Malabar Regional Co-Operative Milk Producers' Union Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fy2015164thinterimdividend.Pdf

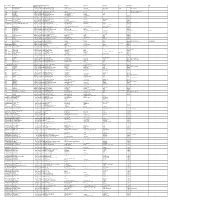

FOLIO_DEMAT ID NAME DIVIDEND WARRANT MICR ADDRESS 1 ADDRESS 2 ADDRESS 3 ADDRESS 4 CITY PINCOD JH1 JH2 AMOUNT NO 001221 DWARKA NATH ACHARYA 180000.00 16400029 5 JAG BANDHU BORAL LANE CALCUTTA 700007 000642 JNANAPRAKASH P.S. 1800.00 16400038 54773 POZHEKKADAVIL HOUSE P.O.KARAYAVATTAM TRICHUR DIST. KERALA STATE 68056 MRS. LATHA M.V. 000691 BHARGAVI V.R. 1800.00 16400040 54775 C/O K.C.VISHWAMBARAN,P.B.NO.63 ADV.KAYCEE & KAYCEE AYYANTHOLE TRICHUR DISTRICT KERALA STATE 000902 SREENIVAS M.V. 1800.00 16400046 54781 SAI SREE, KOORKKENCHERY TRICHUR - 7 KERALA STATE MRS. RAJALAKSHMI SREENIVAS 001036 SANKAR T.C. 9000.00 16400052 54787 DAYA MANDIRAM TRICHUR - 4. KERALA MRS. MADHAVIKUTTY T.A. 002679 NARAYANAN P S 3600.00 16400074 54809 PANAT HOUSE P O KARAYAVATTOM, VALAPAD THRISSUR KERALA 002769 RAMLATH V E 1800.00 16400079 54814 ELLATHPARAMBIL HOUSE NATTIKA BEACH P O THRISSUR KERALA 002966 KUNHIRAMAN K 1800.00 16400098 54833 KADAVATH HOUSE OZHINHA VALAPPU (PO) (DIST) KARASAGOD 000000 003292 SURENDARAN K K 1692.00 16400113 54848 KOOTTALA (H) PO KOOKKENCHERY THRISSUR 000000 003427 JAYAPRAKASH P V 1692.00 16400118 54853 PULIPARAMBIL HOUSE VATANAPILLY THRISSUR 000000 003442 POOKOOYA THANGAL 1692.00 16400120 54855 MECHITHODATHIL HOUSE VELLORE PO POOKOTTOR MALAPPURAM 000000 1201910102051401 RAM PARKASH 4500.00 16400130 54865 HOUSE NO - 24 WARD NO-15 Pehowa 136128 001431 JITENDRA DATTA MISRA 10800.00 16400143 54878 BHRATI AJAY TENAMENTS 5 VASTRAL RAOD WADODHAV PO AHMEDABAD 382415 IN30047610042162 REKHA ANIL WAGLE 3510.00 16400151 54886 202 VINAYAK ANGAN OPP V I P SHOWROOM OLD PRABHADEVI ROAD PRABHADEVI MUMBAI 400025 ANIL VINAYAK WAGLE IN30047643177287 ANJANEYA SECURITIES SERVICES PRIVATE LIM 90000.00 16400152 54887 201 STAR APARTMENT A B NAGVEKAR MARG PRABHADEVI MUMBAI 400025 IN30021412035484 JUHI SAKHUJA 1800.00 16400156 54891 FLAT NO 12 1ST FLOOR WITS END HILL ROAD BANDRA WEST MUMBAI MAHARASHTRA 400050 001012 SHARAVATHY C.H. -

Accused Persons Arrested in Kozhikodu City District from 20.11.2016 to 26.11.2016

