Technical College System of Georgia Review Report for Fiscal Year Ended June 30, 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Explore the Resources! Collection

Library Media Center Fall Semester 2014 Anthony O. Parker, Ph.D. Library Media Center Published Every Semester Volume 5 Issue 4 Explore the Resources! The Anthony O. would like to use From the Faculty, staff and Parker, Ph. D. students have access library services after Dean’s Desk Library Media Center to materials and hours may access the promotes learning professional library online services and supports the assistance at all via the Internet or visit mission of Albany times the facility is one of the neighboring Technical College. open. Students who libraries that have cooperative agreements with us. Featured Resources ! Credo Reference is an online collection of more than 600 highly- “We take pride in regarded full-text serving you. We reference titles. It hope this news- covers every major letter is informa- subject from over 80 tive and sparks your interest. publishers and links Please come by the library to reg- patrons to other related resources available through the library. ister. Registering GALILEO is the doorway to a wealth of information. Through provides pa- trons with a wide GALILEO patrons can access over 150 databases indexing thousands range of ser- of periodicals and scholarly journals. Over 7,000 journal titles are vices.” provided in full text. Other resources included are an encyclopedia, business directories, a collection of over 10,000 full-text books and government publications. Collection Development Please get your requests in for library resources. Faculty, staff, and students are encouraged to participate in the development of the library collection. Instructors, please do not include your cur- rent textbooks. -

Georgia WIOA Eligible Provider List Workforce Development Division 706‐369‐5703

Northeast Georgia WIOA Eligible Provider List Workforce Development Division 706‐369‐5703 The State Eligible Provider List (EPL) is currently under modification by the Governor’s Office of Workforce Development. During this time, our local area will use a list of contract schools, and whose programs align with our local “demand occupation list”, to create our Local EPL. We will use our Local EPL during this transitional time. Once the State’s EPL is complete, we will continue to work with programs that are on the State’s EPL, AND on our demand occupation list. (This list is effective as of April 2018) *** Please be aware this list is subject to change. Depending on the demand in our area, we may not be able to cover the program/ school of choice under the WIOA program. Contact the WIOA office to confirm. ***Please be aware we do not assist with core and/ or provisional classes (for any program under the Medical Field only) at a 2 or 4 year college. ***Please be aware there are deadlines associated with each school. It is the responsibility of each student to inquire with the desired school of these deadlines and each student must have All required documents faxed into the Workforce Development (WIOA) office by our set date. ***Please be aware that some Vendors may have a waiting list. ***Ashona Medical Institute‐ 1315 Milstead Rd. Conyers, GA 30012 770‐922‐6913/ Fax 770‐922‐6916 Programs of Study‐ Certified Nurse Assistant/ Patient Care Technician Certified Nurse Assistant 1 | Page Athens Technical College 800 U.S. -

Websites of Georgia Community Colleges Links Verified February 19, 2006

Websites of Georgia Community Colleges Links verified February 19, 2006 Albany Technical College http://www.albanytech.org/main.cfm?action=pages&PageID=94 Campus Locations: Dougherty County Campus Early County Campus Altamaha Technical Institute http://www.altamaha.tec.ga.us/Resources/Library.htm Campus Locations: Baxley Campus Hazelhurst Campus Ludowici Campus Andrew College http://www.andrewcollege.edu/pittsinfo.html Athens Technical College http://www.athenstech.edu/AcademicAffairs/LibraryServices/ Campus Locations: Athens Campus Elberton Campus Augusta Technical College http://www.augustatech.edu/library/ITCMaindefault.htm Campus Locations: Thomson Campus Waynesboro Campus Bauder College Central Georgia Technical College http://www.centralgatech.edu/library/index.htm Campus Locations: Macon Campus http://www.centralgatech.edu/library/Location-Macon%20Campus.htm Milledgeville Campus http://www.centralgatech.edu/library/Location-Milledgeville%20Campus.htm Jones County Center Putnam County Center Crawford County Center Monroe County Center Twiggs County Center Chattahoochee Technical College http://www.chattcollege.com/Default.aspx?tabid=78 Campus Locations: Marietta Campus Mt. View Campus Paulding Campus South Cobb Campus Columbus Technical College http://www.columbustech.edu/library.cfm Coosa Valley Technical College http://www.cvtcollege.org/library/index.html Campus Locations: Floyd County Campus Gordon County Campus Polk County Campus Darton College http://www.darton.edu/~dclib/index.php DeKalb Technical College http://www.dekalbtech.edu/Library/library.html -

