Zee Entertainment Enterprise (ZEETEL)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ZEEMEDIA [email protected]

ZEEMEDIA [email protected] Collaborative Strategies C o h e s i v e G r o w t h ZEEMEDIA ZEE MEDIA CORPORATION LIMITED REGISTERED OFFICE 14th Floor, A Wing, Marathon Futurex, NM Joshi Marg, Lower Parel, Mumbai - 400013 Maharashtra Tel.: +91 22 7106 1234 Fax: +91 22 2300 2107 Website: www.zeenews.india.com Annual Report 2017-18 OUR ZEEMEDIA PRESENCE INSIDE THIS REPORT Corporate Overview Collaborative Strategies Cohesive Growth 01 Growing Together with Viewer Engagement 02 Growing Together with Advertisers' Reach 03 Growing Together with Society and Government 04 Growing Together with Our Employees - Our Trusted Aides 05 Srinagar Steadfast Progress, Nurturing New Ventures 06 Jammu Raising the Bar with Innovations 08 Message to Shareholders 10 Growth Firmly Embedded in Value System 12 Chandigarh Dehradun Our Channels and Digital Platforms 13 Corporate Information 16 Noida STATUTORY REPORTS Lucknow Varanasi Notice 17 Jaipur Ajmer Directors' Report 26 Patna Corporate Governance Report 43 Kota Management Discussion and Analysis 56 Ranchi Kolkata Ahmedabad Bhopal Indore Vadodara FINANCIAL STATEMENTS Rajkot Raipur Surat Standalone Financial Statements 67 Nagpur Consolidated Financial Statements 121 Bhubaneswar Nasik Aurangabad Thane Mumbai BSE, Mumbai Pune Kohlapur Hyderabad FORWARD LOOKING STATEMENTS Bengaluru Certain statements in this annual report concerning our future growth prospects are forward-looking statements, which involve a number of risks and uncertainties that could cause actual results to differ materially from those in such forward-looking statements. We have tried wherever possible to identify such statements by using words such as 'anticipate', 'estimate', 'expect', 'project', 'intend', 'plan', 'believe' and words of similar substance in connection with any discussion of future performance. -

SL.NO CHANNEL LCN Genre STAR PLUS 101 HINDI GEC

SL.NO CHANNEL LCN Genre 1 STAR PLUS 101 HINDI GEC PAY 2 ZEE TV 102 HINDI GEC PAY 3 SET 103 HINDI GEC PAY 4 COLORS 104 HINDI GEC PAY 5 &TV 105 HINDI GEC PAY 6 SAB 106 HINDI GEC PAY 7 STAR BHARAT 107 HINDI GEC PAY 8 BIG MAGIC 108 HINDI GEC PAY 9 PAL 109 HINDI GEC PAY 10 COLORS RISHTEY 110 HINDI GEC PAY 11 STAR UTSAV 111 HINDI GEC PAY 12 ZEE ANMOL 112 HINDI GEC PAY 13 BINDASS 113 HINDI GEC PAY 14 ZOOM 114 HINDI GEC PAY 15 DISCOVERY JEET 115 HINDI GEC PAY 16 STAR GOLD 135 HINDI MOVIES PAY 17 ZEE CINEMA 136 HINDI MOVIES PAY 18 SONY MAX 137 HINDI MOVIES PAY 19 &PICTURES 138 HINDI MOVIES PAY 20 STAR GOLD 2 139 HINDI MOVIES PAY 21 ZEE BOLLYWOOD 140 HINDI MOVIES PAY 22 MAX 2 141 HINDI MOVIES PAY 23 ZEE ACTION 142 HINDI MOVIES PAY 24 SONY WAH 143 HINDI MOVIES PAY 25 COLORS CINEPLEX 144 HINDI MOVIES PAY 26 UTV MOVIES 145 HINDI MOVIES PAY 27 UTV ACTION 146 HINDI MOVIES PAY 28 ZEE CLASSIC 147 HINDI MOVIES PAY 29 ZEE ANMOL CINEMA 148 HINDI MOVIES PAY 30 STAR GOLD SELECT 149 HINDI MOVIES PAY 31 STAR UTSAV MOVIES 150 HINDI MOVIES PAY 32 RISHTEY CINEPLEX 151 HINDI MOVIES PAY 33 MTV 175 HINDI MUSIC PAY 34 ZING 178 HINDI MUSIC PAY 35 MTV BEATS 179 HINDI MUSIC PAY 36 9X M 181 HINDI MUSIC PAY 37 CNBC AWAAZ 201 HINDI NEWS PAY 38 ZEE BUSINESS 202 HINDI NEWS PAY 39 INDIA TODAY 203 HINDI NEWS PAY 40 NDTV INDIA 204 HINDI NEWS PAY 41 NEWS18 INDIA 205 HINDI NEWS PAY 42 AAJ TAK 206 HINDI NEWS PAY 43 ZEE NEWS 207 HINDI NEWS PAY 44 ZEE HINDUSTAN 209 HINDI NEWS PAY 45 TEZ 210 HINDI NEWS PAY 46 STAR JALSHA 251 BENGALI GEC PAY 47 ZEE BANGLA 252 BENGALI GEC PAY 48 COLORS -