Accused Persons arrested in Kozhikodu city district from 20.11.2016 to 26.11.2016 Name of the Name of Name of the Place at Date & Court at Sl. Name of the Age & Cr. No & Sec Police Arresting father of Address of Accused which Time of which No. Accused Sex of Law Station Officer, Rank Accused Arrested Arrest accused & Designation produced 1 2 3 4 5 6 7 8 9 10 11 Elathur PS Cr Ombathamkandathil Thadangattuv 20-11-2016 no.923/16 Bailed by 1 Unni Sankaran 49/16 M , Westhill, Elathur SI Arunprasad ayal 18.30 Hrs U/S118(a) of Police kozhikode KP Act Elathur PS Cr Thadangattuvayal(H Thadangattuv 20-11-2016 no.924/16 Bailed by 2 Lineesh Sivadasan 31/16 M Elathur SI Arunprasad ), Eranhikkal ayal 18.35 Hrs U/S118(a) of Police KP Act Elathur PS Cr Sargam, Madusoodhan 20-11-2016 no.925/16 Bailed by 3 Sajeesh 37/16 M Netungatiline, Eranhikkal Elathur SI Arunprasad an 20.35 Hrs U/S279&185 Police Mankav, Kozhikode of MV Act Elathur PS Cr Udumbichithodukayi 20-11-2016 no.926/16 U/S Bailed by 4 Rajesh Krishnan 41/16 M Eranhikkal Elathur SI Arunprasad l, Puthiyangadi 20.41 Hrs 15(c) of Police Abkari Act Elathur PS Cr Sreechithra, 29/16 20-11-2016 no.927/16 U/S Bailed by 5 Prajeesh Sasi Maviliparamu, Eranhikkal Elathur SI Arunprasad M 20.55 Hrs 15(c) of Police Edakkad Abkari Act Elathur PS Cr Bavamahal, 21-11-2016 no.928/16 Bailed by 6 Sakkariya Cheriyabava 42/16 M Methalakath(H) Puthiyanirath Elathur SI Arunprasad 00.15 Hrs U/S279&185 Police elathur of MV Act Elathur PS Cr Padinharethekkodut 21-11-2016 no.929/16 SI Surendran Bailed by 7 Suraj Vasu 41/16 -

Indstrial Potential Survey 2017 Kozhikode District

Government of Kerala INDSTRIAL POTENTIAL SURVEY 2017 KOZHIKODE DISTRICT DEPARTMENT INDUSTRIES AND COMMERCE, KERALA Website: www.dic.kerala.gov.in, Email: [email protected] Industrial Potential Survey 2017 - Kozhikode Page 1 Industrial Potential Survey 2017 - Kozhikode Page 2 CHAPTER 1. INTRODUCTION HISTORY OF THE DISTRICT Kozhikode as a district came into existence on 1st January 1957. After the formation of Kerala state in 1956, when Malabar district was divided into three districts, the Central district with headquarters at Calicut (Kozhikode) was named as Kozhikode. The district, which initially had 5 taluks, had undergone several changes and the present district with 4 taluks was formed in 2013. The early history of the district is lost in obscurity. Neither inscription nor works of classical geographers and poets help us in reconstructing in full its early history. However, it is certain that during the Sangam Age the district formed part of the empire of the Cheras. During the Sangam age i.e. in the first two centuries of A.D the district was known as Poozhinad, which was later, annexed to Chera empire. The history of Kozhikode district for the next few centuries i.e. upto 8th century A.D is obscure. Kozhikode and its surroundings were part of Polanad ruled by Kolathiris. The ancestors of present Zamorin family defeated Kolathiri’s forces and established their headquarters at Kozhikode. Because of the persistent efforts and administrative abilities of the rulers who were later known as Zamorin, Kozhikode became an important commercial and trading centre during post Sangam age. During the pre Portuguese period the Zamorin achieved the suzerainty over a large track of land and many neighbouring Rajas accepted him as their protector. -

