Audit Report on the Accounts of Federal Government - (Civil)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Nepali Times Investigation ○○○○○○○○○○○○○○○

# 8 6 - 12 September 2000 20 pages Rs 20 2 DOLPO At home with Monica19 EXCLUSIVE Nordic jaunt Why is Sweden so disinterested in UNACCOUNTED Nepal? Swedish aid to Nepal has dropped dramatically in the past few The good news is that male MPs years, and it is the Nordic country don’t file maternity claims. The bad with the lowest contribution to Nepal’s development. Is it a failure news is that ministers are not paying of our economic diplomacy, or have FOR their phone bills. the Swedes given up on Nepal? A NEPALI TIMES INVESTIGATION ○○○○○○○○○○○○○○○ Foreign Minister Chakra Prasad ○○○○○ irregularities were also pointed out in Bastola is planning to get it straight If you are a taxpayer, some of the money the past, and still remain as wrongs from the horse’s the government is taking from you is because the executive has not taken mouth when he paying for the following expenses: basic steps to regularise the spending. swings through • Rs 1,158,000 in phone and electric- Past efforts by the parliament’s Stockholm this ity bills for ministers over a six- public spending watchdog to get back week. Bastola month period. some of the misused money have failed then goes on to • Eight phone lines registered in the to achieve much. Last week, the Public Norway, which names of dead lawmakers yet to be Accounts Committee (PAC) summoned unlike Sweden, returned to the Parliament Secretariat. officials and gave them another deadline remains fully • Padded expenses amounting to to make amends. “We’ll go to the engaged in thousands of dollars by ministers extent the law allows to get the accounts Nepal. -

Notice Dated 10.12.2013

JAMMU AND KASHMIR PUBLIC SERVICE COMMISSION Reshim Garh, Colony, Bakshi Nagar, Jammu (http://www.jkpsc.nic.in ) Notice Dated 10.12.2013 In continuation to this Office Notification No. PSC/Exam/13/100 dated: 03/12/2013, it is hereby notified that the interview of following shortlisted candidates for the posts of Medical Officer in Health and Medical Education Department advertised vide Notification No. 16-PSC (DR-P) of 2013 dated 17.08.2013 shall be conducted on the dates indicated against each at J&K Public Service Commission Office Resham Garh Colony, Bakshi Nagar, Jammu at 09:30 A.M Sharp. SNO ROLLNO NAME OF THE CANDIDATE PARENTAGE DATE OF INTERVIEW 1 3302068 MALAVIKA JANDIAL VINOD KUMAR GUPTA 23-Dec-13 2 3300119 DANISH ZAHOOR ZAHOOR AHMAD PANDIT 23-Dec-13 3 3300075 SYED AIJAZ NASIR SYED NASIR AHMAD 23-Dec-13 4 3302079 VIPUL KUMAR GUPTA VINOD GUPTA 23-Dec-13 5 3300167 SYED QUIBTIYA KHURSHEED SYED KHURSHEED AHMAD SHAH 23-Dec-13 6 3302092 QURAT UL AIN ARIFA AB MAJID SHIEKH 23-Dec-13 7 3302097 SONY KUMAR WARYAM SINGH 23-Dec-13 8 3300196 MOHD DAWOOD BACHH YAQOOB JAN BACHH 23-Dec-13 9 3302117 DEEPIKA SHARMA VINOD KUMAR SHARMA 23-Dec-13 10 3300312 SYED FAHEEM MAQBOOL SYED MAQBOOL AHMED 23-Dec-13 11 3302168 BHARAT BHUSHAN BASSAN YOG RAJ 23-Dec-13 12 3302210 ATISH GUPTA YASH PAUL GUPTA 23-Dec-13 13 3300414 MOHAMMAD NASEED YAR MOHAMMAD SHEIKH 23-Dec-13 14 3302234 REENA VERMA VISHWA KUMAR VERMA 23-Dec-13 15 3300482 SYED ZAHID HUSSAIN SYED MUZAFARXHUSSAIN 23-Dec-13 16 3300515 SYED KARAR HUSSAIN SYED MUZAFAR SHAH 23-Dec-13 17 3302286 SWATI ARORA -

Jammu and Kashmir Public Service Commission Jammu and Kashmir Public Service Commission