Declaration Under Section 4 (4) of the Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable System) Regulation, 2017 (No

Version 1.0/2019 Declaration Under Section 4 (4) of The Telecommunication (Broadcasting and Cable) Services Interconnection (Addressable System) Regulation, 2017 (No. 1 of 2017) 4(4)a: Target Market Distribution Network Location States/Parts of State covered as "Coverage Area" Bangalore Karnataka Bhopal Madhya Pradesh Delhi Delhi; Haryana; Rajasthan and Uttar Pradesh Hyderabad Telangana Kolkata Odisha; West Bengal; Sikkim Mumbai Maharashtra 4(4)b: Total Channel carrying capacity Distribution Network Location Capacity in SD Terms Bangalore 506 Bhopal 358 Delhi 384 Hyderabad 456 Kolkata 472 Mumbai 447 Kindly Note: 1. Local Channels considered as 1 SD; 2. Consideration in SD Terms is clarified as 1 SD = 1 SD; 1 HD = 2 SD; 3. Number of channels will vary within the area serviced by a distribution network location depending upon available Bandwidth capacity. 4(4)c: List of channels available on network List attached below in Annexure I 4(4)d: Number of channels which signals of television channels have been requested by the distributor from broadcasters and the interconnection agreements signed Nil Page 1 of 37 Version 1.0/2019 4(4)e: Spare channels capacity available on the network for the purpose of carrying signals of television channels Distribution Network Location Spare Channel Capacity in SD Terms Bangalore Nil Bhopal Nil Delhi Nil Hyderabad Nil Kolkata Nil Mumbai Nil 4(4)f: List of channels, in chronological order, for which requests have been received from broadcasters for distribution of their channels, the interconnection agreements -

Dog Flu Strikes Palo Alto Area Page 5

Palo Vol. XXXIX, Number 18 Q February 2, 2018 Alto Dog flu strikes Palo Alto area Page 5 www.PaloAltoOnline.comw w w. P a l o A l t o O n l i n e. c o m In a fix Rising construction costs create high anxiety for city of Palo Alto Page 24 INSIDE THIS ISSUE Pulse 11 Spectrum 12 Transitions 14 Movies 30 Home 35 Puzzles 43 QArts Songwriter, playwright Stew takes on messy heroes Page 29 QSeniors VA studies connect exercise and the brain Page 31 QSports M-A favored in CCS girls wrestling tournament Page 45 TOO MAJOR TOO MINOR JUST RIGHT FOR HOME FOR HOSPITAL FOR STANFORD EXPRESS CARE When an injury or illness needs quick attention but not Express Care is available at two convenient locations: in the Emergency Department, call Stanford Express Care. Staffed by doctors, nurses, and physician assistants, Stanford Express Care Palo Alto Hoover Pavilion Express Care treats children (6+ months) and adults for: 211 Quarry Road, Suite 102 Palo Alto, CA 94304 • Respiratory illnesses • UTIs (urinary tract tel: 650.736.5211 • Cold and flu infections) Stanford Express Care San Jose • Stomach pain • Pregnancy tests River View Apartment Homes • Fever and headache • Flu shots 52 Skytop Street, Suite 10 San Jose, CA 95134 • Back pain • Throat cultures tel: 669.294.8888 • Cuts and sprains Open Everyday by Appointment Only Express Care accepts most insurance and is billed as 9:00am–9:00pm a primary care, not emergency care, appointment. Providing same-day fixes every day, 9:00am to 9:00pm. -