Accused Persons Arrested in Kozhikode City District from 19.04.2020To25.04.2020

Accused Persons arrested in Kozhikode City district from 19.04.2020to25.04.2020 Name of Name of the Name of the Place at Date & Arresting Court at Sl. Name of the Age & Cr. No & Sec Police father of Address of Accused which Time of Officer, which No. Accused Sex of Law Station Accused Arrested Arrest Rank & accused Designation produced 1 2 3 4 5 6 7 8 9 10 11 441/2020 U/s 4(2)(d) r/w 5 NOTICE KUNNAMA 19-04-2020 of Kerala SERVED - Ummer Ahammadul 27, Kuttimmal (H) NGALAM 1 Padanilam at 07:15 Epidemic Sreejith SI JFCM Farooq Kabeer Male Kuttikkattoor (Kozhikode Hrs Diseases Kunnamang City) Ordinance alam 2020 442/2020 U/s 4(2)(d) r/w 5 NOTICE POYITHAZHATH, KUNNAMA AHAMMED 19-04-2020 of Kerala SERVED - HAROON 45, KOTTAMPARAMB NGALAM 2 POYIL PADANILAM at 07:30 Epidemic SREEJITH,TS JFCM RASHEED Male A(PO),MUNDIKKA (Kozhikode THAZHATH Hrs Diseases Kunnamang L THAZHAM City) Ordinance alam 2020 249/2020 U/s 5 r/w 4(2)(d) CHEMMAN NOTICE Febina Manzil, 19-04-2020 of Kerala IP 50, Francis road GADU SERVED - 3 Shefeeque Marakkar Puthiyapalam, at 07:37 Epidemic Anithakumari Male Jn (Kozhikode JFCM - I Kozhikode Hrs Diseases C City) Kozhikode Ordinance 2020 250/2020 U/s 5 r/w 4(2)(d) CHEMMAN NOTICE Laksham veedu, 19-04-2020 of Kerala IP 50, Francis road GADU SERVED - 4 Ismail Babu Nallalam(po), at 07:42 Epidemic Anithakumari Male Jn (Kozhikode JFCM - I Kozhikode Hrs Diseases C City) Kozhikode Ordinance 2020 443/2020 U/s 4(2)(f) r/w 5 NOTICE MANNANATH(H), KUNNAMA 19-04-2020 of Kerala SERVED - 21, MUTTANCHERI, MUTTANCH NGALAM 5 FAVAS UMMAR at 08:00 Epidemic -

District Wise IT@School Master District School Code School Name Thiruvananthapuram 42006 Govt

District wise IT@School Master District School Code School Name Thiruvananthapuram 42006 Govt. Model HSS For Boys Attingal Thiruvananthapuram 42007 Govt V H S S Alamcode Thiruvananthapuram 42008 Govt H S S For Girls Attingal Thiruvananthapuram 42010 Navabharath E M H S S Attingal Thiruvananthapuram 42011 Govt. H S S Elampa Thiruvananthapuram 42012 Sr.Elizabeth Joel C S I E M H S S Attingal Thiruvananthapuram 42013 S C V B H S Chirayinkeezhu Thiruvananthapuram 42014 S S V G H S S Chirayinkeezhu Thiruvananthapuram 42015 P N M G H S S Koonthalloor Thiruvananthapuram 42021 Govt H S Avanavancheri Thiruvananthapuram 42023 Govt H S S Kavalayoor Thiruvananthapuram 42035 Govt V H S S Njekkad Thiruvananthapuram 42051 Govt H S S Venjaramood Thiruvananthapuram 42070 Janatha H S S Thempammood Thiruvananthapuram 42072 Govt. H S S Azhoor Thiruvananthapuram 42077 S S M E M H S Mudapuram Thiruvananthapuram 42078 Vidhyadhiraja E M H S S Attingal Thiruvananthapuram 42301 L M S L P S Attingal Thiruvananthapuram 42302 Govt. L P S Keezhattingal Thiruvananthapuram 42303 Govt. L P S Andoor Thiruvananthapuram 42304 Govt. L P S Attingal Thiruvananthapuram 42305 Govt. L P S Melattingal Thiruvananthapuram 42306 Govt. L P S Melkadakkavur Thiruvananthapuram 42307 Govt.L P S Elampa Thiruvananthapuram 42308 Govt. L P S Alamcode Thiruvananthapuram 42309 Govt. L P S Madathuvathukkal Thiruvananthapuram 42310 P T M L P S Kumpalathumpara Thiruvananthapuram 42311 Govt. L P S Njekkad Thiruvananthapuram 42312 Govt. L P S Mullaramcode Thiruvananthapuram 42313 Govt. L P S Ottoor Thiruvananthapuram 42314 R M L P S Mananakku Thiruvananthapuram 42315 A M L P S Perumkulam Thiruvananthapuram 42316 Govt. -