JAMMU AND KASHMIR PUBLIC SERVICE COMMISSION Resham Ghar Colony, Bakshi Nagar, Jammu (www.jkpsc.nic.in ) Subject: Select list for the posts of Medical Officers in Health & Medical Education Department. Notification No. 01 -PSC (DR-S) of 2014 Dated: 25.02.2014 Whereas, vide this Office Notification No. 16-PSC(DR-P) of 2013 dated 17.08.2013, 769 posts of Medical Officers in Health & Medical Education Department were notified; and Whereas, the interview of shortlisted candidates was conducted from 23.12.2013 to 12.02.2014 at J&K Public Service Commission Office, Resham Garh Colony, Jammu; and Now, therefore, on the basis of performance in the interview coupled with the weight-age in respect of academic merit, experience and other related parameters in accordance with relevant rules the General Merit of Candidates who had appeared in the interview is enclosed as “Annexure-A” to this Notice. Consequent upon the above, the Select List of the candidates in order of merit is given in “Annexure-B” to this Notice. Note :- The Commission reserves the right to have certificate/documents of any candidate verified, if it is at any stage found expedient to do so. The Select List is Provisional. This is subject to the outcome of Writ Petitions pending before any Competent Court of Law. Sd/- (Dr. T.S.Ashok Kumar),IFS Secretary & COE J&K Public Service Commission Copy to:- 1. Secretary to Government, Health & Medical Education Department. 2. Director, Information Department, J&K Government, for publication of this Notification in two leading local dailies of Srinagar/Jammu. -

Collective Directory 061011 Final

www.pildat.org Bridging the Gap between Parliament and Civil Society Directory Parliamentary Committees and relevant Civil Society/Research Organisations of Pakistan www.pildat.org Bridging the Gap between Parliament and Civil Society Directory Parliamentary Committees and relevant Civil Society/Research Organisations of Pakistan PILDAT is an independent, non-partisan and not-for-profit indigenous research and training institution with the mission to strengthen democracy and democratic institutions in Pakistan. PILDAT is a registered non-profit entity under the Societies Registration Act XXI of 1860, Pakistan. Copyright© Pakistan Institute of Legislative Development And Transparency PILDAT All Rights Reserved Printed in Pakistan Published: September 2011 ISBN: 978-969-558-222-0 Any part of this publication can be used or cited with a clear reference to PILDAT This Directory has been compiled and published by PILDAT under the project titled Electoral and Parliamentary Process and Civil Society in Pakistan, in partnership with the East-West Centre, Hawaii and supported by the United Nations Democracy Fund. Published by Pakistan Institute of Legislative Development and Transparency - PILDAT Head Office: No. 7, 9th Avenue, F-8/1, Islamabad, Pakistan Lahore Office: 45-A, Sector XX, 2nd Floor, Phase III Commercial Area, DHA, Lahore Tel: (+92-51) 111-123-345; Fax: (+92-51) 226-3078 E-mail: [email protected]; Web: www.pildat.org Directory of Parliamentary Committees and Relevant Civil Society/Research Organisations of Pakistan Bridging the Gap between the Parliament and the Civil Society CONTENTS Preface 07 Abbreviations and Acronyms 09 Part - I: Synchronisation Matrix - Synchronisation Matrix of the Parliamentary Committees with Relevant Civil Society/Research Organisations Part - II: Special Committees 1. -

