Fintech and Digital Banking 2025 Asia Pacific

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The 50 Years

The 50 years. Foreword 5 Peter Seah, Piyush Gupta A bank is born 7 S Dhanabalan The courage of youth 12 S Dhanabalan Best of all leaders 18 J Y Pillay From negative to positive 22 Ang Kong Hua Of fishmongers and stallholders 26 Shirley Loo-Lim A first against all odds 32 N Ganesan Buses, planes and the stock exchange 36 Tan Soo Nan Daring to do 40 Hong Tuck Kun The condo project that almost wasn’t 44 S Dhanabalan, Ng Kee Choe Ruffling feathers 48 Ng Kee Choe, Elsie Foh City within a city 52 Lau Chan Sin Grand old dame gets a facelift 56 Loh Soo Eng A game-changing first 60 Elsie Foh Putting Singapore on the map 64 Eng-Kwok Seat Moey Turning crisis into opportunity 69 Jeanette Wong A dino-mite story 73 Digor (The last dinosaur alive) A Smart Buddy for a Smart Nation 79 P’ing Lim, Jeremy Soo The journey together continues 85 Chester Teo (A reel-life character) Beyond dollars and cents 89 Eric Ang 50 Enterprises of Change 94 50 Memorable Highlights 146 Once upon a time... 4 Foreword This year, DBS turns 50. With our coming of age, it’s inevitable that we’ve been a little introspective, remembering our roots and celebrating our rich heritage as the former Development Bank of Singapore. In many ways, the DBS story mirrors that of Singapore’s. After all, the bank was founded in 1968, just three years after the independence of Singapore – for the express purpose of financing the nation’s development and industrialisation. -

Annual Securities Report / Yukashoken Hokokusho (Excerpt)

Annual Securities Report “Yukashoken Hokokusho” (Excerpt) for the fiscal year ended March 31, 2020 MUFG Bank, Ltd. Table of Contents Page Cover ............................................................................................................................................................ 1 I. Overview of the Company .................................................................................................................. 2 1. Key Financial Data and Trends ....................................................................................................... 2 2. History ............................................................................................................................................. 5 3. Business Outline .............................................................................................................................. 6 4. Information on Subsidiaries and Affiliates ...................................................................................... 8 5. Employees ..................................................................................................................................... 10 II. Business Overview ............................................................................................................................ 11 1. Management Policy, Business Environment and Issues to be Addressed, etc. .............................. 11 2. Risks Related to Business ............................................................................................................. -

Banks and Corporates Realign Relationships in Asia 2018 Greenwich Leaders: Asian Large Corporate Banking and Cash Management

Banks and Corporates Realign Relationships in Asia 2018 Greenwich Leaders: Asian Large Corporate Banking and Cash Management Q1 2018 Although the names at the top of Asia’s corporate banking market are unchanged from 2017 to 2018, the industry as a whole is actually in the midst of an accelerated evolution, as large companies and a growing list of global, regional and domestic banks work to sort out who is—and who wants to be—relevant to whom. HSBC, Standard Chartered Bank and Citi have been the top three banks in Asia since Greenwich Associates started tracking the large corporate banking market over 15 years ago. In recent years, ANZ Bank and DBS Bank have consistently rounded out the top five, while a few European global franchises have stepped back to varying degrees in the landscape. Amid the stability at the top of the market, a longer term evolution has progressed among the majority of leading banks in Asia. An Increasing Focus on “Target Market” When Greenwich Associates started covering Asia’s corporate banking landscape in the early 2000s, almost all of our bank clients asked to see their results based on our “total sample” research universe—meaning the full sample of interviews conducted with hundreds of large companies from across the entire region. (This year, Greenwich Associates interviewed 708 companies across 11 markets, representing a known universe of some 2,200 companies with annual sales of more than U.S.$500 million.) This approach reflected their broad strategies, with ambitions to serve much of the Asian large corporate banking market. -