Accused Persons Arrested in Kozhikode City District from 08.04.2018 to 14.04.2018

Accused Persons arrested in Kozhikode City district from 08.04.2018 to 14.04.2018 Name of Name of the Name of the Place at Date & Arresting Court at Sl. Name of the Age & Cr. No & Sec Police father of Address of Accused which Time of Officer, which No. Accused Sex of Law Station Accused Arrested Arrest Rank & accused Designation produced 1 2 3 4 5 6 7 8 9 10 11 13-04- Abdu 49, Karuveetil-House, Feroke 155/2018 U/s Unni. K.P, SI BAILED BY 1 Koya 2018, FEROKE Rahiman Male PO- Feroke Chungam 15 of KG Act of Police POLICE 22:45 Palakkott House, 14-04- Abdul 39, 317/2018 U/s KUNNAMAN BAILED BY 2 Alikutty Peringolam Peringolam 2018, Rejeesh SI Basheer Male 118(a) of KP GALAM POLICE Kunnamangalam 00:30 Chalimadam-House, 13-04- 39, Feroke 155/2018 U/s Unni. K.P, SI BAILED BY 3 Abdul Gafoor Muhammed Pallikkal Paramba, 2018, FEROKE Male Chungam 15 of KG Act of Police POLICE Karippur. 22:45 Vallakkal-House, 10-04- 154/2018 U/s Remesh Abdul 40, Feroke BAILED BY 4 Muhammed Nellikkamparamba, 2018, 118(a) of KP FEROKE Kumar. A, SI Kareem Male Chungam 8/4 POLICE Kodiyathur, Mukkam 20:40 Act of Police Kasaba Valathil House, 13-04- 160/2018 U/s Sijith.V,Sub 31, Amsom, New KOZHIKOD BAILED BY 5 Abhilash Haridasan Arakkinar, Maradu, 2018, 118(a) of KP Inspector,Kas Male Bus E CUSBA POLICE Kozhikode city 17:15 Act aba PS Stand,Way In Odangattu, 09-04- 262/2018 U/s 38, KSRTC Bus NADAKKAV Sajiv,. -

Regional Transport Authority Kozhikode Meeting to Be Held on 20/11/2019 at Collectorate Conference Hall, Kozhikode at 10.30 Am

Regional Transport Authority Kozhikode Meeting to be held on 20/11/2019 at Collectorate Conference Hall, Kozhikode at 10.30 am PRESENT 1. SRI. S.SAMBASIVA RAO, IAS, DISTRICT COLLECTOR AND CHAIRMAN, REGIONAL TRANSPORT AUTHORITY, KOZHIKODE. 2. SRI. K.G.SIMON IPS, SUPERINTENDENT OF POLICE, KOZHIKODE (RURAL) AND MEMBER OF REGIONAL TRANSPORT AUTHORITY, KOZHIKODE. 3. SRI.T.C.VINESH, DEPUTY TRANSPORT COMMISSIONER AND MEMBER OF REGIONAL TRANSPORT AUTHORITY, KOZHIKODE ABSTRACT OF THE AGENDA FOR THE MEETING OF REGIONAL TRANSPORT AUTHORITY KOZHIKODE PROPOSED TO BE HELD ON 20/11/2019 AT 10.30 AM AT COLLECTORATE CONFERENCE HALL, CIVIL STATION KOZHIKODE. Fresh Permit Item1 No. G1/6160/2019/D Agenda:- To reconsider the request for grant of concurrence of the Regional Transport Authority, Malappuram to Regional Transport Kozhikode for a fresh regular permit to operate on the inter district route Panamplave-Areakode- Vettilappara(via) Panamplave Palam - Thottumukkam - Kuzhinakkippara - Vadakkumuri - Therattammal –Pathanapuram – Pallippadi – Kallarattikkal – Kinaradappan - Vettilappara - Vilakkuparamba - Edakkattuparamba - Cherupuzhapalam Kavungal Jn-touching Konoorkandi 2 single trips in the morning as OS from Mr.Ilyas.K,S/O Muhammed Kuzhikkara,Kuzhikkara House,Nayarkuzhi PO,REC,Kozhikode. Proposed Timings Panamplave Thottumukkam Areacode Vettilappara Konoorkandi A D A D A D A D A D 6.35 6.41 Vadakkumuri P 7.01 7.10 7.35 P 7.55 8.45 8.20 P 8.00 9.25 9.50 9.55 10.20 10.45 11.10 11.12 11.27 Edakkattu paramba 11.2 Edakkattuparam 11.47 ba 1.25 12.12 01.05 P 1.30 Edakkattuparam 1.45 ba 2.10 P P 2.35 P Edakkattu 2.50 paramba kavungal Jn 2.55 Edakkattuparamb 3.10 a kavungal Jn 4.25 4.05 4.50 Edakkattuparamba P 3.35 p Vadakkumuri kavungal Jn 4.58Panamplave 5.05 Vadakkumuri P 5.25 Bridge 5.55 Panamplave 5.35 6.02 Bridge Vadakkumuri 6.05 Edakkattuparamb 6.20 a kavungal Jn 6.45 p p Edakkattu 7.35 6.55 7.20 paramba kavungal Jn 7.45 Panamplave 7.52 Bridge 8.07 Halt 8.00 Item No.2 No. -