S.No. Roll No Name of Candidate Parentage Grand Total Result 1 Mi/14100

GRAND S.NO. ROLL NO NAME OF CANDIDATE PARENTAGE RESULT TOTAL 1 M-I/14100 RAMAN SINGH THAKUR RAJINDER SINGH 154 PASS 2 M-I/14101 SHABAZ AHMED WAZIR ALI 139 PASS 3 M-I/14102 MEENAKSHI DEVI TARA CHAND 144 PASS 4 M-I/14103 RANDHEER SINGH PRITHVEE SINGH 151 PASS 5 M-I/14104 JAHANGIR NABI GH NABI 126 PASS 6 M-I/14105 YASEEN SAKINDAR SAKINDAR KHAN 132 PASS 7 M-I/14106 MOHD ULFAT MOHD RAFIQ 141 PASS 8 M-I/14107 BANNU SHARMA RAMESH KUMAR 155 PASS 9 M-I/14108 SUNIL SINGH OM NATH 125 PASS 10 M-I/14109 YASEEN IQBAL ABDUL RASHID 155 PASS 11 M-I/14110 AKHTER ALI CHOWDHARY ABDUL KHALIQ 126 PASS 12 M-I/14111 CHAMAN LAL RATTAN CHAND 172 PASS 13 M-I/14112 MUZAFAR AHMED MIR ABDUL AZIZ MIR 172 PASS 14 M-I/14113 RAJAT SHARMA BALBIR KUMAR 132 PASS 15 M-I/14114 VIPUL KHAJURIA MANOHAR LAL KHAJURIA 151 PASS 16 M-I/14115 YASMEEN RAZIA BARKET HUSSAIN 134 PASS 17 M-I/14116 ANKUSH KUMAR ATMA RAM 162 PASS 18 M-I/14117 GULZAR MOHD AMAM DIN 133 PASS 19 M-I/14118 MOHIT SINGH PARDEEP SINGH 159 PASS 20 M-I/14119 SUBHAM ANGRAL DEV RAJ 170 PASS 21 M-I/14120 KULVIR SINGH ROMESH SINGH 157 PASS 22 M-I/14121 SUSHIL KUMAR RAJ KUMAR SHARMA 164 PASS 23 M-I/14122 NASEEB SINGH BISHAN SINGH 168 PASS 24 M-I/14123 JAGAT NARAYAN SWARAN SINGH 170 PASS 25 M-I/14124 PANKAJ DUTTA DESH BHUSHAN 166 PASS 26 M-I/14125 SAHIL SHARMA DEV RAJ 169 PASS 27 M-I/14126 MOHD ASIF ABDUL RASHID 142 PASS 28 M-I/14127 KAILASH KUMAR SHAMBOO NATH 129 PASS 29 M-I/14128 CHETAN SHARMA NAND KISHOR SHARMA 126 FAIL 30 M-I/14129 ANUJ SHARMA KEWAL KRISHAN 171 PASS 31 M-I/14130 PURSHOTAM CHAND KRISHAN LAL 136 PASS 32 -

Primo.Qxd (Page 1)

WEDNESDAY, FEBRUARY 26, 2014 (PAGE 14) DAILY EXCELSIOR, JAMMU 111101824 SAJAD HUSSAIN SHAH 22 March 2014 -- do -- 3300897 TANZEELA NAZIR RBA 50.99 3301395 GURPREET KOUR OM 52.74 3301928 MANZOOR AHMAD OM 45.99 3302377 ABID AKBAR SOFI OM 58.39 (From page 13) 3300898 PARVAIZ AHMED THOKER RBA 48.62 3301396 NADEEM SHOKET OM 59.34 3301932 RASHAD RAFIQ MATTOO OM 50.51 3302378 JYOTI KUMARI SC 44.78 Shortlisted of candidates who qualified the written test and called for JAMMU AND KASHMIR PUBLIC SERVICE COMMISSION 112109996 MUSTUFA ALI LONE 15 March 2014 -- do -- 3300900 NASEER AHMAD TAK OM 58.91 3301397 MANJOTE KOUR SAHNI OM 53.13 3301936 ZAHOOR AHMED OM 66.75 3302379 SHAZIA QAYUM OM 57.06 interview for the post of VLW, ( Rural Dev. Department) Advertisement 3300901 SHAZIA ASHRAF SLC 51.93 3301398 AEJAZ AHMAD BHAT OM 48.94 3301937 NUZHAT SADIQ RBA 55.59 3302380 ANIL KUMAR PARIHAR RBA 51.50 112109997 MUTAHIR AHSAN UNTOO 15 March 2014 -- do -- Notification No 04 of 2013 dated23-02-2013, under Item No 378, District Resham Ghar Colony, Bakshi Nagar, Jammu 3300902 SHUBANA ASHRAF SLC 52.34 3301399 HAAMID ISMAIL OM 51.69 3301939 BURHAN WANI OM 60.88 3302381 HUMA CHAUDHARY ST 49.84 112109999 MUZAFAR AHMAD LONE 15 March 2014 -- do -- Cadre Kulgam. 3300904 AIJAZ AHMAD BHAT RBA 55.80 3301405 ISHTIYAQ RASOOL RATHER RBA 50.63 3301941 ABID HUSSAIN BHAT OM 53.24 3302382 BHARAT BHUSHAN SC 46.48 112110038 MYSAR AHMAD PEER 15 March 2014 -- do -- 111096845 AABID HUSSAIN RATHER 22 March 2014 at Dak Bangalow 3300906 AFROOZAH AKHTER RBA 52.96 3301406 SAJAD KHALIQ WANI OM 54.59 3301942 MOHMAD IQBAL RATHER OM 48.67 3302383 ROHIT KATOCH RBA ABSENT 112110058 NADIM MAJEED 15 March 2014 -- do -- (www.jkpsc.nic.in) Kulgam 3300907 BASHARAT HUSSAIN PANDIT OM 48.92 3301408 GULSHAN AKHTER OM 51.38 3301943 ZUHAIB AHMED WANI OM 55.13 3302384 TAPASYA PANDITA OM 54.59 112110064 NAFEEZ NABI BHAT 15 March 2014 -- do -- 111096846 AABID HUSSAIN RATHER 22 March 2014 -- do -- Subject: Select list for the posts of Medical Officers in Health & Medical Education Department. -