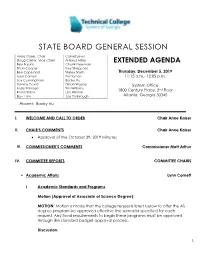

State Board General Session

STATE BOARD GENERAL SESSION Anne Kaiser, Chair Carvel Lewis Doug Carter, Vice Chair Artesius Miller EXTENDED AGENDA Ben Bryant Chunk Newman Shan Cooper Trey Sheppard Ben Copeland Shirley Smith Thursday, December 5, 2019 Lynn Cornett Phil Sutton 11:15 a.m.- 12:05 p.m. Jay Cunningham Baoky Vu Tommy David Dinah Wayne System Office Mary Flanders Tim Williams 1800 Century Place, 2nd Floor Randall Fox Lisa Winton Buzz Law Joe Yarbrough Atlanta, Georgia 30345 Absent: Baoky Vu I. WELCOME AND CALL TO ORDER Chair Anne Kaiser II. CHAIR'S COMMENTS Chair Anne Kaiser Approval of the October 29, 2019 Minutes III. COMMISSIONER’S COMMENTS Commissioner Matt Arthur IV. COMMITTEE REPORTS COMMITTEE CHAIRS Academic Affairs Lynn Cornett I. Academic Standards and Programs Motion (Approval of Associate of Science Degree): MOTION: Motion is made that the college requests listed below to offer the AS degree program be approved effective the semester specified for each request. Any fiscal requirements to begin these programs must be approved through the standard budget approval process. Discussion: 1 Coastal Pines Technical College - Degree program in A. S. - General Studies, AB73, 60 Credit Hours, effective January 2020. Coastal Pines Technical College's (CPTC) student body currently consists of 60% dual enrollment students. CPTC currently is limited in its ability to provide services to students who wish to complete a general associate of science degree prior to high school graduation. The addition of this degree would enable dual enrollment students to complete the associate degree either while in high school or transition to CPTC to complete the degree following their high school graduation. -

Georgia Colleges and Universities Offering ECE Programs of Study That Qualify for SCHOLARSHIPS PUBLIC Colleges & Universities

Georgia Colleges and Universities Offering ECE Programs of Study that Qualify for SCHOLARSHIPS PUBLIC Colleges & Universities 1. Albany State University, Albany 11. Georgia Southern University, Statesboro www.asurams.edu / 229-430-4600 www.georgiasouthern.edu / 912-478-4636 2. Armstrong Atlantic State University, Savannah 12. Georgia Southwestern State University, www.armstrong.edu / 912-344-2503 Americus www.gsw.edu / 229-931-2710 3. Bainbridge College, Bainbridge 13. Georgia State University, Atlanta www.bainbridge.edu / 229-248-2500 www.gsu.edu / 404- 413-2063 4. College of Coastal Georgia, Brunswick 14. Gordon College, Barnesville www.ccga.edu / 912-279-5700 www.gdn.edu / 678-359-5555 5. Columbus State University, Columbus 15. Kennesaw State University, Kennesaw www.columbusstate.edu / 706-507-8800 www.ksu.edu / 770-423-6000 6. Dalton State University, Dalton 16. Middle Georgia State College, Macon (a) www.daltonstate.edu / 706-272-4436 www.mga.edu / 478-471-2700 7. Fort Valley State University, Fort Valley 17. University of Georgia, Athens www.fvsu.edu / 478-825-6211 www.uga.edu / 706-542-3000 8. Georgia College & State University, Milledgeville 18. University of North Georgia, Dahlonega (a, b) www.gcsu.edu / 478-471-2063 www.ung.edu / 706-864-1400 9. Georgia Gwinnett College, Lawrenceville 19. University of West Georgia, Carrollton www.ggc.edu / 678-407-5000 www.westga.edu / 678-839-5000 10. Georgia Regents University, Augusta 20. Valdosta State University, Valdosta www.gru.edu / 706-737-1632 www.valdosta.edu / 229-333-5800 Note: (Satellite campus locations in parentheses) PRIVATE Colleges and Universities 1. Berry College, Rome 11. -