Kozhikode District 2012-13

List of NGC schools of Kozhikode District 2013-14 Sl.N Head of Name of the School o Institution 1 Headmaster A.S.V.U.P.School, Edakkara P.O, Chellannur (via) Kozhikode 673 616 2 Principal MES Raja Residential School, Kallanthode, NIT Campus PO, Kozhikode 673601 3 Principal Govt. Model H.S.School, Kozhikode- 673 001 4 Headmaster Avalakuttooth Govt. High School, Kottoth, Meppayoor, Kozhikode- 673524 5 Headmaster Azad Memorial U.P. School, P.O. Kumaranellur, Mukkam, Kozhikode-673 602 6 Principal Bharathiya Vidyabhavan School, Ponnyankodekunnu, Chevayur, Kozhikode 7 Principal Sri Guruji Vidhyalaya, Beach Road, Kozhikode 673 032 8 Headmaster Govt. U.P. School Padinjattumuri, P.O. Kizhakkumuri, Kozhikode - 673 611 9 Principal Calicut H.S.School for the Handicapped, Snehanagar, Kolathara, Kozhikode- 10 Headmaster Chennamangallur H.S.School, Chennamangallur P.O, Mukkam, Kozhikode- 11 Headmaster Naduvallur A.U.P.S, Kakkur P.O, Kozhikode-673619 12 Headmaster Chinmaya Vidhyalaya,Nellokode 673016 13 Headmistress NGO Quarters Govt. High School, Merikkunnu P.O, Kozhikode-673012 14 Headmistress Maniyoor U.P.School, P.O.Maniyoor Kozhikode-673523 15 Headmaster Achuthan Girls H.S, Chalappuram, Kozhikode-673002 16 Headmaster G.M.U.P School, Poonoor, Unnikulam P.O, Kozhikode-673 574 17 Headmaster Gov: H.S.S, Kokkallur, Kokkallur P.O, Balussery, Kozhikode-673 612 18 Headmaster G.H.S.S, Puduppady, P.O. Puduppady, Kozhikode -673586 19 Headmaster G.U.P.School, Trikuttissery, Vakayad P.O, Naduvannur (Via), Kozhikode-673614 20 Headmaster Govt: M.U.P.School, Nallalam, Kozhikode-673027 21 Principal G.V.H.S.School for Boys, Quilandy, Kozhikode-673 305 22 Principal G.V.H.S.School, Atholy (P.O), Kozhikode-673 315 23 Principal G.V.H.S School, Kuttichira, Kozhikode-673001 24 Principal G.V.H.S.School, Meenchantha, Kozhikode-673018 25 Principal G.V.H.S School, Meppayoor, Meppayoor P.O, Kozhikode-673524 26 Headmaster Kuttamboor H.S Punnassery P.O, Narikkuni (Via) Kozhikode-673585 27 Principal G.V.H.S School, Payyoli, P.O. -

