Management of Legal Risk by Financial Institutions

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Risk-Based Capital Rules

Financial Institution Letter FIL-69-2008 Federal Deposit Insurance Corporation July 29, 2008 550 17th Street NW, Washington, D.C. 20429-9990 RISK-BASED CAPITAL RULES Notice of Proposed Rulemaking on Risk-Based Capital Standards: Standardized Framework Summary: The federal bank and thrift regulatory agencies have jointly issued the attached Notice of Proposed Rulemaking (NPR) and are seeking comment on the domestic application of the Basel II standardized framework for all domestic banks, bank holding companies, and savings associations that are not subject to the Basel II advanced approaches rule. The FDIC will accept comments on the NPR through October 27, 2008. Distribution: FDIC-Supervised Banks (Commercial and Savings) Highlights: Suggested Routing: Chief Executive Officer In the attached NPR, the agencies propose to Chief Financial Officer implement a new optional framework for calculating Chief Accounting Officer risk-based capital based on the Basel II Standardized Related Topics: Approach to credit risk and the Basel II Basic Risk-Based Capital Rules Indicator Approach to operational risk. The proposal 12 CFR Part 325 would: Basel II Attachment: • Expand the use of credit ratings for • “Key Aspects of the Proposed Rule on Risk- determining risk weights, Based Capital Guidelines: Capital Adequacy Guidelines; Standardized Framework” • Base risk weights for residential mortgages • Notice of Proposed Rulemaking, Risk-Based on loan-to-value ratios, Capital Guidelines; Capital Adequacy Guidelines; Standardized Framework • Expand the types of financial collateral and guarantees available to banks to offset credit Contact: risk, Nancy Hunt, Senior Policy Analyst, at [email protected] or (202) 898-6643 • Offer more risk-sensitive approaches for Ryan D. -

Legal Risk Section 2070.1

Legal Risk Section 2070.1 An institution’s trading and capital-markets will prove unenforceable. Many trading activi- activities can lead to significant legal risks. ties, such as securities trading, commonly take Failure to correctly document transactions can place without a signed agreement, as each indi- result in legal disputes with counterparties over vidual transaction generally settles within a very the terms of the agreement. Even if adequately short time after the trade. The trade confirma- documented, agreements may prove to be unen- tions generally provide sufficient documentation forceable if the counterparty does not have the for these transactions, which settle in accor- authority to enter into the transaction or if the dance with market conventions. Other trading terms of the agreement are not in accordance activities involving longer-term, more complex with applicable law. Alternatively, the agree- transactions may necessitate more comprehen- ment may be challenged on the grounds that the sive and detailed documentation. Such documen- transaction is not suitable for the counterparty, tation ensures that the institution and its coun- given its level of financial sophistication, finan- terparty agree on the terms applicable to the cial condition, or investment objectives, or on transaction. In addition, documentation satisfies the grounds that the risks of the transaction were other legal requirements, such as the ‘‘statutes of not accurately and completely disclosed to the frauds’’ that may apply in many jurisdictions. investor. Statutes of frauds generally require signed, writ- As part of sound risk management, institu- ten agreements for certain classes of contracts, tions should take steps to guard themselves such as agreements with a duration of more than against legal risk. -

Legal Risk: the Operational Risk Problem in Microcosm

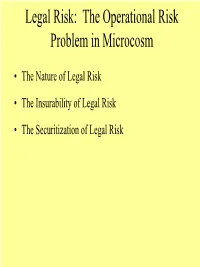

Legal Risk: The Operational Risk Problem in Microcosm • The Nature of Legal Risk • The Insurability of Legal Risk • The Securitization of Legal Risk The Nature of Legal Risk • Difficult to define: losses that depend on how the law allocates risk between financial institutions and other transactors or the government • Difficult to predict but determines whether bank actually bears the losses of an operational failure • Wide ranges of frequency and impact for different kinds of legal risk A Sampling of Court Cases • Sample of decided cases in federal district courts and three state appellate courts, October 1, 2000 - October 1, 2001 • Not a reliable sample: only includes litigated cases that were not settled, and only deals with a short period of time • Purpose: show the variety of different cases in federal court and the difference in legal environment among states Federal District Court Cases October 1, 2000 - October 1, 2001 Type of Case Number Banks as Trustee 4 Antitrust 2 Checks 9 Consumer Protection 54 --Truth in Lending 21 --Fair Debt Collection 9 Contracts 31 Discrimination 24 --Customer 6 --Employees 18 Fraud 15 Holocaust Compensation 1 Indian Land Claims 2 Mortgage or Foreclosure Dispute 8 Patent Infringement 2 RICO 10 Securities Fraud 17 --Fraud 8 --Disclosure 9 Third Party 32 --Deposit Holder or Trustee 18 --Finance Provider or Debt Holder 4 --Mortgage or Lien Holder 10 Torts 4 Trademark 2 Other 7 TOTAL 224 State Court Appellate Cases October 1, 2000 - October 1, 2001 Type of Case California New York Texas Banks as Trustee -

