwriter, former. I Created Disco is the debut studio album by Scottish musician Calvin Harris, released on 15 .. Print/export. Create a book · Download as PDF · Printable version. Buy I Created Disco at the Music Store. Everyday low Available to Download Now . This item:I Created Disco by Calvin Harris Audio CD £ Listen to songs from the album I Created Disco, including "Merrymaking At My Even Calvin Harris might not recognize the Calvin Harris of this debut; the. -

English: C KARAOKE CATALOGUE: C Artist Song Title C

C K A A T R A A L O O K G E U E Songs in English: C KARAOKE CATALOGUE: C Artist Song Title C. J. Lewis Sweets for My Sweet C. W. McCall Convoy C. W. McCall Wolf Creek Pass C+C Music Factory Gonna Make you Sweat (Everybody Dance Now) [Duet] C+C Music Factory Things That Make You Go Hmmm Cab Calloway & the Blues Brothers Minnie the Moocher Band Caesars Jerk It Out Cage the Elephant Cigarette Daydreams Cage the Elephant Shake Me Down Cake Frank Sinatra Cake Let Me Go Cake Never There Cake Short Skirt-Long Jacket Cake The Distance Cal Smith Country Bumpkin Cali Swag District Kickback Calling Adrienne Calling Anything Calling For You Calling Our Lives Calling Wherever You Will Go Calloway I Wanna Be Rich Calum Scott Dancing on My Own Calum Scott No Matter What Calum Scott Rhythm Inside Calum Scott What I Miss Most Calum Scott You Are the Reason Calvin Harris Acceptable in the 80s Calvin Harris Faith Calvin Harris Feel So Close Calvin Harris Flashback Calvin Harris I'm Not Alone Calvin Harris Merrymaking at My Place Calvin Harris My Way Calvin Harris Ready for the Weekend Calvin Harris Summer Calvin Harris The Girls Calvin Harris & Alesso ft Hurts Under Control Calvin Harris & Disciples How Deep Is Your Love Calvin Harris & Disciples How Deep Is Your Love [Duet] KARAOKE CATALOGUE: C 03/11/2020 Page 1 of 41 KARAOKE CATALOGUE: C Calvin Harris & Dua Lipa One Kiss Calvin Harris & Rag'n'Bone Man Giant Calvin Harris & Sam Smith Promises Calvin Harris & The Weeknd Over Now Calvin Harris ft Ayah Marar Thinking About You Calvin Harris ft Ellie Goulding -

Radical Left in Europe 2017

Radical Left in Europe 2017 Documentation of contributions about the radical Left in Europe in addition of the Work- shop of Transform and Rosa Luxemburg Foundation July 7- 9 2016 Cornelia Hildebrandt/Luci Wagner 30.07.2017 DOCUMENTATION: RADIKAL LEFT IN EUROPE AND BERLIN SEMINAR 2016 2 Content Preface ..................................................................................................................................................... 3 Hildebrandt, Cornelia and Baier, Walter ............................................................................................... 10 Radical Left Transnational Organisation Brie, Michael and Candeias, Mario........................................................................................................ 29 The Return of Hope. For an offensive double strategy Dellheim, Judith ..................................................................................................................................... 42 On scenarios of EU development Jokisch, René ......................................................................................................................................... 54 Reconstruction of the EU legislation and Institutions with consequences for the Left Cabanes, de Antoine ............................................................................................................................. 57 The metamorphosis of the Front National Lichtenberger, Hanna ........................................................................................................................... -

Songs by Artist

Nice N Easy Karaoke Songs by Artist Bookings - Arie 0401 097 959 10 Years 50 Cent A1 Through The Iris 21 Questions Everytime 10Cc Candy Shop Like A Rose Im Not In Love In Da Club Make It Good Things We Do For Love In Da' Club No More 112 Just A Lil Bit Nothing Dance With Me Pimp Remix Ready Or Not Peaches Cream Window Shopper Same Old Brand New You 12 Stones 50 Cent & Olivia Take On Me Far Away Best Friend A3 1927 50 Cents Woke Up This Morning Compulsory Hero Just A Lil Bit Aaliyah Compulsory Hero 2 50 Cents Ft Eminem & Adam Levine Come Over If I Could My Life (Clean) I Don't Wanna 2 Pac 50 Cents Ft Snoop Dogg & Young Miss You California Love Major Distribution (Clean) More Than A Woman Dear Mama 5Th Dimension Rock The Boat Until The End Of Time One Less Bell To Answer Aaliyah & Timbaland 2 Unlimited 5Th Dimension The We Need A Resolution No Limit Aquarius Let The Sun Shine In Aaliyah Feat Timbaland 20 Fingers Stoned Soul Picnic We Need A Resolution Short Dick Man Up Up And Away Aaron Carter 3 Doors Down Wedding Bell Blues Aaron's Party (Come And Get It) Away From The Sun 702 Bounce Be Like That I Still Love You How I Beat Shaq Here Without You 98 Degrees I Want Candy Kryptonite Hardest Thing The Aaron Carter & Nick Landing In London I Do Cherish You Not Too Young, Not Too Old Road Im On The Way You Want Me To Aaron Carter & No Secrets When Im Gone A B C Oh, Aaron 3 Of Hearts Look Of Love Aaron Lewis & Fred Durst Arizona Rain A Brooks & Dunn Outside Love Is Enough Proud Of The House We Built Aaron Lines 3 Oh 3 A Girl Called Jane Love Changes