Dbs-Annual-Report-2018.Pdf

BANK OF THE YEAR – GLOBAL The Banker Best Bank in the World TO BE THE BEST BANK IN THE WORLD Global Finance The WORLD’S BEST DIGITAL BANK World’s Euromoney Best WORLD’S BEST BANK BEST BANK FOR SMEs Bank Euromoney SME BANK OF THE YEAR – GLOBAL (PLATINUM WINNER) Global SME Finance (International Finance FOR OUR Corporation) CASH MANAGEMENT GLOBAL BEST SERVICE – OVERALL: #1 Euromoney #1 BEHIND THE CUSTOMERS LOGIN EXPERIENCE MyPrivateBanking BEST PRIVATE BANK FOR INNOVATION PWM/ The Banker BEST PRIVATE BANK FOR ENTREPRENEURS – GLOBAL DBS Group Holdings Ltd Annual Report 2018 Global Finance Perhaps that’s why we were named 12 Marina Boulevard Best Bank in the World Marina Bay Financial Centre Tower 3 Singapore 018982 (65) 6878 8888 | www.dbs.com Co. Reg. No. 199901152M DBS GROUP HOLDINGS LTD facebook.com/dbs ANNUAL REPORT 2018 twitter.com/dbsbank #RecyclemoreWasteless DBS_AR18_Inside Spreads_001-041_Front.indd 1-3 7/3/19 8:03 PM About us DBS is a leading fi nancial services group in Asia with a presence in 18 markets. Headquartered and listed in Singapore, we have a growing presence in the three key Asian axes of growth: Greater China, Southeast Asia and South Asia. Our “AA-” and “Aa1” credit ratings are among the highest in the world. We have been recognised for our leadership globally, having been named “Bank of the Year – Global” by The Banker and “Best Bank in the World” by Global Finance. We are also at the forefront of leveraging technology to shape the future of banking and have been named “World’s Best Digital Bank” by Euromoney. -

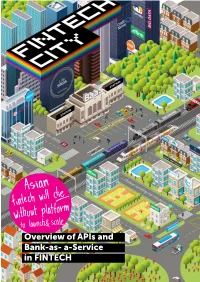

Overview of Apis and Bank-As- A-Service in FINTECH Baas for Banks As Amazone Web Services for E-Commerce

Overview of APIs and Bank-as- a-Service in FINTECH BaaS for banks as Amazone Web Services for e-commerce Traditional bank 2015 customers 67% product Amazon’s profit New fintech comes from AWS! players marketing support ? human resources To fight with - complience IT-guys to support - processing center and manage servers or to earn with - card issuing 2006 - money storage Creation of AWS for new players License Servers You may write off infrastructure investments or use them as new revenue streams While banks have always been looking to con- ratization.¹ Fintech-startups nowadays can serve trol the financial services industry, with the rise of almost any financial need for the eligible popu- fintech, the situation has changed drastically. One lation. Now banks are looking to collaborate with of the core differences in approach to financial fintech so as to not to lose the links in the value services between banks and fintech lies in democ- chains that make them so powerful. Chris Skinner one of the TOP5 fintech-influencers and predictors, author of bestsellers «DIGITAL BANK and «VALUE WEB», managing partner of the BB Fund in London You’re probably all familiar with SaaS – it’s basically paying for applications as you use them, rather than buying them. These services used to cost you a fortune, but are now free or near enough. That’s where banking is going. Banking becomes plug and play apps you stitch together to suit your business or lifestyle. There’s no logical reason why Banking shouldn’t be delivered as SaaS. This is the future bank, and old banks will need to reconsider their services to com- pete with this zero margin model. -