List of Permitted Private Satellite TV Channels As on 31-01-2015

List of Permitted Private Satellite TV Channels as on 31-01-2015 Sr. No. Channel Name Name of the Company Category Upliniking/Downlinkin/ Language Date of Uplinking Only Permission 1 9X 9X MEDIA PRIVATE LIMITED NON-NEWS UPLINKING HINDI 24/09/2007 2 9XM 9X MEDIA PRIVATE LIMITED NON-NEWS UPLINKING HINDI/ENGLISH 24/09/2007 3 9XO (9XM VELNET) 9X MEDIA PRIVATE LIMITED NON-NEWS UPLINKING HINDI 29/09/2011 4 9X JHAKAAS (9X MARATHI) 9X MEDIA PRIVATE LIMITED NON-NEWS UPLINKING MARATHI 29/09/2011 5 9X JALWA (PHIR SE 9X) 9X MEDIA PRIVATE LIMITED NON-NEWS UPLINKING HINDI 29/09/2011 6 9X BANGLA 9X MEDIA PRIVATE LIMITED NON-NEWS UPLINKING BENGALI 17-01-15 7 TV 24 A ONE NEWS TIME BROADCASTING NEWS UPLINKING HINDI/ PUNJABI/ ENGLISH 21/10/2008 PRIVATE LIMITED 8 AP 9 (earlier AR NEWS) A.R. RAIL VIKAS SERVICES PVT. LTD. NEWS UPLINKING HINDI, ENGLISH, MARATHI 14/10/2011 AND ALL OTHER INDIAN SCHEDULE LANGUAGE 9 SATYA A.R. RAIL VIKAS SERVICES PVT. LTD. NON-NEWS UPLINKING HINDI, ENGLISH, MARATHI 14/10/2011 AND ALL OTHER INDIAN SCHEDULE LANGUAGE 10 AADRI ENRICH AADRI ENTERTAINMENT AND MEDIA NON-NEWS UPLINKING TELUGU/HINDI/ENGLISH/GU 22/11/2011 WORKS PVT.LTD. JARATI/TAMIL/KANNADA/B ENGALI/MALAYALAM 11 AADRI WELLNESS AADRI ENTERTAINMENT AND MEDIA NON-NEWS UPLINKING TELUGU/HINDI/ENGLISH/GU 22/11/2011 WORKS PVT.LTD. JARATI/TAMIL/KANNADA/B 12 ABN-ANDHRA JYOTHI AAMODA BROADCASTING COMPANY NEWS UPLINKING TELUGUENGALI/MALAYALAM 30/06/2009 PRIVATE LIMITED 13 ANJAN TV AAP MEDIA PVT.LTD. -

Extraordinary Together

Experience the Extraordinary ANNUAL REPORT 2017-18 ZEE ENTERTAINMENT ENTERPRISES LIMITED WELCOME TO THE EXTRAORDINARY WORLD OF ZEE! The journey of a thousand miles begins with one step. We took our first Our new brand ideology – ‘Extraordinary Together’, celebrates our step 25 years back with a simple idea - create stories that entertain, belief in the power of working together, that we’re greater than the inspire, and touch hearts. We started small but success fuelled our sum of our parts and from collaboration comes the strength to deliver desires, dreams and ambitions. As we moved ahead, the goals became the exceptional. Our mission to create extraordinary entertainment more audacious and we challenged ourselves to do more. We achieved experiences for our audience could not have been achieved without milestones which were not visible at the beginning and looked the support of our employees, partners and peers, who had the faith impossible even as we progressed. True to the saying, ‘A dream you in our vision and walked alongside us. At the cusp of our dream alone is only a dream, a dream you dream together is reality’, 25th anniversary, we reaffirm our commitment to work tirelessly with our vision materialised only because it was shared by our partners and each of them, to create new benchmarks and deliver the extraordinary. peers. Today, our 1.3 billion strong audience in 170+ countries is a result Mosaic, an art-form made of innumerable elements, each of which is of not only our relentless efforts but also of the countless others who vital to the picture that emerges when they all come together, is thus supported us on the way. -

