Living in a 1% World

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Natwest Markets N.V. Annual Report and Accounts 2020 Financial Review

NatWest Markets N.V. Annual Report and Accounts 2020 Financial Review Page Description of business Financial review NWM N.V., a licensed bank, operates as an investment banking firm serving corporates and financial institutions in the European Economic Presentation of information 2 Area (‘EEA’). NWM N.V. offers financing and risk solutions which 2 Description of business includes debt capital markets and risk management, as well as trading 2 Performance overview and flow sales that provides liquidity and risk management in rates, Impact of COVID-19 3 currencies, credit, and securitised products. NWM N.V. is based in Chairman's statement 4 Amsterdam with branches authorised in London, Dublin, Frankfurt, Summary consolidated income statement 5 Madrid, Milan, Paris and Stockholm. Consolidated balance sheet 6 On 1 January 2017, due to the balance sheet reduction, RBSH 7 Top and emerging risks Group’s regulation in the Netherlands, and supervision responsibilities, Climate-related disclosures 8 transferred from the European Central Bank (ECB), under the Single Risk and capital management 11 Supervisory Mechanism. The joint Supervisory Team comprising ECB Corporate governance 43 and De Nederlandsche Bank (DNB) conducted the day-to-day Financial statements prudential supervision oversight, back to DNB. The Netherlands Authority for the Financial Markets, Autoriteit Financiële Markten Consolidated income statement 52 (AFM), is responsible for the conduct supervision. Consolidated statement of comprehensive income 52 Consolidated balance sheet 53 UK ring-fencing legislation Consolidated statement of changes in equity 54 The UK ring-fencing legislation required the separation of essential Consolidated cash flow statement 55 banking services from investment banking services from 1 January Accounting policies 56 2019. -

Industry Analysis

Investment Banks “Teaser” Industry Report Industry Analysis Investment Banks Q1 2012 Industry Overview Raising capital by underwriting and acting on behalf of individuals, corporations, and governments in the issuance of securities is the main thrust of investment banks. They also assist companies involved in mergers and acquisitions (M&As) and provide ancillary services like market making, derivatives trading, fixed income instruments, foreign exchange, commodities, and equity securities. Investment banks bannered the 2008 global financial and economic crisis, with U.S. investment bank Bear Sterns saved by J.P. Morgan Chase. Later in the year, Lehman Brothers filed for bankruptcy due to liquidity, leverage, and losses, as Merrill Lynch narrowly escaped such a fate with its purchase by Bank of America. Lehman Brothers was the largest bankruptcy in history at the time, with liabilities of more than $600 billion. Such unprecedented events caused panic in world markets, sending bonds, equities, and other assets into a severe decline. Morgan Stanley survived with an investment from Japan-based Mitsubishi UFJ Financial Group, and Goldman Sachs took a major investment from Warren Buffet’s Berkshire Hathaway. All major financial players took large financial bailouts from the U.S. government. Post-Lehman Brothers, both American and British banks took a huge beating. In the U.K., hundreds of billions of pounds of public money was provided to support HBOS, Lloyds, and Royal Bank of Scotland (RBS). Upon the government’s pressure, Lloyds took over HBOS to create Lloyds Banking Group and after three years, taxpayers end 2011 nursing a loss on their stake of almost £40 billion ($62.4 billion). -

Sharp -V- Blank (HBOS) Judgment

Neutral Citation Number: [2019] EWHC 3078 (Ch) Case Nos: HC-2014-000292 HC-2014-001010 HC-2014-001387 HC-2014-001388 HC-2014-001389 HC-2015-000103 HC-2015-000105 IN THE HIGH COURT OF JUSTICE CHANCERY DIVISION Royal Courts of Justice Strand, London, WC2A 2LL Date: 15/11/2019 Before: SIR ALASTAIR NORRIS - - - - - - - - - - - - - - - - - - - - - Between: JOHN MICHAEL SHARP Claimants And the other Claimants listed in the GLO Register - and - (1) SIR MAURICE VICTOR BLANK Defendant (2) JOHN ERIC DANIELS (3) TIMOTHY TOOKEY (4) HELEN WEIR (5) GEORGE TRUETT TATE (6) LLOYDS BANKING GROUP PLC - - - - - - - - - - - - - - - - - - - - - Richard Hill QC, Sebastian Isaac, Jack Rivett and Lara Hassell-Hart (instructed by Harcus Sinclair UK Limited) for the Claimants Helen Davies QC, Tony Singla and Kyle Lawson (instructed by Herbert Smith Freehills LLP) for the Defendants Hearing dates: 17-20, 23-27, 30-31 October 2017; 1-2, 6-9, 13-17,20, 22-23, 27, 29-30 November 2017, 1, 11-15, 18-21 December 2017, 12, 16-19, 22-26, 29-31 January 2018, 1-2, 5- 6, 8, 28 February 2018, 1-2 and 5 March 2018 - - - - - - - - - - - - - - - - - - - - - Approved Judgment I direct that pursuant to CPR PD 39A para 6.1 no official shorthand note shall be taken of this Judgment and that copies of this version as handed down may be treated as authentic. ............................. INDEX: The task in hand 1 The landscape in broad strokes 8 The claim in outline. 29 The legal basis for the claim 41 The factual witnesses. 43 The expert witnesses 59 The facts: the emerging financial -