4. KOZHIKODE DISTRICT Contents

4. KOZHIKODE DISTRICT Contents Executive Summary .......................................................................... 101 4.1 General Features ........................................................................ 105 4.2 Trend in Cattle Population .......................................................... 106 4.3 Trend in Milk Production from Bovines ....................................... 107 4.4 Milk Chilling Facilities in Kozhikode District ............................... 107 4.5 Milk Processing ........................................................................... 109 4.6 Milk Marketing ...........................................................................113 4.7 Milk Procurement .......................................................................120 4.8 Cattle Shed and Farm Machineries ............................................. 127 4.9 Cattle Induction .......................................................................... 129 4.10 Establishment of Laboratory in Kozhikode Dairy ....................... 130 4.11 Clean Milk Production .............................................................. 132 4.12 Technical Input Services (TIS) ................................................... 134 4.13 Information and Communication Technology Networking .......... 135 4.14 Manpower Development ............................................................ 136 4.15 Working Capital - Kozhikode District ......................................... 139 Kozhikode District Kozhikkode District 100 Executive Summary The Kozhikode -

Manappuram Finance Ltd IV/470A(Old) W638A(New) Manappuram House Valapad Post, Thrissur-680567 Ph: 0487- 3050417/415/3104500 List

Manappuram Finance Ltd IV/470A(Old) W638A(New) Manappuram House Valapad Post, Thrissur-680567 Ph: 0487- 3050417/415/3104500 FOLIO / DEMAT ID NAME ADDRESS LINE 1 ADDRESS LINE 2 List of Unpaid Dividend as on ADDRESS09.08.2016 LINE (Dividend 3 for the periods 2008-09 toADDRESS 2015-16) LINE 4 PINCOD DIV.AMOUNT DWNO MICR PERIOD IEPF. TR. DATE 000642 JNANAPRAKASH P.S. POZHEKKADAVIL HOUSE P.O.KARAYAVATTAM TRICHUR DIST. KERALA STATE 1800.00 16400038 54773 2015-16 4TH INTERIM DIVIDEND 26-APR-23 000671 SHEFABI K M C/O.SEENATH HUSSAIN CHINNAKKAL HOME PO. VALAPAD PAINOOR 1800.00 16400039 54774 2015-16 4TH INTERIM DIVIDEND 26-APR-23 000691 BHARGAVI V.R. C/O K.C.VISHWAMBARAN,P.B.NO.63 ADV.KAYCEE & KAYCEE AYYANTHOLE TRICHUR DISTRICT KERALA STATE 1800.00 16400040 54775 2015-16 4TH INTERIM DIVIDEND 26-APR-23 000902 SREENIVAS M.V. SAI SREE, KOORKKENCHERY TRICHUR - 7 KERALA STATE 1800.00 16400046 54781 2015-16 4TH INTERIM DIVIDEND 26-APR-23 001036 SANKAR T.C. DAYA MANDIRAM TRICHUR - 4. KERALA 9000.00 16400052 54787 2015-16 4TH INTERIM DIVIDEND 26-APR-23 002626 DAMODARAN NAMBOODIRI K T KANJIYIL THAMARAPPILLY MANA P O MANALOOR THRISSUR KERALA 3600.00 16400071 54806 2015-16 4TH INTERIM DIVIDEND 26-APR-23 002679 NARAYANAN P S PANAT HOUSE P O KARAYAVATTOM, VALAPAD THRISSUR KERALA 3600.00 16400074 54809 2015-16 4TH INTERIM DIVIDEND 26-APR-23 002769 RAMLATH V E ELLATHPARAMBIL HOUSE NATTIKA BEACH P O THRISSUR KERALA 1800.00 16400079 54814 2015-16 4TH INTERIM DIVIDEND 26-APR-23 002966 KUNHIRAMAN K KADAVATH HOUSE OZHINHA VALAPPU (PO) (DIST) KARASAGOD 000000 1800.00 -

Accused Persons Arrested in Kozhikodu City District from 28.06.2015 to 04.07.2015