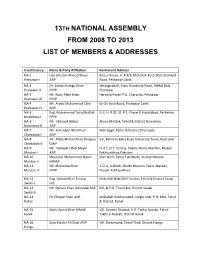

13Th National Assembly from 2008 to 2013 List of Members & Addresses

13TH NATIONAL ASSEMBLY FROM 2008 TO 2013 LIST OF MEMBERS & ADDRESSES Constituency Name & Party Affiliation Permanent Address NA-1 Haji Ghulam Ahmad Bilour Bilour House, H. # 3/2, Mohallah Raza Shah Shaheed Peshawar-I ANP Road, Peshawar Cantt. NA-2 Dr. Arbab Alamgir Khan Jehangirabad, Main University Road, Tehkal Bala, Peshawar-II PPPP Peshawar NA-3 Mr. Noor Alam Khan Haryana Payan P.O. Charpriza, Peshawar Peshawar-III PPPP NA-4 Mr. Arbab Muhammad Zahir 65-Sir Syed Road, Peshawar Cantt. Peshawar-IV ANP NA-5 Eng. Muhammad Tariq Khattak G-2, H. # 92, St. # 7, Phase-II, Hayatabad, Peshawar Nowshera-I PPPP NA-6 Mr. Masood Abbas Akora-Khattak, Tehsil & District Nowshera Nowshera-II ANP NA-7 Mr. Asfandyar Wali Khan Wali Bagh, Tehsil & District Charsadda Charsadda-I ANP NA-8 Mr. Aftab Ahmad Khan Sherpao 5-F, Rehman Baba Road University Town, Peshawar Charsadda-II QWP NA-9 Mr. Himayat Ullah Mayar H. # 1, D.C. Colony, Shamsi Road, Mardan, Khyber Mardan-I ANP Pakhtunkhwa,Pakistan NA-10 Moulana Mohammad Qasim Sher Garh, Tehsil Takhtbahi, District Mardan Mardan-II MMAP NA-11 Mr. Khanzada Khan 172-A, A-Block, Sheikh Matoon Town, Mardan, Mardan-III PPPP Khyber Pakhtunkhwa NA-12 Eng. Usman Khan Tarakai Mohallah Babi Khel Tarakai, Tehsil & District Swabi Swabi-I Ind NA-13 Mr. Pervaiz Khan Advocate ANP Vill. & P.O. Thand Koi, District Swabi Swabi-II NA-14 Pir Dilawar Shah ANP Mohallah Gulshanabad, Jungle Khel, P.O. KDA, Tehsil Kohat & District, Kohat NA-15 Mufti Ajmal Khan MMAP Vill. Ganderi Khattak, P.O. -