Lloyds TSB/HBOS Transaction Customers Will See Greater Continuity of HBOS Products, Services and Brands Than Would Otherwise Be the Case

Anticipated acquisition by Lloyds TSB plc of HBOS plc Report to the Secretary of State for Business Enterprise and Regulatory Reform 24 October 2008 Contents I OVERVIEW ................................................................................................ 4 Conclusions ............................................................................................... 4 Merger jurisdiction ...................................................................................... 5 Substantive competition assessment ............................................................. 5 Remedies................................................................................................... 7 Public interest consideration ......................................................................... 7 II PROCEDURAL OVERVIEW ........................................................................... 8 III PARTIES AND TRANSACTION.....................................................................10 The parties................................................................................................10 Transaction rationale ..................................................................................10 IV JURISDICTION AND LEGAL TEST ................................................................11 V THE COUNTERFACTUAL ............................................................................13 Introduction to the OFT's general approach to the counterfactual.....................13 The appropriate counterfactual in this case ...................................................14 -

Rating Action, Barclays Bank UK

Rating Action: Moody's takes rating actions on Barclays, Lloyds, Santander UK, Nationwide and Close Brothers, following update to banks methodology 13 Jul 2021 London, 13 July 2021 -- Moody's Investors Service (Moody's) has today taken rating actions on Barclays, Lloyds, Santander UK and Close Brothers banking groups and on Nationwide Building Society, including the upgrade of the long-term senior ratings of Lloyds Banking Group plc and Close Brothers Group plc. The rating actions were driven by revisions to Moody's Advanced Loss Given Failure (Advanced LGF) framework, which is applied to banks operating in jurisdictions with Operational Resolution Regimes, following the publication of Moody's updated Banks Methodology on 9 July 2021. This methodology is available at this link: https://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBC_1269625 . A full list of affected ratings and assessments can be found at the end of this Press Release. RATINGS RATIONALE Today's rating actions were driven by revisions to the Advanced Loss Given Failure framework within Moody's updated Banks Methodology: a revised notching guidance table, with thresholds at lower levels of subordination and volume in the liability structure have been applied to the UK banks and Additional Tier 1 (AT1) securities issued by banks domiciled in the UK have been included in the Advanced LGF framework, eliminating the previous analytical distinction between those high trigger instruments that were deemed to provide equity-like absorption of losses before the point of failure and other AT1 securities. Moody's removal of equity credit for high trigger Additional Tier 1 (AT1) instruments from banks' going concern capital means that affected banks have reduced capacity to absorb unexpected losses before the point of failure, everything else being equal. -

The FRC's Enquiries and Investigation of KPMG's 2007 and 2008 Audits Of

Report Professional discipline Financial Reporting Council November 2017 The FRC’s enquiries and investigation of KPMG’s 2007 and 2008 audits of HBOS The FRC’s mission is to promote transparency and integrity in business. The FRC sets the UK Corporate Governance and Stewardship Codes and UK standards for accounting and actuarial work; monitors and takes action to promote the quality of corporate reporting; and operates independent enforcement arrangements for accountants and actuaries. As the Competent Authority for audit in the UK the FRC sets auditing and ethical standards and monitors and enforces audit quality. The FRC does not accept any liability to any party for any loss, damage or costs howsoever arising, whether directly or indirectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this document or arising from any omission from it. © The Financial Reporting Council Limited 2017 The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number 2486368. Registered Offi ce: 8th Floor, 125 London Wall, London EC2Y 5AS Contents Page 1 Executive Summary ........................................................................................................ 3 2 Summary Background: HBOS and the contemporaneous banking and financial conditions ........................................................................................................................ 6 3 Accounting Requirements and Auditing -