The Dodd-Frank Wall Street Reform and Consumer Protection Act July 2010 the DODD-FRANK WALL STREET REFORM and CONSUMER PROTECTION ACT

Understanding the New Financial Reform Legislation: The Dodd-Frank Wall Street Reform and Consumer Protection Act July 2010 THE DODD-FRANK WALL STREET REFORM AND CONSUMER PROTECTION ACT For more information about the matters raised in this Legal Update, please contact your regular Mayer Brown contact or one of the following: Scott A. Anenberg Charles M. Horn +1 202 263 3303 +1 202 263 3219 [email protected] [email protected] Michael R. Butowsky Jerome J. Roche +1 212 506 2512 +1 202 263 3773 [email protected] [email protected] Joshua Cohn David R. Sahr +1 212 506 2539 +1 212 506 2540 [email protected] [email protected] Thomas J. Delaney Jeffrey P. Taft +1 202 263 3216 +1 202 263 3293 [email protected] [email protected] Table of Contents Index of Acronyms / Abbreviations .................................................................................................xv The Dodd-Frank Wall Street Reform and Consumer Protection Act ................................................ 1 A. Summary ................................................................................................................... 1 B. A Very Brief History of the Legislation ...................................................................... 1 C. Overview of the Legislation ...................................................................................... 2 1. Framework for Financial Stability ................................................................. 2 2. Orderly Liquidation Regimen ....................................................................... -

Information About General Risks Associated with Trading in Foreign Currency and Derivatives

Information about general risks associated with trading in foreign currency and derivatives Applicable as from 1 January 2018 Introduction Before trading Derivatives can be used for investment and for hedging financial risks, but whether a derivative is the right financial This information sheet is provided to clients who enter into Trading in derivatives may entail significant risks. The risks instrument for you depends on several factors, including the derivatives and foreign currency transactions. The purpose is depend on the type of transaction and the nature of the investment/hedging purpose and your investment profile. to give you a clear understanding of the risks associated with underlier. Different instruments involve different levels of exposure to these types of products. risk, and in deciding whether to trade an instrument, you According to the Executive Order on Risk Assessment of should be aware of the following risks: Derivatives are financial instruments that derive their value Investment Products issued by the Danish Financial from underlying assets or other factors. The underlying Supervisory Authority, foreign currencies and derivatives are Market risk assets/factors (‘underliers’) may be market assets/factors labelled “red”. “Red” means that the investor risks losing more such as interest rates, foreign exchange rates, equities, than the amount invested or that the product type is difficult to Market risk is the risk of loss arising from adverse changes commodities, or other financial or economic interest or understand. in the value of a derivative instrument due to changes in the property of any kind. underliers. Similarly, adverse changes in the volatility of or The Danish Financial Supervisory Authority’s risk correlation or relationship between these factors may For the purpose of this information sheet, derivatives are assessment of investment products can be viewed at contribute to losses occurring. -

Regulatory Capital Requirements for European Banks

Regulatory Capital Requirements for European Banks Implications of Changing Markets and a New Regulatory Environment July 2009 Table of Contents Chapter 1 – Basics Key Concepts 8 Introduction 10 Basel I Capital Charges 11 Basel II Overview 12 Scope of Application 12 Types of Banks 13 Implementation and Timing 14 IRB Transition Period 15 Basel II – Three Pillars 16 Components of Regulatory Capital 17 Types of Eligible Capital and Provisions 18 Criteria for Recognition of External Ratings 19 Chapter 2 – Capital charges (Pillar 1) Sample Bank 21 Sovereign Exposures 22 Bank Exposures 25 2 Table of Contents (cont’d) Chapter 2 – Capital charges (cont’d) Corporate Exposures 28 Retail Exposures 36 Real Estate Exposures 39 Covered Bonds 43 Specialised Lending 45 Equity 46 Funds 48 Off-Balance Sheet Items 54 Securitisation Exposures 56 Operational Requirements 57 Proposed CRD Amendment – “Significant Credit Risk Transfer” 59 Standardised Banks 61 Ratings Based Approach 61 Most Senior Exposures; second loss positions or better 61 Liquidity Facilities 62 Overlapping Exposures 64 3 Table of Contents (cont’d) Chapter 2 – Capital charges (cont’d) Securitisation Exposures (cont’d) IRB Banks 65 Ratings Based Approach 65 Hierarchy 65 Internal Assessments Approach 67 Supervisory Formula Approach 70 Liquidity Facilities 74 Top-Down Approach 75 Rules for Purchased Corporate Receivables 76 Inferred Ratings 79 BIS Re-securitisation Proposals 80 CRD Retention Rules 83 BIS Other Securitisation Proposals 88 Credit Risk -