PPSC Assistant Superintendent Jail 2015 Solved Past Papers PUNJAB

Download Past Papers of PPSC, FPSC, NTS from www.allresult.pk PPSC Assistant Superintendent Jail 2015 Solved Past Papers PUNJAB PUBLIC SERVICE COMMISSION ASSISTANT SUPERINTENDENT JAIL (BS-16) IN THE PUNJAB PRISON (HOME) DEPARTMENT, 2015 1. Baltoro is a famous ____ of Pakistan. (A) Glacier ✓ (B) River (C) Mountain Lake (D) Mountain Peak 2. Gayari, the site of a catastrophic avalanche in 2012, lies in (A) Siachen ✓ (B) Balochistan (C) Azad Kashmir (D) Salt Range 3. Diamer-Bhasha hydro-electric project is being built on river. (A) Jhelum (B) Kabul (C) Indus ✓ (D) Hunza 4. The main city of Hunza Valley is (A) Karmabad ✓ (B) Gust (C) Battagram (D) Bisham 5. The first ever American President to be assassinated was (A) John Adams ✓ (B) Abraham Lincoln (C) William Coleridge (D) John F. Kennedy 6. Peoples Republic of China was founded in (A) 1950 (B) 1949 ✓ (C) 1948 (D) 1951 7. Which mineral is mostly found in northern and western mountains of Pakistan? (A) Chromite Download Past Papers of PPSC, FPSC, NTS from www.allresult.pk (B) China Clay (C) Limestone (D) Gypsum 8. Barrak Hussain Obama is the President of U.S.A. (A) 42nd (B) 43rd (C) 44th ✓ (D) 40th 9. President Mamnoon Hussain is the President of Pakistan. (A) 12th ✓ (B) 14th (C) 11th (D) 15th 10 All of the following are non-metallic minerals except: (A) Asbestos (B) Graphite (C) Platinum ✓ (D) Sulphur 11. The British Cabinet Mission visited India in (A) 1945 (B) 1946 ✓ (C) 1944 (D) 1947 12 Who founded the Indian National Congress? (A) A.O. -

General Elections-2008 Report

GENERAL ELECTIONS 2008 REPORT VOLUME – II ==================================== ELECTION COMMISSION OF PAKISTAN www.ecp.gov.pk INDEX CONTENTS PAGES NATIONAL ASSEMBLY OF PAKISTAN u Composition iii u Detailed Composition iv u Composition of Provincial Assemblies v u Registered Voters vi u Registered Voters, Votes Polled & Percentage vii u Summary of Statistics viii u Detailed Position of Political Parties/Alliances ix DETAILED RESULTS North West Frontier Province 3 FATAs 17 Federal Capital 27 Punjab 31 Sindh 77 Balochistan 107 u Seats Reserved for Women 115 u Seats Reserved for Non-Muslims 119 PROVINCIAL ASSEMBLIES Detailed Composition 125 PROVINCIAL ASSEMBLY PUNJAB Detailed Results General Seats 127 Seats Reserved for Women 243 Seats Reserved for Non-Muslims 247 PROVINCIAL ASSEMBLY SINDH Detailed Results u General Seats 251 u Seats Reserved for Women 307 u Seats Reserved for Non-Muslims 311 INDEX CONTENTS PAGES PROVINCIAL ASSEMBLY NWFP Detailed Results u General Seats 315 u Seats Reserved for Women 351 u Seats Reserved for Non-Muslims 355 PROVINCIAL ASSEMBLY BALOCHISTAN Detailed Results u General Seats 359 u Seats Reserved for Women 385 u Seats Reserved for Non-Muslims 389 BYE-ELECTIONS Number and Names of Constituencies u National Assembly 395 u Provincial Assemblies 396 Detailed Results u National Assembly 397 u Provincial Assemblies 399 COMPOSITION OF THE NATIONAL ASSEMBLY OF PAKISTAN 1985 – 2008 Year of General Seats Seats Total General Seats Reserved Reserved Membership Election for Non- for Women Muslims 1985 207 10 20 237 1988 207 -

Preliminary Study Parliamentary Committees

Manzil Pakistan 2013 Preliminary Research on Parliamentary Committees AUTHORS: Anum Tasleem, BBA, Institute of Business Administration Karachi Nadeem Zaidi, MBA, Greenwich University Karachi Contributors: Naheed Memon, CEO Manzil Pakistan, Visiting Faculty at IBA, MSc in Economics Birkbeck College, MBA Imperial College London Muzammal Afzaal, M.Phil, Applied Economics Research Centre Karachi Board of Directors: 1. Chairman Salim Raza, former CEO Pakistan Business Council and former Governor State Bank of Pakistan. Masters PPE, Oxford University, UK. 2. Vice Chairman Aasim Siddiqui, and Managing Director Marine Group of Companies. M.B.A Clark University, U.S.A., B.Sc. (Hons) degree in Management Sciences from London School of Economics 3. Najmuddin A. Shaikh, former Pakistani diplomat who stayed as Foreign Secretary of Pakistan from 1994 to 1997. Former Ambassador to Canada, West Germany, United States and Iran. Currently writes columns on foreign affairs and is a graduate of the Fletcher School for Diplomacy 4. Lt. Gen. (R) Syed Muhammad Amjad, joined Pakistan Army in 1965 and retired in 2002. Former Managing Director Fauji Foundation and chaired the Board of Directors of many companies of the Fauji Group 5. Ameena Saiyid OBE, is the current Managing Director of Oxford University Press in Pakistan 6. Rear Admiral (R) Hasan M. Ansari, HI(M),S.Bt.,C Eng(UK), M.I.Mech (E) retired from the Pakistan Navy after 40 years service 7. Ali J. Siddiqui, a sponsor of JS Group, one of Pakistan's largest conglomerates. CEO of the Mahvash and Jahangir Siddiqui Foundation and graduated from Cornell University with a BA in Economics 2 Manzil Pakistan is a non-partisan public policy think tank that strives to transform Pakistan into a modern and progressive nation. -