The Royal Bank of Scotland Group Plc

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt as to the action you should take, you are recommended to seek your own ®nancial advice immediately from your stockbroker, bank manager, solicitor, accountant or other independent ®nancial adviser duly authorised under the Financial Services Act 1986 if you are resident in the United Kingdom, or, if not, from another appropriately authorised independent ®nancial adviser. This document is being sent for information only to option holders. If you have sold or otherwise transferred or sell or otherwise transfer on or before 20 June 2000 all your Ordinary Shares, 11% Cumulative Preference Shares or 51¤2% Cumulative Preference Shares, please forward this document and the accompanying documents immediately to the purchaser or transferee, or to the bank, stockbroker or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. If you sell your Ordinary Shares prior to 20 June 2000 and are not on the register of members as at that date, any Selling Facility Form returned by you will be of no effect. Your attention is drawn to the letter from the Chairman of The Royal Bank of Scotland Group plc set out in Part 1 of this document, which contains a recommendation by your Board to vote in favour of the resolutions to be proposed at the Extraordinary General Meeting referred to below. The Royal Bank of Scotland Group plc (incorporated in Scotland under the Companies Acts 1948 to 1980 with registered number 45551) CIRCULAR TO SHAREHOLDERS and Notice of Extraordinary General Meeting Notice of an Extraordinary General Meeting of The Royal Bank of Scotland Group plc to be held at 11.00 a.m. -

Disclaimer - Important

DISCLAIMER - IMPORTANT Recommended acquisition of HBOS plc (“HBOS”) by Lloyds TSB Group plc (“Lloyds TSB”) (the “Acquisition”) NOTE: AN ELECTRONIC VERSION OF THE ANNOUNCEMENT IS BEING MADE AVAILABLE ON THIS WEBSITE BY LLOYDS TSB IN GOOD FAITH AND FOR INFORMATION PURPOSES ONLY. Access to the Announcement Please read this notice carefully - it applies to all persons who view this part of the website and, depending upon who you are and where you live, it may affect your rights. For regulatory reasons, we have to ensure you are aware of the appropriate regulations for the country which you are in. By viewing this announcement you agree to comply/be bound by the terms of this disclaimer. Overseas Persons The availability of the Acquisition to persons who are not resident in the United Kingdom may be affected by the laws of the relevant jurisdictions in which they are located. Persons who are not resident in the United Kingdom should inform themselves of, and observe, any applicable requirements. Forward looking statements This document includes certain “forward looking statements” with respect to the business, strategy and plans of Lloyds TSB Group and HBOS and their respective expectations relating to the Acquisition and their future financial condition and performance. Statements that are not historical facts, including statements about Lloyds TSB Group’s or HBOS’s or their respective management’s beliefs and expectations, are forward looking statements. Words such as “believes”, “anticipates”, “estimates”, “expects”, “intends”, “aims”, “potential”, “will”, “would”, “could”, “considered”, “likely”, “estimate” and variations of these words and similar future or conditional expressions are intended to identify forward looking statements but are not the exclusive means of identifying such statements. -

The Humbling of the Scottish Banking Industry During the Financial Crisis: Hybris, Financialization and Some Aristotelian Responses

THE HUMBLING OF THE SCOTTISH BANKING INDUSTRY DURING THE FINANCIAL CRISIS: HYBRIS, FINANCIALIZATION AND SOME ARISTOTELIAN RESPONSES. OWEN KELLY, UNIVERSITY OF EDINBURGH Influencing the world since 1583 OUTLINE • Summarize facts of the cases • The climate of financialization • Hybris and hubris – differing conceptions • Aristotle • Conclusions BANK OF SCOTLAND (HBOS) • Formed from Halifax Building Society and Bank of Scotland – a 'mutual' lost to the economy • Sales culture • Financial markets and trading dominate • Excessive pay (like whole sector) • Bad banking practice • Bailout cost £30 billion and a degree of nationalisation • Taken over by Lloyds – Bank of Scotland exists as subsidiary • Investigation damning but no prosecutions ROYAL BANK OF SCOTLAND (RBS) • Aggressive expansion in UK, taking over other banks • Rapid international growth • "An international bank that happens to be based in Scotland" • Biggest bank in the world! • Bad banking practice • Bailout cost £46 billion and a form of nationalisation • No prosecutions • Legal cases and public ownership continue FINANCIALIZATION • "...the substitution of trading and transactions for relationships...the restructuring of finance businesses.....broader economic effects on stability and inequality......[linked to] market fundamentalism....the exaltation of the role of the trader" (Kay, 2015) • Relationships: Gemeinschaft to Gesellschaft • Restructuring – move away from mutuals and partnerships • Risk becomes financialized and 'managed' • Exchange value dominates Fisher's 'misinterpretation' -

Lender of Last Resort Operations During the Financial Crisis: Seven Practical Lessons from the United Kingdom