A New Vision Is Blooming

A NEW VISION IS BLOOMING ZEE 4.0 - ANNUAL REPORT 2020-21 Zee Entertainment Enterprises Limited Transformation stems from the natural evolution of every living being. Inside each of us lies a distinctive desire to do something more than the norm, out of the ordinary. This nature of existence flows from people to businesses, leading them from old path to new, creating opportunities for themselves and for the rest of the world. Media and Entertainment landscape is not untouched by this phenomenon. From consumer FINANCIAL behaviour to consumer experiences, the industry has evolved in all shapes and forms over STATEMENTS the last few decades. Today, we are seeing a paradigm shift in the consumption and delivery 03 of entertainment. In this new realm, the alchemy of the consumer experience is one that blends content creation, delivery, and monetization in a seamless manner. This hyper- STANDALONE competitive, digitally accelerated environment demands a unique strategic vision. We at ZEE INDEX Independent Auditor’s Report 107 are preparing to step into this future with a sharper and synergised version, transforming into ZEE 4.0 - a future-ready organisation to gain competitive advantage. ZEE 4.0 is Balance Sheet 115 designed around enhanced customer centricity with levers for capitalizing on Statement of Profit and Loss 116 immense growth opportunities and driving higher profitability. COMPANY Statement of Cash Flow 117 OVERVIEW The 5G pillars - Governance, Granularity, Growth, Goodwill and Gusto, form 01 Statement of Changes in Equity 119 the cornerstone of ZEE 4.0, sharpening our abilities to capture the emerging Notes 121 opportunities across markets, to transform ZEE into South Asia’s leading Media & Key Performance Indicators 04 STATUTORY Entertainment Company. -

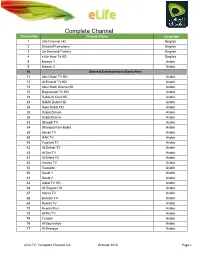

Complete Channel List October 2015 Page 1

Complete Channel Channel No. List Channel Name Language 1 Info Channel HD English 2 Etisalat Promotions English 3 On Demand Trailers English 4 eLife How-To HD English 8 Mosaic 1 Arabic 9 Mosaic 2 Arabic 10 General Entertainment Starts Here 11 Abu Dhabi TV HD Arabic 12 Al Emarat TV HD Arabic 13 Abu Dhabi Drama HD Arabic 15 Baynounah TV HD Arabic 22 Dubai Al Oula HD Arabic 23 SAMA Dubai HD Arabic 24 Noor Dubai HD Arabic 25 Dubai Zaman Arabic 26 Dubai Drama Arabic 33 Sharjah TV Arabic 34 Sharqiya from Kalba Arabic 38 Ajman TV Arabic 39 RAK TV Arabic 40 Fujairah TV Arabic 42 Al Dafrah TV Arabic 43 Al Dar TV Arabic 51 Al Waha TV Arabic 52 Hawas TV Arabic 53 Tawazon Arabic 60 Saudi 1 Arabic 61 Saudi 2 Arabic 63 Qatar TV HD Arabic 64 Al Rayyan HD Arabic 67 Oman TV Arabic 68 Bahrain TV Arabic 69 Kuwait TV Arabic 70 Kuwait Plus Arabic 73 Al Rai TV Arabic 74 Funoon Arabic 76 Al Soumariya Arabic 77 Al Sharqiya Arabic eLife TV : Complete Channel List October 2015 Page 1 Complete Channel 79 LBC Sat List Arabic 80 OTV Arabic 81 LDC Arabic 82 Future TV Arabic 83 Tele Liban Arabic 84 MTV Lebanon Arabic 85 NBN Arabic 86 Al Jadeed Arabic 89 Jordan TV Arabic 91 Palestine Arabic 92 Syria TV Arabic 94 Al Masriya Arabic 95 Al Kahera Wal Nass Arabic 96 Al Kahera Wal Nass +2 Arabic 97 ON TV Arabic 98 ON TV Live Arabic 101 CBC Arabic 102 CBC Extra Arabic 103 CBC Drama Arabic 104 Al Hayat Arabic 105 Al Hayat 2 Arabic 106 Al Hayat Musalsalat Arabic 108 Al Nahar TV Arabic 109 Al Nahar TV +2 Arabic 110 Al Nahar Drama Arabic 112 Sada Al Balad Arabic 113 Sada Al Balad -