The Strategic and Legal Risks of Work-Integrated Learning: an Enterprise Risk Management Perspective

The strategic and legal risks of work-integrated learning: An enterprise risk management perspective CRAIG CAMERON1 Griffith University, Gold Coast, Australia Work-integrated learning (WIL) is a risky business for universities. WIL is a strategic risk worthy of pursuing by universities in the prevailing higher education environment, which is characterized by competition, changes in funding arrangements and stakeholder demand for WIL. Nevertheless the strategic opportunities that WIL presents cannot be achieved without the university taking on unavoidable and distinct legal risks that may have serious financial and reputational consequences for the university. This article examines WIL through a lens of enterprise risk management. The author describes how WIL is a strategic risk for universities, and identifies the possible legal risks of WIL through a review of empirical studies and case law in Australia. It is argued that risk management involves a balance between the university goals of maximizing the strategic value and minimizing the legal risks in relation to WIL. (Asia-Pacific Journal of Cooperative Education, 2017, 18(3), 243-256) Keywords: Work-integrated learning, legal risk, strategic risk, risk management, enterprise risk management This article examines work-integrated learning (WIL) through a lens of enterprise risk management (ERM), a comprehensive process of managing risks across the university that may affect the achievement of university objectives related to its core activities in learning and teaching, research, and service (Abraham, Baird, & Neugebauer, 2013; Ackley et al., 2007; Association of Governing Boards of Universities and Colleges & United Educators, 2014; Kaplin & Lee, 2013; Mattie, 2007). ERM evolved from the private sector, a consequence of lessons learned from the high risk financing strategies responsible for several business failures during the Wall Street crash of the late 1980’s (Clyde-Smith, 2014). -

Legal Risk Management Issues

SOUTHERN RISK MANAGEMENT EDUCATION CENTER DIVISION OF AGRICULTURE 2013 Risk Education Publication Series* R E S E A R C H & E X T E N S I O N University of Arkansas System JesseLegal J. Richardson, Risk Jr. Management Issues An accident can be classified as “tort” when there Introduction is a person or entity legally responsible for the This publication seeks to build upon the Legal Risk accident. For example, if a customer at a farmers’ White Paper authored by Harrison Pittman in the market falls and is injured, a tort may have fall of 2010. Basic legal risks have not changed occurred. If the owner of the farmers’ market was drastically since that earlier white paper. Landowner careless and allowed dangerous conditions to exist, liability, contracts and leases and business organiza the owner may be held liable for the accident. tions remain essential concerns for most producers. However, other legal risk issues have emerged as Landowners, producers and marketers may be liable vital to producers in the South. for injuries to employees, customers, trespassers or third parties. Property damage may also be recov Agricultural risks have been classified as production ered. Although all producers and marketers face risk, marketing risk, financial risk, legal risk and potential tort liability, the risk increases when cus human resources risk (USDA RMA, 1997). Legal tomers are allowed on the property (for example, issues overlap and intersect with the other risk upick or agritourism) and with direct marketing areas. The five main areas of legal risk in agriculture operations. Tort liability, including landowner involve tort liability, contractual arrangements, liability for injuries to persons on the property business structures, tax and estate planning and (whether invited or not), remains the most funda statutory compliance. -

Supervisory Guidance for Managing Settlement Risk in Foreign Exchange Transactions

Foreign exchange settlement risk Supervisory Guidance for Managing Settlement Risk in Foreign Exchange Transactions I Introduction 1. Foreign exchange (FX) settlement risk is the risk of loss when a bank in a foreign exchange transaction pays the currency it sold but does not receive the currency it bought. FX settlement failures can arise from counterparty default, operational problems, market liquidity constraints and other factors. Settlement risk exists for any traded product but the size of the foreign exchange market makes FX transactions the greatest source of settlement risk for many market participants, involving daily exposures of tens of billions of dollars for the largest banks. Most significantly, for banks of any size, the amount at risk to even a single counterparty could in some cases exceed their capital. 2. FX settlement risk is a form of counterparty risk involving both credit risk and liquidity risk. As with other forms of risk, banks need to ensure that they have a clear understanding of how FX settlement risk arises. On the basis of this understanding, policies for managing the risk should be developed at the highest levels within the bank and implemented through a formal and independent process with adequate senior management oversight. As part of this process, a bank has to have measurement systems that provide appropriate and realistic estimates of FX settlement exposures on a timely basis. The development of counterparty settlement limits and the monitoring of the exposures against these limits is a critical control function. The bank also needs to have procedures for reacting in a prompt and balanced manner to failed transactions or other settlement problems. -