Lender of last resort operations during the financial crisis: seven practical lessons from the United Kingdom Andrew Hauser1 Abstract Drawing on the recommendations of the many public reviews of the UK’s experience with lender of last resort (LOLR) operations during the financial crisis, this paper identifies seven practical lessons of wider interest to the central banking community and others. First, lender of last resort operations cannot tackle moral hazard single-handedly: effective alignment of incentives also requires strong microprudential liquid asset requirements and a credible bank resolution regime. Second, the lender of last resort must have a close understanding of the firms to which it might lend, the markets in which they operate and the collateral they have available. Third, ambiguity over the circumstances and terms of LOLR operations may not be as constructive as previously thought: it does not appear to have been effective in limiting moral hazard pre-crisis in the UK, and led to excessive swings in market expectations about the Bank’s willingness to lend. Fourth, as a result, the UK has concluded that the LOLR regime should be richly specified, and embedded in a largely public framework. Fifth, central banks should only lend to solvent institutions – but as a practical matter, illiquidity and insolvency can be hard to distinguish in the midst of a crisis. That requires careful definition of the respective responsibilities of the central bank and the fiscal authority. Sixth, central banks should do all they can to reduce unnecessary stigma associated with their LOLR facilities, whilst recognising that some level of stigma is probably unavoidable. -

Download Pdf File of RBS Group Annual Report 2007

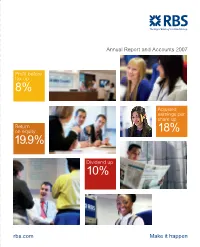

Annual Report and Accounts 2007 Profit before tax up 8% Adjusted earnings per share up Return on equity 18% 19.9% Dividend up 10% rbs.com Make it happen Highlights 2007 Contents Group operating profit up 9% 02 Measuring our success 04 Group profile to £10.3 billion 06 Divisional profile 08 Chairman’s statement 10 Group Chief Executive’s review Profit after tax up 19% to £7.7 billion Adjusted earnings per ordinary Divisional review share up 18% to 78.7p 13 Corporate Markets 15 Retail Markets 17 Ulster Bank 18 Citizens Total dividend up 10% to 33.2p 19 RBS Insurance 20 Manufacturing 21 ABN AMRO Tier 1 capital ratio 7.3% Total capital ratio 11.2% Corporate Responsibility 22 Combating crime 22 Building financial capability 23 Promoting financial inclusion 24 Customer service 24 Citizens in the community 25 Our employees 25 RBS and the environment Report and accounts 27 Business review 91 Governance 117 Financial statements 213 Additional information 235 Shareholder information RBS Group • Annual Report and Accounts 2007 01 Measuring our success Focus on growth and efficiency Income Adjusted cost:income ratio Group operating profit* (£m) (%) (£m) 07 31,115 07 43.9 07 10,282 06 28,002 06 42.1 06 9,414 05 25,569 05 42.4 05 8,251 04 22,515 pro forma 04 42.0 pro forma 04 7,108 pro forma The Group’s total income grew by 11% The Group’s cost:income ratio was 43.9%. Excluding ABN AMRO, Group operating profit increased by 9% to to £31,115 million in 2007. -

Living in a 1% World

LivingLiving inin aa 1%1% WorldWorld FredFred GoodwinGoodwin GroupGroup ChiefChief ExecutiveExecutive Slide 2 Living in a 1% World 1% World Stakeholder pensions Sandler regulated products Slide 3 Living in a 1% World Implications for RBS Lower margins on long term savings Less than 1% of RBS income from long term savings Higher volumes of distribution of long term savings Simpler products, processes better for bank distribution Slide 4 Living in a 1% World What are the required characteristics for growth? Slide 5 Required Characteristics for Growth Organic growth – Large distribution capacity – Multiple brands – Low market shares – Effective sales processes – Able to grow new businesses – Diversity of income Acquisitions – Able to make good acquisitions – Good at integration of acquisitions Efficiency – Able to improve efficiency Slide 6 Large Distribution Capacity Distribution Channels UK Ranking Branches #1 Supermarkets #1 Telephone #1 = Internet #? (large) ATMs #1 Relationship Managers #1 Source: Company Accounts, CACI and Link Slide 7 Multiple Brands Multi-Brand, Multiple Channel Strategy Slide 8 Multiple Brands Multi-Brand, Multiple Channel Strategy Appeals to different customer groups Allows different product variants, pricing Gives flexibility for future Allows management autonomy Slide 9 Low Market Shares UK Market Shares Total RBS Current accounts 21% Savings accounts 8% Personal loans 10% Mortgages 5% Credit cards 17% Life insurance 2% Motor insurance 16%* Home insurance 13%* Small business relationships 30%