Digital Wealth Management in Asia Pacific

Digital Wealth Management in Asia Pacific A comparative analysis across eight key markets 2021 kpmg.com/cn Foreword Asia Pacific has been witnessing strong economic As a result, a growing number of financial institutions prosperity as a result of its open business have widened their target customer groups and environment, relaxed regulatory landscape and a increased focus on developing efficient digital well-developed infrastructure. This has led to a rise in capabilities to cater to mass markets. In relation to the population of High-Net-Worth Individuals mobile access to financial services, the race is on to (HNWIs), particularly the younger generation who provide customers with the best “bank-in-a-pocket” demand technologically advanced and highly service. This race has been joined not just by customised banking and wealth management traditional and neobanks, but also by megatech and solutions, designed specifically to cater to their telecommunications companies with ambitions to growing investment needs. widen their market presence throughout Asia Pacific. The region is home to ~15 million HNWIs, the This move toward digitalisation has further picked up second-largest concentration in the world after North pace post the COVID-19 pandemic. According to America, with an expected growth of 39 percent by KPMG’s 2020 CEO Outlook Survey, 81 percent of 2024, the highest growth forecast globally.1 About CEOs in the Financial Services (FS) sector feel that half of these people are located in mainland China COVID-19 has accelerated digitisation of operations alone. They are looking for highly-personalised and creation of next-generation operating models, advisory solutions from technologically sound while 76 percent feel that it has accelerated the advisors to help plan their family wealth and creation of new digital business models.2 succession. -

Vii) DETAILS of CERTIFICATE of DEPOSITS 69

PRIVATE & CONFIDENTIAL – FOR PRIVATE CIRCULATION ONLY THIS DISCLOSURE DOCUMENT IS NEITHER A PROSPECTUS NOR A STATEMENT IN LIEU OF PROSPECTUS. THIS DISCLOSURE DOCUMENT IS PREPARED IN CONFORMITY WITH SECURITIES AND EXCHANGE BOARD OF INDIA (ISSUE AND LISTING OF DEBT SECURITIES) REGULATIONS, 2008 ISSUED VIDE CIRCULAR NO. LAD-NRO/GN/2008/13/127878 DATED JUNE 06, 2008, AS AMENDED BY SECURITIES AND EXCHANGE BOARD OF INDIA (ISSUE AND LISTING OF DEBT SECURITIES) (AMENDMENT) REGULATIONS, 2012 ISSUED VIDE CIRCULAR NO. LAD-NRO/GN/2012- 13/19/5392 DATED OCTOBER 12, 2012, SECURITIES AND EXCHANGE BOARD OF INDIA’S CIRCULAR ON ISSUES PERTAINING TO PRIMARY ISSUANCE OF DEBT SECURITIES ISSUED VIDE CIR/IMD/DF/18/2013 DATED OCTOBER 29, 2013 READ WITH SEBI CIRCULAR NO CIR/IMD/DF- 1/122/2016 DATED NOVEMBER 11, 2016, THE SECURITIES AND EXCHANGE BOARD OF INDIA (ISSUE AND LISTING OF DEBT SECURITIES) (AMENDMENT) REGULATIONS, 2014 ISSUED VIDE CIRCULAR NO. LAD-NRO/GN/2013-14/43/207 DATED JANUARY 31, 2014, SECURITIES AND EXCHANGE BOARD OF INDIA (LISTING OBLIGATIONS AND DISCLOSURE REQUIREMENTS), REGULATIONS 2015 AND THE RBI CIRCULAR DBR.No.BP.BC.1/21.06.201/2015-16 DATED JULY 1, 2015 READ WITH RBI CIRCULAR DBR.No.BP.BC.71/21.06.201/2015-16 DATED JANUARY 14, 2016 AND RBI CIRCULAR DBR.BP.BC.NO.50/21.06.201/2016-17 DATED FEBRUARY 2, 2017, EACH AS AMENDED FROM TIME TO TIME. BANK OF BARODA (A Government of India Undertaking) Constituted under the Banking Companies (Acquisition and Transfer of Undertakings) Act, 1970 Head Office: Baroda House, Mandvi, Vadodara 390 006, Gujarat, India Tel No: +91-265-2363001, ; Fax No: +91-265-2362914 Corporate Office: Baroda Corporate Centre, C-26, G Block, Bandra-Kurla Complex, Bandra (E), Mumbai 400 051 Tel No: +91-22-66363600; Fax No: +91-22-67592840 E-mail: [email protected], Website: www.bankofbaroda.com DISCLOSURE DOCUMENT DISCLOSURE DOCUMENT FOR PRIVATE PLACEMENT OF UNSECURED, SUBORDINATED, PERPETUAL, ADDITIONAL TIER I, BASEL III COMPLIANT NON CONVERTIBLE TAXABLE BONDS OF (RS. -