How Rich Are Pakistani Mnas December 2009

HOWHOW RICHRICH AREARE PPAKISTAKISTANIANI MNAS?MNAs? Key Points from Analysis of the Declaration of Assets Submitted by MNAs for the Years 2006-2007 and 2007-2008 PILDAT is an independent, non-partisan and not-for-profit indigenous research and training institution with the mission to strengthen democracy and democratic institutions in Pakistan. PILDAT is a registered non-profit entity under the Societies Registration Act XXI of 1860, Pakistan. Copyright ©Pakistan Institute of Legislative Development And Transparency – PILDAT All rights Reserved Printed in Pakistan First Published: December 2009 ISBN: 978-969-558-146-9 Any part of this publication can be used or cited with a clear reference to PILDAT. Pakistan Institute of Legislative Development and Transparency No. 7, 9th Avenue, F-8/1, Islamabad, Pakistan Tel: (+92-51) 111-123-345; Fax: (+92-51) 226-3078 E-mail: [email protected]; Web: www.pildat.org Abbreviations and Acronyms Foreword Executive Summary Average Value of Assets 09 Provincial Picture of Average Assets 10 Provincial Share in the Combined Value of Assets of all MNAs 11 How Political Parties Figure in the MNAs' Assets? 12 The Richest MNAs 13 The Poorest MNAs 14 The Richest and Poorest MNAs in Each Province 15 Richest Female MNAs 25 Richest and Poorest MNAs in each Party 26 Average Assets of Non-Muslim MNAs 29 MNAs Failing to Declare Assets 32 Appendix A: Constituency-wise list of MNAs along with their Assets and Rank Tables Table 1: Average Value of Assets of an MNA 2002-2008 09 Table 2: Ranking of Provinces and Territories -

Annual Report 2019 Driving Investment, Trade and the Creation of Wealth Across Asia, Africa and the Middle East

Annual Report 2019 Driving investment, trade and the creation of wealth across Asia, Africa and the Middle East. Standard Chartered Bank (Pakistan) Ltd. Points of interest Standard Chartered is proud to be operating in Pakistan as the largest and oldest international bank since 1863. 2013 marked Standard Chartered’s 150th year of presence in the country. Goal is Standard Chartered’s leading education programme that provides financial literacy, life skills and employability training to low-income adolescent girls across its footprint. Since the launch of the programme in April 2016, the Bank has reached a total of 11,196 beneficiaries in Pakistan. As a result of our Seeing is Believing projects in Pakistan, we are attributed to decreasing avoidable blindness by 20 per cent across the country. We are the only corporate partner of the Government and play a pivotal role in the National Committee of Eye Health. The largest international Bank in Pakistan with 61 branches in 11 cities and a workforce of over 2,821 employees. Standard Chartered Bank (Pakistan) Ltd. is the first international bank to get an Islamic Banking license and to open the first Islamic Banking branch in Pakistan. The Bank has total assets of over PKR 550 billion and deposits of over PKR 400 billion. In 2018, the Bank achieved its highest ever profit of PKR 18.5 billion (before tax) and is the 6th largest in terms of profitability. Strong recognition by our stakeholders 16th Annual Excellence Awards by CFA Society Awards 2019 Best medium sized Bank Best D&I Bank Runners up for Islamic Banking Window Management Association of Pakistan Awards 2019 Best Commercial Bank Global Diversity and Inclusion Benchmark Awards 2019 BestEmpowering Practices Award in Vision category Progressive Award in Benefits category Progressive Award in Communications category Progressiveentrepreneurs Award in Social Responsibility category The Banker Magazine 2019 Bestto Islamic thrive Bank Asset Triple A - Islamic Finance Awards 2019 BestNo business Loan Advisor is too small to succeed.