Technical College System of Georgia Technical Certificate of Credit (TCC

Technical College System of Georgia Technical Certificate of Credit (TCC) Programs, Diploma, and AAS Degrees CDA Preparation CDA Specialist Developmemet Child Basics Childcare/Education Early Exceptionalities Childhood Early Program Administration Childhood Early Care Specialis Child Family Care Specialist Infant/Toddler Child Youth and Age School DIPLOMA AAS Albany Technical College www.albanytech.edu X1 X1 X1 X1 X1 X1 X1 229.430.3500 Altamaha Technical College www.altamahatech.edu X1 X1 X1 912.427.5800 Athens Technical College X X X www.athenstech.edu X1 X1 X1 706.355.5000 X2 Atlanta Technical College www.atlantatech.edu X1 X1 X1 X1 X1 404.225.4400 Augusta Technical College www.augustatech.edu X X X 706.771.4088 Bainbridge College Technical Studies www.bainbridgecollege.edu X1 X1 X X1 X1 706.649.1800 Central Georgia Technical College X X1 X X www.centralgatech.edu X1 X X2 X2 X1 X1 478.757.3400 X2 Chattahoochee Technical College www.chattahoocheetech.edu X1 X2 X1 X2 X1 X1 X1 770.528.4545 Columbus Technical College www.columbustech.edu X X X X 706.649.1762 X1 X1 X1 X1 706.649.1636 Georgia Piedmont Technical College X X X X X www.gptc.edu X1 X1 X1 X1 X1 X1 X1 404.297.9522 Georgia Northwestern Technical College www.gntc.edu X1 X1 X1 X1 X2 X1 X2 X2 X1 X1 706.624.1124 Gwinnett Technical College X X X X X X www.gwinnetttech.edu X1 X1 X1 X1 X1 X1 770.962.7580 Lanier Technical College X X1 X X1 X X www.laniertech.edu X1 X X2 X1 X2 X1 X1 770.531.6365 X2 Middle Georgia Technical College www.middlegatech.edu X1 X2 X2 X2 X2 X2 478.988.6800 Moultrie -

Georgia Higher Learning and Earnings

Georgia Higher Learning and Earnings David Evans II January 2017 Executive Summary By 2025, over 60 percent of jobs in Georgia likely will require some form of a college education, whether a certificate, associate’s degree, or bachelor’s degree.1 Expected earnings are an important factor in making the decision to pursue a certain degree or major, but these data have not previously been publicly available. With this in mind, the Georgia Higher Learning and Earnings Report presents earnings information for Georgia technical college and college/university graduates who work in Georgia after earning their degrees.2 It presents median, 25th percentile, and 75th percentile wages by degree category (certificate, bachelor’s, etc.), technical college or college/university, program of study, and whether the student graduated with the HOPE scholarship/grant for the first and fifth year after graduation. In addition, it explores award patterns by gender and race/ethnicity.3 In addition to degree type and program of study, it is important to note that many factors, such as student ability/motivation, college selectivity, and job market conditions affect earnings, so the results in this report should not be interpreted as a guarantee of employment or earnings. The report is limited to wage data on graduates who work in Georgia for employers that provide wage data to the Georgia Department of Labor, so it does not include wages earned in out-of-state jobs, as an independent contractor, or as a federal or military employee. With this in mind, the results should be seen as one piece of information that students and parents can use when making program and degree choices. -