Towards Understanding the Impact of Organizational Culture and Risk Management in Banking Sector in Developing Countries

DEGREE PROJECT, IN PROJECT MANAGEMENT AND OPERATIONAL DEVELOPMENT, SECOND LEVEL STOCKHOLM, SWEDEN 2014 Towards Understanding The Impact Of Organizational Culture And Risk Management In Banking Sector In Developing Countries Sitwat Zahra Mir KTH – Royal Institute of Technology Stockholm, School of Industrial Engineering and Management & Habib Metropolitan Bank Pakistan (Subsidiary of Habib Bank A.G. Zurich Switzerland) KTH – Royal Institute of Technology Stockholm, School of Industrial Engineering and Management & Habib Metropolitan 1 Bank Pakistan (Subsidiary of Habib Bank A.G. Zurich Switzerland) www.kth.se Sitwat Zahra Mir MS in Project Management and Operational Development School of Industrial Engineering and Management Royal Institute of Technology Stockholm & Habib Metropolitan Bank Pakistan (Subsidiary of Habib Bank A.G. Zurich) Habib Metropolitan Bank Lahore, Pakistan School of Industrial Engineering and Management Stockholm KTH Examiner: Anna Homström , Kristina Palm Supervisor at KTH: Erika Bellander Supervisor at Habib Metropolitan Bank: Syed Wajahat Hussain 3 4 Abstract Culture of an organization is one of the important factors in determining the success or failure of organizations and their long term performance. Aims of this study are to analyze the cultural features of major banks operating in developing countries especially in Pakistan and investigate risk management processes and models that allow banks in implementing risk based policies and practices. The risk management encompasses big area in banking and it has a controlling role in business. The components of the organizational culture were visualized based on Denison’s Model in Habib Metropolitan Bank (HMB) Pakistan. The current proposed research is of the descriptive type where research domain boundaries were classified as thematic, spatial and time domain. -

Current Bank List

CASH & BANKING LPL Financial Insured Cash Account (ICA): Current Priority Bank List Retail Accounts As of September 21, 2021 About the Priority Bank List (PBL) The Priority Bank List is a list of available banks into which your funds may be deposited, and is available from your financial advisor and on lplfinancial.lpl.com/disclosures. The banks appear in columns by state or region. In the column under your applicable state or region are multiple banks in the order in which your funds will be allocated. The last banks on the list are “Excess Banks” and are noted as such. For PBL banks not included in the Excess Banks category, LPL Financial (as your agent) will ensure that your ICA sweep deposits do not exceed the $250,000 (or $500,000 for joint accounts) FDIC-defined ownership category limits. For the Excess Banks, your funds may be deposited without consideration of the $250,000 and $500,000 limits. However, this will only be done when there is insufficient capacity in other banks on the PBL to take your assets and not break through the $250,000 and $500,000 limits—and is meant to be temporary in nature. You may not change the order of the banks on the PBL. However, you may, at any time, designate a bank as ineligible to receive your funds. This will result in your funds not being deposited into this bank—or if already there, we will remove your funds from that bank and designate the bank as ineligible to receive future deposits. Unless you direct us to place your funds in a different investment, your funds from eliminated banks will be deposited at the first available bank set forth on the Priority Bank List, as amended by you. -