Btn Platinum 460 With

BTN PLATINUM 460 WITH GST DD-National DD Podhigai NAGORIK TV HD ZEE TV ZING DD-News AIR Punjabi I Plus Tv &TV ZEE SALAM INDIA NEWS DD Kohima STAR TV BANGLA ZEE ANMOL ZEE BANGLA DD-Bharti DD Saptgiri DILLAGIII BIC MAGIC ZEE BANGLA CINEMA Chardikla Time TV FM Gold Delhi Movie Plus ZEE CINEMA ZEE BOLLYWOOD AASTHA BHAJAN AIR Hindi Balle Balle Non-Stop Music & PPICTURE LIVING FOODZ SANSKAR AIR NE Multiplex ZEE ACTION ZEE HINDUSTAN MAHA MOVIE Rainbow Mumbai PEACE OF MIND ZEE NEWS 24 GHANTA SAHARA ONE EZ MALL Mtunes ZEE BUSINESS ZEE ANMOL CINEMA BIG MAGIC Wow Cinema WOW ZEE ETC ABP NEWS Sahara MUM Box Cinema 9XM Sahara NAT First India SONY AATH SONY WAH AASTHA FASHIONTV HD MADANI TV BANGLA SONY YAY AXN ZEE HINDUSTAN FIRANGI TV 100 SET MAX SONY PIX DD MARATI Cinema TV Kaatyayani SET MAX 2 SONY SIX 9XO NEWS TIME AASAM Paras Gold SONY MIX SONY ESPN NEWS STATE FASHIONTV India T TV SONY SAB TEN 1 DD NEWS Arihant ASIAN TV SONY TV TEN 2 MASTI 24 Ghanta PTC NEWS SONY PAL TEN 3 ALAMI SAHARA 9X JALWA PTC PUNJABI BBC EARTH DD Oriya SUDARSHAN TV PTC CHAK DE DD Punjabi TV9 Bharatvarsh PTC PUNJABI GOLD STAR PLUS JALSHA MOVIES DD North East R PLUS INDIASIGN TEST STAR GOLD STAR GOLD SELECT Sahara UP Show Box PRAG NEWS STAR MOVIES STAR SPORTS 1 DD Yadagiri DD INDIA NEWS STATE MP CHG STAR WORLD STAR SPORTS 2 DD KISAN RANG NEWS STATE UP UK FOX LIFE STAR SPORTS 3 DD CHANDANA BOISAKHI TV OSCAR MOVIES BHOJPURI STAR JALSHA STAR SPORTS 1HINDI Lok Sabha SWAYAM CHATTAGRAM NGC STAR SPORTS SELECT 1 RSTV NEWS LIVE DHIPTO NGC WILD STAR SPORTS SELECT 2 DANGAL INDIA TV R TV -

HELPING India Achieve Its POTENTIAL

HELPING India achieve its POTENTIAL Annual Report 2012-13 We nurture the unique potential Zee Learn Ltd. is a leading education company, founded with the purpose of ‘Improving Human Capital’. The company has contributed in the field of education across age groups, all the while maintaining its core values of integrity, ownership, leadership, trust and continuous learning. We believe that every child has a unique and infinite potential and we are committed to help children realize their capabilities. Under its portfolio, Zee Learn has over 1250 centres of the leading preschool chain in India, Kidzee, educating over 270,000 children over the years. With over 135 K-12 schools already signed under franchise network and the endeavours of our skilled professionals and academicians we have created the fastest growing chain of schools in India–Mount Litera Zee School (MLZS). With the ever- growing need for premium preschool education, Zee Learn has also initiated Mount Litera World Pre School in its brand portfolio. of children to improve the human capital of our country Capitalising on our experience of running high-performance schools, we have branched out in providing school management services to 6 schools under MLZS. For subject and skill-specific interventions in schools, we provide a curriculum-mapped activity-based science program called Braincafé Science to 95 schools across India. In FY13 Zee Learn also started providing educational content and management services to India’s first edutainment TV channel for children, ‘ZeeQ’. The youth is looking to explore vocational courses outside the traditional curriculum. Zee Institute of Media Arts (ZIMA) provides diploma courses in TV and film making courses and Zee Institute of Creative Art (ZICA) is India’s first full-fledged institute providing diploma courses in 2D and 3D animation, widespread across the country with 31 centres spread across 16 cities in India. -