The Definition of Legal Risk and Its Management by Central Banks

International In-house Counsel Journal Vol. 1, No. 1, June 2007, 43–49 The definition of legal risk and its management by central banks KATJA JULIE WU¨ RTZ Principal Legal Counsel at the European Central Bank, Frankfurt, Germany1 Currently, there are no international rules specific to central banks on what is to be understood by ‘legal risk’ and how it should be managed. In the context of the discussion on Basel II (the International Convergence of Capital Measurement and Capital Standards), it was considered that assessing, monitoring and mitigating legal risk may positively affect the way in which financial institutions conduct business. Basel II was transposed into Community legislation by means of the Recast Banking Directive2 and the Recast Capital Adequacy Directive3 which do not define the concept of legal risk but instead include it under the wider definition of operational risk. The concept of legal risk as applied by central banks may have some common ground with the concept as applied to credit institutions. However, when managing legal risk, the fundamental differences between central banks and credit institutions in terms of functions, risk profile, etc. and the roles of central banks as public entities and the risk of reputational loss related to their tasks need to be taken into account. Nonetheless, some elements of managing legal risk may be common to both central banks and credit institutions, depending on the special characteristics of the institution in question. Introduction In the aftermath of the corporate scandals of recent years, increased focus has been given to the importance of financial institutions’ legal risk management as part of their overall risk management. -

Chapter 16 Doing the Numbers, Page 475: Arrow Bar's Balance Sheet

Chapter 16 Doing the Numbers, page 475: Arrow Bar’s Balance Sheet [By the Editors] Please see the module titled “Solving for X and Other Friends from High School.” ___________________________________________________________________________ Room to Argue, page 478: Is Limited Liability Good or Bad? Reading One This reading summarizes the moral hazard problem in limited liability and discusses the evidence of excess risk taking. A CONTROL-BASED APPROACH TO SHAREHOLDER LIABILITY FOR CORPORATE TORTS Nina A. Mendelson 102 Colum. L. Rev. 1203 Copyright © 2002, Directors of the Columbia Law Review Association, Inc.; Nina A. Mendelson … III. Excessive Risk Taking Under Limited Liability Limited liability's moral hazard is the incentive created for corporations to engage in excessively risky activity, shifting the costs of this activity to tort and environmental victims. Much commentary has recognized the problem as a general matter. The following Sections outline the basic problem and provide some additional comments on evidence collected to date. These Sections also discuss the phenomenon of the corporation with a controlling shareholder. The corporate temptation to choose excessively risky activity will be especially pronounced when corporate equity is in the hands of a parent corporation or controlling shareholder. A. The Basic Moral Hazard Problem At least with respect to risky activities for which tort victims might seek to obtain legal recourse, limited liability presents an opportunity to avoid paying the appropriately-sized tort judgment. A corporation may be created or operated in a way that renders it "judgment- proof" - having only nominal assets available to pay a tort judgment. Or, a corporation simply may have inadequate assets available to fully cover its responsibility. -

Legal Risk Exposure in Islamic Finance Andrew WHITE Singapore Management University, [email protected]

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Institutional Knowledge at Singapore Management University Singapore Management University Institutional Knowledge at Singapore Management University Research Collection School Of Law School of Law 1-2013 Legal risk exposure in Islamic finance Andrew WHITE Singapore Management University, [email protected] Chen Mee KING Follow this and additional works at: https://ink.library.smu.edu.sg/sol_research Part of the Commercial Law Commons, and the Religion Law Commons Citation WHITE, Andrew and KING, Chen Mee. Legal risk exposure in Islamic finance. (2013). Islamic finance the new regulatory challenge. 225-235. Research Collection School Of Law. Available at: https://ink.library.smu.edu.sg/sol_research/2822 This Book Chapter is brought to you for free and open access by the School of Law at Institutional Knowledge at Singapore Management University. It has been accepted for inclusion in Research Collection School Of Law by an authorized administrator of Institutional Knowledge at Singapore Management University. For more information, please email [email protected]. Published in Islamic finance the new regulatory challenge. Wiley, 2013, Pages 225-235 https://doi.org/10.1002/9781118628973 CHAPTER 10 Legal Risk Exposure in Islamic Finance Andrew White and Chen Mee King1 1. INTRODUCTION In the post-crisis environment of the past few years (since 2007–2008), risk avoidance and the management of risk have both become an increasingly prominent feature of the finance landscape. Financial institutions and reg- ulators are today much more sensitive to the various potential areas of risk and, especially, risk contagion.