A Case Study on Punjab National Bank Scam

Journal of Xi' an Shiyou University, Natural Science Edition ISSN : 1673-064X A Case Study on Punjab National Bank Scam (Is it only a scam or failure of the combined banking system?) Dr. Meda Srinivasa Rao Dr. B. Kishore Babu Professor, KL Business School, Professor, KL Business School Koneru Lakshmaiah Education Koneru Lakshmaiah Education Foundation, Foundation Vaddeswaram, Vaddeswaram, Andhra Pradesh-522502 Andhra Pradesh-522502 Abstract: The “biggest bank loot scam in 70 years” in independent India happened in one of the largest Public Sector Bank that had trembled entire banking sector. Punjab National Bank (PNB) India’s second largest public sector bank released a disaster on Valentine's Day i.e. 14th February 2018 by revealing a scam of Rs.11,400 crore directed by one of the country's richest businessman of the diamond, Nirav Modi. He ranked 85th on Forbes’s 2017 list of India’s richest people. Nirav Modi had directed and executed the scam with the support of Deputy Manager of PNB Mumbai branch named Gokul Nath Shetty and clerk Manoj Kharat. Modi and his Uncle Mehul Choksi schemed with these two people. They had facilitated the issuance of unauthorized LOU (Letter of Undertaking) to Modi and his company without following an appropriate procedure. The post scam had impacted shares of PNB by evaporating the market capitalization value worth of Rs.8000 crore due to that the entire banking sector was under shocking waves. Whistleblower had transcribed to the Prime Minister’s Office (PMO) at 2016, notifying the government for the “biggest bank loot scam in 70 years” but no prompt action was taken by the government. -

17Th October, 2017 Press Release OCBC Bank Is the Strongest Bank in Singapore and Ranks the 8Th Among the Strongest Bank in Asia

EMBARGOED The information in this letter is STRICTLY embargoed from any form of media coverage TAB International Pte Ltd until 17th October 2017 10, Hoe Chiang Road, #14-06 Keppel Tower, Singapore 089315 Tel: (65) 6236 6520 Fax: (65) 6236 6530 www.theasianbanker.com 17th October, 2017 Press Release OCBC Bank is the strongest bank in Singapore and ranks the 8th among the Strongest Bank in Asia Pacific in 2017, despite substantial pressure on banks in the region to maintain profitability - OCBC Bank is the strongest bank in Singapore and ranks 8th Strongest Bank in Asia Pacific in 2017 - Despite the strength of their balance sheets, Asia Pacific banks continue to face massive challenges in growing profits, a conundrum created by modern capital rules - Overall asset quality of Asia Pacific banks deteriorated marginally in 2016, adding pressures to profitability Toronto, Canada, 17th October 2017 - In general, the Asia Pacific banking sector delivered better results in this year’s the Asian Banker 500 (AB500) Strongest Banks by Balance Sheet evaluation, which is the most comprehensive annual evaluation that captures the quality and sustainability of the balance sheets of the banks in the region. Bank of China (Hong Kong) continues to top the Strongest Banks by Balance Sheet ranking in Asia Pacific in 2017, based on a very detailed and transparent scorecard that ranks commercial banks on six areas of balance sheet financial performance; namely the ability to scale, balance sheet growth, risk profile, profitability, asset quality and liquidity. The bank, along with other strongest banks in the region, was recognised at the AB500 Strongest Banks by Balance Sheet ceremony held in conjunction with the annual SWIFT organised SIBOS convention in Toronto, Canada. -

Cash Management Solutions

CASH & BANKING LPL Financial Insured Cash Account (ICA): Current Priority Bank List Retail Accounts Effective March 30, 2020 ABOUT THE PRIORITY BANK LIST (PBL) The Priority Bank List is a list of available Banks into which your funds may be deposited and is available from your financial advisor and on lplfinancial.lpl.com/disclosures. The Banks appear in columns by state or region. In the column under your applicable state or region are multiple Banks in the order in which your funds will be allocated. The last banks on the list are “Excess Banks” and are noted as such. For all other banks on the PBL except these Excess Banks, LPL Financial as your agent will ensure that your ICA sweep deposits do not exceed the $250,000 (or $500,000 for joint accounts) FDIC-defined ownership category limits. For the Excess Banks, your funds may be deposited without consideration of the $250,000 and $500,000 limits. However, this will only be done when there is insufficient capacity in other Banks on the PBL to take your assets and not break through the $250,000 and $500,000 limits and is meant to be temporary in nature. You may not change the order of the Banks on the PBL. However, you may, at any time, designate a Bank as ineligible to receive your funds. This will result in your funds not being deposited into this bank or if already there, we will remove your funds from that Bank and designate the Bank as ineligible to receive future deposits. Unless you direct us to place your funds in a different investment, your funds from eliminated Banks will be deposited at the first available Bank set forth on the Priority Bank List, as amended by you.