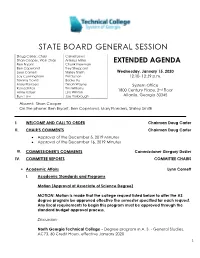

State Board General Session

STATE BOARD GENERAL SESSION Doug Carter, Chair Carvel Lewis Shan Cooper, Vice Chair Artesius Miller EXTENDED AGENDA Ben Bryant Chunk Newman Ben Copeland Trey Sheppard Lynn Cornett Shirley Smith Wednesday, January 15, 2020 Jay Cunningham Phil Sutton 12:10- 12:39 p.m. Tommy David Baoky Vu Mary Flanders Dinah Wayne System Office Randall Fox Tim Williams 1800 Century Place, 2nd Floor Anne Kaiser Lisa Winton Buzz Law Joe Yarbrough Atlanta, Georgia 30345 Absent: Shan Cooper On the phone: Ben Bryant, Ben Copeland, Mary Flanders, Shirley Smith I. WELCOME AND CALL TO ORDER Chairman Doug Carter II. CHAIR'S COMMENTS Chairman Doug Carter Approval of the December 5, 2019 Minutes Approval of the December 16, 2019 Minutes III. COMMISSIONER’S COMMENTS Commissioner Gregory Dozier IV. COMMITTEE REPORTS COMMITTEE CHAIRS Academic Affairs Lynn Cornett I. Academic Standards and Programs Motion (Approval of Associate of Science Degree) MOTION: Motion is made that the college request listed below to offer the AS degree program be approved effective the semester specified for each request. Any fiscal requirements to begin this program must be approved through the standard budget approval process. Discussion: North Georgia Technical College - Degree program in A. S. - General Studies, AC73, 60 Credit Hours, effective January 2020. 1 The General Studies Associate of Science (AS) degree prepares students to pursue a four-year degree or for careers in multiple fields of studies. Graduates develop academic and professional knowledge and skills necessary to succeed in the profession of their choice or to further their education at a four-year institution. This program provides students the option to combine general education along with occupational courses to create a specialized degree suited to their individual career goals. -

Explore the Resources! Collection

Library Media Center Spring Semester 2015 Anthony O. Parker, Ph.D. Library Media Center Published Every Semester Volume 6 Issue 2 Explore the Resources! The Anthony O. would like to use From the Faculty, staff and Parker, Ph. D. students have access library services after Dean’s Desk Library Media Center to materials and hours may access the promotes learning professional library online services and supports the assistance at all via the Internet or visit mission of Albany times the facility is one of the neighboring Technical College. open. Students who libraries that have cooperative agreements with us. Featured Resources ! Credo Reference is an online collection of more than 600 highly- “We take pride in regarded full-text serving you. We reference titles. It hope this news- covers every major letter is informa- subject from over 80 tive and sparks your interest. publishers and links Please come by the library to reg- patrons to other related resources available through the library. ister. Registering GALILEO is the doorway to a wealth of information. Through provides pa- trons with a wide GALILEO patrons can access over 150 databases indexing thousands range of ser- of periodicals and scholarly journals. Over 7,000 journal titles are vices.” provided in full text. Other resources included are an encyclopedia, business directories, a collection of over 10,000 full-text books and government publications. Collection Development Please get your requests in for library resources. Faculty, staff, and students are encouraged to participate in the development of the library collection. Instructors, please do not include your cur- rent textbooks. -

TCSG Post COVID GED Testing.Xlsx

Post COVID-19 Open PV GED Testing Sites Testing Center Location/Campus Albany Technical College Main Campus Athens Technical College Clarke Athens Technical College Hart Athens Technical College Washington/Wilkes Athens Technical College Walton Atlanta Technical College Main Campus Atlanta Technical College South Campus Augusta Technical College Richmond Clayton County Board of Education Jonesboro Central Georgia Technical College Macon Central Georgia Technical College Milledgeville Central Georgia Technical College Warner Robins Chattahoochee Technical College Appalachian Chattahoochee Technical College Dallas Chattahoochee Technical College North Metro Chattahoochee Technical College Canton Coastal Pines Technical College Main Campus Coastal Pines Technical College Golden Isle Coastal Pines Technical College Jesup Cobb County School District Paulding County Campus Columbus Technical College Main Campus GA Northwestern Technical College Floyd GA Northwestern Technical College Walker GA Northwestern Technical College Whitfield/Murray GA Northwestern Technical College Gordon Georgia Piedmont Technical College Main Campus Gwinnett Technical College Lawrenceville Gwinnett Technical College Milton Lanier Technical College Barrow Lanier Technical College Banks Lanier Technical College Cummings Lanier Technical College Dawson North GA Technical College Clarkesville North GA Technical College Blairsville Oconee Fall Line Technical College Main Campus Oconee Fall Line Technical College Sandersville Ogeechee Technical College Main Campus Online -