Hindi Movie Cluster Niche Channels

ANNUAL REPORT 2016-17 A TO ZEE OF CONTENT LEADERSHIP CORPORATE OVERVIEW STATUTORY REPORTS 01 02 ZEEL At A Glance 02 46 Management Discussion And Analysis 04 Events And Milestones 66 Notice 06 Message From The Chairman 70 Directors’ Report 08 Key Performance Indicators 76 Annexures to Directors’ Report 10 Message From The MD & CEO 88 Secretarial Audit Report 12 All You Can See 90 Report on Corporate Governance 14 We Speak Your Language 104 Business Responsibility Report 16 We Are Where You Want To Be 109 Certification of Financial Statements 18 All The World Is A Stage 20 More. Much More Than TV. 22 Business Overview FINANCIAL STATEMENTS 30 Strategy For Sustainable Growth 03 STANDALONE 32 Q&A With Amit Goenka - CEO (International Business) 110 Independent Auditor’s Report 34 Q&A With Chief Finance and Strategy Officer 114 Balance Sheet 36 Board Of Directors 115 Statement of Profit and Loss 38 Leading With People 116 Statement of Changes in Equity 40 Leading With Thought. Growing Through Engagement 117 Statement of Cash Flow 42 Corporate Social Responsibility 119 Notes 43 Caring For The Environment 162 Last Five Years Financial Highlights 44 Corporate Information 163 Performance Ratios - An Analysis CONSOLIDATED 164 Independent Auditor’s Report 168 Balance Sheet 169 Statement of Profit and Loss 170 Statement of Changes in Equity 171 Statement of Cash Flow 173 Notes ATTENDANCE SLIP & ROUTE MAP FOR VENUE OF AGM PROXY FORM ON THE COVER Forward-looking statement In this Annual Report, we have disclosed forward-looking information to enable investors to comprehend our A TO ZEE OF CONTENT prospects and take investment decisions. -

Page 01 Sept 11.Indd

THURSDAY 11 SEPTEMBER 2014 • [email protected] • www.thepeninsulaqatar.com • 4455 7741 Pulling the plug: inside Apple’s Watch a CAMPUS • Qatar Academy boost for wireless teachers begin school year on ‘positive’ note charging P | 4 P | 12 FOOD • 10 fresh ways to use butternut squash The 60th anniversary edition of the Guinness World Records book will reflect on six decades of record-breaking, while P | 6 also featuring the latest additions to the oddball hall of fame like long tongues and leaping cats. BOOKS • What neuroscience tells us about getting organised P | 7 FILM • Whiff of humour permeates Jon Stewart debut drama Rosewater P | 8-9 HEALTH • Reversing the deadly effects of sitting too long P | 11 LEARN ARABIC WORLD • Learn commonly used Arabic words RECORDS and their meanings P | 13 2 PLUS | THURSDAY 11 SEPTEMBER 2014 COVER STORY Long tongues and leaping cats in 60th World Records book Alley secured her place in World Records book for the longest jump by a cat. rom super-long tongues Bennett, who started collecting in to leaping cats, a host of 1995. weird and wacky land- In Japan, Akiko Obata has the Fmarks have made the cut largest collection of plastic food, for 60th anniversary edition of with more than 8,000 items includ- the Guinness World Records book ing giant plastic burgers, donuts launched yesterday. and dishes of everything from soup The new edition reflects on six to desserts filling her apartment. decades of record-breaking, while Meanwhile Alley of the United also featuring the latest additions States takes the longest jump by to the oddball hall of fame.