Accused Persons arrested in Kozhikodu city district from 28.06.2015 to 04.07.2015 Name of Name of the Name of the Place at Date & Arresting Court at Sl. Name of the Age & Cr. No & Sec Police father of Address of Accused which Time of Officer, Rank which No. Accused Sex of Law Station Accused Arrested Arrest & accused Designation produced 1 2 3 4 5 6 7 8 9 10 11 CrNo. Souparnika, Ayyappan 56/15 17.00 hrs 518/15U/s SI Suresh Bailed by 1 Ramesan Cherukulam, Purakkattiri Elathur PS Pilla Male 28/06/2015 118(a) of KP Babu Police Choyibazar ACT CrNo.519/201 22/15 Edavanathazham, Kunduparamb 18.05 hrs 5 U/s 279 Jr Si Aswani. Bailed by 2 Vysakh Premanandan Elathur PS Male Makkada, Kakkodi a 28/05/2015 IPC 185 Of J.S Police MV Act CrNo.520/201 Akhil 24/15 Kozhipadannayil, 18.20 hrs 5 U/s 279 Jr Si Aswani. Bailed by 3 Prakasan Elathur Elathur PS Prakash Male Elathur 28/06/2015 IPC 185 Of J.S Police MV Act CrNo.522/201 Puthanayil, SI 56/15 19.30 hrs 5 U/s 279 Bailed by 4 Rajendran Sadanandan Rarichan road, Morikkara Elathur PS Jayachandra Male 29/06/2015 IPC 185 Of Police Eranhippalam Kumar MV Act CrNo.523/201 Kolathur Paramba, 19.40 hrs 40/15 5 U/s 279 SI Surendran Bailed by 5 Baiju Chathukutti Padinhattumuri, Morikkara 29/- Elathur PS Male IPC 185 Of T Police Kakkodi 06/2015 MV Act Vinod @ 32/15 Satheesh Nivas, 14.00 hrs Cr. -

Regional Transport Authority, Kozhikode, Meeting to Be Held on 23/6/2016 at Collectorate Conference Hall, Kozhikode at 10.30AM

Regional Transport Authority, Kozhikode, Meeting to be held on 23/6/2016 at Collectorate Conference Hall, Kozhikode at 10.30AM. PRESENT: 1. SRI.N.PRASANTH, IAS, DISTRICT COLLECTOR AND CHAIRMAN, REGIONAL TRANSPORT AUTHORITY, KOZHIKODE. 2. SRI. N. VIJAYAKUMAR, IPS, SUPERINTENDENT OF POLICE KOZHIKKODE (RURAL) AND MEMBER OF REGIONAL TRANSPORT AUTHORITY, KOZHIKODE. 3. SRI.B.J.ANTONY, DEPUTY TRANSPORT COMMISSIONER AND MEMBER OF REGIONAL TRANSPORT AUTHORITY, KOZHIKODE. Item No.1 No. G1/5920/2016/D Agenda:-To consider the request for grant of concurrence of the Regional Transport Authority, Wayanad to Regional Transport Kozhikode since a portion lying in this jurisdiction in respect of S/C KL 35 A 4649 so as to renew the regular permit for a further period of 5 years to operate on the route Perikkallur-Kozhikode-NBS via Pulpally-S.Battery-Meenangadi-Muttil- Vivekananda Hospital-Edapetty-Kainatty-Kalpetta-Puzhamudi-Kalpetta Govt.College-Chundale-Vythiri police stationJn-Pookottu Lake-Thalipuzha- Lakkidi-Adivaram-Thamarassery court Road-Koduvally-Kunnamangalam- Karanthur and Medical college- as LSOS valid up to 26.5.2016. Request from: Secretary, Regional Transport Authority, Wayanad vide reference No. C1/3698/2016 Item No.2 No. G1/5919/2016/D Agenda:-To consider the request for grant of concurrence of the Regional Transport Authority, Wayanad to Regional Transport Kozhikode since a portion lying in this jurisdiction in respect of S/C KL 12 E 8007 so as to renew the regular permit for a further period of 5 years to operate on the route Kolavally- Ambedkar colony-Kozhikode via Lakkidi-Adivaram-Thamarassery Chungam- Court Road-Koduvally-Kunnamangalam-Hotel Highway Jn-Mundikkal thazham and Medical college- as LSOS valid up to 19.6.2012.