Photo ID for Voting Las Identificaciones Con Foto Para Votar

Photo ID for Voting Las Identificaciones con foto para votar Georgia Colleges and Universities Universidades de Georgia Abraham Baldwin Agricultural College Georgia Perimeter College Albany State University Georgia Southern University Armstrong Atlantic State University Georgia Southwestern State University Atlanta Metropolitan College Georgia State University Augusta State University Gordon College Bainbridge College Kennesaw State University Clayton State University Medical College of Georgia Coastal Georgia Community College Middle Georgia State University Columbus State University University of North Georgia Dalton State College Savannah State University Darton College Skidaway Institute of Oceanography East Georgia College Southern Polytechnic State University Fort Valley State University South Georgia College Georgia College & State University University of Georgia Georgia Gwinnett College University of West Georgia Georgia Highlands College Valdosta State University Georgia Institute of Technology Waycross College Georgia Technical Colleges Universidades Técnicas de Georgia Albany Technical College Middle GA Technical College Altamaha Technical College Moultrie Technical College Athens Technical College North GA Technical College Atlanta Technical College Ogeechee Technical College Augusta Technical College Okefenokee Technical College Central GA Technical College Sandersville Technical College Chattahoochee Technical College Savannah Technical College Columbus Technical College South GA Technical College DeKalb Technical College Southern Crescent Technical College Georgia NorthwesternTechnical College Southeastern Technical College Gwinnett Technical College Southwest GA Technical College Heart of GA Technical College West GA Technical College Lanier Technical College Wiregrass Georgia Technical College Form# GAC&U_ID-E&S-17 . -

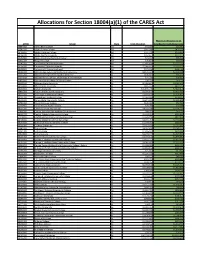

Allocations for Section 18004(A)(1) of the CARES Act

Allocations for Section 18004(a)(1) of the CARES Act Maximum Allocation to be OPEID School State Total Allocation Awarded for Institutional Costs 00884300 Alaska Bible College AK $42,068 $21,034 02541000 Alaska Career College AK $941,040 $470,520 04138600 Alaska Christian College AK $201,678 $100,839 00106100 Alaska Pacific University AK $254,627 $127,313 03160300 Alaska Vocational Technical Center AK $71,437 $35,718 03461300 Ilisagvik College AK $36,806 $18,403 01146200 University Of Alaska Anchorage AK $5,445,184 $2,722,592 00106300 University Of Alaska Fairbanks AK $2,066,651 $1,033,325 00106500 University Of Alaska Southeast AK $372,939 $186,469 00100200 Alabama Agricultural & Mechanical University AL $9,121,201 $4,560,600 04226700 Alabama College Of Osteopathic Medicine AL $186,805 $93,402 04255500 Alabama School Of Nail Technology & Cosmetology AL $77,735 $38,867 03032500 Alabama State College Of Barber Styling AL $28,259 $14,129 00100500 Alabama State University AL $6,284,463 $3,142,231 00100800 Athens State University AL $845,033 $422,516 00100900 Auburn University AL $15,645,745 $7,822,872 00831000 Auburn University Montgomery AL $5,075,473 $2,537,736 00573300 Bevill State Community College AL $2,642,839 $1,321,419 00101200 Birmingham-Southern College AL $1,069,855 $534,927 00103000 Bishop State Community College AL $2,871,392 $1,435,696 03783300 Blue Cliff Career College AL $105,082 $52,541 04267900 Brown Beauty Barber School AL $70,098 $35,049 00101300 Calhoun Community College AL $4,392,248 $2,196,124 04066300 Cardiac And